Driving Dreams: Unlocking the Best Weokie Car Loan Rates for Your Next Vehicle

Driving Dreams: Unlocking the Best Weokie Car Loan Rates for Your Next Vehicle Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or pre-owned vehicle is an exciting prospect. It’s a significant investment, and for most, securing a car loan is a crucial step. While many financial institutions offer auto loans, understanding the nuances of options like those provided by Weokie Credit Union can make a substantial difference in your overall experience and the affordability of your dream car.

This comprehensive guide is designed to be your ultimate resource for navigating Weokie car loan rates. We’ll delve deep into what influences these rates, how to prepare for your application, and expert strategies to secure the most favorable terms possible. Our goal is to equip you with the knowledge to make informed decisions, ensuring you drive away not just with a great car, but with a smart financial deal.

Driving Dreams: Unlocking the Best Weokie Car Loan Rates for Your Next Vehicle

Why Consider Weokie Credit Union for Your Auto Loan? The Credit Union Advantage

Before we dive into the specifics of rates, it’s important to understand why Weokie Credit Union stands out in the crowded auto loan market. Unlike traditional banks, credit unions operate on a not-for-profit model, owned by their members. This fundamental difference often translates into tangible benefits for borrowers.

Based on my experience in the financial sector, credit unions like Weokie are typically able to offer more competitive interest rates on loans, including auto loans, and higher yields on savings accounts. This is because their primary mission isn’t to generate profits for shareholders, but to serve the financial well-being of their members. This member-centric approach fosters a unique lending environment.

Furthermore, Weokie, being deeply rooted in the Oklahoma community, understands the local economic landscape and its members’ needs. This localized focus often means more personalized service and a willingness to work with members through various financial situations, which can be a huge advantage when seeking financing.

Deconstructing Weokie Car Loan Rates: The Core Influencers

Understanding what factors influence your specific Weokie car loan rate is paramount. It’s not a one-size-fits-all number; rather, it’s a personalized calculation based on several key variables. Let’s break down the most significant contributors.

Your Credit Score: The Undisputed King of Rates

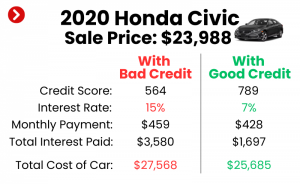

Without a doubt, your credit score is the single most influential factor in determining the interest rate you’ll be offered on a Weokie car loan. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay the loan on time. A higher credit score signals lower risk to the lender, resulting in more favorable, lower interest rates.

FICO scores, which range from 300 to 850, are widely used. Generally, scores above 720 are considered excellent, 670-719 good, 580-669 fair, and below 580 poor. Even a slight improvement in your score can lead to significant savings over the life of an auto loan. Pro tips from us: always check your credit report before applying to correct any errors and understand your standing.

The Loan Term: How Long Will You Be Paying?

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). Generally, shorter loan terms come with lower interest rates because the lender’s risk is reduced over a shorter period. While a shorter term means higher monthly payments, it also means you pay less interest overall.

Conversely, longer loan terms result in lower monthly payments, making a car seem more affordable upfront. However, you’ll end up paying significantly more in total interest over the life of the loan. It’s a trade-off between immediate affordability and long-term cost. Weokie offers various terms to fit different budgets, so understanding this balance is crucial.

The Loan Amount: Borrowing More Can Affect Rates

The total amount you wish to borrow also plays a role in your Weokie car loan rate. While not as direct as your credit score, larger loan amounts can sometimes carry slightly different rates. Lenders assess risk differently for very high-value loans compared to smaller ones.

It’s always wise to only borrow what you truly need and can comfortably afford. Over-borrowing can strain your budget and potentially impact the rate you qualify for, especially if it pushes your debt-to-income ratio too high.

Your Down Payment: A Powerful Tool for Lower Rates

Making a substantial down payment is one of the most effective strategies to secure a lower interest rate. When you put money down, you reduce the amount you need to borrow, which decreases the lender’s risk. This equity in the vehicle from day one makes you a more attractive borrower.

Beyond potentially lowering your interest rate, a larger down payment also reduces your monthly payments and lessens the likelihood of becoming "upside down" on your loan (owing more than the car is worth). Based on my experience, aiming for at least 10-20% down on a new car can yield excellent results in rate negotiation.

Vehicle Type: New vs. Used, and Even the Model

The type of vehicle you intend to purchase can also subtly influence your Weokie car loan rate. New cars often qualify for slightly lower rates than used cars. This is primarily because new cars typically have a clear, higher value and predictable depreciation, making them less risky collateral for the lender.

Used cars, while often more affordable to buy, come with more variables like age, mileage, and condition, which can translate into slightly higher rates. Some lenders also consider specific models or makes, especially if they have a history of rapid depreciation or reliability issues, though this is less common with major credit unions like Weokie.

Current Market Conditions: A Broader Economic Lens

While not something you can directly control, the broader economic environment and prevailing interest rates set by the Federal Reserve indirectly affect all lending rates, including Weokie car loan rates. When the Fed raises its benchmark rates, it typically leads to higher rates across the board for consumers, and vice-versa.

