Driving Dreams Home: The Ultimate Guide to Securing an NRI Car Loan in India

Driving Dreams Home: The Ultimate Guide to Securing an NRI Car Loan in India Carloan.Guidemechanic.com

For Non-Resident Indians (NRIs) living abroad, the allure of owning a car in their homeland often represents more than just convenience; it symbolizes connection, comfort, and a seamless integration into life back home during visits. Whether it’s for your family’s use, for your own comfort when you return, or as a strategic investment, securing a car loan in India as an NRI can seem like navigating a labyrinth. Many NRIs find themselves wondering about the specific requirements, processes, and the best financial avenues available.

This comprehensive guide is meticulously crafted to demystify the NRI car loan landscape in India. As expert financial content writers and experienced advisors in the NRI finance sector, we understand the unique challenges and opportunities you face. Our goal is to equip you with all the essential knowledge, practical insights, and insider tips to make your dream of driving an Indian car a smooth reality. Get ready to embark on a journey that will not only answer all your questions but also empower you to make informed decisions.

Driving Dreams Home: The Ultimate Guide to Securing an NRI Car Loan in India

Understanding the NRI Car Loan Landscape: More Than Just a Loan

Before diving into the specifics, it’s crucial to grasp what an NRI car loan truly entails and why it’s a specialized financial product. It’s not just a standard car loan; it’s a facility designed with the unique financial and residential status of Non-Resident Indians in mind.

What Exactly is an NRI Car Loan?

An NRI car loan is a specific financial product offered by Indian banks and Non-Banking Financial Companies (NBFCs) to individuals who hold Indian passports but reside outside the country for employment, business, or vocational purposes. It allows these individuals to purchase a new or used car in India, often for their own eventual use or for their family members residing in India. The key differentiator lies in the eligibility criteria, documentation, and sometimes, the repayment mechanisms, which are tailored to the NRI’s overseas income and residential status.

This specialized loan product acknowledges the fact that NRIs have a distinct financial footprint. Their income is typically earned in foreign currency, their credit history might be primarily overseas, and their physical presence in India is often limited. Therefore, lenders have developed bespoke solutions to mitigate the perceived risks associated with lending to someone who is not physically present in the country for most of the year.

Why is it a Specialized Product?

The specialization of NRI car loans stems from several factors:

- Residential Status & Verification: Lenders need to verify the NRI status according to FEMA (Foreign Exchange Management Act) guidelines. This often requires specific documentation like passports, visas, and overseas address proofs.

- Income Source & Repayment: The primary source of income is overseas, which can introduce complexities related to currency conversion and transfer. Repayment typically needs to happen through NRE (Non-Resident External) or NRO (Non-Resident Ordinary) accounts, ensuring compliance with foreign exchange regulations.

- Credit History Assessment: An NRI might have an excellent credit history in their country of residence but a limited or non-existent one in India. Lenders need alternative methods to assess creditworthiness, often relying on co-applicants or robust income proofs.

- Logistical Challenges: The physical distance can make the application, verification, and disbursement process more challenging. This is where mechanisms like a Power of Attorney (POA) become indispensable.

Based on my experience, many NRIs initially approach standard loan products, only to find that their residential status poses a barrier. Recognizing the distinct nature of an NRI car loan from the outset will save you significant time and effort in your application journey.

Eligibility Criteria: Are You Ready to Drive Your Dream Car?

Understanding the eligibility requirements is the first critical step towards securing your NRI car loan. While specific criteria can vary slightly between lenders, a common set of benchmarks applies across the board.

1. NRI Status Definition:

You must officially qualify as a Non-Resident Indian under the Foreign Exchange Management Act (FEMA). Generally, an Indian citizen is considered an NRI if they reside outside India for more than 182 days during the financial year. This is a fundamental requirement that underpins the entire loan application process. Banks will meticulously check your passport and visa stamps to confirm your residential status.

2. Age Requirements:

Typically, applicants must be between 21 and 60-65 years of age at the time of loan application, with the maximum age extending up to 70 years by the time the loan matures. This ensures that the applicant has sufficient working years remaining to comfortably repay the loan. Younger applicants may need a co-applicant to strengthen their profile.

