Drive Your Dreams: The Ultimate Guide to Securing an RBS Car Loan

Drive Your Dreams: The Ultimate Guide to Securing an RBS Car Loan Carloan.Guidemechanic.com

The open road, the fresh scent of a new interior, the thrill of a journey – owning your ideal car is an exciting prospect. However, for many, turning this dream into a reality hinges on securing the right financing. Navigating the world of car loans can feel overwhelming, with countless options and terms to understand.

That’s where a reputable financial institution like RBS comes into play. An RBS Car Loan could be the key to unlocking your automotive aspirations. This comprehensive guide will demystify everything you need to know about RBS Car Loans, from eligibility and application to understanding interest rates and comparing alternatives. Our goal is to equip you with the knowledge to make an informed decision, ensuring a smooth ride from application to ownership.

Drive Your Dreams: The Ultimate Guide to Securing an RBS Car Loan

Understanding RBS Car Loans: What Are They, Really?

At its core, an RBS Car Loan is a personal loan specifically designed to help you purchase a vehicle. Unlike some dealership finance options that tie you to a particular car or dealer, an RBS Personal Loan for a car offers flexibility. It provides you with a lump sum of money, which you then use to buy your chosen car outright, effectively making you a cash buyer at the dealership.

This means you own the car from day one, without the complexities of hire purchase agreements or personal contract plans where ownership might be deferred. The loan is then repaid to RBS in fixed monthly instalments over an agreed period, making budgeting straightforward and predictable.

RBS, like many major banks, primarily offers unsecured personal loans for vehicle purchases. This means you don’t need to use your car as collateral. While this can be a relief for many, it also means that the bank assesses your creditworthiness very carefully. Your ability to repay the loan is based on your financial history and current income, not on the value of the asset you’re buying.

Why Consider an RBS Car Loan? The Advantages That Stand Out

When exploring car financing options, RBS Car Loans present several compelling benefits that make them a strong contender. Understanding these advantages can help you determine if this is the right path for your next vehicle purchase.

Competitive Interest Rates

One of the primary draws of an RBS Car Loan is the potential for competitive interest rates. As a well-established bank, RBS often offers rates that can be more attractive than those found through dealership finance packages, especially for applicants with strong credit histories. Lower interest rates translate directly into less money paid over the life of the loan.

Based on my experience in the finance sector, securing a good interest rate is paramount. Even a small percentage difference can save you hundreds, if not thousands, of pounds over several years. It’s always worth comparing the Annual Percentage Rate (APR) offered by banks like RBS against other lenders.

Flexible Repayment Terms

RBS understands that everyone’s financial situation is unique. They typically offer a range of repayment terms, allowing you to choose a period that best suits your budget and financial goals. Whether you prefer shorter terms to pay off the loan quicker or longer terms to reduce your monthly outgoings, you’ll likely find an option that works for you.

This flexibility is a significant advantage. It empowers you to tailor your loan to your personal cash flow, ensuring that your monthly repayments are manageable and don’t strain your finances. Always consider the total cost over the full term, not just the monthly payment.

No Collateral Required (for Unsecured Loans)

As mentioned, most RBS Car Loans are unsecured. This means you don’t have to pledge your car or any other asset as security for the loan. This offers a level of financial freedom and peace of mind. Should unforeseen circumstances arise, your vehicle isn’t directly at risk of repossession by the lender solely due to the loan.

Pro tips from us: While an unsecured loan means less risk to your assets, it places a greater emphasis on your credit score during the application process. Banks use your credit history as their primary indicator of your repayment reliability.

Predictable Monthly Payments

One of the greatest benefits of a fixed-rate personal loan, which is common for RBS Car Loans, is the predictability of your monthly payments. Once your loan is approved and the interest rate is set, your monthly instalment will remain the same throughout the entire repayment period. This consistency makes budgeting incredibly simple.

You’ll know exactly how much money needs to be allocated each month, allowing you to plan your other expenses with confidence. There are no surprises, which is a huge relief in personal finance.

Streamlined Application Process

RBS has invested in making its application process as straightforward and efficient as possible. Many applicants can complete the initial stages online, often receiving an instant decision or a quick response. This convenience saves time and reduces the hassle often associated with applying for finance.

