Drive Your Way to Financial Freedom: The Ultimate Guide to Using Your Car For A Loan

Drive Your Way to Financial Freedom: The Ultimate Guide to Using Your Car For A Loan Carloan.Guidemechanic.com

Life often throws unexpected financial curveballs. Whether it’s an urgent medical bill, a sudden home repair, or an unforeseen business opportunity, immediate access to funds can be critical. For many, traditional bank loans aren’t an option due to credit history or lengthy approval processes. This is where the concept of using your car for a loan enters the picture, offering a unique avenue for quick capital.

But what exactly does it mean to "use your car for a loan"? And is it the right solution for you? This comprehensive guide will peel back the layers, providing you with an in-depth understanding of car title loans, their mechanics, benefits, risks, and crucial alternatives. Our goal is to empower you with the knowledge to make an informed, responsible financial decision.

Drive Your Way to Financial Freedom: The Ultimate Guide to Using Your Car For A Loan

Understanding "Use Your Car For A Loan": The Core Concept

At its heart, using your car for a loan means leveraging the equity you have in your vehicle as collateral to secure a short-term loan. This type of financing is most commonly known as a car title loan or an auto equity loan. Instead of relying primarily on your credit score, lenders assess the value of your car to determine the loan amount.

What is a Car Title Loan?

A car title loan is a secured loan where your vehicle’s clear title serves as collateral. This means you temporarily hand over your car’s title to the lender, but you get to keep driving your car during the loan term. Once you fully repay the loan, including interest and fees, the title is returned to you.

The amount you can borrow typically ranges from 25% to 50% of your car’s wholesale value. This percentage can vary significantly depending on the lender, your state’s regulations, and the specific condition of your vehicle. Lenders evaluate factors like make, model, year, mileage, and overall condition to appraise your car.

How Does This Type of Loan Work?

The process usually begins with an application, either online or in person. You’ll need to provide documentation to prove ownership of your car, its value, and your ability to repay the loan. Once approved, you’ll sign an agreement, hand over your car’s title (or allow the lender to place a lien on it), and receive your funds.

Repayment terms vary, but car title loans are often structured as short-term, lump-sum payments or a series of smaller installments over a few months. The interest rates can be significantly higher than traditional loans, which is a crucial point we will explore in detail.

Key Terminology to Know

Navigating the world of car title loans requires understanding specific terms:

- Collateral: This is an asset (in this case, your car’s title) that a borrower offers to a lender to secure a loan. If the borrower defaults, the lender can seize the collateral.

- Lien: A legal claim placed on an asset (your car) by a lender until a debt is repaid. When you take out a car title loan, the lender places a lien on your title.

- Equity: The difference between the market value of your car and the amount you still owe on it. For a car title loan, you typically need to have significant or full equity (a "clear title").

- Principal: The original amount of money borrowed, excluding interest.

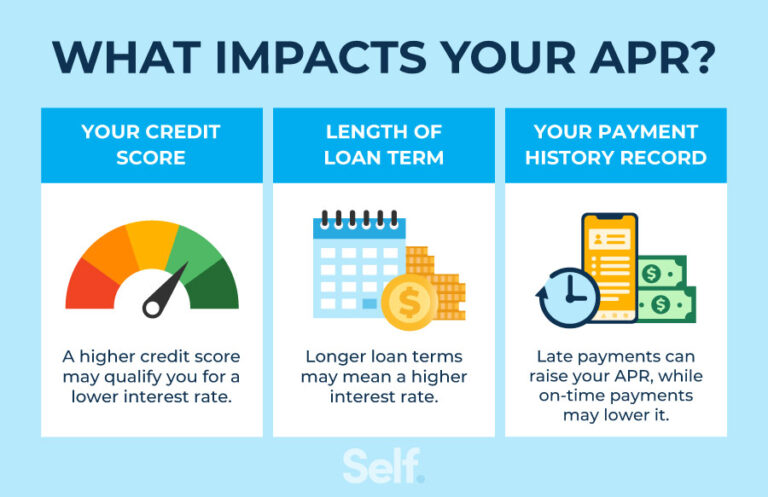

- Interest Rate (APR): The annual percentage rate, which represents the true cost of the loan over a year, including all fees and charges. This is often very high for title loans.

