Driving Dreams Forward: Your Ultimate Guide to Local Bad Credit Car Loans

Driving Dreams Forward: Your Ultimate Guide to Local Bad Credit Car Loans Carloan.Guidemechanic.com

Needing a reliable vehicle is often a necessity, not a luxury. It’s essential for commuting to work, taking children to school, running errands, and simply navigating daily life. However, for many individuals, the journey to car ownership hits a significant roadblock: a less-than-perfect credit score. The thought of applying for a car loan with bad credit can feel daunting, leading to frustration and the belief that approval is impossible.

But what if we told you that having bad credit doesn’t automatically close the door to car ownership? There’s a viable path forward, and it often begins right in your own community. This comprehensive guide will demystify local bad credit car loans, offering you a detailed roadmap to finding financing, understanding the process, and ultimately, driving away in a vehicle that meets your needs. We’ll explore every facet, from preparation to post-purchase, ensuring you’re equipped with the knowledge to make informed decisions and transform a challenging situation into an opportunity.

Driving Dreams Forward: Your Ultimate Guide to Local Bad Credit Car Loans

What Exactly Are Local Bad Credit Car Loans?

When we talk about "bad credit car loans," we’re generally referring to what the financial industry calls "subprime auto loans." These are loans extended to borrowers whose credit scores fall below a certain threshold, typically FICO scores under 620. Mainstream lenders might shy away from these applicants due to perceived higher risk.

However, a specialized segment of the lending market is dedicated to serving individuals with less-than-ideal credit histories. These lenders, often found locally, understand that a credit score doesn’t always tell the full story of an individual’s financial capability or their commitment to making payments. They look beyond the numbers to assess your current financial stability and willingness to pay.

Focusing on local bad credit car loans offers distinct advantages over purely online options. When you work with a local lender or dealership, you can engage in face-to-face discussions, build rapport, and explain your situation in detail. This personal interaction can be invaluable, especially when your credit history requires a more nuanced understanding than an algorithm can provide. Local institutions are often more flexible and might have a deeper understanding of the local economy and its unique challenges.

Why Your Credit Score Matters (But Isn’t Everything)

Your credit score is essentially a three-digit number that summarizes your credit risk at a specific point in time. It’s generated from the information in your credit report and is used by lenders to quickly assess your likelihood of repaying a loan. A higher score typically means lower risk and, consequently, better loan terms.

For individuals seeking auto loans with bad credit, a low score signals to lenders that there might have been past financial difficulties, such as missed payments, defaults, or bankruptcies. This perception of higher risk is precisely why traditional banks often decline applications from those with poor credit. They operate under strict guidelines and prioritize borrowers with proven track records of responsible credit management.

However, it’s crucial to understand that a low credit score isn’t an insurmountable barrier to obtaining a car loan. While it does influence the terms you’ll be offered, it doesn’t preclude you from getting approved. Many lenders specialize in car loans for bad credit because they recognize that life happens, and people deserve a second chance. They focus on your current ability to pay, your employment history, and other factors that demonstrate stability, even if your past credit history is rocky.

Understanding the Challenges and Opportunities

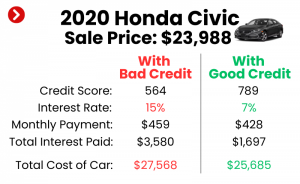

Securing auto loans with bad credit comes with its unique set of challenges. The most prominent among these is typically a higher Annual Percentage Rate (APR), which translates to more interest paid over the life of the loan. Lenders charge higher interest rates to compensate for the increased risk they assume when lending to borrowers with poor credit. You might also find loan terms to be stricter, with potentially shorter repayment periods or requirements for a larger down payment.

Despite these challenges, pursuing a bad credit car loan presents a significant opportunity. Successfully managing and repaying this loan can be a powerful tool for rebuilding your credit score. Each on-time payment you make is reported to credit bureaus, demonstrating your improved financial responsibility. Over time, this positive payment history can significantly boost your score, opening doors to better financial products and lower interest rates in the future.

