Drive Your Dreams: Unlocking the Best Meritrust Car Loan Rates for Your Next Vehicle

Drive Your Dreams: Unlocking the Best Meritrust Car Loan Rates for Your Next Vehicle Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect for many. However, navigating the complexities of auto financing can often feel daunting. For residents of Kansas and those seeking a community-focused financial partner, Meritrust Credit Union stands out as a beacon of trust and value. If you’re wondering about Meritrust Car Loan Rates and how to secure the best possible deal, you’ve landed in the right place.

As an expert blogger and professional SEO content writer with extensive experience in personal finance, I understand the critical importance of not just finding a loan, but finding the right loan. This comprehensive guide will meticulously explore everything you need to know about Meritrust’s auto financing options, helping you drive away with confidence and a clear understanding of your financial commitment. We’ll delve deep into the factors influencing rates, the application process, and invaluable strategies to maximize your savings.

Drive Your Dreams: Unlocking the Best Meritrust Car Loan Rates for Your Next Vehicle

Why Choose Meritrust for Your Car Loan? The Credit Union Advantage

Before we dive into the specifics of Meritrust Car Loan Rates, it’s essential to understand the fundamental difference that sets credit unions apart from traditional banks. Meritrust Credit Union operates on a not-for-profit model, meaning its primary focus is on serving its members, not maximizing shareholder profits. This unique structure translates directly into tangible benefits for you, the borrower.

Unlike big banks, credit unions like Meritrust often offer more competitive interest rates on loans and higher yields on savings accounts. This is because any surplus earnings are reinvested back into the credit union to provide better services, lower fees, and, crucially, more favorable loan terms for their members. When you become a Meritrust member, you’re not just a customer; you’re a co-owner.

This membership-centric approach fosters a deeper relationship, often leading to more personalized service and a genuine desire to help you achieve your financial goals. Based on my experience, this personalized touch can make a significant difference, especially when you need tailored advice or encounter unexpected financial situations.

Understanding Meritrust Car Loan Rates: Key Factors at Play

The advertised car loan rates you see are often a starting point. Your actual Meritrust Car Loan Rate will be determined by a combination of individual financial factors. It’s crucial to understand these elements, as they empower you to take proactive steps towards securing the most favorable terms. Let’s break down the primary determinants:

Your Credit Score: The Cornerstone of Loan Rates

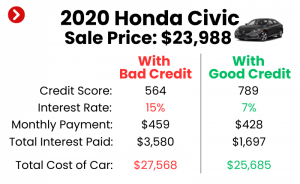

Without a doubt, your credit score is the single most influential factor in determining the interest rate you’ll be offered. Lenders, including Meritrust, use your credit score as a primary indicator of your creditworthiness and your likelihood of repaying the loan. A higher credit score signals lower risk to the lender, which typically translates into a lower interest rate for you.

Credit scores, such as FICO scores, range from 300 to 850. Generally, scores above 700 are considered "good," while those above 760 are "excellent." If your score falls into the excellent category, you can expect to qualify for Meritrust’s most competitive car loan rates. Conversely, a lower credit score will likely result in a higher interest rate, reflecting the increased risk the credit union takes on.

Pro tips from us: Before you even think about applying for a car loan, pull your credit report from all three major bureaus (Equifax, Experian, and TransUnion). Review it carefully for any errors or discrepancies that could be negatively impacting your score. Correcting these errors can often boost your score quickly. For an in-depth look at managing your credit, check out our guide on .

Loan Term: Balancing Monthly Payments and Total Interest

The loan term, or the length of time you have to repay the loan, also significantly impacts your Meritrust Car Loan Rate and the total cost of your vehicle. Common loan terms range from 36 months (3 years) to 72 or even 84 months (6 to 7 years).

A shorter loan term, such as 36 or 48 months, generally comes with a lower interest rate. While your monthly payments will be higher, you’ll pay significantly less interest over the life of the loan. This is because the credit union has its funds tied up for a shorter period, reducing their overall risk exposure.

