Driving Dreams While Unemployed: A Comprehensive Guide to Securing a Car Loan

Driving Dreams While Unemployed: A Comprehensive Guide to Securing a Car Loan Carloan.Guidemechanic.com

The open road, the freedom of mobility, the sheer convenience of having your own vehicle – these are aspirations many of us share. But what happens when life throws a curveball, and you find yourself navigating the challenging terrain of unemployment? The thought of securing a car loan during such a period can feel like an impossible dream.

As expert bloggers and professional SEO content writers, we understand this dilemma deeply. Based on our extensive experience in the financial landscape, we’re here to tell you that while challenging, getting a car loan while unemployed isn’t entirely out of reach. This comprehensive guide will dissect the nuances of this situation, offering practical strategies, insightful advice, and crucial warnings to help you make an informed decision. Our ultimate goal is to empower you with the knowledge to potentially turn that dream into a reality, even without a traditional paycheck.

Driving Dreams While Unemployed: A Comprehensive Guide to Securing a Car Loan

The Elephant in the Room: Can You Really Get a Car Loan While Unemployed?

Let’s cut straight to the chase: Yes, it is possible to get a car loan when you’re unemployed, but it’s significantly more difficult than if you had a steady job. Lenders, at their core, are in the business of assessing risk. Their primary concern is whether you have the consistent financial capacity to repay the loan on time.

When you’re unemployed, that fundamental proof of income – the regular paycheck – is missing. This immediately flags you as a higher risk in their sophisticated assessment models. However, "unemployed" doesn’t always mean "no income." This distinction is crucial and forms the bedrock of our discussion.

Lenders need assurance. Without a traditional job, you need to provide alternative, verifiable sources of income or strong financial indicators that demonstrate your ability and willingness to meet your payment obligations. It’s about painting a clear, compelling picture of your financial stability, even when your employment status is in flux.

Understanding Lender Requirements: More Than Just a Paycheck

To understand how to get a car loan while unemployed, you first need to understand what lenders typically look for in any applicant. These criteria are designed to minimize their risk and ensure a return on their investment. When one piece of the puzzle (like employment) is missing, the others become even more critical.

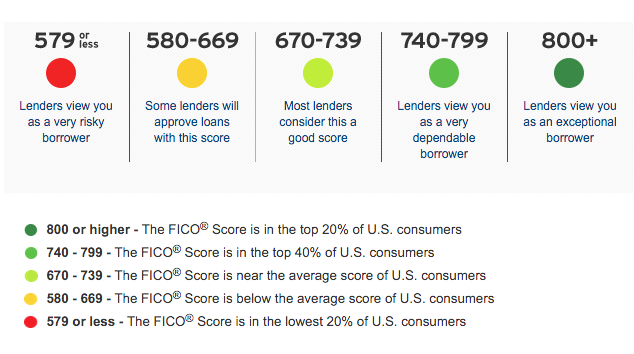

Firstly, lenders scrutinize your credit score and history. A strong credit score (generally 670 and above) indicates a history of responsible borrowing and repayment. This is a huge asset, as it tells the lender you’re reliable, even if your current income situation is temporary. Conversely, a poor credit history will make your task exponentially harder.

Secondly, they evaluate your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. While "income" might be the sticking point for you, a low DTI shows that your existing financial obligations are manageable, leaving room for a new car payment. Lenders prefer a DTI of 36% or less, though some may go higher for well-qualified applicants.

Thirdly, and most critically for our discussion, is stable income. Lenders want to see a consistent, predictable stream of money coming in. This is usually where unemployment poses the biggest challenge. They need to be confident that whatever income you present is reliable enough to cover the car loan payments for the foreseeable future.

Finally, the collateral (the car itself) also plays a role. In the event you default on the loan, the lender can repossess and sell the vehicle to recover their losses. This provides a safety net for them, but it doesn’t replace the need for a solid income source.

Unconventional Income Sources That Lenders May Consider

While a W-2 paycheck is the gold standard for lenders, it’s not the only form of income they might accept. The key here is verifiability and consistency. You need to be able to prove that these income streams are regular and sufficient to cover your potential car payments.

Unemployment Benefits: This is often the first thought for those out of work. Yes, some lenders will consider unemployment benefits as income. However, there are significant caveats. These benefits are temporary and typically replace only a fraction of your previous salary. Lenders will evaluate the duration of your benefits and whether they are sufficient to cover the loan payments comfortably. They usually require proof of ongoing eligibility and the amount.

Spousal or Partner Income: If you’re applying for a joint loan with a spouse or partner who is employed, their income can be a powerful asset. This is one of the most straightforward ways to bolster your application. The lender will then assess the combined income and credit profiles of both applicants.

Rental Income: Do you own property that you rent out? Consistent rental income can be a valid source of funds for a car loan. You’ll need to provide lease agreements and bank statements showing regular rent deposits. This demonstrates a reliable, ongoing revenue stream that is independent of traditional employment.