3. Income & Employment Stability:

This is perhaps the most crucial criterion. Lenders look for a stable and sufficient income source in foreign currency.

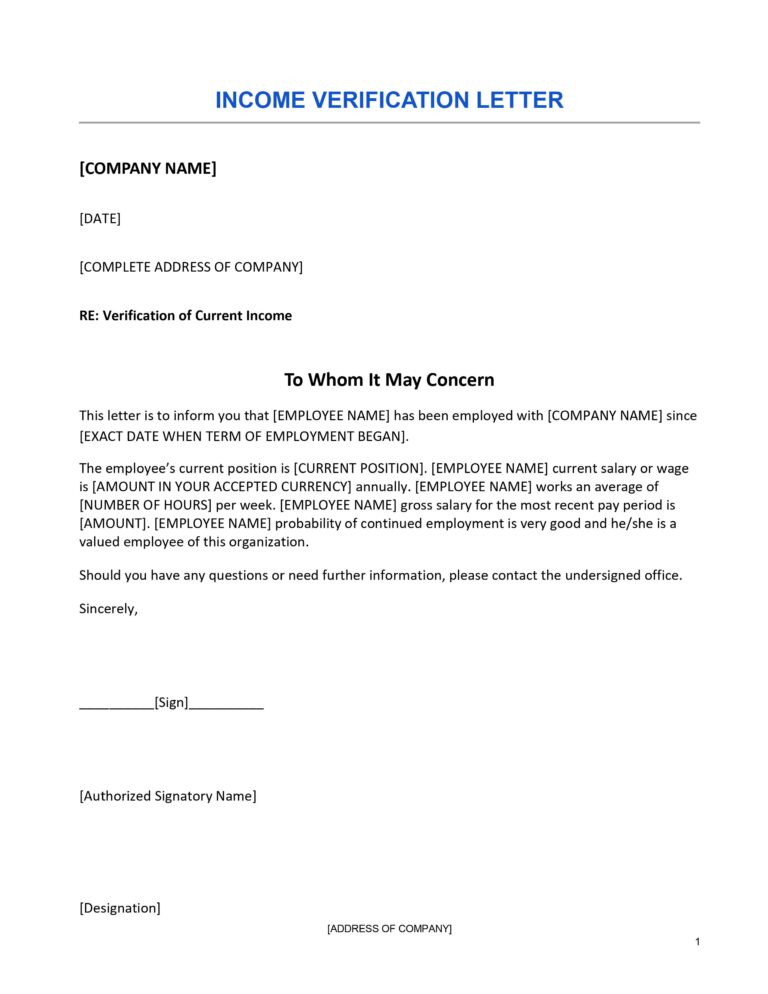

- For Salaried NRIs: You’ll typically need to show a consistent employment history, often a minimum of 1-2 years overseas. Banks usually stipulate a minimum monthly income, which varies depending on the loan amount and the country of residence. They want to see proof of regular salary credits into your overseas bank account.

- For Self-employed NRIs: The requirements are often more stringent, demanding a longer period of business stability (e.g., 2-3 years) and comprehensive financial statements, tax returns from your country of residence, and proof of business registration. The income stability here is paramount to the lender.

4. CIBIL Score/Credit History in India:

While your overseas credit score is important, Indian lenders primarily look at your CIBIL score or any existing credit history in India. If you have previous loans or credit cards in India and have maintained a good repayment record, it significantly boosts your eligibility. For those with no credit history in India, lenders will place more emphasis on your overseas income, employment stability, and the strength of your co-applicant.

5. Co-applicant Requirements: Often Essential for NRIs:

Many banks mandate a resident Indian co-applicant for NRI car loans. This is a critical risk mitigation strategy for lenders. The co-applicant acts as a guarantor and is equally liable for the loan repayment.

- Who can be a co-applicant? Usually, immediate family members like parents, spouse, or siblings residing in India are accepted.

