Driving Dreams: Your Ultimate Guide to DACA Friendly Car Loans

Driving Dreams: Your Ultimate Guide to DACA Friendly Car Loans Carloan.Guidemechanic.com

For many DACA recipients, securing a car loan can feel like navigating a complex maze with invisible walls. The dream of owning a reliable vehicle – essential for work, education, and daily life – often comes with unique financial challenges. Yet, the good news is that securing a DACA-friendly car loan is absolutely possible. It requires understanding the landscape, knowing your options, and presenting your financial profile strategically.

This comprehensive guide is designed to empower DACA recipients with the knowledge and tools needed to drive away in their own car. We’ll break down the myths, outline the steps, and share expert insights to help you secure an auto loan that fits your needs. Our goal is to make this process transparent, accessible, and ultimately, successful for you.

Driving Dreams: Your Ultimate Guide to DACA Friendly Car Loans

Understanding the DACA Landscape for Auto Financing

The journey to car ownership for DACA recipients often differs from that of U.S. citizens or permanent residents. Lenders typically assess risk based on factors like credit history, income stability, and residency status. For DACA individuals, perceived temporary status and a potentially limited credit footprint can sometimes lead to hesitation from traditional lenders.

However, it’s crucial to understand that your DACA status does not automatically disqualify you from getting a car loan. Many financial institutions recognize the stability and contributions of DACA recipients. They are increasingly adapting their lending practices to accommodate individuals with Employment Authorization Documents (EADs) and Social Security Numbers (SSNs). The key is to know which lenders are DACA friendly and what specific criteria they prioritize.

Based on my experience working with numerous DACA recipients, the biggest hurdle isn’t always eligibility, but rather knowing where to look and how to present your financial story effectively. Many DACA recipients are financially stable, employed, and diligent payers, yet they face unnecessary hurdles due to a lack of specific guidance. This article aims to fill that gap.

Key Factors Lenders Consider for DACA Applicants

When a DACA recipient applies for a car loan, lenders evaluate several critical aspects to determine their creditworthiness and ability to repay the loan. Understanding these factors can help you prepare a stronger application.

1. Employment Authorization Document (EAD) Validity

Your EAD, also known as a work permit, is perhaps the most critical document. It confirms your legal ability to work in the United States. Lenders want assurance that you have a stable income source for the duration of the loan. The longer the validity period remaining on your EAD, the more comfortable lenders generally feel.

It’s highly advisable to apply for your car loan when your EAD has a significant period of validity remaining, ideally six months or more. Some lenders might require at least 12 months remaining on your EAD, especially for longer loan terms. This shows a reduced risk of income interruption.

2. Stable Income and Employment History

Lenders look for consistent employment and a verifiable income. This demonstrates your capacity to make regular loan payments. They will typically ask for pay stubs, W-2 forms, or tax returns to confirm your income.

A steady job history, ideally with the same employer for a year or more, strengthens your application. Even if you’ve changed jobs, consistent employment in your field shows reliability. Lenders want to see a predictable cash flow that can comfortably cover your monthly car payments alongside other living expenses.

3. Credit History (or Lack Thereof)

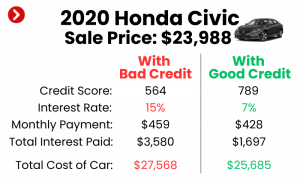

A strong credit history is a lender’s primary indicator of financial responsibility. This includes a track record of paying bills on time, managing credit cards, and handling previous loans. For many DACA recipients, especially those who arrived in the U.S. at a young age, building a traditional credit history can be a challenge.

Don’t despair if your credit history is thin or non-existent. Some DACA-friendly lenders are willing to look beyond a perfect credit score. They might consider alternative data, such as utility bill payments, rent payments, or bank account stability. However, actively working to build your credit will always put you in a better position.

4. Down Payment Amount

A substantial down payment significantly reduces the risk for lenders. When you put down a larger sum of money upfront, you’re financing a smaller amount, which means lower monthly payments and less risk for the lender in case of default. It also shows your financial commitment to the purchase.

Based on my experience, aiming for a down payment of at least 10-20% of the car’s purchase price can dramatically improve your chances of approval and potentially secure a better interest rate. This is especially true if your credit history is still developing.

5. Length of DACA Status and Renewal History

While not always explicitly stated, some lenders might subtly consider how long you’ve held DACA status and your history of timely renewals. A consistent record of renewing your DACA status demonstrates stability and a commitment to maintaining your legal work authorization.

This factor speaks to the perceived long-term stability of your residency and employment. A longer, uninterrupted DACA history can reassure lenders about your future ability to maintain employment and, consequently, repay your loan.

6. Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)

Most DACA recipients have an SSN, which is essential for reporting your credit activity to the major credit bureaus. If for some reason you only have an ITIN, it’s a bit more challenging but not impossible. Lenders primarily use SSNs to access credit reports and track loan performance.