From my years of observing banking processes, the move towards digital applications has significantly improved the user experience. While you may still need to provide documentation, the initial assessment is much faster than in previous years.

Eligibility Criteria for an RBS Car Loan: Do You Qualify?

Before you even think about applying, it’s crucial to understand the eligibility requirements for an RBS Car Loan. Meeting these criteria is the first step towards approval. RBS, like all lenders, has specific guidelines to assess an applicant’s ability to repay the loan.

Age Requirements

Typically, you must be at least 18 years old to apply for any form of credit in the UK. For a personal loan with a significant sum, RBS may have an upper age limit, often around 70 or 75 at the end of the loan term, to ensure the loan can be comfortably repaid within a reasonable working life. Always check the specific age criteria on their official website.

Residency Status

To be eligible for an RBS Car Loan, you generally need to be a permanent UK resident. This means having a stable address in the UK and often, a minimum period of residency within the country. This helps the bank verify your identity and assess your financial history within the UK system.

Income Stability and Employment Status

Lenders need assurance that you have a consistent and sufficient income to meet your monthly repayments. RBS will typically require proof of stable employment or a regular, verifiable income stream. This could be in the form of payslips, bank statements, or tax returns if you are self-employed.

They aren’t just looking for income, but stable income. A long-standing employment history with the same employer or within the same industry can significantly strengthen your application.

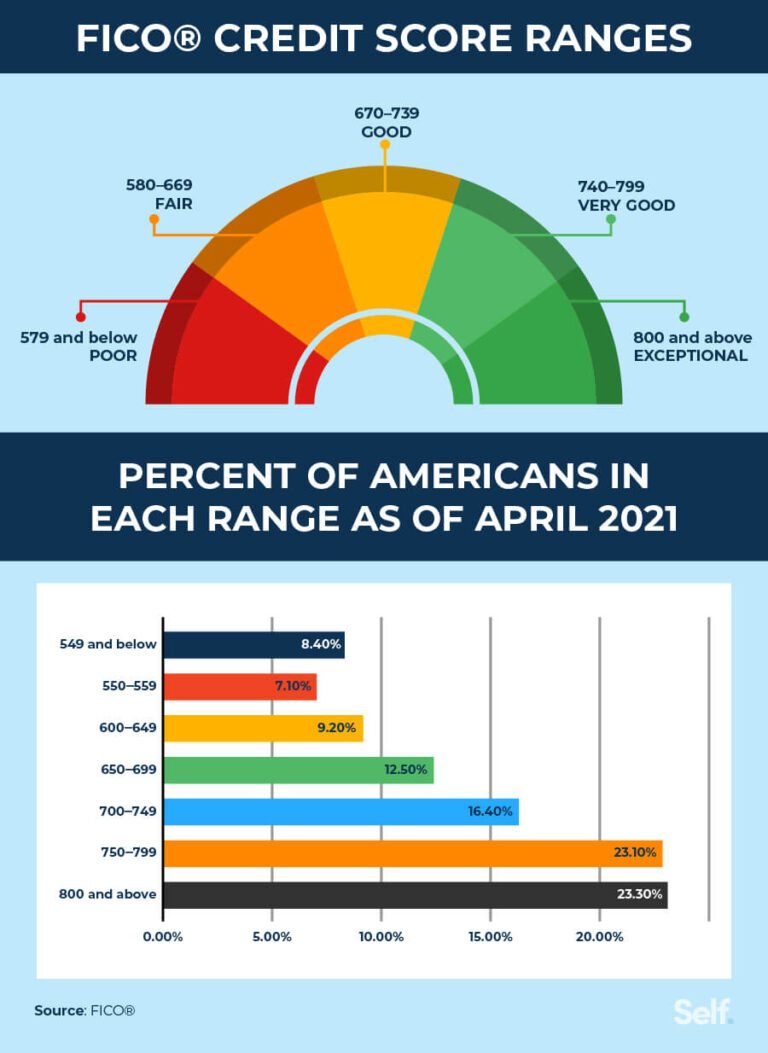

Credit Score: The Crucial Factor

Your credit score is arguably the most important element in your loan application. It’s a numerical representation of your creditworthiness, built from your past borrowing and repayment behaviour. A good to excellent credit score demonstrates to RBS that you are a reliable borrower who manages debt responsibly.