Conversely, opting for a longer loan term will result in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, longer terms almost always come with higher interest rates, and you’ll end up paying substantially more in total interest over the life of the loan. This can lead to a situation where you are "upside down" on your loan, meaning you owe more than the car is worth, especially if the vehicle depreciates quickly.

Your Down Payment: Showing Financial Commitment

Making a substantial down payment on your car loan demonstrates your financial commitment and reduces the amount you need to borrow. From Meritrust’s perspective, a larger down payment means less risk for them, as they have less capital at stake.

A strong down payment can lead to a lower interest rate. It also reduces your monthly payments and lessens the likelihood of being upside down on your loan. Based on my experience, aiming for at least 10-20% of the vehicle’s purchase price as a down payment is a smart financial move. For used cars, a larger down payment is even more beneficial due to their typically faster depreciation rate.

Vehicle Age and Type: New vs. Used Car Loans

The age and type of the vehicle you intend to purchase can also influence your Meritrust Car Loan Rate. New cars generally qualify for lower interest rates compared to used cars. This is because new vehicles are perceived as less risky; they haven’t been subject to wear and tear, and their value is more predictable in the immediate future.

Used car loans often carry slightly higher interest rates due to the inherent uncertainties associated with pre-owned vehicles, such as unknown maintenance history and faster depreciation. However, Meritrust offers competitive rates for both new and used vehicles, ensuring you have options regardless of your preference. It’s always worth comparing rates for both to see what makes the most sense for your budget.

Debt-to-Income (DTI) Ratio: Your Ability to Repay

Meritrust will also look at your debt-to-income (DTI) ratio, which is the percentage of your gross monthly income that goes towards paying your monthly debt payments. This includes housing, credit card minimums, student loans, and other installment loans. A lower DTI ratio indicates that you have more disposable income available to comfortably make your car loan payments.

A DTI ratio typically below 36% is considered ideal by lenders. If your DTI is high, it might signal to Meritrust that taking on additional debt could strain your finances, potentially leading to a higher interest rate or even a loan denial. Managing your existing debt responsibly before applying for a car loan is a crucial step.

Types of Meritrust Auto Loans: Tailored to Your Needs

Meritrust Credit Union offers a diverse range of auto loan products designed to meet various needs and financial situations. Understanding these options will help you choose the best path forward.

New Car Loans

If you’re eyeing that brand-new vehicle, Meritrust provides competitive financing for the latest models. These loans typically come with the most attractive interest rates, especially for borrowers with excellent credit. Meritrust often has promotional rates for new cars, making it an excellent choice for first-time buyers or those looking to upgrade.

Used Car Loans

For those seeking value and affordability, Meritrust’s used car loans are an excellent option. While the rates might be slightly higher than new car loans, they remain highly competitive compared to many other lenders. Meritrust finances a wide range of used vehicles, typically up to a certain age or mileage limit. It’s important to verify these specifics directly with the credit union.

Auto Loan Refinancing

Do you already have a car loan with another institution at a higher interest rate? Meritrust Car Loan Rates for refinancing could save you a substantial amount of money over the life of your loan. Refinancing involves taking out a new loan, often with a lower interest rate, to pay off your existing car loan. This can significantly reduce your monthly payments or the total interest paid.

Based on my experience, refinancing is particularly beneficial if your credit score has improved since you first took out your loan, or if interest rates have dropped. It’s also a smart move if you want to adjust your loan term to better fit your current financial situation, perhaps by shortening it to pay less interest or lengthening it to reduce monthly payments.

Other Vehicle Loans

Beyond traditional cars, Meritrust may also offer financing for other recreational vehicles. This could include motorcycles, RVs, boats, and even ATVs. If you’re looking to finance an adventure, it’s worth checking with Meritrust about their specialized loan products for these types of vehicles.