Based on my experience, many individuals view their first bad credit car loan as a stepping stone. It’s not just about getting a car; it’s about proving your creditworthiness and setting yourself on a path toward financial recovery. This perspective transforms a perceived obstacle into a strategic opportunity for long-term financial health.

Preparing for Your Local Bad Credit Car Loan Journey

Thorough preparation is the cornerstone of a successful car loan application, especially when you’re navigating the complexities of bad credit. Taking the time to organize your finances and understand your standing will significantly improve your chances of approval and help you secure more favorable terms.

Know Your Credit Report Inside Out

Before you even step foot into a dealership or lender’s office, pull your credit reports from all three major bureaus: Experian, Equifax, and TransUnion. You can do this for free annually at AnnualCreditReport.com. Review each report meticulously for any inaccuracies or errors.

Pro tips from us: Disputing and correcting errors can sometimes lead to an immediate, albeit small, bump in your credit score. Even a few points can make a difference in a lender’s perception. Understanding what’s on your report also helps you anticipate what lenders will see and allows you to explain any past issues proactively.

Assess Your True Budget

One of the common mistakes to avoid is falling in love with a car you can’t truly afford. Beyond the monthly payment, remember to factor in insurance, fuel, maintenance, and potential repair costs. Create a realistic monthly budget that accounts for all your expenses, ensuring you can comfortably make your car payments without stretching yourself too thin.

Pro tips from us: Use an online car payment calculator to estimate various scenarios based on different interest rates and loan terms. This will give you a clearer picture of what kind of monthly payment is sustainable for your financial situation. Remember, the goal is not just to get a car, but to keep it without financial stress.

Gather Essential Documents

Lenders specializing in bad credit car loans will require extensive documentation to verify your identity, income, and residence. Having these documents ready and organized will streamline the application process and demonstrate your preparedness.

Typically, you’ll need:

- Proof of Identity: Valid driver’s license, passport, or state ID.

- Proof of Income: Recent pay stubs (last 2-3 months), bank statements, or tax returns if self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- References: Sometimes personal or professional references are requested.

- Down Payment: Proof of funds if you plan to make a down payment.

Having everything in order sends a strong signal to lenders that you are serious and responsible, which can be particularly impactful when your credit history is a concern.

Finding the Right Local Lender or Dealership

The search for local bad credit car loans requires a targeted approach. Not all lenders are equipped or willing to work with borrowers who have challenging credit. Knowing where to look is half the battle.

Specialized Dealerships: "Buy Here, Pay Here" (BHPH)

"Buy Here, Pay Here" dealerships are often the first place many people with bad credit consider. These dealerships act as both the seller and the lender, meaning they finance the car directly themselves rather than through a third-party bank. This can be a quick path to approval since their lending decisions are based solely on their internal criteria, often prioritizing your income and ability to pay over your credit score.

While BHPH dealerships can be a lifeline, it’s crucial to approach them with caution. They typically charge significantly higher interest rates, and the cars offered might be older models with potentially higher maintenance needs. Always read the fine print carefully, understand the total cost, and inspect the vehicle thoroughly.

Local Banks & Credit Unions

Don’t overlook your local banks and, especially, credit unions. While they may have stricter lending criteria than BHPH lots, credit unions are member-owned and often more flexible and willing to work with members who have bad credit, particularly if you have an existing relationship with them. They tend to offer more competitive rates and personalized service than larger national banks.

Building a relationship with a local financial institution can pay dividends. They might be more understanding of your situation and offer solutions tailored to your circumstances. It’s always worth applying with them first, as their terms are generally more favorable.

Online Aggregators (with a Local Focus)

While the goal is "local," some online platforms specialize in connecting borrowers with local dealerships or lenders who work with bad credit. These platforms can be a good starting point for finding options in your area without having to visit multiple places physically. However, remember that the personal interaction aspect is key when dealing with bad credit. Use these tools to identify potential local partners, but always follow up with a direct, in-person visit if possible.

