Drive Your Dreams: The Ultimate Guide to Securing an NGF CU Car Loan

Drive Your Dreams: The Ultimate Guide to Securing an NGF CU Car Loan Carloan.Guidemechanic.com

Purchasing a new vehicle is often more than just a transaction; it’s an investment in freedom, convenience, and a significant life milestone. Whether you’re eyeing that sleek new sedan, a reliable family SUV, or a rugged pickup truck, the path to ownership frequently involves securing a car loan. For many, navigating the world of auto financing can feel overwhelming, with countless options and jargon.

This is where understanding your choices, especially from a trusted financial partner like a credit union, becomes invaluable. Today, we’re going to embark on a comprehensive journey into the specifics of an NGF CU Car Loan. Our goal is to equip you with all the knowledge you need to make an informed decision, ensuring your car-buying experience is smooth, transparent, and financially sound.

Drive Your Dreams: The Ultimate Guide to Securing an NGF CU Car Loan

We’ll dive deep into why NGF CU stands out, explore their loan offerings, demystify the application process, and share expert tips to help you secure the best possible terms. Get ready to turn the key on your next vehicle purchase with confidence!

Understanding the Landscape of Car Loans: Your Financial Compass

Before we specifically address the benefits of an NGF CU Car Loan, it’s crucial to grasp the fundamental nature of auto financing. A car loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that money, plus interest, over a predetermined period. This allows you to acquire a car without needing to pay the full price upfront.

For most individuals, a car loan is an indispensable tool for vehicle acquisition. It provides the flexibility to spread out the cost over several years, making car ownership accessible and manageable within a monthly budget. Without this option, owning a car would be an unattainable dream for a vast majority of the population.

There are primarily two types of car loans you’ll encounter: those for new vehicles and those for used vehicles. Each comes with its own set of considerations regarding interest rates, loan terms, and eligibility. Additionally, refinancing an existing car loan offers another pathway to potentially lower your monthly payments or total interest paid, a strategy we’ll explore further.

Why a Credit Union Like NGF CU Often Tops the Charts for Auto Financing

When considering where to secure your next auto loan, you have numerous choices: big banks, online lenders, and dealership financing. However, credit unions consistently emerge as a preferred option for many savvy borrowers, and for good reason. Understanding these inherent advantages helps frame the value of an NGF CU Car Loan.

Based on my experience in the financial industry, credit unions operate differently from traditional banks. They are not-for-profit organizations owned by their members, which fundamentally shifts their priorities. Instead of maximizing profits for shareholders, their primary focus is on providing beneficial services and competitive rates to their members. This cooperative structure directly translates into tangible advantages for you, the borrower.

These benefits often include lower interest rates on loans, fewer fees, and a more personalized, member-centric approach to customer service. Because they serve their members rather than external investors, credit unions can often pass on savings in the form of more favorable loan terms. This makes a significant difference over the life of a car loan, potentially saving you hundreds, if not thousands, of dollars.

Diving Deep into the NGF CU Car Loan Experience

Now, let’s zero in on what makes an NGF CU Car Loan a compelling choice for your next vehicle purchase. NGF CU, like other member-focused credit unions, is committed to supporting its community with accessible and affordable financial solutions. Their car loan offerings are designed with the member’s financial well-being at heart, aiming to make your car ownership dreams a reality without unnecessary financial strain.

Who is NGF CU? A Partner in Your Financial Journey

While specific details about NGF CU’s history and community involvement would be found directly on their website, generally, credit unions like NGF CU pride themselves on being pillars of their local communities. They often have a strong track record of providing personalized financial guidance and fostering long-term relationships with their members. Choosing an NGF CU Car Loan means opting for a financial partner that understands your needs and works to empower you.

Exploring the Types of NGF CU Car Loans Available

NGF CU typically offers a range of auto loan products designed to fit various needs and financial situations. This flexibility is a key advantage, ensuring you can find a loan that aligns with your specific requirements.

