Driving Dreams in the Desert: Your Comprehensive Guide to Bad Credit Car Loans in Las Vegas

Driving Dreams in the Desert: Your Comprehensive Guide to Bad Credit Car Loans in Las Vegas Carloan.Guidemechanic.com

The shimmering lights of the Las Vegas Strip, the vast expanse of the Mojave Desert, and the bustling energy of this unique city all demand one thing for true freedom: a reliable car. Whether it’s for commuting to work, exploring Red Rock Canyon, or simply navigating the city’s spread-out landscape, personal transportation isn’t just a convenience in Las Vegas – it’s often a necessity. But what if your credit score has taken a hit, leaving you feeling stranded before you even start your engine?

Based on my extensive experience in the auto finance sector and as an expert blogger, the phrase "bad credit" often conjures images of closed doors and rejected applications. However, for residents of Las Vegas, securing a car loan with less-than-perfect credit is not only possible but a journey many successfully undertake every day. This comprehensive guide will illuminate the path, demystifying bad credit car loans in Las Vegas and empowering you with the knowledge to drive away in the vehicle you need. We’ll delve deep into every aspect, ensuring you have all the tools to make an informed decision and rebuild your financial future, one on-time payment at a time.

Driving Dreams in the Desert: Your Comprehensive Guide to Bad Credit Car Loans in Las Vegas

Understanding the Las Vegas Landscape and Your Credit Score

Before we dive into the specifics of obtaining a loan, it’s crucial to understand why a car is so vital in Las Vegas and what "bad credit" truly means in the eyes of a lender.

The Unspoken Necessity: A Car in Las Vegas

Las Vegas is a city built for cars. While the RTC (Regional Transportation Commission) offers bus services, its reach is limited, and travel times can be extensive, especially if you live outside the main tourist corridors or work non-traditional hours. From the sprawling master-planned communities like Summerlin and Henderson to the industrial zones and the sheer distances between attractions, relying solely on public transport or ride-sharing services can quickly become impractical and expensive. A car provides the flexibility and independence essential for life in the Entertainment Capital of the World.

Demystifying "Bad Credit": What Lenders See

Your credit score is a three-digit number that summarizes your creditworthiness, primarily based on your payment history, amounts owed, length of credit history, new credit, and credit mix. For lenders, it’s a quick snapshot of your financial reliability.

- FICO Score Ranges (Commonly Used):

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor (Bad Credit): 300-579

If your score falls into the "Fair" or "Poor" categories, you’re generally considered to have "bad credit." This doesn’t mean you’re a bad person; it simply indicates to lenders that there’s a higher perceived risk associated with lending to you. This might be due to past missed payments, bankruptcies, foreclosures, or a limited credit history (sometimes called "thin file").

The good news? Many lenders in Las Vegas specialize in subprime auto loans and are willing to work with individuals whose scores reflect these challenges. They understand that life happens, and a credit score doesn’t always tell the whole story.

The Reality of Bad Credit Car Loans in Las Vegas

Yes, bad credit car loans are absolutely possible in Las Vegas. The city’s dynamic economy and diverse population mean there’s a significant demand for such financing options. Lenders specializing in this niche understand that people need reliable transportation regardless of their credit history.

What to Expect: The Key Differences

When pursuing a car loan with bad credit, it’s important to set realistic expectations. The terms will likely differ from those offered to someone with excellent credit.

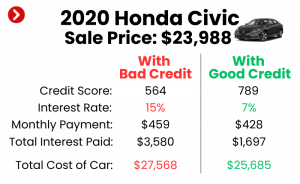

- Higher Interest Rates: This is the most significant difference. Lenders take on more risk, so they compensate by charging a higher interest rate. This means the total cost of your loan will be greater over time.

- Stricter Loan Terms: You might face a shorter repayment period, requiring higher monthly payments, or a longer one to make payments more affordable, which increases the total interest paid.

- Potential for a Larger Down Payment: Lenders often require a more substantial down payment to reduce their risk and show your commitment to the loan.

- Limited Vehicle Choices: You might be guided towards slightly older or less expensive vehicles that pose less risk to the lender if repossession becomes necessary.

Common Misconceptions to Dispel

- "I’ll never get approved." This is simply untrue. While approval isn’t guaranteed, many lenders specifically cater to this market.

- "All bad credit loans are scams." While caution is always advised, reputable lenders offer legitimate poor credit car financing in Vegas. The key is thorough research and understanding the terms.

- "I have to settle for a junk car." Not necessarily. You can still find reliable transportation. The focus should be on mechanical soundness and affordability, not just luxury.

Pro tips from us: Focus on the overall value and reliability of the car, not just the monthly payment. A lower monthly payment over a very long term can mean you pay significantly more in interest.

Finding the Right Lender for Bad Credit Car Loans in Las Vegas

The Las Vegas market offers several avenues for securing an auto loan with bad credit. Knowing where to look and what to expect from each can significantly impact your experience.

1. Dealerships Specializing in Bad Credit

Many dealerships in Las Vegas have dedicated finance departments that work with a network of lenders specializing in subprime auto loans. These dealerships often advertise their willingness to help customers with "all credit types."

- Advantages: Convenience of one-stop shopping (find a car and financing), staff experienced in navigating complex credit situations.

- Disadvantages: May have fewer options for specific car models, could push higher-interest loans if you don’t compare.

When visiting these dealerships, be upfront about your credit situation. They are often equipped to handle it.

2. Online Lenders and Platforms

The digital age has brought forth numerous online platforms and lenders that specialize in bad credit auto loans. Many act as aggregators, connecting you with multiple lenders based on a single application.

- Advantages: Quick pre-approval process, ability to compare multiple offers from the comfort of your home, often less pressure than in-person sales.

- Disadvantages: Less personal interaction, need to be wary of predatory lenders (always check reviews and credentials).

Look for platforms that offer pre-qualification without impacting your credit score (soft inquiry).

3. Local Credit Unions and Banks

While often more stringent, some local credit unions and community banks in Las Vegas might offer options for members with less-than-perfect credit, especially if you have an existing relationship with them.

- Advantages: Potentially lower interest rates than subprime lenders if approved, more personalized service.

- Disadvantages: Stricter eligibility requirements, generally harder to qualify for with very poor credit.

It’s always worth checking with institutions where you have accounts; sometimes loyalty can play a small role.

4. "Buy Here, Pay Here" (BHPH) Lots

These dealerships lend you the money directly, often without a traditional credit check. Payments are made directly to the dealership. You’ll find several of these operations throughout the Las Vegas Valley.

- Advantages: High approval rates, especially for those with very poor credit or no credit history.

- Disadvantages: Typically much higher interest rates, limited vehicle selection (often older models), some may not report payments to credit bureaus, meaning no credit-building benefit.

Common mistakes to avoid are not fully understanding the contract at a BHPH lot. Always scrutinize every line. While a viable option for some, these loans are often a last resort due to their typically unfavorable terms.

Pro tips from us: When vetting any lender, check their reviews, look for transparency in their offerings, and ensure they are licensed to operate in Nevada. A reputable lender will never pressure you into signing anything you don’t understand.

The Application Process for a Bad Credit Car Loan

Applying for a bad credit car loan in Las Vegas doesn’t have to be intimidating. Knowing what lenders look for and having your documents ready can streamline the process.

Required Documents: Be Prepared

Lenders want to confirm your identity, your ability to pay, and your stability. Here’s what you’ll typically need:

- Proof of Identity: Valid driver’s license, state ID.

- Proof of Residence: Utility bill, lease agreement, mortgage statement (confirming your Las Vegas address).

- Proof of Income: Recent pay stubs (usually 1-3 months), bank statements, tax returns (if self-employed). Lenders want to see consistent income.

- Proof of Employment: Contact information for your employer.

- References: Sometimes required, especially for BHPH lots.

- Down Payment: Be prepared to show proof of funds for your down payment.

Gathering these documents beforehand demonstrates responsibility and can speed up your application.

What Lenders Look For Beyond Your Credit Score

Even with bad credit, lenders assess several other factors to gauge your risk:

- Debt-to-Income Ratio (DTI): This compares your monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments.

- Payment History on Other Debts: Even if you have bad credit, showing consistent, on-time payments on other current obligations (like rent or utility bills) can be a positive sign.

- Job Stability: A long, stable employment history in Las Vegas suggests a reliable income source.

- Residency Stability: Living at the same address for a significant period can also indicate stability.

- Down Payment Amount: A larger down payment reduces the loan amount and the lender’s risk, making you a more attractive borrower.

Based on my experience, presenting a strong overall financial picture, even with a low credit score, significantly improves your chances of approval.

The Pre-Approval Process: Your Strategic First Step

Many lenders offer pre-approval, which allows you to find out how much you can borrow before you even step foot on a lot. This often involves a "soft" credit inquiry that doesn’t harm your score.

- Benefits of Pre-Approval:

- Know Your Budget: You’ll know your maximum loan amount, helping you shop for cars within your means.

- Stronger Negotiating Position: You’re a cash buyer to the dealership, with financing already secured.

- Avoid Surprises: You’ll have a clear idea of your potential interest rate and terms.

Pro tips from us: Always get pre-approved from at least two different lenders if possible. This allows you to compare offers and leverage them for the best possible deal.

Key Factors Influencing Your Bad Credit Car Loan Terms

Several elements play a critical role in shaping the terms of your auto financing with a low credit score in Vegas. Understanding these can help you optimize your loan.

1. The Power of a Down Payment

A down payment is perhaps the most impactful factor when you have bad credit. It directly reduces the amount you need to borrow, which in turn lowers the lender’s risk.

- Benefits:

- Lower Monthly Payments: Less borrowed means smaller payments.

- Reduced Total Interest: You’ll pay interest on a smaller principal amount.

- Improved Approval Odds: Lenders see you as less risky.

- Better Terms: May qualify for slightly lower interest rates.

Aim for at least 10-20% of the car’s purchase price. Even a few hundred dollars can make a difference.

2. The Co-Signer Option: Friend or Foe?

A co-signer is someone with good credit who agrees to take on responsibility for your loan if you fail to pay. This can significantly improve your chances of approval and secure a better interest rate.

- When to Consider: If you have a trusted family member or friend willing to help, and you are absolutely confident in your ability to make payments.

- Risks: If you miss payments, it negatively impacts both your credit and your co-signer’s credit. It can also strain relationships.

Common mistakes to avoid are asking someone to co-sign without a clear, written agreement about repayment expectations. Always understand the full implications for both parties.

3. Vehicle Choice: Smart Decisions

When your credit is challenged, the type of car you choose matters.

- Focus on Affordability: Opt for a reliable, used vehicle that fits comfortably within your budget, both for the loan payment and ongoing costs (insurance, maintenance).

- Avoid High-End or Brand New: These cars carry higher price tags and depreciate quickly, making them riskier for lenders and a heavier financial burden for you.

From years of observing the auto loan market, prioritizing a mechanically sound, budget-friendly car over a luxury model is a cornerstone of smart bad credit financing.

4. Loan Term: Short vs. Long

The loan term is the length of time you have to repay the loan.

- Shorter Terms (e.g., 36-48 months): Higher monthly payments, but you pay less interest overall and own the car sooner.

- Longer Terms (e.g., 60-72 months): Lower monthly payments, but you pay significantly more in total interest over the life of the loan. You also risk owing more than the car is worth (negative equity) for a longer period.

Pro tips from us: Always try to secure the shortest term with monthly payments you can comfortably afford. If you must take a longer term for affordability, consider making extra payments when possible to reduce the principal faster.

5. Understanding Interest Rates

The interest rate is the cost of borrowing money, expressed as a percentage. With bad credit, your interest rate will be higher.

- Annual Percentage Rate (APR): This is the total cost of the loan, including interest and any fees. Always compare APRs, not just interest rates.