- What strengthens a co-applicant’s profile? A co-applicant with a stable income, good CIBIL score, and sufficient assets in India significantly improves your chances of approval and can sometimes even help secure better interest rates.

- Pro Tip: Choosing a co-applicant with a strong financial standing and a clear credit history in India is one of the best strategies to streamline your NRI car loan application. Their creditworthiness effectively bridges any gaps in your Indian credit profile.

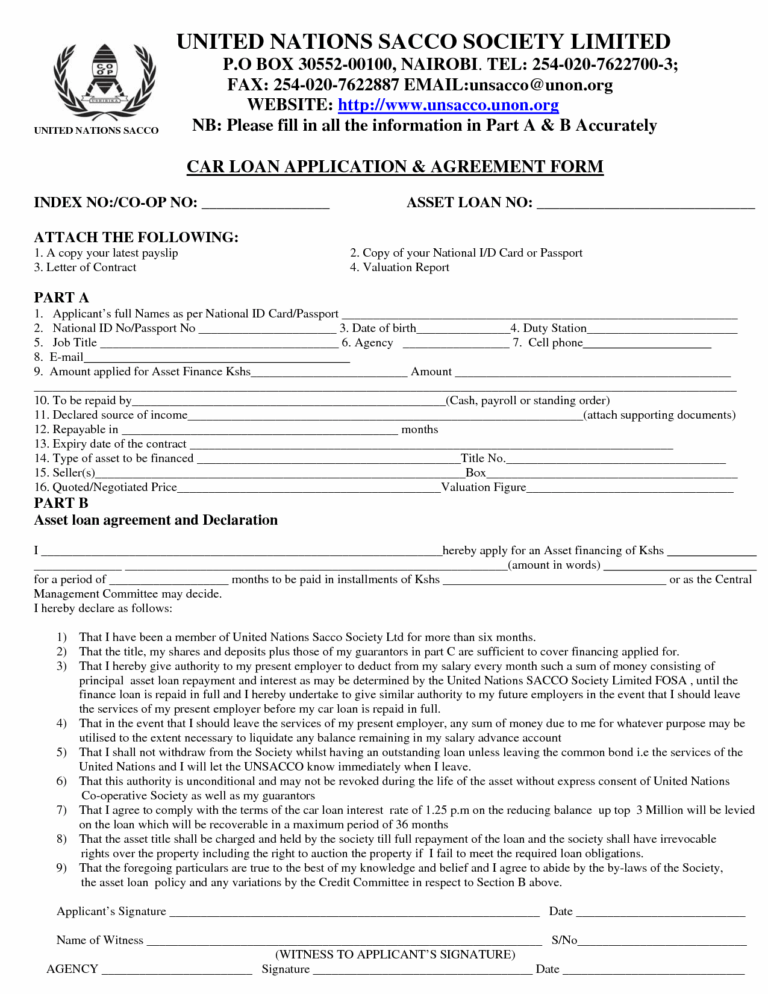

Documentation Demystified: What You’ll Need to Prepare

The paperwork involved in an NRI car loan can seem daunting, but with proper preparation, it’s manageable. Lenders require a comprehensive set of documents to verify your identity, residential status, income, and ability to repay.

1. Identity Proof:

- Valid Passport (all relevant pages including visa stamps)

- Valid Indian Visa / Work Permit / Residence Permit

- Overseas Citizenship of India (OCI) or Person of Indian Origin (PIO) Card (if applicable)

2. Address Proof:

- Overseas Address Proof: Utility bills (electricity, gas, water), driving license, bank statements, or rental agreement from your country of residence.

- Indian Address Proof: Aadhar Card, Indian Driving License, Utility bills (electricity, landline phone bill) in your name or your co-applicant’s name. This establishes your link to India.

3. Income Proof:

This is where lenders assess your financial capacity to repay the loan.

- For Salaried Individuals:

- Latest 3-6 months’ salary slips.

- Employment contract/appointment letter.

- Latest 1-2 years’ income tax returns from your country of residence.

- Latest 6-12 months’ overseas bank statements reflecting salary credits.

