Driving Dreams: Your Ultimate Guide to Buying a Used Car With a Loan

Driving Dreams: Your Ultimate Guide to Buying a Used Car With a Loan Carloan.Guidemechanic.com

The allure of a brand-new car is undeniable, but for many savvy shoppers, the path to vehicle ownership takes a different, often smarter, route: a used car. Opting for a pre-owned vehicle can unlock significant savings, sidestepping the steep depreciation that new cars experience. When combined with the strategic use of a loan, it becomes an accessible and financially sound decision for countless individuals.

However, navigating the world of used car purchases and securing the right financing can feel like a complex maze. This comprehensive guide is designed to demystify the entire process, empowering you with the knowledge and confidence to make an informed choice. We’ll dive deep into every crucial step, from budgeting and securing a loan to finding the perfect vehicle and finalizing the deal, ensuring you drive away with peace of mind.

Driving Dreams: Your Ultimate Guide to Buying a Used Car With a Loan

Why a Used Car? The Smart Choice for Many

Choosing a used car isn’t just about saving money upfront; it’s about making a financially intelligent decision that benefits you in the long run. New cars lose a significant portion of their value the moment they’re driven off the lot, a phenomenon known as depreciation. By opting for a used vehicle, you effectively let the previous owner absorb the brunt of this initial loss.

This means you can often acquire a well-maintained vehicle with desirable features for a fraction of its original price. Furthermore, insurance premiums for used cars are typically lower than those for new models, adding to your overall savings. It’s a compelling argument for practicality over pristine newness.

The Foundation: Assessing Your Financial Readiness

Before you even begin browsing car listings, the most critical step is to understand your own financial landscape. This foundational work will dictate what kind of car you can realistically afford and the type of loan you’re likely to qualify for. Skipping this step is one of the common mistakes to avoid.

Budgeting Like a Pro: Beyond the Monthly Payment

Many people focus solely on the monthly car payment, but this is just one piece of the puzzle. A truly professional budget considers the total cost of ownership. This includes not only the loan principal and interest but also essential recurring expenses like insurance, registration fees, maintenance, and potential repair costs.

Based on my experience, overlooking these ancillary costs can quickly turn an "affordable" monthly payment into a financial strain. Pro tips from us include creating a detailed spreadsheet that projects all these expenses. Remember, what you can borrow might be different from what you can comfortably afford each month without compromising other financial goals.

Consider your Debt-to-Income (DTI) ratio. Lenders use this to assess your ability to manage monthly payments and repay debts. A lower DTI indicates less financial risk, making you a more attractive borrower. Aim for a DTI below 36%, including your new car payment, to keep your finances healthy.

Credit Score: Your Financial Passport

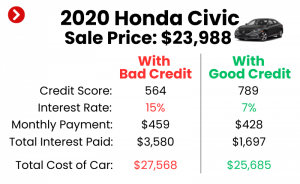

Your credit score is arguably the most influential factor in securing a favorable used car loan. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use this score to determine the risk involved in lending you money.

A higher credit score typically translates to lower interest rates on your loan, saving you hundreds or even thousands of dollars over the loan’s lifetime. Conversely, a lower score can lead to higher rates or even loan denial. Before applying for any loan, obtain a free copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your score. Address any errors you find promptly.

If your credit score isn’t where you want it to be, take steps to improve it. Paying bills on time, reducing existing debt, and avoiding new credit applications can all help boost your score. Even a slight improvement can significantly impact the interest rate offered on your pre-owned vehicle loan.

Down Payment: The Game Changer

A substantial down payment can dramatically improve your financial position when buying a used car with a loan. Putting money down upfront reduces the amount you need to borrow, which in turn lowers your monthly payments and the total amount of interest you’ll pay over the life of the loan. It’s a powerful tool for reducing your financial burden.

Furthermore, a larger down payment can help you avoid negative equity, a situation where you owe more on the car than it’s worth. This is particularly important with used cars, as their value can fluctuate. Lenders also view borrowers with significant down payments as less risky, potentially leading to better loan terms and more favorable car loan approval.

Common mistakes to avoid are skipping the down payment entirely or putting down a minimal amount. While tempting to conserve cash, this often leads to higher monthly payments and a greater risk of being underwater on your loan. Aim for at least 10-20% of the vehicle’s purchase price if possible.