Pro tips from us: Before committing to any lender, read reviews online. Look for testimonials regarding their transparency, customer service, and willingness to work with borrowers in similar situations. Word-of-mouth referrals from trusted friends or family can also lead you to reputable local establishments.

Strategies to Improve Your Approval Chances & Terms

Even with bad credit, there are proactive steps you can take to strengthen your loan application and potentially secure better terms. These strategies demonstrate your commitment and reduce the lender’s perceived risk.

Make a Significant Down Payment

One of the most effective ways to improve your approval chances for auto loans with bad credit is to offer a substantial down payment. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also shows the lender that you are serious about the purchase and have some financial stability.

Based on my experience, a down payment of 10-20% of the car’s value is ideal, but any amount you can contribute will help. It not only increases your approval odds but also reduces your monthly payments and the total interest paid over the life of the loan.

Find a Co-signer

If you have a trusted friend or family member with good credit who is willing to co-sign your loan, this can significantly boost your chances of approval and potentially secure a lower interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

However, understand the gravity of this decision. A co-signer’s credit is on the line, and any missed payments will negatively impact both your credit scores. It’s a serious commitment for both parties, so ensure open communication and a clear understanding of the responsibilities involved.

Choose the Right Car

When you’re seeking car loans for bad credit, being realistic about your vehicle choice is paramount. Aim for a reliable, practical, and affordable used car rather than a brand-new, high-end model. Lenders are more comfortable financing a less expensive vehicle, as it represents lower risk.

Focus on a car that meets your essential needs, is fuel-efficient, and has a good reputation for reliability. Avoiding luxury models or cars with extensive customization will make the loan more accessible and your payments more manageable.

Show Proof of Stable Income

Lenders want to see a consistent and reliable income source. This is often more important than your credit score when dealing with subprime loans. Demonstrate that you have been steadily employed for an extended period, preferably six months to a year or more, at your current job.

The longer your employment history and the more stable your income, the more confident lenders will be in your ability to make regular payments. Be prepared to provide multiple pay stubs or bank statements to verify your income.

The Application Process: What to Expect

Once you’ve done your homework and found a promising local lender or dealership, it’s time for the application process. While it might seem intimidating, understanding each step can ease your concerns.

You’ll typically start by filling out a loan application, either online or in person. This form will ask for personal details, employment history, income information, and your residential history. Be honest and accurate with all information provided. Lenders will verify these details, and any discrepancies could lead to delays or rejection.

After submitting your application, you’ll likely have a discussion with a finance manager. This is your opportunity to explain any specific challenges in your credit history or highlight positive aspects of your current financial situation. Don’t be afraid to be transparent; honesty builds trust.

Even with bad credit, there might be room for negotiation, especially regarding the total price of the vehicle or specific loan terms. While interest rates might be less flexible, you can still discuss down payment options, trade-in values, or add-on features. Common mistakes to avoid are rushing through this discussion or feeling pressured to sign anything you don’t fully understand. Take your time, ask questions, and ensure all your concerns are addressed.

Understanding Your Loan Terms and Conditions

When you’re offered a loan, it’s absolutely critical to understand every aspect of the terms and conditions before you sign. This is particularly true for bad credit car loans, where rates and fees can be higher.

Interest Rates (APR)

The Annual Percentage Rate (APR) is the most significant factor determining the total cost of your loan. For bad credit loans, expect a higher APR compared to prime loans. This is the lender’s way of mitigating risk. Ensure you understand how the APR translates into your monthly payment and the total interest you’ll pay over the loan’s lifetime.

Loan Term

The loan term refers to the length of time you have to repay the loan, typically ranging from 36 to 72 months, or even longer. A longer loan term means lower monthly payments but results in paying significantly more interest over time. Conversely, a shorter term means higher monthly payments but less total interest paid. Choose a term that balances affordability with the overall cost of the loan.