If you have an SSN, ensure it’s accurately provided on your application. If you only have an ITIN, you will need to seek out lenders who specifically cater to ITIN holders, which are fewer but do exist. Always clarify this with the lender upfront.

Strategies for Securing a DACA Friendly Car Loan

Now that you understand what lenders look for, let’s explore actionable strategies to strengthen your application and find the right financing.

1. Building a Strong Credit Profile

Even if you have thin credit, it’s never too late to start building it. This is a foundational step for any major financial transaction.

- Secured Credit Cards: These cards require a cash deposit that becomes your credit limit. By using it responsibly and paying on time, you demonstrate creditworthiness.

- Credit Builder Loans: Offered by some credit unions and community banks, these loans place the borrowed money in a savings account while you make payments. Once paid off, you get access to the funds and have a positive payment history reported.

- Authorized User Status: If a trusted family member with excellent credit is willing, becoming an authorized user on their credit card can help you piggyback on their good credit history. However, ensure they maintain good payment habits.

- Pay Bills On Time: This includes rent, utilities, and any other regular payments. While not always reported to credit bureaus, consistent payment history shows responsibility.

2. Gathering Necessary Documentation

Being prepared with all required documents streamlines the application process and shows you’re serious.

- Employment Authorization Document (EAD): Original and copies.

- Social Security Card: Or ITIN documentation.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms (last 1-2 years), or tax returns if self-employed.

- Proof of Residency: Utility bills, bank statements, or a lease agreement with your current address.

- Bank Statements: Showing consistent income and savings.

- Driver’s License: A valid U.S. driver’s license is usually required.

3. The Power of a Down Payment

As mentioned, a larger down payment is your friend. It reduces the amount you need to borrow, which can lead to lower interest rates and more favorable loan terms.

Think of your down payment as a statement of commitment. Lenders see it as you having "skin in the game," making you less likely to default. It can also help offset any perceived risks associated with a limited credit history. If you can save up, even an extra 5% can make a significant difference.

4. Considering a Co-Signer

A co-signer can be a game-changer, especially if you have limited credit or a shorter DACA validity period. A co-signer is someone with excellent credit who agrees to be equally responsible for the loan if you default.

- Who Makes a Good Co-Signer? Someone with a strong credit score, stable income, and a long history of financial responsibility. This is often a trusted family member or close friend.

- Risks and Responsibilities: Both you and your co-signer are legally bound to the loan. If you miss payments, it impacts both your credit scores, and the co-signer is on the hook for the remaining balance.

- When It’s a Good Idea: If you’re confident in your ability to make payments but need that extra boost to secure better terms, a co-signer can be invaluable. It can help you get approved or qualify for a significantly lower interest rate.

5. Exploring Different Lender Types

Not all lenders are created equal, especially for DACA recipients. Shopping around is crucial.

- Credit Unions: Often more community-focused and flexible than large banks. They tend to have more personalized lending approaches and may be more understanding of unique financial situations, including DACA status. They often offer competitive rates.

- Community Banks: Similar to credit unions, smaller local banks may offer more tailored solutions and be more willing to work with DACA applicants.

- Online Lenders: Some online lenders specialize in non-traditional borrowers or offer more flexible criteria. Do thorough research, read reviews, and ensure they are reputable.

- Dealership Financing: While convenient, dealership financing can sometimes have higher interest rates, especially if they know you have limited options. Always compare their offer with pre-approvals you’ve secured elsewhere.

- Avoid Buy Here, Pay Here (BHPH): Pro tips from us: Common mistakes to avoid are rushing into the first offer you receive, especially from "buy here, pay here" lots. These establishments often cater to individuals with poor credit but typically come with extremely high interest rates, predatory terms, and can trap you in a cycle of debt. They rarely report to major credit bureaus, so they won’t help build your credit either.

The Application Process: Step-by-Step Guide for DACA Recipients

Applying for a car loan can seem daunting, but breaking it down into manageable steps makes it easier.

Step 1: Know Your Credit (or Lack Thereof)

Before you even think about cars, get a clear picture of your credit. Obtain your free credit report from AnnualCreditReport.com. Review it for any errors and understand your credit score. If you have no score, that’s okay; you’ll focus on demonstrating financial stability and income.

Understanding your credit profile (or lack of one) helps you anticipate what lenders will see. It also empowers you to address any inaccuracies or begin the process of building credit proactively.

Step 2: Budgeting and Affordability

Determine how much car you can truly afford. This isn’t just about the monthly payment; it includes insurance, gas, maintenance, and potential repair costs. Use an online car loan calculator to estimate payments based on different interest rates and loan terms.

Overextending yourself on a car loan is a common mistake. Based on my experience, a good rule of thumb is that your total car expenses (payment, insurance, gas) shouldn’t exceed 10-15% of your net monthly income.

Step 3: Get Pre-Approved

Pro tips from us: Always get pre-approved before stepping onto a dealership lot. This gives you significant leverage during negotiations. A pre-approval tells you exactly how much you can borrow, at what interest rate, and under what terms.