Securing Your Loan: Where to Look and What to Expect

Once you have a clear understanding of your budget and credit, the next step is to explore your financing options. This phase is crucial for empowering you during the car buying process. Don’t wait until you’re at the dealership to think about financing.

Pre-Approval: Your Power Play

Securing pre-approval for a used car loan is one of the most strategic moves you can make. What is it? It’s a conditional offer from a lender that tells you exactly how much money they are willing to lend you, at what interest rate, and for what loan term, before you even choose a car. This acts as a powerful negotiating tool.

With pre-approval in hand, you walk into a dealership as a cash buyer. You know your budget limit and your financing terms, which removes the pressure of in-house financing and allows you to focus solely on the car’s price. This transparency ensures you get the best deal, both on the vehicle and the loan itself.

Pro tips from us: Explore various sources for pre-approval. Banks, credit unions, and online lenders all offer competitive rates for used car financing. Credit unions, in particular, often provide excellent rates to their members. Shop around and compare offers to find the best terms for your pre-owned vehicle loan.

Loan Terms and Interest Rates: Understanding the Details

When evaluating loan offers, two key factors demand your close attention: the loan term and the interest rate. The interest rate, expressed as an Annual Percentage Rate (APR), is the cost of borrowing money, including fees. A lower APR means less money paid back over time.

The loan term refers to the length of time you have to repay the loan, typically measured in months (e.g., 36, 48, 60, or 72 months). A shorter loan term generally results in higher monthly payments but lower overall interest paid. Conversely, a longer term means lower monthly payments but more interest paid over time.

Based on my experience, many buyers are tempted by the lowest monthly payment a longer term offers, without fully realizing the significant increase in total interest costs. Always consider the total cost of the loan, not just the monthly installment. Aim for the shortest term you can comfortably afford to minimize interest expenses and achieve a quicker car loan approval.

Common Loan Pitfalls: Stay Vigilant

While securing a loan can be straightforward, there are several common loan pitfalls to watch out for. Be wary of balloon payments, which are large lump sums due at the end of the loan term after a series of smaller payments. These can catch borrowers off guard if not properly planned for.

Also, scrutinize all fees and charges associated with the loan. Some lenders may include excessive administrative fees or unnecessary add-ons that inflate the total cost. Always ask for a detailed breakdown of all charges. Another pitfall is agreeing to an interest rate that is significantly higher than what your credit score suggests you should qualify for. This can happen if you don’t shop around for pre-approval.

Finally, be mindful of negative equity. This occurs when the value of your car is less than the outstanding balance of your loan. If you need to sell or trade in the vehicle while in a negative equity situation, you’ll have to pay the difference out of pocket or roll it into your next car loan, creating a cycle of debt.

Finding Your Perfect Used Car: Beyond the Price Tag

With your financing pre-approved, you’re ready to shift your focus to the vehicle itself. This stage requires diligent research and careful inspection to ensure you’re making a wise investment.

Research, Research, Research: Knowledge is Power

Don’t jump into a purchase without thorough research. Start by identifying your needs: What size car do you need? What features are essential? What’s your average commute? Then, research specific makes and models known for reliability, safety, and good resale value within your budget.

Utilize online resources like Consumer Reports, Edmunds, and Kelley Blue Book to read reviews, compare models, and understand common issues. These sites also provide estimated market values, helping you gauge if a car is priced fairly. This research will narrow down your options and prevent you from making an impulsive decision.

Dealer vs. Private Seller: Weighing Your Options

You generally have two main avenues for buying a used car: a licensed dealership or a private seller. Each has its pros and cons. Dealerships often offer certified pre-owned (CPO) vehicles, which come with warranties and have undergone rigorous inspections. They also handle all the paperwork, making the process smoother.

However, dealership prices are typically higher due to overhead and profit margins. Private sellers, on the other hand, often offer lower prices because they don’t have the same overhead. The downside is that private sales usually come "as is," with no warranty or recourse if issues arise. Pro tips from us: If buying from a private seller, be extra diligent with inspections and paperwork.

Consider your comfort level with risk and your willingness to handle potential complications. For many, the peace of mind offered by a reputable dealer, especially with a CPO vehicle, outweighs the potential savings of a private sale. For a deeper dive into negotiation tactics, you might find our article on helpful.