It’s a good idea to have a general awareness of the current interest rate landscape. This context helps you understand if the rates you are being offered are competitive relative to the market, rather than just in isolation.

Navigating the Weokie Car Loan Application Process

Applying for a car loan can seem daunting, but Weokie Credit Union strives to make the process as straightforward as possible for its members. Knowing what to expect and how to prepare can significantly smooth your path to approval.

Getting Started: Pre-Qualification vs. Pre-Approval

Before you even step foot in a dealership, consider getting pre-qualified or pre-approved through Weokie. These are distinct processes, and understanding the difference is key.

Pre-qualification provides an estimate of how much you might be able to borrow and at what general rate, based on a soft credit inquiry. This doesn’t affect your credit score and is a great way to gauge your options without commitment.

Pre-approval, on the other hand, involves a more thorough review of your financial information and a hard credit inquiry. If approved, Weokie will give you a specific loan amount and interest rate, often with a commitment letter valid for a certain period. This puts you in a much stronger negotiating position at the dealership, as you know exactly what financing you have secured.

Required Documents: Be Prepared

When you apply for a Weokie car loan, whether online, by phone, or in person, you’ll need to provide several documents to verify your identity, income, and financial stability. Common requirements include:

- Proof of Identity: Government-issued photo ID (driver’s license, passport).

- Proof of Income: Recent pay stubs, W-2 forms, or tax returns if self-employed.

- Proof of Residency: Utility bill or lease agreement with your current address.

- Social Security Number: For credit checks.

- Vehicle Information (if already chosen): Make, model, year, VIN, and sale price.

Gathering these documents in advance will streamline your application and prevent unnecessary delays.

The Application Itself: What to Expect

The Weokie car loan application will ask for your personal details, employment history, income, and existing debts. Be honest and accurate in your responses. Any discrepancies could slow down the process or even lead to denial.

Once submitted, Weokie’s lending team will review your application, pulling your credit report and assessing all the factors we discussed earlier. They may contact you for additional information or clarification. The goal is to match you with the best possible loan product for your financial situation.

Strategies to Secure the Best Weokie Car Loan Rates

Now that we understand the factors and the process, let’s explore actionable strategies to ensure you land the most competitive Weokie car loan rates. These pro tips come from years of observing successful financial planning.

Pro Tip 1: Boost Your Credit Score Before You Apply

This is perhaps the most impactful step you can take. If you have time before needing a car loan, focus on improving your credit score.

- Pay all bills on time, every time: Payment history is the biggest component of your FICO score.

- Reduce your outstanding debt: Especially on credit cards. Lowering your credit utilization ratio (debt vs. available credit) can significantly help.

- Avoid opening new credit accounts: This can temporarily lower your score.

- Check your credit report for errors: Incorrect information can unfairly lower your score. You can get a free report annually from AnnualCreditReport.com.

Pro Tip 2: Make a Substantial Down Payment

As mentioned, a larger down payment reduces the loan amount and signals lower risk to Weokie. Aim for at least 10-20% of the vehicle’s purchase price if your budget allows.

This not only helps secure a better rate but also reduces your monthly payments and protects you from negative equity early in the loan term. It’s a win-win strategy.

Pro Tip 3: Choose the Shortest Loan Term You Can Comfortably Afford

While longer terms mean lower monthly payments, they cost you more in interest over time. If your budget permits, opt for a shorter loan term (e.g., 48 or 60 months instead of 72 or 84).

This strategy often comes with a lower interest rate, and you’ll pay off your car faster, saving you hundreds or even thousands of dollars in interest. Run different scenarios with Weokie’s loan officers to see the impact.

Pro Tip 4: Leverage Pre-Approval as a Negotiating Tool

Getting pre-approved by Weokie gives you immense power at the dealership. You walk in knowing your maximum loan amount and your interest rate. This allows you to focus on negotiating the car’s price, rather than getting caught up in financing games.

If the dealership tries to offer you a higher rate, you can confidently decline, knowing you already have a better offer. This empowers you to secure the best deal on both the car and the financing.

Common Mistakes to Avoid When Seeking a Car Loan

Based on my observations, many borrowers inadvertently make mistakes that cost them money. Avoid these pitfalls:

- Applying to too many lenders at once: Multiple hard inquiries in a short period can negatively impact your credit score. Focus on a few strong contenders like Weokie.

- Not checking your credit report: Errors can derail your application or lead to higher rates. Always review your report well in advance.

- Focusing only on the monthly payment: While important, fixating solely on the lowest monthly payment can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan.

- Accepting dealership financing without comparing: Dealerships often mark up interest rates. Always compare their offer with a pre-approval from Weokie or another trusted lender.

Beyond the Rate: Other Weokie Auto Loan Benefits & Considerations

While the interest rate is a primary concern, Weokie Credit Union offers additional features and services that add value to your auto loan experience.

