Driving Dreams: Your Ultimate Guide to Bad Credit Car Loans in Appleton, WI

Driving Dreams: Your Ultimate Guide to Bad Credit Car Loans in Appleton, WI Carloan.Guidemechanic.com

Navigating the path to car ownership can feel like an uphill battle, especially when a less-than-perfect credit score stands in your way. For many residents in Appleton, WI, the dream of reliable transportation is essential for work, family, and daily life. But what happens when your credit history makes traditional lenders hesitant?

The good news is that securing a vehicle with bad credit isn’t an impossible feat. With the right knowledge and approach, you can find Bad Credit Car Loans Appleton WI that fit your budget and help you rebuild your financial future. This comprehensive guide will walk you through everything you need to know, from understanding your credit to driving off the lot in your new car.

Driving Dreams: Your Ultimate Guide to Bad Credit Car Loans in Appleton, WI

Understanding Bad Credit and Auto Loans

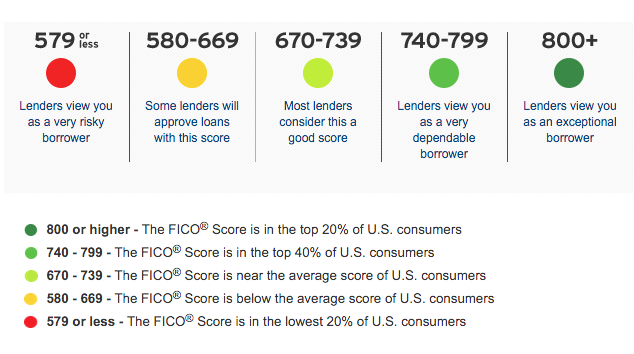

Before diving into the specifics of Bad Credit Car Loans Appleton WI, it’s crucial to understand what "bad credit" truly means in the eyes of an auto lender. Generally, a FICO score below 600-620 is considered subprime or bad credit. This score reflects your past financial behavior, indicating to lenders a higher risk of default.

When traditional banks or credit unions see a low score, they often see a red flag. They might perceive you as a borrower who has struggled with payments in the past, leading them to deny your loan application or offer less favorable terms. However, this doesn’t mean all doors are closed.

Why Traditional Lenders Hesitate

Mainstream lenders, like large national banks, prefer borrowers with strong credit scores because they represent lower risk. Their business model is built on providing loans at competitive rates to a wide, reliable customer base. When a borrower has a history of missed payments, bankruptcies, or collections, it suggests an increased likelihood of similar issues occurring with a new car loan.

This risk assessment often translates into higher interest rates, stricter terms, or outright rejections for those with bad credit. Their primary goal is to minimize risk and maximize returns.

The Reality: It’s Possible, Just Different

Based on my experience working within the automotive financing industry, I can confidently say that securing a car loan with bad credit is absolutely possible. The process simply requires a different approach and an understanding of the specialized lenders and programs designed for this very situation. These lenders are often more willing to look beyond just your credit score and consider your current financial stability.

They understand that life happens, and a past financial misstep shouldn’t permanently bar you from essential transportation. Their focus shifts from solely your credit score to your ability to make payments moving forward, often taking into account your income, employment history, and down payment.

The Appleton, WI Landscape for Bad Credit Auto Loans

Appleton, WI, like many vibrant communities, has a diverse range of financing options available for car buyers. The key is knowing where to look and what to expect from lenders who specialize in car loans for bad credit Appleton residents. Local factors, such as the presence of community credit unions and dealerships that cater to all credit types, can make a significant difference.

Many local dealerships and financial institutions in the Fox Valley understand the unique needs of their community members. They are often more accessible and willing to work with individuals facing credit challenges than large, impersonal national chains. This local focus can be a real advantage for you.

Types of Lenders Available in the Area

When searching for Appleton auto loans no credit or bad credit, you’ll primarily encounter three main types of lenders:

-

Specialized Dealerships: Many dealerships in and around Appleton have dedicated finance departments that work with a network of subprime lenders. These are often the most straightforward option, as they can handle both the car sale and the financing in one place. Some even offer "Buy Here Pay Here" options, where the dealership itself is the lender.