New Car Loans: If you’re looking to drive off the lot in a brand-new vehicle, an NGF CU new car loan can provide competitive rates and terms. These loans often come with the lowest interest rates due to the vehicle’s higher value and lower depreciation risk for the lender. Typical loan terms can range from 36 to 72 months, sometimes even longer, depending on the vehicle price and your creditworthiness. A new car loan from NGF CU allows you to enjoy the latest features and peace of mind that comes with a factory warranty, all while benefiting from favorable financing.

Used Car Loans: Opting for a used vehicle can be a smart financial move, offering excellent value. NGF CU understands this and provides robust used car loan options. While interest rates for used cars might be slightly higher than for new ones due to factors like age and mileage, NGF CU strives to keep them competitive. They will typically have age and mileage restrictions for the vehicles they finance, ensuring the car remains a viable asset throughout the loan term. Securing a used car loan through NGF CU means you can still benefit from their member-focused rates, even on a pre-owned vehicle.

Refinancing Your Existing Car Loan: Perhaps you already have a car loan but are looking for better terms. An NGF CU Car Loan for refinancing could be your solution. Refinancing involves taking out a new loan to pay off your current auto loan, ideally at a lower interest rate or with more favorable terms. This strategy can significantly reduce your monthly payments, decrease the total interest you’ll pay over the loan’s life, or even allow you to shorten your loan term to pay off the debt faster. It’s an excellent option if your credit score has improved since you first took out your loan, or if you initially financed through a dealership at a higher rate.

The NGF CU Application Process: A Smooth Ride Ahead

Securing an NGF CU Car Loan doesn’t have to be a complicated ordeal. Their process is designed to be straightforward and transparent, guiding you every step of the way.

1. Consider Pre-Approval: Pro tips from us suggest that the first and most strategic step is to get pre-approved for your car loan. Pre-approval means NGF CU reviews your financial information and determines how much you can borrow, along with an estimated interest rate, before you even step foot in a dealership. This transforms you into a cash buyer, giving you significant leverage in price negotiations. You’ll know your budget upfront, preventing emotional overspending and ensuring you get a fair deal on the car itself.

2. Gather Your Documents: While the exact list may vary slightly, you’ll generally need to provide proof of income (pay stubs, tax returns), identification (driver’s license), proof of residence (utility bill), and information about the vehicle you intend to purchase (if you’ve already chosen one). Having these documents ready beforehand will significantly expedite your application process.

3. Application Submission: NGF CU typically offers both online and in-branch application options. The online portal provides convenience, allowing you to apply from anywhere at any time. If you prefer a more personal touch or have specific questions, visiting a branch lets you speak directly with a loan officer who can walk you through the process.

4. Approval Timeline: The approval timeline for an NGF CU Car Loan can vary. While some applications might receive an instant decision, others may take a few business days, especially if additional information is required. Rest assured, NGF CU aims to process applications efficiently, understanding your eagerness to get behind the wheel.

Eligibility and Requirements for an NGF CU Car Loan

Like any financial institution, NGF CU has specific criteria for loan approval. Understanding these requirements beforehand will help you prepare and increase your chances of success.

Membership is Key: As a credit union, the first and foremost requirement is typically membership. If you’re not already a member, don’t worry! NGF CU will provide clear guidelines on how to become one, often involving a simple application and a small deposit into a savings account. Eligibility for membership is usually based on factors like where you live, work, or specific affiliations.