Pension or Retirement Income: For retirees or those receiving pension payments, this is often considered a stable and reliable income source. Lenders will typically require official statements or direct deposit records to verify the amount and consistency of these payments. This category often presents a strong case for approval due to its long-term nature.

Disability Benefits: Similar to pension income, long-term disability benefits (from government programs or private insurance) are usually accepted as verifiable income. The key is to provide official documentation that confirms the benefits are ongoing and of a sufficient amount. This shows a steady, albeit non-employment-based, income.

Child Support or Alimony: If you receive regular, court-ordered child support or alimony payments, these can also be considered income. Lenders will require official documentation, such as court orders and bank statements, to confirm the regularity and amount of these payments. It’s crucial that these payments are consistent and legally binding.

Freelance or Gig Economy Income: In today’s economy, many people earn income through freelance work, consulting, or the gig economy (e.g., rideshare driving, delivery services). If you have a documented history of consistent earnings from these sources, some lenders may consider it. You’ll need to provide extensive proof, such as tax returns (showing self-employment income), bank statements, and invoices, to demonstrate stability. This is where your ability to maintain meticulous financial records truly pays off.

Savings and Investments: While not a direct income stream, a significant amount of savings or liquid investments can act as a strong indicator of your ability to make payments. Some lenders might view this as a reserve fund that can cover payments for a certain period. This shows financial prudence and provides a buffer.

Pro tips from us: Lenders scrutinize these alternative income sources more closely than a W-2 salary. Be prepared to provide comprehensive documentation, often spanning several months, to prove consistency. The more stable and verifiable your income source, the better your chances.

Building a Strong Case: Strategies for Unemployed Applicants

Even with unconventional income, securing a car loan while unemployed requires a strategic approach. You need to proactively address lender concerns and present yourself as the least risky applicant possible. Here are several proven strategies:

Improve Your Credit Score

Your credit score is your financial resume. A higher score tells lenders you’re a responsible borrower, which becomes even more critical when your employment status is a question mark. Before applying, check your credit report for errors and dispute any inaccuracies. Pay down existing debts, especially credit card balances, to lower your credit utilization ratio.

Making all your payments on time, every time, is paramount. Even small improvements can significantly impact a lender’s perception of your risk. This proactive step can sometimes outweigh the lack of traditional employment income in the eyes of a potential lender.

Down Payment is Your Best Friend

A substantial down payment is perhaps one of the most effective strategies for an unemployed applicant. When you put down a significant portion of the car’s price, you reduce the amount you need to borrow, which in turn lowers the lender’s risk. It also demonstrates your financial commitment and capability.

A larger down payment means smaller monthly payments and less interest paid over the life of the loan. From the lender’s perspective, it shows you have skin in the game and are less likely to default. Aim for at least 20% of the car’s value, or even more if possible.

Consider a Co-signer

Bringing a co-signer with a strong credit history and stable income can dramatically improve your chances of approval. A co-signer legally agrees to be responsible for the loan if you fail to make payments. This provides a safety net for the lender.

Choose a co-signer wisely – typically a trusted family member or close friend. Ensure they understand the full implications, as their credit will be affected if you miss payments. While it can be a great solution, it also carries a significant responsibility for the co-signer.

Choose the Right Vehicle

Resist the urge to go for a luxury or brand-new vehicle. When you’re unemployed, your focus should be on affordability and reliability. Opt for a used, fuel-efficient, and reasonably priced car that meets your transportation needs without breaking the bank.

Lenders are more likely to approve loans for less expensive vehicles because the monthly payments are lower, making them more manageable with limited income. A practical choice demonstrates financial prudence, which works in your favor.

Explore Different Lender Types

Not all lenders are created equal, especially when it comes to unconventional circumstances.

- Credit Unions: These member-owned financial institutions often have more flexible lending criteria than traditional banks. They are known for working with members to find solutions and may be more sympathetic to unique financial situations.

- Online Lenders: Many online lenders specialize in various credit profiles and income situations. They often use alternative data points for assessment and can offer quicker decisions. However, always research their reputation and read reviews.

- "Buy-Here, Pay-Here" Dealerships (with caution): These dealerships often provide in-house financing, making them more lenient with approvals, including for those with no income or bad credit. However, common mistakes to avoid are falling into high-interest rates and predatory terms. Their loans typically come with significantly higher interest rates and less favorable terms, which can lead to a debt spiral. Use them only as a last resort and read every single word of the contract.

Prepare Impeccable Documentation

No matter your income source, meticulous documentation is key. Gather everything you need before you apply. This includes:

- Bank statements (at least 3-6 months) showing consistent deposits from your alternative income sources.

- Benefit letters (unemployment, disability, pension, etc.)

- Court orders for child support/alimony.

- Tax returns (especially if self-employed).

- Proof of assets (investment statements, savings accounts).

- Letters from potential employers (if you have job offers pending).

The more organized and comprehensive your documentation, the more credible your application will appear. Transparency is crucial here; don’t try to hide anything.