-

Local Banks and Credit Unions: While traditional banks might be stricter, local credit unions often have more flexible lending policies, especially for their members. They are community-focused and may be more inclined to work with you if you have an established relationship with them. It’s always worth checking with institutions like Capital Credit Union or Fox Communities Credit Union.

-

Online Lenders and Brokers: A growing number of online platforms specialize in connecting bad credit borrowers with lenders nationwide, including those serving Appleton. These can offer convenience and a wide range of options, but require careful vetting on your part.

Preparing for Your Bad Credit Car Loan Application

Preparation is paramount when seeking how to get a car loan with bad credit WI. The more organized and informed you are, the better your chances of securing favorable terms. Think of this as building a strong case for yourself as a reliable borrower, despite your credit history.

Taking these preparatory steps can significantly improve your odds and potentially lead to better interest rates and loan terms. It shows lenders that you are serious and responsible.

1. Know Your Credit Score and Report

Pro tips from us: The first and most crucial step is to obtain a copy of your credit report and score. You can get free copies of your credit report from each of the three major bureaus (Equifax, Experian, TransUnion) once a year at AnnualCreditReport.com. Review it carefully for any errors, which are surprisingly common. Disputing and correcting errors can potentially boost your score.

Understanding what’s on your report will help you anticipate a lender’s perspective. It also allows you to explain any past issues proactively, showing transparency.

2. Budgeting: Determine What You Can Truly Afford

Before you even look at cars, sit down and create a realistic budget. Consider not just the monthly car payment, but also insurance, fuel, maintenance, and potential repair costs. A common mistake to avoid is focusing solely on the monthly payment without considering the total cost of ownership.

Your debt-to-income ratio (DTI) is a critical factor for lenders. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments. provides excellent resources to help you create a solid financial plan.

3. Gather Essential Documents

Lenders specializing in bad credit loans will require more documentation to verify your identity, income, and residence. Be prepared with:

- Proof of Income: Recent pay stubs (last 2-3 months), tax returns if self-employed, or bank statements.

- Proof of Residence: Utility bills (electricity, gas, water) or a lease agreement.

- Proof of Identity: Valid driver’s license or state ID.

- Proof of Insurance: You’ll need this before driving off the lot.

- References: Sometimes required, especially for "Buy Here Pay Here" options.

Having these documents ready demonstrates your readiness and can speed up the application process considerably.

4. The Power of a Down Payment

A significant down payment is one of the most effective tools you have when seeking buy a car with bad credit Appleton. It reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the life of the loan. More importantly, it signals to lenders that you have financial discipline and are committed to the purchase.

Lenders see a down payment as a direct investment from you, which reduces their risk. Even 10-20% down can make a substantial difference in your approval chances and loan terms.

5. Leveraging a Trade-in

If you have an existing vehicle, using it as a trade-in can function similarly to a down payment. The equity you have in your old car (its value minus any outstanding loan balance) can be applied towards your new purchase, reducing the amount you need to finance.

Be sure to get an accurate appraisal of your trade-in value before you start shopping. This ensures you get a fair deal and can maximize its impact on your new loan.

Finding the Right Lender/Dealership in Appleton

The Appleton area offers various avenues for individuals seeking dealerships that work with bad credit Appleton. Your choice of lender can significantly impact your interest rate, loan terms, and overall experience. It’s crucial to research and compare your options carefully.

Don’t feel pressured to make a quick decision. Take your time to explore all available avenues to find the best fit for your specific financial situation.

Specialized Dealerships and "Buy Here Pay Here"

Many local dealerships are equipped to handle subprime financing. They work with a network of lenders who specialize in higher-risk loans. These dealerships often advertise their ability to help customers with bad credit.

"Buy Here Pay Here" (BHPH) dealerships are another option. These dealerships finance the car themselves, meaning you make your payments directly to them.

- Pros of BHPH: Often a higher approval rate, even with very poor credit; quick approval process.

