Driving Dreams: How to Secure the Best Car Loan with an 800 Credit Score

Driving Dreams: How to Secure the Best Car Loan with an 800 Credit Score Carloan.Guidemechanic.com

Having an 800 credit score isn’t just a number; it’s a golden ticket in the world of personal finance. When it comes to securing a car loan with an 800 credit score, you’re in an enviable position. This exceptional credit rating signals to lenders that you are a highly responsible borrower, translating into the most favorable terms and the lowest interest rates available.

This comprehensive guide will delve deep into how to leverage your stellar credit to get the absolute best car loan, explore your financing options, and navigate the application process like a pro. We’ll uncover strategies to maximize your savings and avoid common pitfalls, ensuring your car buying experience is as smooth and cost-effective as possible. Prepare to drive away with confidence, knowing you’ve secured a fantastic deal.

Driving Dreams: How to Secure the Best Car Loan with an 800 Credit Score

The Unmatched Power of an 800 Credit Score

An 800 credit score places you in the "exceptional" category, typically reserved for the top tier of borrowers. This score isn’t merely good; it’s a testament to years of diligent financial management, including timely bill payments, low credit utilization, and a diverse credit history. Lenders view this score as a virtually ironclad guarantee of reliability.

What does this mean for a car loan? It means you’re perceived as an extremely low-risk applicant. Lenders are eager to offer you money because they are highly confident you will repay it as agreed. This eagerness directly translates into significant advantages for you, the borrower.

Based on my extensive experience in the financial industry, an 800-plus score essentially puts the ball in your court. You’re not just applying for a loan; you’re dictating the terms to a certain extent. This power dynamic is crucial to understand and harness during your car buying journey.

Unlocking the Best Car Loan Rates and Terms

The most immediate and tangible benefit of a car loan with an 800 credit score is access to the lowest possible Annual Percentage Rates (APRs). Lenders compete fiercely for borrowers with excellent credit, as they represent their safest investments. This competition drives down interest rates for you.

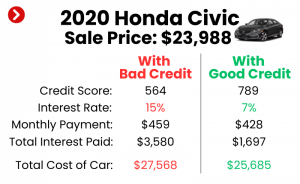

To illustrate, consider this: a borrower with an average credit score (say, 680) might qualify for a 6-7% APR on a new car loan. Someone with a lower score could face double-digit rates. However, with an 800 credit score, you’re looking at rates that often hover in the low single digits, sometimes even under 3% depending on market conditions and the lender.

This difference, seemingly small on a percentage basis, can save you thousands of dollars over the life of the loan. For example, on a $30,000 loan over five years, the difference between a 3% and a 7% APR could mean paying an extra $4,000 or more in interest. Your 800 score protects you from these unnecessary costs.

Furthermore, an exceptional credit score also grants you greater flexibility with loan terms. While shorter terms are often financially smarter (less interest paid), an 800 score might allow you to qualify for a slightly longer term with a still-competitive rate, if that better suits your monthly budget. However, always be cautious about extending loan terms unnecessarily, as it increases the total interest paid.

Navigating Your Options: Where to Get a Car Loan

With an 800 credit score, you have your pick of lenders, each offering unique advantages. Understanding these options is key to securing the most advantageous car loan with an 800 credit score.

Dealership Financing

Many car buyers opt for financing directly through the dealership. This can be incredibly convenient, as you handle the car selection and financing all in one place. Dealerships often work with multiple lenders, acting as intermediaries to find you a loan.

Pros:

- Convenience: Streamlined process, often quick approval.

- Special Offers: Dealerships sometimes have manufacturer-backed low APR promotions, especially for new cars, which are almost exclusively available to top-tier credit holders.

- Negotiation: You can often negotiate the interest rate alongside the car price.

Cons:

- Potential Markups: Dealers might mark up the interest rate offered by the underlying lender to earn a profit.

- Limited Comparison: While they work with multiple lenders, you’re still relying on their selection rather than doing your own comprehensive shopping.

Banks & Credit Unions

Traditional financial institutions are often a prime source for competitive car loans. If you have an existing relationship with a bank or credit union, you might find favorable terms there.

Pros:

- Competitive Rates: Banks and especially credit unions are known for offering very competitive rates to their members, particularly those with excellent credit.

- Relationship Banking: Existing customers may receive preferential treatment or quicker approval processes.

- Personalized Service: You often have a dedicated loan officer who can guide you through the process.

Cons:

- Stricter Requirements: Some banks might have slightly more stringent application processes or require a physical visit.

- Slower Process: Can sometimes take a bit longer than online lenders or dealership financing.