- For Self-employed Individuals:

- Business registration documents.

- Latest 2-3 years’ audited financial statements (Profit & Loss, Balance Sheet).

- Latest 2-3 years’ income tax returns from your country of residence.

- Latest 6-12 months’ overseas bank statements for your business and personal accounts.

4. Bank Account Statements:

- Latest 6-12 months’ NRE/NRO bank account statements in India. These accounts are crucial for loan disbursement and EMI repayments, as all transactions must comply with FEMA regulations.

5. Power of Attorney (POA): When and Why It’s Crucial:

Since you might not be physically present in India for the entire loan process, a Power of Attorney (POA) becomes indispensable.

- What is a POA? It’s a legal document authorizing another person (your resident Indian family member, typically the co-applicant) to act on your behalf for specific tasks, such as signing loan agreements, vehicle registration documents, and other related paperwork.

- Types of POA: A General Power of Attorney (GPA) gives broad powers, while a Special Power of Attorney (SPA) grants specific powers for a particular transaction. For car loans, an SPA specifically detailing the car purchase and loan agreement is usually preferred.

- Attestation: The POA must be duly executed and attested by an Indian Embassy/Consulate in your country of residence or notarized and apostilled as per Hague Convention.

- Common Mistake to Avoid: Submitting an incomplete or improperly attested POA can lead to significant delays. Ensure all details are accurate, the scope of authority is clear, and it’s legally valid in India. Our pro tip is to get the POA drafted by a legal expert in India and then have it executed and attested overseas.

6. Car-Specific Documents:

- Proforma Invoice or Quotation from the authorized car dealer. This document details the make, model, variant, and ex-showroom price of the car you intend to purchase.

- KYC documents of the co-applicant (Aadhar Card, PAN Card, address proof, income proof).

The Application Process: A Step-by-Step Guide to Your Loan Journey

Navigating the application process for an NRI car loan can be streamlined with a clear understanding of each stage. Based on my experience, a methodical approach significantly reduces stress and potential delays.

1. Researching Lenders: Banks vs. NBFCs:

Start by researching various banks and NBFCs in India that offer NRI car loans. Major public and private sector banks like ICICI Bank, HDFC Bank, Axis Bank, State Bank of India, and Kotak Mahindra Bank are prominent players in this segment. Compare their:

- Interest rates (fixed vs. floating)

- Processing fees and other charges

- Eligibility criteria

- Required documentation

- Loan-to-Value (LTV) ratio (the percentage of the car’s value they will finance)

- Customer service, especially their dedicated NRI desks.

2. Pre-approval Checks:

Before submitting a full application, some lenders offer a pre-approval process where they assess your basic eligibility based on initial information. This can give you an idea of the loan amount you might qualify for and helps you budget effectively for your car purchase. It also saves time by ensuring you meet fundamental requirements before gathering all detailed documents.

3. Application Submission:

Once you’ve chosen a lender, you’ll need to fill out the loan application form.

- Online Application: Many banks now offer online application portals, which is convenient for NRIs. You can upload scanned copies of your documents.

- Offline Application (through POA): Alternatively, your resident Indian co-applicant or POA holder can submit the physical application form and documents at a bank branch in India on your behalf.

- Ensure all fields are accurately filled, and all required documents (as detailed in the previous section) are attached.

4. Verification Process:

This is a critical stage where the lender verifies all the information and documents provided.

- Document Verification: The bank’s team will meticulously check the authenticity and validity of all your submitted documents, including your passport, visa, income proofs, and bank statements.

- Co-applicant Verification: The co-applicant’s details, CIBIL score, and income stability will also be thoroughly verified.

- Telephonic Verification: Expect calls to your overseas contact number and possibly to your employer for employment verification. Similarly, your co-applicant in India will undergo verification checks.

- Pro Tip from us: Ensure your contact details (both overseas and Indian) are up-to-date and accessible. Inform your employer that a bank might contact them for verification to avoid any misunderstandings or delays.