Loan Protection Options

Weokie often provides optional loan protection products that can offer peace of mind. These might include:

- GAP (Guaranteed Asset Protection) Insurance: If your car is totaled or stolen, GAP covers the difference between what your insurance pays and what you still owe on the loan, preventing you from being "upside down."

- Extended Warranty/Vehicle Service Agreements: These can protect you from unexpected repair costs after the manufacturer’s warranty expires.

Discuss these options with Weokie to see if they fit your needs and budget.

Auto Loan Refinancing

Did you get a car loan elsewhere with a higher interest rate? Weokie may be able to help you refinance your existing auto loan. Refinancing can potentially lower your interest rate, reduce your monthly payments, or even change your loan term, saving you money over time.

This is an excellent option if your credit score has improved since you took out your original loan or if market rates have dropped. It’s always worth exploring if you feel you’re paying too much.

Exceptional Member Service

One of the hallmarks of a credit union like Weokie is its commitment to member service. This often translates into a more personal, understanding, and responsive approach than you might find at larger, more impersonal financial institutions. When you have questions, concerns, or need assistance, knowing you have a dedicated team ready to help is invaluable. This is a significant part of the credit union advantage.

Real-Life Scenarios: Why Weokie Could Be Your Go-To

Let’s look at a few hypothetical scenarios to illustrate how Weokie’s approach to car loans can benefit different individuals:

Scenario 1: The First-Time Buyer with Fair Credit

Sarah is a recent college graduate with a steady job but a limited credit history, resulting in a fair credit score. Many banks might offer her a high interest rate. At Weokie, as a member, she might find more understanding and potentially better rates or even guidance on how to improve her credit, thanks to their community-focused mission. They might also be more willing to work with her on a reasonable down payment plan.

Scenario 2: The Established Member with Excellent Credit

Mark has been a Weokie member for years, has an excellent credit score, and is looking for a new SUV. Weokie, recognizing his loyalty and creditworthiness, is likely to offer him some of their absolute best car loan rates, ensuring he gets a highly competitive deal. His pre-approval process would be swift and straightforward.

Scenario 3: The Savvy Refinancer

Emily bought a car a year ago with a less-than-ideal interest rate from the dealership. Since then, she’s improved her credit score significantly. She approaches Weokie for a refinance. Based on her improved credit and Weokie’s competitive rates, she secures a new loan at a much lower interest rate, saving her a substantial amount of money over the remaining term of her loan. This demonstrates the ongoing value of credit union membership.

Frequently Asked Questions About Weokie Car Loans

Here are some common questions prospective borrowers have, along with concise answers.

1. Who can join Weokie Credit Union?

Membership eligibility for Weokie Credit Union typically includes individuals who live, work, worship, or attend school in specific Oklahoma counties, as well as family members of current members. It’s always best to check their official website for the most up-to-date and specific eligibility requirements. Joining is usually a simple process, often requiring a small deposit into a savings account.

2. What is the minimum credit score required for a Weokie car loan?

While Weokie doesn’t typically publish a strict minimum credit score, like most lenders, a higher score will always yield better rates. They consider a holistic view of your financial situation. Even if your score isn’t perfect, as a member-focused institution, they may offer options or guidance that traditional banks might not. It’s always worth applying or speaking with a loan officer.

3. Can I get a Weokie car loan with no down payment?

Yes, it is often possible to secure a Weokie car loan with no down payment, especially for borrowers with excellent credit. However, making a down payment is highly recommended as it reduces your overall loan amount, can lead to lower interest rates, and helps prevent negative equity. It’s a smart financial move if your budget allows.

4. How long does it take to get approved for a Weokie car loan?

Approval times for Weokie car loans can vary. Often, if you have all your documentation ready and apply during business hours, you can receive a decision within a few hours or one business day. Pre-approvals tend to be quicker, providing you with financing certainty before you even visit a dealership.

5. Does Weokie offer loans for both new and used vehicles?

Yes, Weokie Credit Union provides competitive auto loans for both new and used vehicles. Their rates and terms may differ slightly between new and used cars, reflecting the different risk profiles, but they aim to offer excellent options for both categories.

Drive Confidently with Weokie

Securing the right car loan is a cornerstone of a successful vehicle purchase. By thoroughly understanding Weokie car loan rates, the factors that influence them, and applying our expert strategies, you are well-positioned to make an informed and financially sound decision. Weokie Credit Union, with its member-centric approach and competitive offerings, stands as a strong contender for your auto financing needs.

Don’t just drive a car; drive a smart financial choice. Take the time to understand your options, prepare your finances, and leverage the benefits of a credit union. Visit Weokie Credit Union’s official website or speak with a loan officer today to explore your personalized car loan rates and start your journey towards your next vehicle with confidence.

Disclaimer: This article provides general information and is not financial advice. Weokie Credit Union’s specific rates, terms, and eligibility criteria are subject to change and may vary based on individual circumstances. Always consult directly with Weokie Credit Union for the most accurate and up-to-date information.

Further Reading: