Driving Dreams: Your Ultimate Guide to Securing a $3000 Car Loan with Bad Credit

Driving Dreams: Your Ultimate Guide to Securing a $3000 Car Loan with Bad Credit Carloan.Guidemechanic.com

Life can throw unexpected curveballs, and sometimes, those curveballs include a less-than-perfect credit score when you desperately need a reliable set of wheels. The thought of securing any loan, let alone an auto loan, with bad credit can feel like an uphill battle. But what if you only need a modest amount, like a $3000 car loan? Is it truly possible to get approved, even with a challenging credit history?

The answer, thankfully, is yes – but it requires a strategic approach, a clear understanding of the landscape, and a commitment to smart financial decisions. This comprehensive guide is designed to empower you, providing unique insights and actionable steps to navigate the world of subprime auto financing. Our ultimate goal is to help you drive away in a car that meets your needs, even with bad credit.

Driving Dreams: Your Ultimate Guide to Securing a $3000 Car Loan with Bad Credit

Understanding the $3000 Car Loan with Bad Credit Landscape

When we talk about a "$3000 car loan bad credit," we’re usually referring to financing a used vehicle at the lower end of the price spectrum. This amount is often sought by individuals who need basic transportation for work, school, or essential errands, where an expensive new car simply isn’t an option or a priority.

Bad credit, in this context, typically means a FICO score below 620, though some lenders consider scores up to 660 as "subprime." Lenders view bad credit as an indicator of higher risk, making them more hesitant to approve loans. However, specialized lenders and specific strategies exist to bridge this gap.

Why a $3000 Loan and What "Bad Credit" Means for Auto Financing

A $3000 car loan often targets older, higher-mileage vehicles that are still mechanically sound enough to provide reliable transport. These cars are a lifeline for many, especially when public transportation isn’t an option. The lower principal amount can make lenders more amenable, even with bad credit, compared to a much larger loan.

For lenders, "bad credit" isn’t just a number; it tells a story of past financial struggles, such as missed payments, defaults, or bankruptcies. When assessing your application, they’re looking at your credit history to gauge your likelihood of repaying the new loan. It’s crucial to remember that while your past is important, your current financial stability and willingness to pay are also significant factors.

The Reality of "Guaranteed Approval" Car Loans

You might encounter advertisements promising "guaranteed approval car loans" or "no credit check car loan" options. Based on my experience, it’s vital to approach these claims with extreme caution. True "guaranteed approval" is almost nonexistent in legitimate lending, as lenders always perform some level of due diligence to assess risk.

Often, these offers come with exceptionally high interest rates, predatory terms, or may lead you to "buy here, pay here" dealerships with inflated prices and less consumer protection. While they might get you a car, the long-term financial cost can be crippling. Our pro tip is to always scrutinize any offer that seems too good to be true, as it usually is.

The Challenges of Securing an Auto Loan with Bad Credit

Navigating the path to a car loan with bad credit presents a unique set of challenges. Understanding these hurdles beforehand can help you prepare and avoid common pitfalls. The key is to be realistic and proactive in addressing potential issues.

Higher Interest Rates and Loan Costs

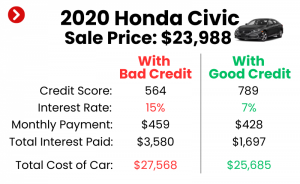

The most significant challenge for individuals with bad credit is the higher interest rates they face. Lenders charge more to compensate for the increased risk they’re taking. This means that a $3000 car loan could end up costing you significantly more over the loan term compared to someone with excellent credit.

It’s not uncommon to see annual percentage rates (APRs) for subprime auto loans in the double digits, sometimes even reaching 20-30% or more. This higher interest directly translates into larger monthly payments and a greater total cost for the car. Understanding the full cost, not just the monthly payment, is paramount.

Stricter Lender Requirements and Limited Options

Lenders specializing in bad credit car loans often have more stringent requirements beyond just your credit score. They might ask for detailed proof of income, employment history, residency stability, and a lower debt-to-income ratio. The pool of lenders willing to finance individuals with bad credit is also smaller, limiting your options compared to prime borrowers.

Common mistakes to avoid include applying with too many different lenders simultaneously, as each "hard inquiry" can further ding your credit score. Instead, focus on targeted applications with lenders known to work with bad credit.