Pro tip from us: Before applying, always check your credit report with the major credit reference agencies (Experian, Equifax, TransUnion). Correct any errors and understand where you stand. A higher score will likely lead to better interest rates and a higher chance of approval.

Debt-to-Income Ratio

RBS will also look at your existing debt obligations relative to your income. This is known as your debt-to-income (DTI) ratio. If a significant portion of your income is already committed to other loan repayments, mortgages, or credit card bills, it might indicate that taking on more debt could put a strain on your finances.

Lenders want to see that you have enough disposable income left after your essential outgoings to comfortably afford the new car loan payments. A high DTI can be a red flag, even if you have a good credit score.

The Application Process: A Step-by-Step Guide

Applying for an RBS Car Loan can be a straightforward process if you’re well-prepared. Following these steps will help ensure a smooth journey from inquiry to approval.

Step 1: Research & Preparation

Before you even fill out a form, take the time to research. Determine the exact amount you need to borrow and for how long. Use online loan calculators to get an estimate of your potential monthly repayments. Crucially, check your eligibility criteria and your credit score as discussed earlier.

Understanding your financial standing beforehand can prevent disappointment and unnecessary credit checks. Knowing the car you want and its approximate price will also help you determine the precise loan amount.

Step 2: Gathering Documents

Once you’re ready to apply, you’ll need to have several documents on hand. While the exact list can vary slightly, common requirements include:

- Proof of Identity: Passport or driving licence.

- Proof of Address: Utility bill or bank statement (dated within the last three months).

- Proof of Income: Recent payslips (typically 3-6 months) or bank statements showing salary deposits. Self-employed individuals may need tax returns or certified accounts.

- Bank Account Details: For loan disbursement and direct debit setup.

Common mistakes to avoid during this stage include submitting outdated or incomplete documentation. Ensure all copies are clear and all information matches your application form precisely.

Step 3: Online Application or Branch Visit

RBS offers convenient ways to apply. You can typically apply online through their website, which is often the quickest method. The online form will guide you through providing your personal, financial, and employment details. Alternatively, if you prefer face-to-face assistance, you can visit an RBS branch to complete your application with the help of a customer service representative.

My professional advice is that if your situation is straightforward, the online application is highly efficient. If you have complex financial circumstances or prefer personalized guidance, a branch visit might be more suitable.

Step 4: Loan Assessment

After you submit your application, RBS will conduct an assessment. This involves reviewing the information you’ve provided, performing a credit check (which will leave a "hard" footprint on your credit file), and verifying your income and employment details. They use this information to determine your creditworthiness and whether they can offer you a loan, along with the specific interest rate.

This stage can take anywhere from a few minutes for an instant decision online to a few business days if further verification or documentation is required. Patience is key here.

Step 5: Approval & Disbursement

If your application is successful, RBS will inform you of the approval and the terms of your loan, including the interest rate, monthly repayment amount, and total loan term. Once you accept these terms, the funds will typically be disbursed directly into your bank account within a few business days. You can then use this money to purchase your car.

It’s crucial to carefully read and understand the loan agreement before signing. Ensure you are fully comfortable with all the terms and conditions.

Understanding Interest Rates and Repayment

Deciphering interest rates and repayment structures is vital for any car loan. It directly impacts the total cost of your vehicle and your monthly budget.

Fixed vs. Variable Rates

Most personal loans offered by RBS for car purchases come with a fixed interest rate. A fixed rate means the interest rate remains constant throughout the entire loan term. This provides stability and predictability, as your monthly repayments will not change.

A variable rate, conversely, can fluctuate with market conditions (e.g., changes in the Bank of England base rate). While a variable rate might offer lower initial payments, it introduces uncertainty. For most consumers, especially when budgeting for a significant purchase like a car, a fixed rate offers peace of mind.

APR (Annual Percentage Rate): Why It’s Important

The Annual Percentage Rate (APR) is more than just the headline interest rate. It’s the total cost of borrowing, expressed as an annual percentage. The APR includes the interest rate plus any additional mandatory fees associated with the loan. This makes it a more accurate figure for comparing different loan offers.

From my years of observing loan markets, understanding APR is non-negotiable. Always compare the APR, not just the advertised interest rate, when looking at different loan products. A lower APR means a cheaper loan overall.