5. Loan Sanction & Disbursement:

Upon successful verification and approval, the bank will issue a loan sanction letter. This letter outlines the approved loan amount, interest rate, tenure, EMI amount, and any specific terms and conditions.

- Acceptance: You (or your POA holder) will need to formally accept the sanction letter.

- Disbursement: Once the sanction letter is accepted, and all final formalities (like signing the loan agreement and hypothecation of the car) are completed, the loan amount is typically disbursed directly to the car dealer. The car can then be registered in your name (or jointly with the co-applicant) in India.

Common mistakes to avoid during this process include not fully understanding the terms in the sanction letter or failing to follow up regularly with the bank. Maintaining clear and consistent communication with your chosen bank and your POA holder is key to a smooth process.

Key Factors to Consider When Choosing an NRI Car Loan

Selecting the right NRI car loan isn’t just about getting the lowest interest rate. It involves a holistic evaluation of various factors that impact your overall cost and repayment experience.

1. Interest Rates: Fixed vs. Floating

- Fixed Interest Rate: Your EMI remains constant throughout the loan tenure, providing predictability. This is often preferred by NRIs who want stability in their financial planning, especially given potential currency fluctuations.

- Floating Interest Rate: Your EMI can change based on market interest rate movements (linked to the bank’s MCLR or external benchmarks). While it might offer lower rates initially, it carries the risk of increased payments if rates rise.

- Pro Tip: While a lower interest rate is attractive, consider the stability offered by a fixed rate if you prefer consistent budgeting, especially for long-term loans.

2. Loan Tenure: Flexibility and EMI Impact

Loan tenure refers to the period over which you repay the loan, typically ranging from 1 to 7 years.

- Longer Tenure: Results in lower EMIs, making it more affordable on a monthly basis. However, you end up paying more interest over the loan’s lifetime.

- Shorter Tenure: Means higher EMIs but a significantly lower total interest outgo.

Choose a tenure that aligns with your financial capacity and long-term plans.

3. Processing Fees & Other Charges: Beware of Hidden Costs

Beyond the interest rate, various charges can add to the total cost of your loan.

- Processing Fee: A one-time fee charged by the lender for processing your loan application. This can be a fixed amount or a percentage of the loan.

- Documentation Charges: Fees for preparing loan documents.

- CIBIL Report Charges: Cost for pulling your credit report.

- Prepayment/Foreclosure Charges: Penalties if you decide to repay your loan earlier than scheduled. These can vary widely, so understanding them upfront is crucial if you anticipate early closure.

- Late Payment Penalties: Charges levied for delayed EMI payments.

Always ask for a detailed breakdown of all applicable charges before finalizing your loan.

4. Loan-to-Value (LTV) Ratio:

The LTV ratio indicates the percentage of the car’s ex-showroom price that the bank is willing to finance. For example, an 80% LTV means the bank will finance 80% of the car’s value, and you need to pay the remaining 20% as a down payment. LTVs for NRI car loans can sometimes be slightly lower than for resident Indian loans due to perceived higher risk. A higher LTV means a lower down payment from your side.

5. Prepayment/Foreclosure Options:

Understanding the terms for prepaying or foreclosing your loan is vital.

- Prepayment: Paying a portion of your outstanding loan amount before the due date.

- Foreclosure: Paying off the entire outstanding loan amount before the scheduled tenure ends.

Many loans come with lock-in periods (e.g., 6-12 months) before you can prepay or foreclose, and charges may apply. If you foresee receiving a bonus or other lump sum that could help you clear your loan early, look for lenders with flexible prepayment options and reasonable charges.

6. Customer Service & NRI Desk Support:

Given the geographical distance, dedicated NRI customer service can be invaluable.

- Responsiveness: How quickly do they respond to queries?

- Communication Channels: Do they offer email, international calling, or chat support?

- Dedicated NRI Relationship Manager: Some banks provide a dedicated manager for NRI clients, offering personalized assistance. This can significantly smooth out the process.