The All-Important Vehicle Inspection: Non-Negotiable

This is perhaps the most critical step in buying a used car. Never, under any circumstances, purchase a used vehicle without a pre-purchase inspection (PPI) by an independent, certified mechanic of your choosing. This isn’t just a suggestion; it’s a non-negotiable step.

A PPI can uncover hidden mechanical issues, accident damage, or looming repairs that are not apparent during a casual test drive. The cost of a PPI is a small investment that can save you thousands in unexpected repairs down the line. Common mistakes to avoid are skipping the PPI or relying solely on the seller’s inspection report.

While a mechanic handles the in-depth check, you can also perform a basic visual inspection yourself. Look for consistent panel gaps, signs of fresh paint (indicating repairs), check fluid levels and colors, inspect tire tread depth, and test all lights and electronics. Listen for unusual noises during the test drive.

Vehicle History Report: Uncovering the Past

A vehicle history report, such as those from CarFax or AutoCheck, is another essential tool for uncovering a used car’s past. This report can reveal crucial information like accident history, salvage titles, flood damage, odometer discrepancies, previous owners, and service records. It’s like a detailed resume for the car.

While not foolproof, a comprehensive report provides invaluable insights that can influence your buying decision. For example, a car with a salvage title means it was declared a total loss by an insurance company, often due to significant damage, and its value and safety could be compromised. Always review this report carefully, comparing it with your mechanic’s findings.

The Negotiation and Finalizing the Deal

You’ve found the perfect car, and your loan is ready. Now comes the moment to finalize the deal. This stage requires confidence and attention to detail.

Negotiation Tactics: Be Prepared to Walk Away

Armed with your pre-approval and research, you are in a strong negotiating position. Know the market value of the car you’re interested in, and be prepared to make a fair offer based on that knowledge and the car’s condition. Don’t be afraid to negotiate on the price.

Leverage your pre-approval as a negotiating chip. If the dealer knows you already have financing, they might be more willing to budge on the car’s price. The most powerful tactic you possess is the willingness to walk away if the deal isn’t right. There are always other cars available.

Understanding the Paperwork: Read Every Word

Once you agree on a price, you’ll be presented with a stack of paperwork. This includes the sales agreement, the loan documents, and various disclosures. Do not rush through this process. Read every single document carefully before signing.

Ensure the final sales price matches what you agreed upon, and that there are no hidden fees or unexpected charges. Verify that the loan terms (APR, term length, monthly payment) are exactly as you discussed and as per your pre-approval. If anything seems unclear or incorrect, ask for clarification. Don’t sign anything you don’t fully understand.

Insurance: Don’t Forget It!

Before you drive off the lot, you’ll need to secure insurance for your used car. Lenders typically require full coverage (comprehensive and collision) on financed vehicles to protect their investment. Without proof of insurance, you won’t be able to complete the purchase.

Get insurance quotes before you finalize the car purchase. Premiums can vary significantly based on the car’s make, model, year, your driving history, and your location. Factor these costs into your overall budget. Having quotes ready will prevent any last-minute surprises and ensure a smooth transaction.

Post-Purchase: Smart Ownership

Your journey doesn’t end when you drive your used car home. Smart ownership practices are key to protecting your investment and ensuring its longevity.

Establish a regular maintenance schedule based on the manufacturer’s recommendations. Timely oil changes, tire rotations, and fluid checks can prevent minor issues from becoming major, costly repairs. Keep detailed records of all maintenance and repairs for future reference and to enhance resale value.

As you pay down your loan, consistently making on-time payments will boost your credit score even further. If interest rates drop significantly or your credit score improves dramatically, you might consider refinancing your used car loan to secure an even lower interest rate, saving you more money over time.

Drive Away with Confidence

Buying a used car with a loan is a smart financial move that offers excellent value and accessibility. By meticulously planning your budget, understanding your credit, securing favorable financing, and thoroughly inspecting your chosen vehicle, you can navigate this process with confidence. This guide has equipped you with the expert knowledge to avoid common pitfalls and make a truly informed decision.

Your dream car, at an affordable price, is within reach. Start your journey today, armed with the insights you’ve gained, and drive away knowing you’ve made a financially sound choice. For more resources on consumer auto buying, you can visit the Federal Trade Commission’s guide on buying a car: https://www.consumer.ftc.gov/articles/buying-car