- Cons of BHPH: Typically much higher interest rates, shorter loan terms, limited car selection, and sometimes less reporting to credit bureaus (which means it might not help rebuild your credit as effectively).

Based on my experience, BHPH should generally be a last resort due to the higher costs involved. However, for some, it might be the only viable option.

Local Credit Unions

As mentioned, local credit unions like Capital Credit Union or Fox Communities Credit Union can be excellent resources. They often have a more personalized approach and may be more willing to look at your individual circumstances rather than just your credit score. If you’re already a member or meet their membership requirements, it’s definitely worth inquiring about their auto loan options.

They might offer slightly better rates than specialized subprime lenders due to their non-profit nature and community focus.

Online Lenders

Online lenders have streamlined the application process, allowing you to get pre-approved from the comfort of your home. They often have a wide network of lenders, increasing your chances of finding an offer. Websites like LendingTree or Capital One Auto Navigator can help you compare multiple offers without impacting your credit score with multiple hard inquiries.

Always check the legitimacy and reviews of online lenders. Ensure they are transparent about their terms, fees, and privacy policies.

Questions to Ask Potential Lenders

When speaking with any lender, be prepared with a list of questions:

- What is the Annual Percentage Rate (APR)? (This includes interest and fees, giving you the true cost of the loan).

- What are the loan terms (length of the loan)?

- Are there any prepayment penalties if I pay off the loan early?

- What are all the fees associated with this loan?

- Do you report payments to all three major credit bureaus? (Crucial for improve credit score Appleton efforts).

Don’t just jump at the first offer. Compare at least 2-3 different offers to ensure you’re getting the best possible terms.

The Application and Approval Process

Once you’ve done your research and prepared your documents, the application process for bad credit car loans Appleton WI typically follows a clear path. While it might seem daunting, breaking it down into steps makes it more manageable.

Understanding each stage will help you navigate the process confidently and make informed decisions.

Step-by-Step: Application, Negotiation, Approval

- Application: You’ll fill out a loan application, either online or in person. This will ask for your personal details, employment history, income, and residence information.

- Document Submission: Provide all the necessary documents you gathered during your preparation phase.

- Credit Check: The lender will perform a hard inquiry on your credit report. This will temporarily lower your score by a few points, but the impact is minimal if done within a short shopping window (usually 14-45 days, depending on the scoring model).

- Review and Offer: The lender reviews your application and documents. If approved, they will present you with a loan offer detailing the interest rate, loan term, and monthly payment.

- Negotiation (if applicable): While not always possible with bad credit loans, you can sometimes negotiate on the interest rate, loan term, or even the price of the car itself. Every little bit helps.

- Signing and Funding: Once you agree to the terms, you’ll sign the loan documents. The dealership will then receive funds from the lender, and you can drive off in your new car.

Understanding Interest Rates and APR

With bad credit, expect higher interest rates than someone with excellent credit. This is how lenders mitigate the increased risk they’re taking. An interest rate of 10-25% or even higher is not uncommon for subprime auto loans.

The Annual Percentage Rate (APR) is crucial to understand. It represents the true annual cost of your loan, including the interest rate and any other fees or charges. Always compare APRs, not just interest rates, when evaluating loan offers. A lower APR means a cheaper loan overall.

The Importance of Reading the Fine Print

Never sign any loan agreement without thoroughly reading and understanding every single clause. Pay close attention to:

- Total Amount Financed: The actual amount of money you are borrowing.

- Total Payment: The total amount you will pay over the life of the loan, including interest.

- Late Payment Fees: What happens if you miss a payment.

- Prepayment Penalties: Are you charged if you pay off the loan early?

- Default Clauses: Under what conditions can the lender repossess your vehicle?

If anything is unclear, ask for clarification. Don’t be afraid to take the contract home and review it calmly before committing.

What to Do If You’re Denied

A denial isn’t the end of the road. If your application is rejected:

- Ask Why: Lenders are required to tell you the reason for denial. This feedback is invaluable.

- Re-evaluate Your Budget: Perhaps you were aiming for too expensive a car.

- Increase Your Down Payment: Save more money.

- Find a Cosigner: A trusted individual with good credit can significantly improve your chances.