The Meritrust Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan with Meritrust is a streamlined process designed for efficiency and transparency. Here’s a general overview of what you can expect:

Step 1: Preparation is Key – Know Your Budget and Needs

Before you even think about applying, determine how much car you can truly afford. This involves not just the monthly loan payment but also insurance, fuel, maintenance, and potential registration fees. Use online calculators to estimate payments at various interest rates and terms.

Gather necessary documents, which typically include:

- Proof of identity (driver’s license)

- Proof of income (pay stubs, tax returns)

- Proof of residence (utility bill)

- Vehicle information (if you’ve already chosen a car)

Step 2: Get Pre-Approved – Your Power Play

One of the most valuable pieces of advice I can offer is to get pre-approved for your car loan before you visit a dealership. Pre-approval from Meritrust provides you with a clear understanding of how much you can borrow, at what interest rate, and for what term.

This empowers you as a cash buyer at the dealership. You can focus solely on negotiating the car’s price, without the added pressure or distraction of financing. Dealers are notorious for trying to roll financing into the negotiation, often at less favorable rates. With a Meritrust pre-approval in hand, you dictate the terms. Common mistakes to avoid are going to the dealership without pre-approval, as you give up significant negotiation leverage.

Step 3: Complete the Application

You can typically apply for a Meritrust auto loan online, over the phone, or in person at one of their branch locations. The application will ask for your personal information, employment details, income, and financial obligations. Be prepared to provide accurate and complete information to avoid delays.

Meritrust’s loan officers are known for their helpfulness, so don’t hesitate to ask questions if you’re unsure about any part of the application.

Step 4: Review and Approval

Once you submit your application, Meritrust will review your financial profile, including your credit report, DTI ratio, and income. They will then determine your eligibility and the specific Meritrust Car Loan Rates you qualify for. If approved, you’ll receive an offer outlining the loan amount, interest rate, term, and monthly payment.

Step 5: Finalize and Fund Your Loan

Upon approval, you’ll sign the necessary loan documents. If you’ve already selected a vehicle, the funds can be disbursed directly to you or the dealership. This process is usually quick and efficient, allowing you to drive off in your new vehicle without unnecessary delays.

How to Secure the Best Meritrust Car Loan Rates: Pro Strategies

While your credit score is a major player, there are several other proactive steps you can take to ensure you get the most competitive Meritrust Car Loan Rate possible.

- Improve Your Credit Score: As mentioned, this is paramount. Pay all bills on time, keep credit card balances low, and avoid opening new credit accounts right before applying for a car loan. Even small improvements can make a difference.

- Increase Your Down Payment: The more you put down, the less you borrow, and the lower your risk profile becomes for Meritrust. This often translates into better rates.

- Consider a Shorter Loan Term: If your budget allows for higher monthly payments, opting for a shorter term will almost always result in a lower interest rate and significantly less total interest paid.

- Automate Your Payments: Some financial institutions, including credit unions, offer a slight interest rate discount if you agree to set up automatic payments from your Meritrust checking account. This guarantees on-time payments and reduces administrative costs for the credit union.

- Be a Meritrust Member with a Strong Relationship: While not always a direct rate reduction, being a long-standing, active member with other accounts (checking, savings, direct deposit) can sometimes influence loan decisions and show your commitment to the credit union, fostering a more favorable view of your application.

- Shop Around (Even with Meritrust): While Meritrust often offers excellent rates, it’s always wise to compare their offer with other credit unions or even banks if you have time. However, ensure you apply within a short window (14-45 days) so that multiple inquiries only count as one hard inquiry on your credit report. Then, bring the best offer back to Meritrust to see if they can match or beat it.

Common Mistakes to Avoid When Applying for a Car Loan

Even with the best intentions, borrowers can make errors that negatively impact their loan experience. Here are common pitfalls to steer clear of:

- Not Getting Pre-Approved: As discussed, this puts you at a disadvantage at the dealership, potentially leading to higher rates or unfavorable terms.

