Driving Dreams: Your Ultimate Guide to Car Loans for Used Cars with Bad Credit

Driving Dreams: Your Ultimate Guide to Car Loans for Used Cars with Bad Credit Carloan.Guidemechanic.com

Getting a reliable set of wheels is often a necessity, not a luxury. Whether it’s for commuting to work, taking kids to school, or running essential errands, a car provides freedom and stability. But what if your credit history isn’t sparkling? Specifically, what if you’re looking for car loans for used cars with bad credit?

This can feel like an uphill battle, a daunting challenge that leaves many feeling stuck. However, I’m here to tell you that it’s absolutely possible. While it requires a strategic approach and realistic expectations, securing financing for a used car, even with a less-than-perfect credit score, is a path many have successfully navigated.

Driving Dreams: Your Ultimate Guide to Car Loans for Used Cars with Bad Credit

In this comprehensive guide, we’ll dive deep into everything you need to know. From understanding why bad credit is a hurdle to the practical steps you can take, and the common pitfalls to avoid, we’ll equip you with the knowledge to drive away in your next used car. Let’s hit the road!

The Reality of Bad Credit and Car Loans

Before we explore solutions, it’s crucial to understand why bad credit presents a challenge when seeking a car loan. Lenders assess risk; they want to know if you’re likely to repay the money they lend. Your credit score is their primary tool for this assessment.

A low credit score, generally considered anything below 600-620, signals to lenders that you might have had difficulty managing debt in the past. This could be due to late payments, defaults, bankruptcies, or a high debt-to-income ratio. For them, it translates to a higher risk of non-payment.

Because of this increased risk, lenders will either be more hesitant to approve your application or will offer you less favorable terms. This typically means higher interest rates and potentially shorter loan terms, leading to higher monthly payments. It’s their way of compensating for the perceived risk.

Is Getting a Used Car Loan with Bad Credit Truly Possible?

Yes, absolutely! While it’s more challenging than for someone with excellent credit, it is far from impossible. Many lenders specialize in what are known as "subprime auto loans," which are designed for individuals with lower credit scores.

The market for used cars also plays a significant role here. Used cars are generally less expensive than new ones, which means you’ll be borrowing a smaller amount. A smaller loan amount can be easier for lenders to approve, even with bad credit, because their exposure to risk is reduced.

Based on my experience, many people mistakenly believe they have "no options" if their credit score isn’t perfect. This simply isn’t true. It’s about knowing where to look, what to prepare, and how to present yourself as a reliable borrower.

Navigating the Road: Steps to Secure a Used Car Loan with Bad Credit

Securing a car loan when your credit isn’t ideal requires a methodical approach. Don’t rush into the first offer you see. Instead, follow these proven steps to maximize your chances of approval and secure the best possible terms.

1. Know Your Credit Score and Report Inside Out

This is your starting point, your baseline. Before you even think about visiting a dealership or applying for a loan, get a clear picture of your credit health. You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, TransUnion) once every 12 months through AnnualCreditReport.com.

What to look for:

- Errors: Incorrect accounts, wrong addresses, or identity theft can negatively impact your score. Dispute any inaccuracies immediately.

- Open Accounts: Understand all your current debts and credit lines.

- Payment History: Note any late payments or collections.

- Credit Utilization: How much of your available credit are you using? High utilization can lower your score.

Understanding your report allows you to anticipate what lenders will see and address any issues proactively. It also helps you understand why your score is what it is, empowering you to explain your situation if necessary.

2. Set a Realistic Budget

With bad credit, you’re likely to face higher interest rates. This makes budgeting even more critical. Don’t just think about the monthly car payment; consider the total cost of ownership.

Pro tips from us: Factor in insurance, fuel, maintenance, and potential repair costs for a used car. Use an online car loan calculator to see how different interest rates and loan terms affect your monthly payment. Aim for a payment that comfortably fits into your budget without straining your finances.

A common mistake to avoid is focusing solely on the monthly payment. A low monthly payment might sound appealing, but if it comes with an extremely long loan term and a high interest rate, you could end up paying significantly more over the life of the loan.

3. Save for a Down Payment

This is arguably one of the most impactful steps you can take to improve your chances of approval and secure better terms. A substantial down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk.

Benefits of a larger down payment:

- Increased Approval Odds: Lenders see you as more committed and less risky.