Repayment Calculators: Budgeting with Precision

RBS, like most lenders, provides online loan calculators. These tools are invaluable for planning your finances. By inputting the loan amount, interest rate, and desired repayment term, you can instantly see your estimated monthly payments and the total amount repayable.

Using these calculators allows you to play with different scenarios. You can see how extending the loan term reduces monthly payments but increases the total interest paid, or how a larger down payment reduces the amount you need to borrow.

Early Repayment Options

Many personal loans offer the option to make overpayments or repay the loan in full before the agreed term ends. This can be a great way to save on interest charges. However, some lenders may apply early repayment charges to compensate for the interest they lose.

It’s essential to check RBS’s specific terms regarding early repayment. Based on my experience, many UK banks allow partial overpayments without penalty, but a full early settlement might incur a small charge. Always read the fine print in your loan agreement.

Comparing RBS Car Loans with Other Financing Options

While an RBS Car Loan can be an excellent choice, it’s wise to consider it within the broader landscape of car finance options. Understanding the alternatives helps you make the best decision for your unique situation.

Dealership Finance

Dealerships often offer their own finance packages, such as Personal Contract Purchase (PCP) or Hire Purchase (HP). While convenient, these can sometimes come with higher interest rates or less flexible terms than a direct bank loan. The interest rates can also be negotiated, but the transparency might be less clear than with a bank.

Based on my experience, many first-time car buyers overlook comparing dealership finance with external personal loans. Always get a quote from your bank before you walk into a dealership; it gives you stronger negotiating power.

Personal Contract Purchase (PCP)

PCP is a popular option where you pay monthly instalments for a set period, but you don’t own the car at the end of the term. Instead, you have three options: return the car, pay a final "balloon payment" to own it, or use any equity as a deposit for a new PCP deal.

PCP often has lower monthly payments than a traditional loan, but you don’t own the car until the final payment, and mileage restrictions usually apply.

Hire Purchase (HP)

With Hire Purchase, you pay monthly instalments over a set period, and once the final payment is made (including an ‘option to purchase’ fee), you own the car. It’s essentially a loan secured against the car itself.

HP payments are typically higher than PCP but lower than an equivalent personal loan for the same car, as the loan is secured. You only truly own the car at the end of the agreement.

Other Bank Loans

Of course, RBS isn’t the only bank offering personal loans for car purchases. It’s always a good idea to compare offers from several reputable banks and financial institutions. Interest rates and terms can vary significantly between lenders, even for applicants with similar credit profiles.

This comparison can often reveal better deals or more suitable terms for your specific needs. For a detailed breakdown of different car finance options, you might find our article on "Choosing the Right Car Finance: A Comprehensive Guide" helpful.

Pro Tips for a Successful RBS Car Loan Application

To maximise your chances of approval and secure the best possible terms for your RBS Car Loan, consider these expert tips.

- Improve Your Credit Score: This is fundamental. Pay bills on time, reduce existing debt, and check your credit report for errors. A stronger credit score translates to better loan offers.

- Save for a Down Payment: While not strictly necessary for an unsecured personal loan, a larger down payment reduces the amount you need to borrow, thereby lowering your monthly payments and overall interest paid. It also shows financial responsibility.

- Know Your Budget: Before applying, thoroughly assess your monthly income and outgoings. Understand exactly how much you can comfortably afford to repay each month without stretching your finances too thin.

- Read the Fine Print: Never skip reading the full loan agreement. Understand all terms, conditions, fees, and early repayment clauses. My professional advice here is simple: patience is a virtue, and thoroughness pays off.

- Don’t Apply to Multiple Lenders Simultaneously: Each "hard" credit check leaves a mark on your credit file. Multiple checks in a short period can negatively impact your score, making you appear desperate for credit. Apply to one or two well-researched options first.

Common Mistakes to Avoid When Getting a Car Loan

Even with the best intentions, applicants sometimes make errors that can jeopardise their loan application or lead to less favourable terms. Avoid these common pitfalls.

- Not Checking Your Credit Score: This is a big one. Many people apply blind, only to be rejected due to an unknown issue on their credit report. Always check first.