- Explore Other Lenders: Don’t give up on the first try.

Strategies to Improve Your Chances and Future

Securing a bad credit car loan in Appleton, WI, is just the first step. You can implement several strategies to not only improve your chances of approval but also use this loan as a stepping stone to better financial health.

View this loan as an opportunity to demonstrate responsible financial behavior and build a stronger credit profile for the future.

Consider a Cosigner

A cosigner is someone with good credit who agrees to take on the responsibility of the loan if you fail to make payments. Their strong credit profile can help you get approved and potentially secure a lower interest rate.

- Pros: Increased approval chances, potentially lower interest rates.

- Cons: The cosigner is equally responsible for the debt, and their credit will be affected if you miss payments. Only ask someone you trust deeply and who understands the implications.

Start with a Smaller, More Affordable Car

It might be tempting to aim for your dream car, but with bad credit, starting modest is often the smartest move. Opt for a reliable, used car that fits comfortably within your budget. A lower loan amount means lower monthly payments, which are easier to manage and less risky for lenders.

This approach allows you to build a positive payment history, making it easier to upgrade to a better vehicle in the future. Focus on affordable car payments Appleton.

Building Credit: Making Payments on Time

This is arguably the most significant benefit of a bad credit car loan. Every on-time payment you make is reported to the credit bureaus, gradually improving your credit score. Consistency is key here.

Set up automatic payments if possible, or mark your calendar to ensure you never miss a due date. This loan can be a powerful tool for rebuilding your credit.

Refinancing: The Long-Term Strategy

Once you’ve made 6-12 months of on-time payments, your credit score will likely have improved. At this point, you may be eligible to refinance your car loan at a lower interest rate. Refinancing can significantly reduce your monthly payments and the total amount of interest you pay over the life of the loan.

- provides excellent information on when and how to consider refinancing your auto loan. This strategy can save you thousands of dollars.

Common Pitfalls and How to Avoid Them

Even with the best intentions, car buyers with bad credit can fall prey to certain traps. Being aware of these common mistakes can help you make a smarter, safer purchase in Appleton.

Knowledge is your best defense against predatory practices and costly errors.

High-Pressure Sales Tactics

Some dealerships might try to rush you into a decision or pressure you into buying add-ons you don’t need (like extended warranties or rust protection) to increase their profit. Stand firm. You have the right to take your time, ask questions, and walk away if you feel uncomfortable.

Never sign anything you don’t fully understand or feel pressured to agree to.

Hidden Fees

Carefully review the entire sales contract for any unexpected charges. These could include excessive documentation fees, arbitrary "preparation" fees, or inflated registration costs. Every fee should be clearly explained and justified.

If you see a charge you don’t recognize or understand, ask for an explanation. If it seems unreasonable, try to negotiate its removal.

Unrealistic Payment Plans

Be wary of lenders who approve you for a loan with payments that stretch your budget too thin. While a longer loan term might mean lower monthly payments, it also means paying more interest over time and potentially being upside down on your loan for longer.

Ensure your monthly payment is comfortable and sustainable, even if unexpected expenses arise. Don’t let a lender convince you to take on more than you can truly afford.

Ignoring the Total Cost of the Loan

As discussed, focusing only on the monthly payment is a common pitfall. Always look at the total cost of the loan, including all interest and fees over the entire term. A lower monthly payment over a very long term might seem appealing, but it often results in paying significantly more in the long run.

Calculate the total cost before committing to any loan. This holistic view will give you the clearest picture of your financial commitment.

Your Path to Auto Ownership in Appleton, WI

Securing Bad Credit Car Loans Appleton WI might present unique challenges, but it’s far from an impossible dream. By understanding your credit, meticulously preparing your finances, researching specialized lenders, and adopting smart strategies, you can drive away in a reliable vehicle while simultaneously working to improve your financial standing.

Remember, this isn’t just about getting a car; it’s about taking a proactive step towards rebuilding your credit and gaining greater financial freedom. With diligent payments and smart choices, this car loan can be the catalyst for a brighter financial future. Drive confidently, Appleton!