Potential for Predatory Lending Practices

Unfortunately, where there’s vulnerability, there can be exploitation. The bad credit auto loan market is not immune to predatory lenders who might offer unfavorable terms. These can include excessively high interest rates, hidden fees, long loan terms that make you pay more interest, or loans that exceed the car’s value.

Based on my experience, always read the fine print carefully, and if something feels off, walk away. Don’t be pressured into signing anything you don’t fully understand or agree with. Trust your gut and seek a second opinion if necessary.

Preparing for Your $3000 Car Loan Application

Preparation is your most powerful tool when seeking a car loan with bad credit. A well-prepared applicant demonstrates responsibility and seriousness, which can positively influence a lender’s decision. This phase is about gathering information and strengthening your financial position as much as possible.

Check Your Credit Report and Dispute Errors

Before you even think about applying for a loan, get a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion). You can do this for free annually at AnnualCreditReport.com. Review it meticulously for any errors or inaccuracies.

Mistakes on your credit report are surprisingly common, and disputing them can potentially boost your credit score. Even a small improvement can make a difference in your loan eligibility and interest rate. This step also gives you a clear picture of what lenders will see.

Understand Your Budget Beyond the Monthly Payment

While the monthly payment is important, a truly comprehensive budget considers the total cost of car ownership. This includes not just the loan payment, but also insurance, fuel, maintenance, and potential repairs. For a $3000 car, especially an older model, maintenance costs can be a significant factor.

Pro tips from us: Create a realistic budget that accounts for all these expenses. Can you comfortably afford the payment and all the other costs without straining your finances? Lenders will look at your ability to repay, and showing you’ve thought this through demonstrates financial maturity.

Save for a Down Payment – Even a Small Amount Helps

Even a small down payment can make a significant difference when applying for a bad credit car loan. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid. More importantly, it signals to lenders that you are financially invested in the purchase.

A down payment also reduces the lender’s risk, as you immediately have equity in the vehicle. For a $3000 car loan, even $300-$500 down can be a strong positive indicator. It shows you’re committed and have some savings.

Gather Necessary Documents

Lenders will require several documents to verify your identity, income, and residency. Having these ready will streamline the application process. Typically, you’ll need:

- Proof of Income: Recent pay stubs (usually 2-3 months), bank statements, or tax returns if self-employed.

- Proof of Residency: Utility bills, lease agreement, or mortgage statements.

- Proof of Identity: Driver’s license or state-issued ID.

- Social Security Number.

- References: Sometimes requested, usually personal references.

Being organized and having all your paperwork in order shows you are a serious and responsible applicant.

Know Your Car Needs: Realistic Expectations

With a $3000 car loan, your options will be limited to older, potentially higher-mileage vehicles. It’s important to set realistic expectations. You won’t be getting a luxury vehicle or a brand-new model. Focus on reliability, safety, and functionality.

Consider what you truly need in a car versus what you want. A basic sedan or hatchback that gets you from point A to point B reliably is often the best choice in this price range. Prioritize good maintenance history over flashy features.

Finding the Right Lenders for Bad Credit Car Loans

Not all lenders are created equal, especially when it comes to financing for individuals with bad credit. Knowing where to look and understanding the different types of lenders can significantly improve your chances of approval.

Subprime Lenders: Specialists in Bad Credit Auto Loans

Subprime lenders specialize in providing loans to individuals with less-than-perfect credit scores. They understand the challenges and structure their loans to accommodate higher risk. These lenders often look beyond just your credit score, considering factors like your employment history, income stability, and ability to make a down payment.

While their interest rates are higher than prime lenders, they offer a viable path to securing an auto loan when traditional banks might say no. Many online platforms connect you with a network of subprime lenders, allowing you to compare offers.

Dealership Financing: "Buy Here, Pay Here" Options

Many dealerships offer in-house financing, particularly "Buy Here, Pay Here" (BHPH) dealerships. These establishments lend money directly to customers, often without extensive credit checks, making them an option for those with very poor credit. The approval process can be quicker and less stringent.

However, common mistakes to avoid with BHPH dealerships include inflated car prices, very high interest rates, and often less flexible payment terms. They might also have limited vehicle selection and fewer consumer protections. While they offer accessibility, it’s crucial to understand the total cost and all terms before committing.