- Lower Monthly Payments: Less borrowed means less to repay each month.

- Reduced Interest Paid: You’re paying interest on a smaller principal amount.

- Positive Equity: You start with equity in the car, protecting you from being "upside down" (owing more than the car is worth).

Based on my experience, even 10-20% of the car’s price can make a significant difference. If you can, aim for more. It shows financial discipline and a genuine intent to repay.

4. Explore All Your Lender Options

Don’t limit yourself to just one type of lender. With bad credit, casting a wider net can yield better results.

- Dealership Financing (Special Finance Departments): Many larger dealerships have "special finance" departments that work with a network of subprime lenders. They are experienced in matching buyers with bad credit to suitable financing options.

- Online Lenders: Numerous online platforms specialize in bad credit auto loans. These can be a great starting point for pre-qualification, as they often have streamlined application processes and can connect you with multiple lenders.

- Credit Unions: Often overlooked, credit unions are member-owned and may be more willing to work with members who have bad credit, especially if you have a history with them. Their rates can sometimes be more competitive than traditional banks.

- Buy Here, Pay Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. While they often offer "guaranteed approval," their interest rates are typically very high, and the vehicle selection might be limited or higher priced. This should generally be a last resort.

Pro tips from us: Be wary of any lender promising "guaranteed approval for bad credit" without any conditions. Always read the fine print.

5. Get Pre-Qualified (Soft Inquiry)

Before you fall in love with a car, get pre-qualified for a loan. Many online lenders and some dealerships offer pre-qualification with a "soft inquiry," which doesn’t hurt your credit score.

Pre-qualification gives you a realistic idea of how much you can borrow, at what estimated interest rate, and under what terms. This empowers you when negotiating at the dealership, as you’ll know your buying power beforehand. It also prevents you from wasting time on cars outside your approved budget.

6. Consider a Co-Signer

If you have a trusted friend or family member with excellent credit who is willing to co-sign your loan, this can significantly improve your chances of approval and potentially secure a lower interest rate.

What a co-signer does: They legally agree to take responsibility for the loan if you fail to make payments. This reduces the lender’s risk. However, it’s a serious commitment for the co-signer, as any missed payments will affect their credit score as well. Ensure both parties fully understand the implications.

7. Gather All Necessary Documents

Being prepared can speed up the application process and show lenders you are serious and organized.

Documents you’ll likely need:

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residence (utility bill, lease agreement)

- Proof of identity (driver’s license, social security card)

- References (sometimes required)

- Proof of insurance (required before you drive off the lot)

Having these documents ready demonstrates reliability and efficiency.

What to Expect: Understanding the Terms of Your Bad Credit Car Loan

When you have bad credit, the terms of your car loan will likely differ from someone with a high credit score. It’s crucial to understand these differences to make an informed decision.

Higher Interest Rates

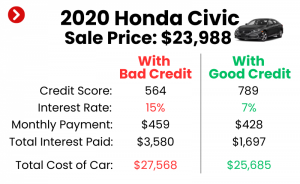

This is the most significant difference. Lenders charge higher interest rates to compensate for the increased risk associated with bad credit borrowers. While someone with excellent credit might get an APR of 3-5%, you might see rates ranging from 10% to 25% or even higher.

Pro tips from us: Don’t let a high interest rate deter you entirely, especially if you desperately need a car. Focus on securing a reliable vehicle now and then work on improving your credit to refinance the loan later.

Shorter Loan Terms (Sometimes Longer, But Be Cautious)

Sometimes, to make monthly payments more affordable despite high interest, lenders might offer longer loan terms (e.g., 72 or even 84 months). While this reduces the monthly payment, it significantly increases the total amount of interest you’ll pay over the life of the loan.

A common mistake to avoid is blindly accepting a longer term for a lower payment. Always calculate the total cost of the loan. Shorter terms, while having higher monthly payments, can save you thousands in interest over time.

Limited Vehicle Selection

With bad credit, lenders might impose restrictions on the age, mileage, or value of the car they’re willing to finance. They might prefer newer used cars with lower mileage because they represent less risk of immediate mechanical failure, which could jeopardize your ability to make payments.

This is why looking for a reliable, affordable used car is key. Focus on practicality and necessity over luxury.