Pro Tip: Don’t just compare interest rates in isolation. Create a total cost of ownership calculation, factoring in processing fees, potential prepayment charges, and the convenience of customer service. A slightly higher interest rate might be worth it for a bank that offers superior support and transparency.

Top Banks Offering NRI Car Loans in India

While we refrain from endorsing specific banks, it’s helpful to know which financial institutions are generally recognized for offering robust NRI car loan products. Most major public and private sector banks in India have dedicated NRI banking divisions that cater to these specific needs.

Some of the prominent banks known for their NRI car loan offerings include:

- ICICI Bank: Often cited for its comprehensive NRI services and digital platforms.

- HDFC Bank: Known for its extensive network and competitive rates.

- Axis Bank: Offers a range of financial products for NRIs, including vehicle loans.

- State Bank of India (SBI): As a public sector giant, it has a vast reach and offers various NRI banking solutions.

- Kotak Mahindra Bank: Another private sector bank with a strong NRI presence.

It is crucial to remember that their offerings, interest rates, and specific eligibility criteria can change. We highly recommend visiting the official NRI sections of these banks’ websites or contacting their dedicated NRI customer service desks directly to get the most up-to-date information and compare their current schemes before making a decision.

Advantages of Securing an NRI Car Loan

Opting for an NRI car loan offers several compelling benefits that make it an attractive financial solution for those looking to purchase a vehicle in India.

1. Financial Flexibility: Don’t Deplete Overseas Savings

One of the primary advantages is that it allows you to purchase a car in India without having to liquidate your hard-earned foreign currency savings. Instead of transferring a large lump sum, which might incur conversion charges and impact your overseas investment plans, you can leverage a loan. This preserves your foreign currency assets for other investments or needs in your country of residence, offering greater financial agility.

2. Building Credit History in India:

Securing and diligently repaying an NRI car loan is an excellent way to establish or improve your credit history in India. A strong CIBIL score is crucial for future financial endeavors, such as home loans, personal loans, or even credit cards in India. By demonstrating responsible borrowing and repayment, you lay a solid foundation for your financial future back home. This can be particularly beneficial if you plan to eventually repatriate to India.

3. Convenience for Family in India:

Many NRIs purchase cars primarily for their family members residing in India. An NRI car loan makes this financially feasible without putting a direct strain on the family’s local income. It provides immense convenience and mobility for your loved ones, enhancing their quality of life and ensuring they have reliable transportation. This acts as a tangible support system from afar.

4. Potential Tax Benefits (Consult an Expert):

While car loans for personal use generally don’t offer significant tax benefits in India, there might be specific scenarios or evolving regulations where some deductions are applicable, particularly if the vehicle is used for business purposes by a family member (though this is less common for typical NRI car loans). It’s always advisable to consult with a qualified tax advisor in India to understand any potential tax implications or benefits specific to your situation.

Potential Challenges & How to Overcome Them

While the benefits are clear, NRIs can face unique challenges when applying for a car loan. Being aware of these and knowing how to mitigate them is crucial for a smooth process.

1. Perceived Risk by Lenders:

From a lender’s perspective, an NRI applicant, being physically distant, might represent a higher risk compared to a resident Indian. This perception can sometimes lead to slightly higher interest rates, more stringent documentation requirements, or a mandatory co-applicant.

- How to Overcome: Present a very strong financial profile, including robust income proofs, stable employment history, and a good CIBIL score (if available). A financially strong resident Indian co-applicant is often the best way to mitigate this perceived risk.

2. Documentation Hassles: Distance and Attestation:

Gathering all required documents, especially those needing attestation from Indian embassies or consulates overseas, can be time-consuming and cumbersome. The physical distance can make coordinating paperwork difficult.

- How to Overcome: Start collecting documents well in advance. Create a checklist and tick off each item. Utilize digital copies where possible for initial submissions and then send attested physical copies via reliable courier services. Understand the attestation requirements precisely to avoid rework.

3. Fluctuating Exchange Rates (if repaying from overseas):

If your loan repayment (EMI) is linked to an NRE/NRO account that you regularly fund from your overseas income, fluctuations in the foreign exchange rate can impact your actual cost. A depreciating Indian Rupee against your foreign currency can make EMIs cheaper in foreign currency terms, while an appreciating Rupee can make them more expensive.