Common Pitfalls and How to Avoid Them

Navigating the world of car loans while unemployed is fraught with potential missteps. Being aware of these common pitfalls can save you from financial headaches down the road.

Applying with Too Many Lenders

It might seem logical to cast a wide net, but applying for multiple loans in a short period can actually harm your credit score. Each application typically results in a "hard inquiry" on your credit report, which can temporarily lower your score. A cluster of hard inquiries suggests to lenders that you’re desperate for credit, making you appear riskier.

Instead, research lenders thoroughly and pre-qualify with a few to get an idea of potential rates without impacting your credit score. This allows you to compare offers more strategically.

Hiding Your Financial Situation

Attempting to conceal your unemployment or misrepresenting your income is a grave mistake. Lenders perform thorough checks, and any deception will likely be discovered, leading to an immediate rejection of your application and potentially harming your ability to secure future credit.

Be transparent and honest about your current financial standing. Explain your situation clearly and focus on the steps you’re taking to mitigate risk, such as actively seeking employment or leveraging alternative income sources. Honesty builds trust.

Overlooking the Total Cost of Car Ownership

A car loan payment is just one piece of the puzzle. Pro tips from us: many applicants focus solely on the monthly payment and forget about the other significant costs. These include:

- Car insurance: This can be substantial, especially for newer vehicles or drivers with less-than-perfect records.

- Maintenance and repairs: Used cars, while cheaper upfront, might require more frequent maintenance.

- Fuel costs: Factor in your daily commute and typical driving habits.

- Registration and taxes: Annual fees that add up.

Failing to budget for these additional expenses can quickly turn an "affordable" car into a financial burden. Create a comprehensive budget that includes all potential car-related costs before committing to a loan.

Falling for Predatory Loans

When faced with limited options, it’s easy to become desperate and accept any loan offer. Common mistakes to avoid are falling prey to predatory lenders who target vulnerable individuals with incredibly high-interest rates, hidden fees, and unfavorable terms. These loans often lead to a cycle of debt that is incredibly difficult to escape.

Always read the fine print, understand all terms and conditions, and never feel pressured to sign anything you don’t fully comprehend. If an offer seems too good to be true, or if a lender isn’t transparent, walk away. For more information on identifying predatory lending, you can check out resources from trusted financial institutions or consumer protection agencies. (Internal Link Placeholder: Check out our guide on "Spotting Predatory Lending Practices").

Alternatives to a Traditional Car Loan

Sometimes, a traditional car loan simply isn’t feasible or advisable, especially when unemployed. It’s important to consider all your options to avoid unnecessary financial strain.

Buying a Cheaper Used Car with Cash: If you have savings, purchasing an older, reliable used car outright can be the most financially responsible decision. This eliminates monthly payments, interest charges, and the stress of loan applications. While it might not be your dream car, it provides essential transportation without added debt.

Public Transportation or Ride-Sharing: Depending on where you live, public transport (buses, trains) or ride-sharing services (Uber, Lyft) might be a more cost-effective solution in the short term. Calculate the monthly cost of these alternatives versus a car loan plus all associated ownership costs. You might be surprised by the savings.

Borrowing from Family or Friends: While not always an option, a personal loan from a trusted family member or friend can offer much more flexible terms and lower (or no) interest. If you go this route, always put the agreement in writing to avoid misunderstandings and maintain the relationship. Treat it with the same seriousness as a bank loan.

The Future of Your Finances: Planning for Employment

Securing a car loan while unemployed is often a temporary solution to an immediate need. However, it’s crucial to view this decision within the broader context of your financial future. The ultimate goal should be to find stable employment.

Actively searching for a job should remain your top priority. The sooner you re-enter the workforce with a steady income, the stronger your financial position will become. Not only will this make your car loan payments much more manageable, but it will also open doors to better financial products and opportunities in the future.

Once re-employed, you might even consider refinancing your car loan for a lower interest rate, especially if you initially took out a loan with less favorable terms. A strong employment history will significantly improve your chances of securing better loan terms down the line. (External Link Placeholder: For general advice on job searching and career development, you might visit a reputable site like the U.S. Department of Labor’s CareerOneStop.)

Conclusion: Driving Forward with Informed Decisions

The journey to securing a car loan while unemployed is undoubtedly challenging, but as we’ve explored, it’s not an impossible feat. It demands meticulous preparation, a clear understanding of your financial landscape, and a strategic approach to addressing lender concerns. By leveraging alternative income sources, presenting a strong financial profile, and carefully choosing your lending partners, you can increase your chances of approval.

Remember, the ultimate goal is not just to get a loan, but to get a sustainable loan that doesn’t plunge you into further financial distress. Prioritize affordability, be transparent with lenders, and always consider the total cost of car ownership. With careful planning and responsible decision-making, you can indeed navigate this complex situation and drive towards a more stable future.

What has been your experience with securing financing during challenging times? Share your insights and questions in the comments below – your experiences can help others on their journey!