Online Lenders

The digital age has brought a new wave of lenders specializing in online applications and rapid approvals. These platforms can be incredibly efficient for securing a car loan with an 800 credit score.

Pros:

- Speed & Convenience: Apply from anywhere, often get instant pre-approvals.

- Comparison Tools: Many online platforms allow you to compare offers from multiple lenders side-by-side.

- Highly Competitive Rates: Online lenders often have lower overheads, which can translate into better rates for top-tier borrowers.

Cons:

- Less Personal Interaction: The process is largely self-service.

- Beware of Scams: Always ensure you’re using a reputable online lender. Stick to well-known names.

Pro tips from us: Don’t limit yourself to just one type of lender. With an 800 credit score, you have the luxury of choice. Apply for pre-approval from at least two different sources (e.g., your credit union and an online lender) before even stepping foot in a dealership. This strategy gives you leverage and a benchmark rate.

The Car Loan Application Process with Excellent Credit

Even with an 800 credit score, understanding and preparing for the application process is crucial. Your excellent credit will smooth the path, but knowing the steps ensures you maximize its advantage.

The Power of Pre-Approval

This is arguably the single most important step for anyone seeking a car loan with an 800 credit score. Pre-approval means a lender has reviewed your credit and financial situation and has conditionally agreed to lend you a specific amount at a certain interest rate.

Why is pre-approval so powerful? It transforms you into a cash buyer at the dealership. You know exactly how much you can spend and what your interest rate will be before you even start negotiating the car’s price. This eliminates the uncertainty of financing from the car-buying equation. Based on my experience, walking into a dealership with a pre-approval letter in hand immediately signals to the sales team that you’re a serious buyer who means business, often leading to a more straightforward negotiation.

To get pre-approved, you’ll typically fill out an application online or in person. This involves a "soft inquiry" on your credit (which doesn’t affect your score) to provide initial offers, followed by a "hard inquiry" if you decide to proceed with a specific lender. Remember, multiple hard inquiries for the same type of loan within a short period (usually 14-45 days, depending on the scoring model) are generally treated as a single inquiry, so shop around without fear of significantly impacting your score.

Required Documents

While an 800 credit score streamlines things, you’ll still need standard documentation to finalize your loan. Having these ready will expedite the process.

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Pay stubs (from the last 1-2 months), W-2 forms, or tax returns if self-employed. Lenders need to verify you have a stable income to support the monthly payments.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement with your current address.

- Social Security Number: For credit verification.

- Vehicle Information: Once you’ve selected a car, the lender will need its VIN (Vehicle Identification Number) and details.

Understanding Loan Terms: APR, Duration, and Monthly Payments

Even with excellent credit, it’s vital to fully understand the components of your loan offer.

- APR (Annual Percentage Rate): This is the true cost of borrowing, including interest and any fees. Always focus on the APR, not just the interest rate.

- Loan Duration (Term): This is how long you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter term means higher monthly payments but less interest paid overall. A longer term means lower monthly payments but significantly more interest paid over time.

- Monthly Payments: The amount you’ll pay each month. While an 800 score secures a low rate, ensure the monthly payment fits comfortably within your budget, even if you could technically afford more.

Pro tips from us: Always ask for a full amortization schedule if possible. This document details how your payments will be allocated between principal and interest over the loan’s life. It’s a great way to visualize your total cost.

Beyond the Rate: Other Factors to Consider

While a low APR is the primary benefit of a car loan with an 800 credit score, other elements contribute to the overall value of your loan and car purchase. Overlooking these can still lead to less-than-optimal outcomes.

Loan Term Length

As mentioned, loan term length significantly impacts your total cost. With an 800 credit score, you’ll likely qualify for attractive rates across various terms.

- Shorter Terms (36-48 months): These result in higher monthly payments but drastically reduce the total interest paid. You’ll own the car outright sooner, building equity faster.

- Longer Terms (60-72 months, sometimes 84 months): These offer lower monthly payments, which can be appealing for budget management. However, the total interest paid increases substantially, and you risk owing more than the car is worth (being "underwater") as depreciation outpaces your principal payments.

Common mistakes to avoid are extending terms purely for a lower monthly payment if you can comfortably afford a shorter one. The long-term savings are significant.

Down Payment

With an 800 credit score, you might not be required to make a substantial down payment, or even any down payment at all. Lenders trust your ability to repay. However, making a down payment is almost always a smart financial move.

- Reduces Loan Amount: A larger down payment means you’re borrowing less, which directly reduces your monthly payments and the total interest you’ll pay.

- Instant Equity: You start with equity in your vehicle, mitigating the impact of immediate depreciation.

- Better Loan-to-Value (LTV): A strong down payment improves your LTV ratio, which can sometimes even shave a few basis points off your interest rate, even with an 800 score.

Debt-to-Income (DTI) Ratio

Even with a perfect payment history, your debt-to-income (DTI) ratio still matters. This ratio compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to take on new debt.

While an 800 score indicates responsible debt management, if your DTI is excessively high (e.g., over 40-50%) due to other large loans (like a mortgage or student loans), a lender might still hesitate, or at least scrutinize your application more closely. Keep your DTI in mind, even if your credit score is stellar.

Vehicle Choice

The type of vehicle you choose can also influence loan terms, even with an 800 score.

- New vs. Used: New cars often qualify for slightly lower interest rates, sometimes with manufacturer incentives. Used cars might have slightly higher rates due to perceived higher risk, but their lower purchase price often makes them more affordable overall.

- Luxury vs. Economy: While your score gets you the best rate for any car, a very expensive luxury car will naturally lead to a larger loan amount and higher monthly payments. Ensure the car choice aligns with your budget, not just what your credit score can "get" you.

Maximizing Your 800 Score Advantage

Your 800 credit score is a powerful negotiating tool. Don’t leave money on the table by not leveraging it fully.

Negotiation Power

Armed with a pre-approval from an external lender, you have significant leverage at the dealership.

- Benchmark Rate: You know the lowest rate you can get elsewhere. Present this to the dealership and challenge them to beat it. They often can, especially if they want to earn your business and meet sales quotas.

- Separate Negotiations: Negotiate the car price first, independent of the financing. Once you’ve agreed on a price, then discuss financing options, comparing their offers against your pre-approval. Based on my experience, trying to negotiate both at once can lead to confusion and less favorable outcomes.

Shopping Around

Even with pre-approval, don’t stop there. Get firm offers from 2-3 different lenders (banks, credit unions, online lenders) and at least one offer from the dealership. Comparing these offers side-by-side allows you to identify the truly best deal. Look at the APR, any origination fees, and the overall loan terms.

Refinancing (If Necessary)

While less likely for someone starting with an 800 credit score, if for some reason you end up with a less-than-ideal rate (perhaps you bought a car impulsively before getting pre-approved), your excellent credit makes refinancing a straightforward process. You can easily apply for a new loan with a lower APR to pay off the existing one, saving money over time.

Maintaining Your Pristine Credit Score

Securing a great car loan with an 800 credit score is fantastic, but maintaining that score is equally important for future financial endeavors.

- On-Time Payments: The bedrock of good credit. Set up automatic payments to ensure you never miss a due date on your car loan or any other credit account.

- Manage Credit Utilization: Keep your credit card balances low relative to your credit limits. High utilization can temporarily ding your score.

- Monitor Your Credit Report: Regularly check your credit reports from all three bureaus (Experian, Equifax, TransUnion) for errors or fraudulent activity. You can get free annual reports from AnnualCreditReport.com. For more tips on maintaining excellent credit, check out our guide on .

Common Mistakes Even 800-Scorers Make

Even with exceptional credit, it’s possible to make missteps that diminish your advantage. Be vigilant.

- Not Shopping Around for Rates: Assuming the first offer is the best because of your score is a huge mistake. Always compare multiple lenders.

- Focusing Only on the Monthly Payment: A low monthly payment often comes with a longer loan term and significantly more interest paid. Always consider the total cost of the loan.

- Ignoring the Fine Print: Read your loan agreement carefully. Understand all fees, prepayment penalties (rare with excellent credit, but check), and other terms.

- Letting the Dealership Run Too Many Hard Inquiries: While multiple inquiries for a car loan within a specific window count as one for scoring purposes, excessive, unrelated inquiries can be detrimental. Stick to your pre-approvals and limit new applications.

Conclusion: Drive Away with Confidence

A car loan with an 800 credit score puts you in the driver’s seat, literally and financially. Your exceptional credit rating is a powerful asset that demands the best possible terms and the lowest interest rates. By understanding your options, getting pre-approved, shopping around diligently, and negotiating wisely, you can secure a car loan that perfectly complements your financial health.

Don’t settle for anything less than the best. Leverage your 800 credit score to minimize your borrowing costs, maximize your savings, and embark on your next automotive adventure with complete peace of mind. Your financial diligence has paid off; now, enjoy the rewards. You might also find our article on helpful for further insights into loan costs. For official credit score information, refer to .