Based on my experience in financial advisory, understanding these terms upfront is non-negotiable. It helps you grasp the full implications of the loan agreement.

Why People Consider Using Their Car For A Loan

The reasons individuals turn to car title loans are diverse, often stemming from immediate, pressing financial needs combined with limited access to conventional credit.

Emergency Financial Needs

Life is unpredictable. A sudden medical emergency, an unexpected car repair, or a looming utility shut-off can create immediate cash flow problems. When faced with such urgent situations, a car title loan can seem like a rapid solution to bridge the gap. The speed of approval and disbursement is a significant draw for many.

Poor Credit History

Traditional banks and credit unions heavily rely on credit scores to assess risk. If your credit score is low or non-existent, securing a personal loan can be challenging, if not impossible. Car title lenders, on the other hand, focus more on the value of your vehicle and your ability to repay, making them accessible to those with less-than-perfect credit.

Quick Access to Funds

One of the most appealing aspects of using your car for a loan is the speed. Unlike traditional loans that can take days or even weeks for approval, car title loans can often be approved and funded within the same day. This rapid turnaround is crucial for individuals facing time-sensitive financial crises.

No Traditional Bank Options

For some, their financial situation simply doesn’t align with the strict requirements of mainstream lenders. This could be due to a lack of banking history, self-employment with irregular income, or a history of past financial difficulties. Car title loans offer an alternative when other doors are closed.

The Application Process: Step-by-Step

Applying for a car title loan is typically a streamlined process designed for speed. However, understanding each step ensures you are prepared and can navigate it effectively.

Eligibility Requirements

Before you even start, ensure you meet the basic criteria. The most fundamental requirement is owning your vehicle outright, meaning you have a clear title with no outstanding liens.

Other common requirements include being at least 18 years old, possessing a valid government-issued ID, and having proof of income. Some lenders may also require proof of residency and vehicle insurance.

Documents Needed

Gathering your documents beforehand will significantly speed up the process. You’ll typically need:

- Your Car’s Clear This is paramount. It must be in your name and free of any liens.

- Government-Issued Photo ID: A driver’s license or state ID.

- Proof of Income: Pay stubs, bank statements, or other verifiable income sources.

- Proof of Residency: Utility bills or lease agreements.

- Vehicle Registration and Insurance: Some lenders require these.

- References: Occasionally requested, though less common.

Online vs. In-Person Application

You usually have two main options for applying:

- Online Application: Many lenders offer convenient online forms where you can submit your details and upload documents. This is often the fastest way to get pre-approved.

- In-Person Application: Visiting a physical branch allows for face-to-face interaction, vehicle inspection on-site, and often immediate fund disbursement if approved.

Pro Tips for a Smooth Application

- Clean Your Car: While not always required, a well-maintained and clean car can sometimes lead to a higher appraisal value, potentially increasing your loan amount.

- Know Your Car’s Value: Do a quick online search (e.g., Kelley Blue Book, NADAguides) to get an estimate of your car’s trade-in and private party value. This helps you gauge reasonable loan offers.

- Read Reviews: Before applying, research potential lenders. Look for customer reviews and check their standing with consumer protection agencies.

- Ask Questions: Don’t hesitate to clarify anything you don’t understand about the terms, fees, or repayment schedule.

Based on my experience, a little preparation goes a long way in ensuring a stress-free application and preventing misunderstandings down the line.

Benefits of Using Your Car For A Loan

While carrying significant risks, car title loans do offer certain advantages that make them a viable option for some individuals in specific circumstances.

Speed and Accessibility

The primary benefit is the rapid access to funds. When you need cash quickly, traditional banks often can’t compete with the turnaround time of car title lenders. Approvals can happen in minutes, and funds can be disbursed on the same day. This speed is invaluable during true financial emergencies.

Credit Score Not the Primary Factor

For those with a less-than-perfect credit history, car title loans offer a lifeline. Lenders primarily focus on the value of your collateral (your car) and your ability to repay, rather than extensively scrutinizing your credit report. This opens up borrowing opportunities for many who would otherwise be denied.

You Keep Driving Your Car

Unlike pawn loans where you surrender the item, with a car title loan, you retain possession and use of your vehicle. This is a significant advantage, as your car is often essential for work, errands, and daily life. You give up the title temporarily, not the car itself.

The Risks and Downsides You Must Know

Despite the potential benefits, using your car for a loan comes with substantial risks that borrowers must fully understand before committing. This is where informed decision-making truly matters.

High Interest Rates (APR)

This is arguably the most significant drawback. Car title loans are notorious for their extremely high Annual Percentage Rates (APRs), often ranging from 100% to 300% or even higher. To put this into perspective, a typical credit card APR might be 15-25%. These exorbitant rates mean that the cost of borrowing can quickly outweigh the principal amount, leading to a much larger total repayment than you initially borrowed.

Pro tips from us: Always calculate the total cost of the loan, not just the monthly payment. A $1,000 loan with a 200% APR repaid over 3 months could easily cost you an additional $500 or more in interest and fees.

Risk of Repossession

Since your car’s title is used as collateral, defaulting on the loan means the lender has the legal right to repossess your vehicle. This is a very real and devastating consequence. Losing your primary mode of transportation can lead to further financial hardship, impacting your ability to get to work, run errands, and maintain your independence.

Common mistakes to avoid are underestimating your ability to repay. Always have a clear, realistic plan for how you will make every payment on time.

Debt Cycle Potential

The high costs and short repayment terms can easily trap borrowers in a cycle of debt. If you can’t repay the loan in full, lenders might offer to "roll over" the loan, meaning you pay only the interest and extend the loan term. This incurs new fees and more interest, making it incredibly difficult to escape the debt spiral. Each rollover increases the total cost of the loan exponentially.

Impact on Credit (If Defaulted)

While your credit score isn’t the primary factor for approval, defaulting on a car title loan can still negatively impact your credit. If the lender reports the default to credit bureaus or sells the debt to a collection agency, it will appear on your credit report, making it harder to obtain credit in the future.

Regulatory Variations

The legality and regulation of car title loans vary significantly by state. Some states have strict caps on interest rates and loan amounts, while others have very few protections for consumers. It’s crucial to understand the laws in your specific state before applying.

Responsible Borrowing: Navigating Car Title Loans Safely

If you decide that using your car for a loan is your only viable option, it’s paramount to approach it with extreme caution and a strategy for responsible borrowing.

Assess Your Repayment Ability Realistically

Before you sign anything, conduct a thorough, honest assessment of your financial situation. Can you genuinely afford to repay the loan, including all interest and fees, within the agreed-upon timeframe? Create a detailed budget that accounts for all your income and expenses. Do not rely on uncertain future income.

Compare Lenders Thoroughly

Don’t jump at the first offer. Shop around and compare offers from multiple lenders. Look beyond just the advertised loan amount. Compare APRs, fees, repayment terms, and any penalties for late payments or early repayment.

Pro tips from us: Use online comparison tools or call different lenders to get detailed quotes. Transparency is key.

Understand the Fine Print

Every loan agreement has fine print for a reason. Read the entire contract carefully before signing. Pay close attention to:

- The total loan amount and repayment schedule.

- The Annual Percentage Rate (APR) – this is the true cost.

- All associated fees (origination fees, processing fees, late payment fees, repossession fees).

- The terms for default and repossession.

- Any clauses about loan rollovers or extensions.

Ask Questions

If there’s anything you don’t understand in the contract, ask the lender to explain it clearly. Do not sign until you are completely comfortable with every clause and number. A reputable lender will be transparent and willing to answer your questions.

Pro tips from us: Have a clear repayment plan. Know exactly where the money for each payment will come from. This proactive approach can prevent future financial distress.

Alternatives to Car Title Loans

Given the high risks associated with car title loans, exploring alternatives should always be your first step. Many other financial solutions might be safer and more affordable.

Personal Loans (Unsecured/Secured)

- Unsecured Personal Loans: These don’t require collateral and are based on your creditworthiness. While harder to get with poor credit, some lenders specialize in loans for those with fair credit. Interest rates are significantly lower than title loans.

- Secured Personal Loans: If you have other assets (like savings, CDs, or even jewelry), you might be able to secure a personal loan with lower interest rates than a title loan.

Credit Union Loans

Credit unions are non-profit organizations that often offer more favorable loan terms and lower interest rates than traditional banks, especially for members. They may be more willing to work with individuals with less-than-perfect credit. Membership is usually easy to obtain.

Borrowing from Friends or Family

While it can be awkward, borrowing from trusted friends or family can be an interest-free or low-interest solution. It’s crucial to treat this as a formal loan, drawing up an agreement with clear repayment terms to avoid damaging relationships.

Community Assistance Programs

Many non-profit organizations, charities, and government agencies offer financial assistance for specific emergencies like utility bills, rent, or medical expenses. Searching for "emergency financial assistance near me" can yield valuable local resources.

Payday Alternative Loans (PALs)

Offered by federal credit unions, PALs are small loans designed as an alternative to high-cost payday loans. They have lower interest rates (capped at 28% APR), longer repayment terms, and lower application fees. They are a much safer option than title loans for short-term needs.

Building an Emergency Fund

The best long-term solution to avoid needing high-cost loans is to build an emergency fund. This involves setting aside money specifically for unexpected expenses. Even small, consistent contributions can grow into a significant buffer over time. can provide detailed steps.

Choosing the Right Lender

If, after careful consideration of alternatives, you determine a car title loan is your only option, selecting a reputable and transparent lender is critical.

Reputation and Reviews

Research potential lenders extensively. Check online reviews, look for complaints with the Better Business Bureau (BBB), and search for any regulatory actions against them. A lender with a long history of positive customer feedback and transparent practices is always preferable.

Transparency in Terms

A trustworthy lender will be completely upfront about all loan terms, including the APR, all fees, and the repayment schedule. They should provide a clear, easy-to-understand contract without hidden clauses. Be wary of any lender who pressures you to sign quickly or avoids answering direct questions.

Customer Service

Good customer service is indicative of a professional and ethical business. Test their responsiveness and helpfulness before committing. Are they easy to reach? Do they provide clear answers? This can be crucial if you encounter issues during your repayment period.

State Licensing

Ensure the lender is properly licensed to operate in your state. This provides a layer of consumer protection. You can usually verify a lender’s license through your state’s financial regulatory authority website. For instance, the Consumer Financial Protection Bureau (CFPB) offers resources and information on financial products and consumer rights, which can be a valuable external source for understanding your options and protections.

Conclusion: Drive Your Decisions with Knowledge

Using your car for a loan, specifically through car title loans, can provide a rapid influx of cash when traditional options are out of reach. However, this convenience comes with substantial risks, primarily high interest rates and the very real possibility of losing your vehicle if you default.

Our ultimate mission here is not to discourage you from seeking solutions, but to equip you with comprehensive knowledge. By understanding how these loans work, their inherent benefits and dangers, and the array of available alternatives, you can make a truly informed decision that safeguards your financial well-being. Always prioritize responsible borrowing, thoroughly research your options, and never hesitate to ask questions. Your financial future deserves careful consideration and strategic planning.

We encourage you to explore other articles on our blog, such as , to further enhance your financial literacy and make the best choices for your personal circumstances.