- Ignoring Your Credit Report: Errors on your report can unfairly lower your score. Always review it before applying.

- Borrowing More Than You Can Afford: It’s tempting to get the most expensive car you can qualify for, but this can stretch your budget thin and lead to financial stress. Focus on what’s truly affordable.

- Focusing Only on Monthly Payments: While important, fixating solely on the lowest monthly payment can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan.

- Forgetting About Insurance and Maintenance: These are substantial ongoing costs of car ownership. Factor them into your overall budget, not just the loan payment. A pro tip: get insurance quotes before you finalize your car purchase, as rates vary wildly depending on the vehicle.

- Accepting Dealer Financing Without Question: Dealers often mark up interest rates on loans they originate to earn a commission. Always compare their offer to your Meritrust pre-approval.

Refinancing Your Existing Car Loan with Meritrust: A Closer Look

Perhaps you already have a car loan but are looking for a better deal. Meritrust’s auto loan refinancing options deserve your attention. Refinancing can be a game-changer, potentially saving you thousands over the life of your loan.

When is refinancing with Meritrust a good idea?

- Your Credit Score Has Improved: If your score has significantly risen since you first bought the car, you might qualify for much lower Meritrust Car Loan Rates.

- Market Interest Rates Have Dropped: Interest rates fluctuate. If rates are lower now than when you first financed, refinancing can lock in those savings.

- You Want to Change Your Loan Term: You might want to shorten your term to pay off the car faster and save on interest, or lengthen it to reduce your monthly payments if your financial situation has changed.

- You Have a High-Interest Loan: If you originally financed through a dealership or another lender with a less favorable rate, Meritrust could offer a significant improvement.

- You Want to Remove a Co-Signer: If your financial standing has improved, refinancing can allow you to remove a co-signer from the loan.

The process for refinancing is similar to applying for a new loan. Meritrust will assess your creditworthiness and the value of your vehicle. They’ll then offer you new terms, and if accepted, they’ll pay off your old loan, and you’ll begin making payments to Meritrust. This simple step can lead to substantial long-term savings.

Beyond Car Loans: The Holistic Value of Meritrust Membership

Choosing Meritrust for your car loan isn’t just about securing a competitive rate; it’s about becoming part of a financial community that values its members. As a Meritrust member, you gain access to a full suite of banking services, often with lower fees and better terms than traditional banks. This can include:

- Checking and Savings Accounts: With competitive rates and fewer fees.

- Credit Cards: Often with lower interest rates and attractive rewards programs.

- Mortgages and Home Equity Loans: Competitive financing for your home.

- Personal Loans: For various financial needs.

- Financial Planning Resources: Guidance to help you manage your money effectively.

This holistic approach means that Meritrust can be a long-term financial partner, supporting you through various life stages and financial goals. For more general advice on budgeting and saving for big purchases, you might find our article on helpful.

Conclusion: Drive Smarter with Meritrust Car Loan Rates

Securing the best possible car loan rate is a critical step in smart financial planning for your vehicle purchase. Meritrust Car Loan Rates stand out for their competitiveness, reflecting the credit union’s member-first philosophy. By understanding the factors that influence your rate – primarily your credit score, loan term, and down payment – you empower yourself to take control of your financing journey.

Remember to leverage the power of pre-approval, thoroughly review your credit report, and consider all the benefits that come with being a Meritrust Credit Union member. Whether you’re buying new, used, or looking to refinance, Meritrust offers a transparent, member-focused approach to auto financing that can save you money and provide peace of mind.

Don’t let the excitement of a new car overshadow the importance of sound financial decisions. Take the proactive steps outlined in this guide, and you’ll be well on your way to driving your dream car with a loan that truly works for you. Visit Meritrust Credit Union’s official website today to explore their current car loan rates and begin your application process. Your journey to a smarter car loan starts here.

For additional independent resources on choosing the right auto loan, you can always consult trusted external sources like the Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/.