- How to Overcome: Monitor exchange rates and, if possible, transfer funds when the exchange rate is favorable. Consider hedging options or maintaining a buffer in your NRE/NRO account to absorb minor fluctuations. Some NRIs prefer to keep their NRE account well-funded to minimize the impact of short-term rate changes.

4. Communication Gaps:

Time zone differences and reliance on email or international calls can sometimes lead to communication delays with bank representatives in India.

- How to Overcome: Designate a specific point of contact at the bank (preferably an NRI relationship manager) and your POA holder in India. Establish clear communication protocols and preferred timings. Leverage online portals and email for documented communication.

- Common Mistake to Avoid: Underestimating the time and effort required for communication and follow-ups. Regular, proactive communication is essential.

Pro Tips for a Smooth NRI Car Loan Experience

Having guided numerous NRIs through this process, we’ve distilled some invaluable pro tips to ensure your car loan journey is as seamless as possible.

- Start Early: The process, from research to disbursement, can take time, especially with international documentation and verification. Begin your research and document gathering several weeks, or even months, before you plan to make the purchase. This buffer time allows you to address any unforeseen challenges without rushing.

- Maintain a Good Credit Score in India: If you have any existing financial dealings in India (e.g., old loans, credit cards), ensure you maintain an impeccable repayment record. A strong CIBIL score will significantly strengthen your loan application and potentially fetch you better interest rates.

- Have a Reliable Co-applicant: As discussed, a financially sound resident Indian co-applicant is often a game-changer. Choose someone with a stable income, good credit history, and whom you trust implicitly, as they share equal responsibility for the loan.

- Understand the Power of Attorney (POA) Thoroughly: This document is your legal proxy. Ensure it is drafted precisely, covers all necessary actions (signing loan documents, vehicle registration, etc.), and is properly attested as per Indian legal requirements. Any ambiguity or error can cause major delays.

- Leverage Digital Platforms: Most leading Indian banks offer robust online banking and application portals for NRIs. Utilize these for initial applications, document uploads, and tracking your application status. This reduces the need for physical presence and speeds up the process.

- Read the Fine Print: Before signing any loan agreement, meticulously read through all terms and conditions. Pay close attention to interest rates, processing fees, prepayment/foreclosure charges, and any clauses related to default. If anything is unclear, seek clarification from the bank or a legal expert.

Future Outlook: The Evolving Landscape for NRIs

The financial landscape for NRIs in India is continually evolving, driven by technological advancements and increasing recognition of the NRI community’s economic contributions. We anticipate further streamlining of processes, with more digital solutions reducing the need for physical paperwork and making applications even more accessible from anywhere in the world. As financial institutions increasingly embrace AI and data analytics, credit assessment for NRIs, even those with limited Indian credit history, is likely to become more sophisticated and efficient. This ongoing shift promises an even smoother experience for NRIs looking to invest in their home country.

Conclusion: Your Road to Driving Home is Clear

Securing an NRI car loan in India might appear intricate at first glance, but with the right knowledge, preparation, and strategic approach, it’s a perfectly achievable goal. From understanding the nuanced eligibility criteria and meticulously preparing your documents to comparing lender offerings and leveraging the support of a reliable co-applicant, every step plays a crucial role in realizing your dream.

This guide has provided you with an in-depth roadmap, drawing upon expert insights to empower you with confidence. By following these recommendations, you’re not just applying for a loan; you’re taking a significant step towards solidifying your connection with India, ensuring convenience for your family, and building your financial presence back home.

Don’t let distance be a barrier to your aspirations. Start your journey today, compare your options diligently, and soon you’ll be driving your dream car on Indian roads. For a deeper dive into managing your finances as an NRI, explore our guide on . If you’re curious about the general car buying process in India, you might find our article on helpful. For official definitions and regulations regarding NRI status, always refer to the Reserve Bank of India (RBI) guidelines on their official website: .