Potential for Additional Fees

Be on the lookout for various fees that can inflate the cost of your loan. These might include origination fees, documentation fees, or loan processing fees. Always ask for a clear breakdown of all costs associated with the loan.

Improving Your Chances and Your Credit

Getting a car loan for a used car with bad credit isn’t just about securing financing; it’s also an opportunity to start rebuilding your credit.

Strategies to Enhance Your Loan Application:

- Demonstrate Stable Income: Lenders prioritize consistent income. Proof of steady employment and a stable income source can outweigh some negative credit history.

- Keep Your Debt-to-Income Ratio Low: Lenders look at how much of your income goes towards debt payments. Try to pay down other debts before applying for a car loan.

- Choose a Practical Car: Opt for an affordable, reliable used car rather than an expensive model. This shows financial responsibility and makes the loan more manageable.

- Be Honest About Your Credit: Don’t try to hide your credit situation. Be upfront about past issues and explain how you’ve improved your financial habits.

Rebuilding Your Credit Post-Loan:

Once you secure the loan, make every payment on time, every month. This is the single most effective way to improve your credit score.

- On-Time Payments: Payment history accounts for a significant portion of your credit score.

- Monitor Your Credit: Continue to check your credit report regularly for errors and to track your progress.

- Avoid New Debt: Try not to take on additional significant debt while you’re working on improving your credit.

Consistency is key here. Over time, responsible repayment of your auto loan will demonstrate to future lenders that you are a reliable borrower, opening doors to better financial opportunities.

Common Mistakes to Avoid When Seeking a Used Car Loan with Bad Credit

Navigating the world of bad credit auto loans can be tricky. Knowing what pitfalls to avoid is just as important as knowing what steps to take.

- Applying Everywhere: Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your score. Apply only with lenders you’ve researched and are likely to approve you. Group your applications within a short period (usually 14-45 days) so they count as a single inquiry for scoring purposes.

- Ignoring Your Budget: Don’t let the excitement of a new car overshadow financial prudence. Over-extending yourself can lead to missed payments, repossession, and further damage to your credit.

- Not Reading the Fine Print: Always read the entire loan agreement carefully. Understand the APR, loan term, total amount repayable, and any prepayment penalties.

- Settling for the First Offer: With bad credit, it’s easy to feel desperate and accept the first offer. Take the time to compare offers from different lenders. Even a small difference in APR can save you hundreds, if not thousands, over the life of the loan.

- Forgetting About Insurance: Car insurance is a non-negotiable expense. Get insurance quotes before finalizing your loan, as it can be a significant monthly cost, especially for certain vehicles.

Alternatives and Next Steps

If, after exploring all options, you find that a traditional bad credit car loan isn’t feasible right now, don’t despair. There are alternatives and strategies you can employ to improve your situation.

- Save More: Focus on saving a larger down payment. The more you put down, the less you need to borrow, making you a more attractive borrower.

- Improve Your Credit Score First: If your need for a car isn’t immediate, dedicate a few months to actively improving your credit score. Pay all bills on time, reduce credit card balances, and correct any errors on your credit report. For more detailed strategies, you might find our article on "How to Rapidly Improve Your Credit Score in 6 Months" helpful. (Internal Link Placeholder)

- Consider a Less Expensive Vehicle: Even within the used car market, there’s a wide range of prices. Lowering your target price can make financing easier.

- Public Transportation/Ridesharing: While not ideal for everyone, using these options temporarily can help you save money and build credit before committing to a car loan.

For additional unbiased information on consumer credit and financial management, I recommend exploring resources from the Consumer Financial Protection Bureau (CFPB). (External Link)

Conclusion: Your Journey to a Used Car with Bad Credit

Securing a car loan for a used car when you have bad credit is a journey that requires patience, preparation, and perseverance. It’s not about magic bullet solutions, but about understanding the landscape and taking smart, strategic steps.

By knowing your credit, budgeting wisely, saving for a down payment, exploring diverse lenders, and understanding loan terms, you significantly increase your chances of success. Remember, this isn’t just about getting a car; it’s also an opportunity to demonstrate financial responsibility and rebuild your credit for a brighter financial future.

Don’t let a past credit stumble define your present needs. With the right approach, you can absolutely find a reliable used car and get back on the road. We hope this comprehensive guide empowers you to make informed decisions and achieve your goal of car ownership. Drive safely, and drive smartly!