- How to Compare: Use online calculators to see how different APRs impact your total cost. Even a percentage point difference can save you hundreds or thousands over the life of the loan.

Navigating the Dealership Experience with Bad Credit

Walking into a dealership in Las Vegas with bad credit can feel daunting, but being prepared and confident can make all the difference.

Be Transparent and Honest

Don’t try to hide your credit situation. Dealerships run credit checks anyway, and being upfront establishes trust. Simply state, "I know my credit isn’t perfect, but I’m looking for reliable transportation and a loan I can afford."

Focus on the Total Price, Not Just Monthly Payments

Salespeople often focus on the monthly payment to make a car seem more affordable. This can lead to longer loan terms and higher overall costs.

- Negotiate the Car’s Price First: Treat it as a separate transaction. Get the best possible price on the vehicle before discussing financing.

- Then Discuss Financing: With your pre-approval in hand (if you have one), you have leverage. Compare the dealer’s financing offer to your pre-approval.

- Calculate Total Cost: Always ask for the total amount you will pay over the life of the loan, including interest and fees.

Common mistakes to avoid are getting caught up in the excitement and only focusing on the monthly payment. This is how people end up paying far more for a car than it’s worth.

Read Every Line of the Contract

Before signing anything, meticulously read the entire loan agreement. If you don’t understand a term, ask for clarification.

- Key things to check:

- Purchase price of the vehicle.

- Interest rate (APR).

- Loan term.

- Total amount financed.

- Any additional fees or add-ons (extended warranties, gap insurance, etc.).

- Prepayment penalties (though less common now).

Pro tips from us: Never feel rushed to sign. Take your time, and if possible, bring a trusted friend or family member to review the contract with you. This is a significant financial commitment.

Improving Your Credit While Paying Off Your Car Loan

A bad credit car loan in Las Vegas isn’t just a means to get a car; it’s a powerful tool for credit rebuilding. This is your chance to turn a negative into a positive.

The Opportunity: A Path to Better Credit

Every on-time payment you make on your car loan will be reported to the major credit bureaus. This consistent positive payment history is the single most important factor in improving your credit score.

- How it Works: As you make timely payments, your payment history improves, signaling to future lenders that you are a reliable borrower.

- Building a Foundation: This new positive tradeline helps offset past negative marks, gradually increasing your score.

Tips for On-Time Payments

- Set Up Automatic Payments: This is the easiest way to ensure you never miss a due date.

- Budget Carefully: Factor your car payment, insurance, and fuel costs into your monthly budget.

- Create Reminders: If automatic payments aren’t an option, use calendar alerts or apps to remind you a few days before the payment is due.

- Communicate with Your Lender: If you foresee a problem making a payment, contact your lender immediately. They may offer options like deferment, which is better than missing a payment.

Monitor Your Credit Score

Regularly check your credit report to track your progress and ensure there are no errors.

- Free Annual Reports: You’re entitled to a free credit report from each of the three major bureaus (Equifax, Experian, TransUnion) once a year at AnnualCreditReport.com.

- Credit Monitoring Services: Many banks and credit card companies offer free credit score monitoring.

From years of observing clients, actively monitoring your credit encourages financial responsibility and helps you spot potential issues early.

Other Credit-Building Strategies

While your car loan is a major step, combine it with other good habits:

- Pay All Bills on Time: This includes rent, utilities, and credit card payments.

- Keep Credit Card Balances Low: Aim to use less than 30% of your available credit on any card.

- Avoid Opening Too Many New Credit Accounts: This can signal risk to lenders.

- Maintain a Mix of Credit: A car loan (installment credit) combined with a credit card (revolving credit) can be beneficial.

Alternatives to a Bad Credit Car Loan (Short-Term Considerations)

While securing a bad credit car loan is a primary goal for many, it’s worth considering short-term alternatives if your situation is particularly dire or if you need time to save for a better down payment.

1. Public Transportation in Las Vegas

The RTC (Regional Transportation Commission of Southern Nevada) offers bus services throughout the Las Vegas Valley. While not as comprehensive as some major cities, it serves many key areas.