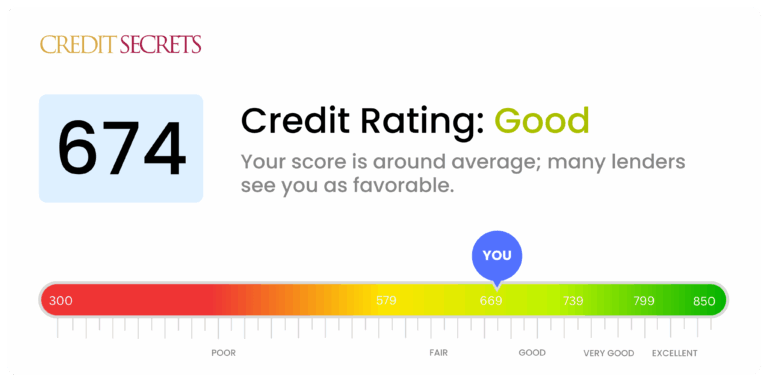

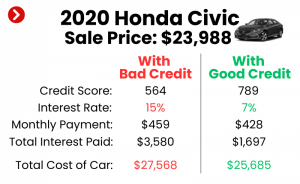

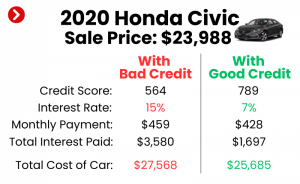

Credit Score Considerations: Your credit score plays a significant role in determining your interest rate and loan eligibility. While a higher credit score (generally 700+) will unlock the most favorable rates, NGF CU, being member-focused, often works with individuals across a spectrum of credit profiles. They may offer solutions for those with fair or even improving credit, though the rates might be higher to reflect the increased risk. It’s always a good idea to check your credit score before applying.

Income Stability: Lenders want to ensure you have the capacity to repay the loan. Demonstrating a stable source of income is crucial. This helps NGF CU assess your ability to make consistent monthly payments without financial strain.

Down Payment Expectations: While not always strictly required, making a down payment on your car loan is highly recommended. It reduces the amount you need to borrow, lowers your monthly payments, and can even help you secure a better interest rate. A typical down payment might range from 10% to 20% of the vehicle’s price, though even a smaller amount can make a difference.

Debt-to-Income Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to gauge your ability to take on additional debt. A lower debt-to-income ratio indicates less financial risk and a greater capacity to manage a new car loan.

Understanding NGF CU Car Loan Rates and Terms

The interest rate and loan term are two of the most critical factors influencing the total cost of your NGF CU Car Loan. It’s essential to understand how these are determined and what options are available.

Factors Influencing Rates: Several elements contribute to the interest rate you’ll be offered. Your credit score is paramount; a higher score signals lower risk to the lender, resulting in a lower rate. The loan term also matters – shorter terms often have slightly lower rates. The type of vehicle (new vs. used) and the loan amount can also play a role.

Typical Loan Terms: NGF CU typically offers flexible loan terms to accommodate various budgets. Common terms include 36, 48, 60, and 72 months. While longer terms result in lower monthly payments, they also mean you’ll pay more in total interest over the life of the loan. Conversely, shorter terms have higher monthly payments but save you money on interest in the long run.

The Importance of Comparison: Even within NGF CU, rates can vary based on the factors mentioned. It’s always wise to compare the Annual Percentage Rate (APR) – which includes interest and certain fees – across different loan terms to see what best fits your financial plan. For a deeper dive into understanding interest rates and how they impact your loans, check out our article on .

Maximizing Your NGF CU Car Loan: Smart Strategies from the Experts

Securing an NGF CU Car Loan is just one part of the equation. Strategic planning can help you get the absolute best deal and manage your auto financing effectively.

Get Pre-Approved and Negotiate with Confidence: As mentioned, pre-approval is a game-changer. It gives you concrete financing in hand, allowing you to focus purely on the vehicle’s price at the dealership. You’re negotiating from a position of strength, not desperation, which can lead to significant savings on the car itself.

Improve Your Credit Score Before Applying: Even small improvements to your credit score can translate into lower interest rates. Pay down existing debts, especially credit card balances, and avoid applying for new credit in the months leading up to your car loan application. A higher score directly impacts the favorability of your NGF CU Car Loan terms.

Consider a Substantial Down Payment: The more money you put down upfront, the less you need to borrow. This not only reduces your monthly payments but also decreases the total interest paid over the loan’s term. A larger down payment can also help mitigate the risk of being "upside down" on your loan, where you owe more than the car is worth.

Choose the Right Loan Term for Your Budget: While a longer loan term offers lower monthly payments, common mistakes to avoid are extending the term purely for a smaller payment without considering the total cost. Assess your budget honestly. If you can comfortably afford a shorter term, you’ll save a substantial amount in interest over time. Balance affordability with the overall financial impact.