- Borrowing More Than You Need: It’s tempting to borrow a little extra for accessories or unexpected costs. However, every extra pound borrowed accrues interest, increasing your total cost. Borrow only what’s necessary for the car.

- Ignoring the Total Cost (APR, Fees): Focusing solely on the monthly payment can be misleading. Always look at the APR and the total amount repayable over the loan term to understand the true cost.

- Skipping the Fine Print: As mentioned, neglecting the terms and conditions can lead to unpleasant surprises later, especially regarding fees or early repayment penalties.

- Not Comparing Offers: Settling for the first offer you receive without comparing it to others is a common mistake that can cost you money. Always shop around, even if it’s just for one or two alternative quotes.

RBS Car Loan Alternatives: When RBS Might Not Be the Right Fit

While RBS offers competitive car loan options, it’s possible that their terms might not align perfectly with everyone’s specific needs or credit profile. If an RBS Car Loan isn’t the ideal solution for you, several reputable alternatives exist.

- Other High Street Banks: Major banks like Lloyds, Barclays, NatWest (part of the same group as RBS, but sometimes with slightly different product offerings), HSBC, and Santander all offer personal loans for car purchases. Their rates and eligibility criteria can vary, making it worthwhile to compare.

- Specialist Car Finance Providers: Companies like Zuto, CarFinance 247, or smaller, niche lenders specialise solely in vehicle finance. They might offer more flexible options for individuals with less-than-perfect credit, albeit often at higher interest rates.

- Credit Unions: If you’re a member of a credit union, they often provide personal loans with competitive rates and a more community-focused approach. Eligibility is usually tied to where you live or work.

- Guarantor Loans: For those with poor credit history, a guarantor loan, where a trusted friend or family member co-signs the loan and agrees to make payments if you default, can be an option. However, this carries significant risk for the guarantor.

For a broader understanding of responsible borrowing and financial health, we recommend visiting a trusted external source like the MoneySavingExpert Car Finance Guide (https://www.moneysavingexpert.com/car-finance/) for impartial advice on various car finance products.

FAQs (Frequently Asked Questions) about RBS Car Loans

Let’s address some common questions that often arise when considering an RBS Car Loan.

Q: Can I get an RBS car loan with bad credit?

A: While RBS primarily targets applicants with good to excellent credit scores due to the unsecured nature of their personal loans, they assess each application individually. A lower credit score might still get approved, but it’s likely to come with a higher interest rate. It’s always best to improve your credit score before applying. For tips on this, read our article: "Boost Your Credit Score: The Ultimate Guide to Financial Freedom".

Q: How long does approval take for an RBS Car Loan?

A: Many online applications receive an instant conditional decision. However, full approval and fund disbursement can take anywhere from a few hours to a few business days, depending on whether RBS needs to request additional documentation or conduct further checks.

Q: What can the loan be used for?

A: An RBS Car Loan (personal loan) is typically for purchasing a car, whether new or used, from a dealership or a private seller. Because the funds are paid directly to you, you have the flexibility to use them for the vehicle you choose, without the bank dictating the seller.

Q: Is there an age limit for the car I want to buy?

A: Since an RBS Car Loan is an unsecured personal loan, there are usually no specific age restrictions on the vehicle itself, unlike some secured car finance products. The focus is on your ability to repay the loan, not the car’s depreciation.

Q: Can I repay my RBS Car Loan early?

A: Yes, you can typically repay your RBS Car Loan early, either in part or in full. However, it’s crucial to check your loan agreement for any potential early repayment charges. While many banks have reduced or removed these, some may still apply a small fee.

Conclusion: Your Journey to Car Ownership Starts Here

Securing a car loan is a significant financial decision, and choosing the right lender is paramount. An RBS Car Loan offers a compelling package of competitive rates, flexible terms, and a straightforward application process, making it a strong contender for anyone looking to finance their next vehicle. By understanding the eligibility criteria, meticulously preparing your application, and carefully comparing offers, you empower yourself to make a truly informed choice.

Remember, the goal isn’t just to get a loan, but to get the right loan that aligns with your financial health and future aspirations. With the insights provided in this guide, you’re well-equipped to navigate the world of RBS Car Loans with confidence, paving the way for you to drive away in your dream car. Your journey to car ownership doesn’t have to be complicated; with the right information, it can be an exciting and rewarding experience.