Having a pre-approval in hand means you walk into the dealership as a cash buyer, focusing on the car price, not the financing. This prevents the dealer from inflating prices or adding unnecessary fees.

Step 4: Shop Smart for Your Vehicle

Once pre-approved, focus on finding the right car within your budget. Research different makes and models, read reviews, and compare prices from various dealerships. Consider a reliable used car to start; they depreciate slower and are generally more affordable.

Don’t feel pressured to buy the first car you see. Take your time, test drive several options, and ensure the vehicle meets your needs and budget.

Step 5: Negotiation

Negotiate the car’s price first, separate from financing. If you have a pre-approval, use it as your baseline. Don’t be afraid to walk away if you don’t feel you’re getting a fair deal. Dealerships often have flexibility, especially towards the end of the month.

Remember, the goal is to get the best overall deal, which includes both the car price and the loan terms. Having done your homework on both fronts will serve you well.

Step 6: Read the Fine Print

Before signing anything, meticulously read the entire loan agreement. Understand the interest rate, annual percentage rate (APR), loan term, total amount to be paid, and any fees or penalties for late payments. Ask questions about anything you don’t understand.

Never rush through this stage. This is a legally binding contract, and understanding every clause protects you from future surprises.

Common Mistakes DACA Applicants Make (and How to Avoid Them)

Navigating the car loan process can be tricky, and certain missteps can hinder your chances or lead to unfavorable terms.

- Not Understanding Their Credit Situation: Many DACA recipients assume they have no credit and don’t bother to check. This can lead to missed opportunities or accepting higher rates than necessary. Always get your credit report.

- Not Having Proper Documentation: Arriving at a lender or dealership without all required documents can cause delays, frustration, and even denial. Be organized and bring everything they might need.

- Falling for Predatory Loans: As mentioned, "buy here, pay here" lots and other lenders offering "guaranteed approval" often charge exorbitant interest rates. These loans can cripple your finances. Always compare offers and prioritize reputable lenders.

- Not Shopping Around for Lenders: Settling for the first offer you receive is a common mistake. Different lenders have different criteria and rates. Get quotes from at least 3-5 different sources (credit unions, banks, online lenders) to find the best deal.

- Not Negotiating Effectively: Whether it’s the car price or the loan terms, negotiation is key. If you don’t ask, you don’t get. Be confident, informed, and prepared to counter offers.

Pro Tips for DACA Recipients on Their Car Loan Journey

Beyond the core strategies, here are some additional insights to help you succeed:

- Focus on Financial Stability: The more stable your finances appear, the better. This includes having a consistent job, a savings account, and managing any existing debts responsibly.

- Maintain Consistent Employment: Lenders favor applicants with a steady work history. Try to avoid frequent job changes leading up to your loan application.

- Renew DACA Early and Consistently: Timely DACA renewals demonstrate responsibility and ensure continuous work authorization, which reassures lenders. Don’t let your EAD expire.

- Be Transparent with Lenders: Don’t hide your DACA status. Instead, be upfront and ask if they have experience working with DACA recipients. This saves time and helps you find DACA-friendly lenders faster.

- Don’t Be Afraid to Ask Questions: If you don’t understand something, ask. A reputable lender will take the time to explain the terms and conditions clearly.

- Consider a Used Car First: For your first car loan, a reliable used car is often a more financially savvy choice. It’s less expensive, meaning a smaller loan, potentially lower payments, and a quicker path to building positive credit history.

Beyond the Loan: Building Your Financial Future

Securing a DACA-friendly car loan is not just about getting a car; it’s a significant step in building your financial future in the United States.

- Importance of Paying On Time: Making every payment on time is paramount. This builds a strong positive payment history, which is the most crucial factor in your credit score. This car loan can be a powerful tool for establishing excellent credit.

- Using the Car Loan to Build Credit: As you consistently make on-time payments, the loan activity will be reported to credit bureaus. Over time, this will build a robust credit history, opening doors to other financial products like mortgages or better credit cards in the future.

- Exploring Refinancing Options Down the Line: Once you’ve established a strong payment history for 12-24 months and your credit score has improved, you might be eligible to refinance your car loan at a lower interest rate. This can save you a substantial amount of money over the life of the loan.

For more information on DACA, visit the official USCIS website:

Conclusion: Your Path to Car Ownership is Within Reach

The journey to securing a DACA-friendly car loan may present unique challenges, but it is a journey well worth taking. With the right preparation, knowledge, and strategic approach, DACA recipients can absolutely achieve their dream of car ownership.

Remember, you are not alone in this process. Many DACA-friendly lenders recognize your contributions and are ready to work with you. By understanding the key factors lenders consider, building a strong financial profile, and carefully navigating the application process, you can secure favorable financing. Take these steps with confidence, and soon you’ll be driving towards a brighter, more independent future. Your dream car is waiting!