Fees and Charges

Scrutinize the loan agreement for any additional fees or charges. These can include origination fees, documentation fees, or prepayment penalties. Some lenders might include optional add-ons like extended warranties or GAP insurance. While some of these might be beneficial, ensure you understand what you’re paying for and if it’s truly necessary.

Total Cost of the Loan

Beyond the monthly payment, calculate the total cost of the loan. This includes the principal amount borrowed, plus all the interest and fees. This comprehensive view will give you the clearest picture of what you’re truly committing to.

Pro tips from us: Never sign a loan agreement if you have unanswered questions or feel rushed. Take the document home if necessary, and review it carefully. If possible, have a trusted advisor or financially savvy friend look it over with you. Knowledge is power, especially when making a significant financial commitment like an auto loan.

Post-Approval: Using Your Car Loan to Rebuild Credit

Getting approved for a bad credit car loan is a significant achievement, but the journey doesn’t end there. In fact, this is where the real opportunity to improve your financial standing begins. Your car loan can become a powerful tool for credit rebuilding.

The most critical step is to make every single payment on time, every month. Consistency is key. Each on-time payment is reported to the major credit bureaus, creating a positive entry on your credit report. Over several months, this consistent positive behavior will gradually, but surely, start to raise your credit score.

Based on my experience, individuals who diligently make their car payments often see a noticeable improvement in their credit scores within 12-18 months. This improvement can open doors to better financial products, such as credit cards with lower interest rates or even the possibility of refinancing your car loan at a more favorable rate down the line. Refinancing can significantly reduce your monthly payments and the total interest paid, further solidifying your financial recovery.

Set up automatic payments if possible, or create reminders to ensure you never miss a due date. Think of each payment not just as paying for your car, but as an investment in your financial future.

Common Mistakes to Avoid When Seeking Local Bad Credit Car Loans

Navigating the world of local bad credit car loans can be tricky. Being aware of common pitfalls can save you money, time, and future headaches.

- Not Checking Your Credit Report: Skipping this crucial step leaves you vulnerable to errors and unaware of your actual standing. You can’t effectively negotiate or understand offers if you don’t know your starting point.

- Applying Everywhere: Each time you apply for a loan, a hard inquiry is made on your credit report, which can temporarily lower your score. Spreading applications across many lenders in a short period can make your credit look worse. Focus on a few reputable lenders you’ve researched.

- Not Budgeting Properly: Overestimating what you can afford leads to financial strain and potential default. Remember to factor in all car-related expenses, not just the monthly payment.

- Ignoring the Total Cost: Focusing solely on the monthly payment can be misleading. A lower monthly payment often means a longer loan term and significantly more interest paid over time. Always ask for the total cost of the loan.

- Settling for the First Offer: Even with bad credit, it’s wise to compare offers from a few different local lenders or dealerships. The first offer might not always be the best, and a little comparison shopping can save you thousands.

- Hiding Information: Being dishonest about your income, employment, or credit history will only hurt you. Lenders will verify this information, and any falsehoods will lead to immediate rejection or even legal consequences. Transparency is always the best policy.

Conclusion

Obtaining a car loan with bad credit can seem like an uphill battle, but it is far from an impossible feat. By understanding the nuances of local bad credit car loans, preparing diligently, and approaching the process strategically, you can absolutely achieve your goal of car ownership. This journey is not just about getting a set of wheels; it’s a powerful opportunity to demonstrate financial responsibility, rebuild your credit, and pave the way for a more secure financial future.

Remember, patience, thorough research, and a clear understanding of your financial situation are your greatest assets. Don’t be discouraged by past credit challenges. Instead, empower yourself with the knowledge from this guide and embark on your car loan journey with confidence. Your path to driving dreams forward starts now, right in your local community.