Don’t Overlook Insurance Requirements: Lenders typically require you to carry full coverage insurance (collision and comprehensive) on a financed vehicle. Factor the cost of this insurance into your overall budget. Get quotes from several providers before finalizing your purchase, as insurance premiums can vary significantly.

Real-World Scenarios: How an NGF CU Car Loan Can Help

Let’s look at how an NGF CU Car Loan might benefit different individuals in practical terms:

Scenario 1: The First-Time Car Buyer (Sarah, 24) Sarah needs her first reliable car for her new job. She has a decent credit score but limited credit history. An NGF CU Car Loan, with its member-focused approach, might offer her a competitive rate that a traditional bank wouldn’t, recognizing her potential as a long-term member. The personalized guidance from a loan officer could also help her navigate the process with ease.

Scenario 2: The Refinancing Strategist (Mark, 38) Mark bought his SUV two years ago at a high interest rate from the dealership. His credit score has significantly improved since then. By refinancing his existing loan with NGF CU, Mark could potentially lower his interest rate by several percentage points, saving him hundreds of dollars annually and reducing his overall loan cost.

Scenario 3: The Savvy Used Car Shopper (Emily, 45) Emily is looking for a dependable used minivan for her family. She’s found a great deal on a 3-year-old model. An NGF CU Car Loan for a used vehicle would provide her with competitive financing, allowing her to secure a valuable asset without overpaying on interest, especially when compared to some subprime lenders.

Beyond the Loan: The Full Spectrum of NGF CU Membership Benefits

Choosing an NGF CU Car Loan is often just the beginning of a beneficial financial relationship. As a member, you gain access to a wider array of services and a community-oriented approach that distinguishes credit unions.

NGF CU likely offers a full suite of financial products, including checking and savings accounts, credit cards, personal loans, and potentially even mortgage services. Consolidating your financial needs with one trusted institution simplifies your money management and can often lead to even better rates and personalized service across the board. Credit unions are known for their financial education resources and commitment to member well-being, fostering a supportive environment for your financial growth. Explore other financial solutions in our guide to .

Frequently Asked Questions About NGF CU Car Loans

To help clarify common queries, here are some frequently asked questions regarding NGF CU Car Loans:

- Can I apply for an NGF CU Car Loan if I’m not a member yet? Typically, you’ll need to become a member to apply for a loan. However, the membership process is usually straightforward and can often be completed simultaneously with your loan application.

- What credit score do I need to get approved? While a higher credit score (e.g., 700+) will secure the best rates, NGF CU often works with members across various credit profiles. It’s always best to apply or speak with a loan officer to understand your specific options.

- How long does the loan approval process take? Approval times can vary. Some applicants may receive instant decisions, especially for pre-approvals, while others might take a few business days depending on the complexity of the application and the need for additional documentation.

- Can I refinance a car loan I have with another lender through NGF CU? Yes, refinancing is a common service offered by credit unions. If you have an existing car loan with another institution, NGF CU can help you explore options to lower your rate or adjust your terms.

- Are there any hidden fees with an NGF CU Car Loan? Credit unions are known for their transparency and typically have fewer fees than traditional banks. However, it’s always wise to review all loan disclosures carefully and ask about any potential application, origination, or closing fees.

Conclusion: Your Road to Vehicle Ownership Starts with NGF CU

Securing the right car loan is a cornerstone of a successful vehicle purchase, and an NGF CU Car Loan presents a compelling option for many. By offering competitive rates, flexible terms, and a member-first philosophy, NGF CU empowers you to make a financially sound decision. From new car purchases to used vehicles and even refinancing existing loans, their comprehensive offerings are designed to meet diverse needs.

Remember, armed with knowledge about pre-approval, understanding your credit, and choosing the right loan terms, you can navigate the car financing landscape with confidence. Don’t just settle for any loan; choose a partner that prioritizes your financial well-being.

Take the first step towards driving your dream car today. Explore the options for an NGF CU Car Loan, get pre-approved, and experience the difference of member-focused financing. For more general information on auto loan best practices and consumer rights, you can visit the External Link: Consumer Financial Protection Bureau’s Auto Loan Guide. Your perfect ride, financed wisely, awaits!