- Pros: Cost-effective, environmentally friendly.

- Cons: Limited routes, longer travel times, not ideal for all work schedules or locations.

2. Ride-Sharing Services

Uber and Lyft are widely available in Las Vegas, offering on-demand transportation.

- Pros: Convenient, door-to-door service.

- Cons: Can become very expensive for daily commutes or frequent use, especially with surge pricing.

3. Borrowing from Family or Friends

If you have a supportive network, a short-term loan from a trusted individual could be an option.

- Pros: Potentially interest-free or low-interest, flexible terms.

- Cons: Can strain relationships if not repaid, often lacks formal credit-building benefits.

If you choose this route, always create a clear, written agreement to protect both parties.

4. Saving Up for a Cash Car

If your immediate transportation needs aren’t critical, saving up for a modest used car that you can pay for in cash eliminates the need for a loan entirely.

- Pros: No interest payments, no monthly car payment, complete ownership immediately.

- Cons: Requires patience and discipline, may not be feasible if a car is an immediate necessity.

This option also allows you to focus on building your credit through other means before taking on a car loan.

Conclusion: Driving Forward with Confidence

Securing a bad credit car loan in Las Vegas is a journey that many residents successfully navigate, and with the right knowledge and approach, you can too. From understanding your credit score and the unique needs of driving in the Entertainment Capital to strategically choosing a lender and negotiating terms, every step you take brings you closer to reliable transportation and an improved financial future.

Remember, this isn’t just about getting a car; it’s about making a smart financial decision that can serve as a stepping stone to better credit and greater financial freedom. Be prepared, be patient, and be proactive. By making consistent, on-time payments, you’re not just paying off your car; you’re actively rebuilding your credit and opening doors to future opportunities. So, take the wheel, embrace the process, and drive confidently toward your goals in the vibrant city of Las Vegas. Your journey starts now.

Frequently Asked Questions About Bad Credit Car Loans in Las Vegas

Q1: Can I get a car loan in Las Vegas with a credit score below 500?

A1: While challenging, it is still possible. Lenders specializing in subprime loans look at more than just your credit score, including your income, job stability, and down payment amount. "Buy Here, Pay Here" dealerships are often the most lenient for very low scores.

Q2: What’s the typical interest rate for a bad credit car loan in Las Vegas?

A2: Interest rates for bad credit car loans can vary widely, often ranging from 10% to 25% or even higher, depending on your specific credit score, income, the loan term, and the lender. It’s crucial to compare APRs from multiple lenders.

Q3: How much of a down payment do I need for a bad credit car loan?

A3: While some lenders might offer loans with no down payment, it’s highly recommended to make one, especially with bad credit. Aim for at least 10-20% of the car’s purchase price to improve your chances of approval and secure better terms.

Q4: Will applying for a car loan hurt my credit score?

A4: A pre-qualification or pre-approval often involves a "soft" credit inquiry, which does not impact your score. However, when you formally apply for a loan, lenders perform a "hard" inquiry, which can temporarily drop your score by a few points. Multiple hard inquiries for the same type of loan within a short period (typically 14-45 days) are often grouped as one for scoring purposes.

Q5: Can I refinance my bad credit car loan later to get a better interest rate?

A5: Yes, absolutely! This is a smart strategy. After 6-12 months of consistent, on-time payments, your credit score should improve. You can then apply to refinance your loan with a different lender, potentially securing a much lower interest rate and reducing your total cost.

Q6: What if I have no credit history at all?

A6: Having no credit history (a "thin file") is different from having bad credit, but it still poses a challenge for lenders. You might need a co-signer, a larger down payment, or to start with a "Buy Here, Pay Here" lot to establish your credit history before moving to traditional lenders.

Q7: Are there specific dealerships in Las Vegas known for helping with bad credit?

A7: Many dealerships advertise their ability to work with "all credit types." It’s best to research online, read reviews, and look for dealerships that highlight their special finance departments or relationships with subprime lenders. You can also start by checking online aggregators that connect you with multiple suitable lenders.