Credit Unions: Often More Lenient

Credit unions are member-owned financial institutions known for their customer-centric approach. They often have more flexible lending criteria than large banks and may be more willing to work with members who have bad credit. Their interest rates are also generally more competitive.

If you’re a member of a credit union, or eligible to join one, it’s definitely worth exploring their auto loan options. They tend to prioritize relationship banking, which can be beneficial for borrowers with challenging credit histories.

Online Lenders: Convenience and Multiple Offers

The internet has opened up numerous avenues for bad credit auto loans. Many online lenders and marketplaces specialize in connecting borrowers with subprime auto lenders. The convenience of applying from home and potentially receiving multiple offers without visiting various dealerships is a major advantage.

Based on my experience, online platforms can save you time and help you compare different interest rates and terms. Just ensure you’re using reputable sites and carefully review any loan offers you receive. Look for transparent terms and positive customer reviews.

The Application Process: What to Expect

Once you’ve done your preparation and identified potential lenders, it’s time to apply. Understanding the process and knowing what to expect can reduce stress and help you make informed decisions.

Filling Out the Application and Providing Information

The application process will typically involve providing personal information, employment details, income verification, and residency proof. Be honest and thorough in your application. Any discrepancies can delay or even derail your approval.

Lenders will use this information, along with a credit check, to assess your ability to repay the loan. They’ll want to see stability in your employment and income. For a $3000 car loan, showing consistent income is often more important than a pristine credit score.

Understanding Terms and Conditions (APR, Loan Term, Fees)

Once approved, you’ll receive a loan offer outlining the terms and conditions. Pay close attention to the Annual Percentage Rate (APR), which reflects the true cost of borrowing, including interest and some fees. Compare the APR, not just the interest rate, across different offers.

Also, examine the loan term (how long you have to repay) and any associated fees, such as origination fees or late payment penalties. A longer loan term might mean lower monthly payments, but you’ll pay more in total interest over time.

The Importance of Reading the Fine Print

This cannot be stressed enough: read every single word of your loan agreement. Do not sign anything you don’t fully understand. Ask questions about anything that is unclear, including prepayment penalties, default clauses, and repossession policies.

Pro tips from us: If possible, take the loan documents home to review them without pressure, or bring a trusted advisor with you. This is especially critical with bad credit car loans, where terms can sometimes be less favorable.

Negotiating Your Loan (Even with Bad Credit)

While your negotiation power might be limited with bad credit, it’s not entirely absent. You can still try to negotiate the interest rate, loan term, or even the price of the car itself. For example, if you have a significant down payment or a co-signer, you might have more leverage.

Don’t be afraid to walk away if the terms aren’t acceptable. Having a pre-approved offer from another lender (if you’ve applied to multiple) can also give you a stronger negotiating position.

Alternative Strategies and Co-Signers

Sometimes, even with careful preparation, securing a $3000 car loan with bad credit can be challenging. Exploring alternative strategies, such as involving a co-signer, can significantly improve your chances.

The Power of a Co-Signer

A co-signer is someone with good credit who agrees to take on the legal responsibility for your loan if you fail to make payments. This significantly reduces the risk for the lender, making them more likely to approve your application and potentially offer a lower interest rate.

However, a co-signer takes on a serious financial obligation. Their credit will be affected if you miss payments, and they will be legally bound to repay the loan. Common mistakes to avoid include not fully discussing the responsibilities with your co-signer. Ensure both parties understand the commitment.

Secured Loans (Less Common for $3000 Cars)

While less common for a $3000 car loan, a secured loan involves offering collateral (like savings or another asset) to back the loan. This reduces the lender’s risk and can make approval easier, even with bad credit. However, the risk is that you could lose your collateral if you default.

For a $3000 car, the car itself typically serves as collateral for the loan. Using additional collateral might be an option if you have significant assets and are struggling to get approved otherwise.

Private Sales with a Personal Loan (Proceed with Caution)

Another approach could be to secure a personal loan and use the funds to purchase a car from a private seller. Personal loans can sometimes have better interest rates than subprime auto loans, but they are often harder to get with bad credit.

Furthermore, if you purchase from a private seller, you won’t have the same consumer protections as buying from a dealership. You’ll be responsible for all inspections and verifying the car’s condition. This strategy requires more legwork and a higher level of caution.

Managing Your $3000 Car Loan and Improving Your Credit

Getting the loan is only half the battle. Successfully managing your $3000 car loan can be a powerful stepping stone to improving your credit score and securing better financial opportunities in the future. This is where your commitment to financial responsibility truly shines.

Make Payments On Time, Every Time

This is the single most important action you can take. Your payment history accounts for the largest portion of your credit score (35%). Making all your car loan payments on time will demonstrate responsible financial behavior to credit bureaus.

Set up automatic payments, mark your calendar, or do whatever it takes to ensure you never miss a due date. Each on-time payment is a positive mark on your credit report, slowly building a better financial future.

Avoid Missing Payments and Understand the Consequences

Missing even one payment can have serious negative repercussions. It can significantly drop your credit score, incur late fees, and damage your relationship with the lender. Repeated missed payments can lead to repossession of your vehicle, further devastating your credit.

Based on my experience, if you foresee difficulty making a payment, contact your lender immediately. They may be willing to work with you on a temporary payment plan or deferral, which is always better than simply missing a payment.

Don’t Take on More Debt While Building Credit

While you’re working to improve your credit with your car loan, avoid taking on additional debt. Applying for new credit cards or other loans can signal financial instability to credit bureaus and lenders. Focus on responsibly managing your existing debt.

Your goal should be to show a pattern of consistent, reliable repayment. This period is about demonstrating your ability to handle existing credit responsibly, not about acquiring more.

Monitor Your Credit Score and See Your Progress

Regularly check your credit score and report to see the positive impact of your on-time payments. Seeing your score gradually improve can be incredibly motivating and confirms that your efforts are paying off. Many banks and credit card companies now offer free credit score monitoring.

Understanding what factors influence your score will also help you make better financial decisions. This loan can be a powerful tool for credit rebuilding if managed correctly.

What Kind of Car Can You Get for $3000?

With a $3000 budget, whether financed or cash, setting realistic expectations for the vehicle itself is crucial. This isn’t about luxury; it’s about reliability and practicality.

Realistic Expectations: Older Models, Higher Mileage

For $3000, you’ll generally be looking at cars that are 10-15+ years old, with mileage often well over 100,000 miles. Think popular, dependable models known for their longevity, such as older Honda Civics, Toyota Corollas, Ford Focuses, or some Chevrolet models.

The key is to find a car that has been well-maintained throughout its life, rather than one that just looks good. Minor cosmetic flaws are often acceptable if the mechanics are sound.

The Absolute Importance of a Pre-Purchase Inspection

Never, under any circumstances, buy a used car without a pre-purchase inspection (PPI) by an independent, trusted mechanic. For a $3000 car, this step is non-negotiable. Even if the car seems perfect, an expert eye can uncover hidden issues that could cost you hundreds or thousands down the line.

A PPI typically costs around $100-$200, which is a small price to pay to avoid buying a lemon. It can save you from immediate repair costs that far exceed the car’s value.

Focus on Reliability Over Luxury

When your budget is $3000, reliability should be your number one priority. Research models known for their durability and low cost of ownership. Avoid cars with known chronic issues or those that are expensive to repair.

While a car might not be flashy, a reliable vehicle will provide the transportation you need without unexpected breakdowns and costly fixes. This focus helps ensure your $3000 car loan truly serves its purpose.

For further reading on specific models that offer good value in this price range, you might find our article helpful in understanding the types of vehicles often financed through these avenues.

Conclusion: Your Path to a Car with Bad Credit is Achievable

Securing a $3000 car loan with bad credit is undoubtedly a challenging endeavor, but as we’ve explored, it is entirely achievable with the right approach. It requires thorough preparation, careful lender selection, diligent management of your loan, and realistic expectations for both the financing and the vehicle itself.

By understanding your credit situation, budgeting wisely, saving for a down payment, and diligently making your payments on time, you’re not just getting a car; you’re taking a significant step towards rebuilding your financial health. This loan can be a powerful tool for demonstrating responsibility and paving the way for a brighter financial future.

Don’t let a past credit stumble deter you from the essential transportation you need. Take these steps, be persistent, and you can drive away with confidence. Start your journey today – prepare, research, and drive smart!

External Resource: For more information on understanding your credit score and reports, visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/