Driving Dreams: Your Ultimate Guide to Securing a Car Loan with No Credit and No Money Down

Driving Dreams: Your Ultimate Guide to Securing a Car Loan with No Credit and No Money Down Carloan.Guidemechanic.com

The dream of owning a car is a common one, offering freedom, convenience, and independence. But what if you’re standing at the starting line with no credit history to speak of and no cash for a down payment? The phrase "car loan no credit no money down" often sounds like an impossible quest, a financial unicorn that simply doesn’t exist. Many believe it’s a myth, a fantasy peddled by predatory lenders.

However, based on my experience in the automotive finance industry and years of observing lending trends, while challenging, securing a car loan under these exact circumstances isn’t entirely out of reach. It requires a deep understanding of the market, strategic planning, and a willingness to explore unconventional paths. This comprehensive guide is designed to empower you with the knowledge and strategies needed to navigate this complex landscape successfully. We’ll break down the hurdles, explore viable solutions, and offer pro tips to help you get behind the wheel, even when traditional routes seem closed.

Driving Dreams: Your Ultimate Guide to Securing a Car Loan with No Credit and No Money Down

Understanding the "No Credit, No Money Down" Challenge

Before diving into solutions, let’s dissect why securing a car loan with no credit and no money down is perceived as such a monumental task. Lenders, at their core, are in the business of assessing risk. When you present yourself with no credit history and no down payment, you’re essentially a blank slate with no financial track record and no immediate equity in the vehicle.

The "No Credit" Dilemma: A Lack of Financial Footprint

Having "no credit" is distinct from having "bad credit." Bad credit means you have a history of missed payments or financial difficulties, signaling a high-risk borrower. No credit, on the other hand, means lenders have no data to evaluate your past financial behavior. They can’t see if you pay bills on time, how much debt you manage, or if you’ve ever defaulted.

This lack of information makes it difficult for them to predict your future payment habits. Traditional lenders, like big banks and credit unions, often rely heavily on credit scores (FICO, VantageScore) to make lending decisions. Without a score, you’re an unknown variable, and unknowns equal risk in their eyes.

The "No Money Down" Hurdle: Why Lenders Prefer Equity

A down payment serves multiple crucial purposes for a lender. First, it reduces the amount of money they need to lend you, thereby decreasing their exposure to risk. Second, it immediately gives you equity in the vehicle. This equity means you have a vested interest in the car and are less likely to default on the loan, as doing so would mean losing your initial investment.

Without a down payment, the loan amount is 100% of the car’s value, or even more if you roll taxes and fees into the loan. This situation, known as being "upside down" or "underwater" on a loan from day one, means you owe more than the car is worth. If you default, the lender might not recoup their full investment if they have to repossess and sell the vehicle.

Is Securing a Car Loan with No Credit & No Money Down Really Possible?

The short answer is: yes, but with caveats. It’s not a common or easy path, and it often comes with less favorable terms. However, it’s not entirely impossible. Success hinges on being resourceful, understanding your options, and setting realistic expectations.

You might not walk into a luxury dealership and drive away with a brand-new car under these conditions. However, a reliable, used vehicle could be within reach. The key is to be prepared for higher interest rates and potentially shorter loan terms, reflecting the increased risk lenders are taking.

Strategies for Securing a Car Loan with No Credit & No Money Down

Now that we understand the challenges, let’s explore actionable strategies. From years of observing financing trends, I’ve seen these approaches prove successful for many individuals in similar situations.

1. Explore Alternative Lenders: Beyond Traditional Banks

When big banks say no, it’s time to look elsewhere. Several types of lenders specialize in working with individuals who have limited or no credit history.

- Buy Here Pay Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. They often don’t rely on traditional credit scores and instead focus on your income and ability to make payments.

- Pro Tip: While BHPH can be a lifeline, their interest rates are typically much higher than traditional loans. Always read the fine print carefully, understand the total cost of the loan, and ensure they report payments to credit bureaus to help you build credit.

- Internal Link Opportunity: For those exploring options beyond traditional financing, our deep dive into Understanding Buy Here Pay Here Dealerships: Pros, Cons, and What to Expect offers valuable insights.

- Credit Unions: Unlike banks, credit unions are member-owned and often more flexible in their lending criteria. They are known for working with members who have unique financial situations, including those with limited credit.

- They might be willing to approve a loan based on your relationship with the credit union, your employment history, or if you agree to specific conditions, like setting up automatic payments from your account.

- Common Mistake to Avoid: Don’t assume all credit unions are the same. Shop around and discuss your specific situation with loan officers.

2. The Power of a Co-signer

A co-signer is someone with good credit who agrees to take legal responsibility for your loan if you fail to make payments. This significantly reduces the risk for the lender, as they now have two parties to pursue for payment.

- Choosing a Co-signer: This should be someone you trust implicitly, like a parent, close relative, or a very good friend. They are putting their credit on the line for you.

- Responsibilities: Both you and your co-signer are equally responsible for the debt. Any missed payments will negatively affect both of your credit scores.

- Benefits: A co-signer can not only help you get approved but also potentially secure a lower interest rate than you’d get on your own. It’s an excellent way to start building your own credit history.

3. Start Small: Focus on a More Affordable Vehicle

While a brand-new SUV might be your dream, a more modest, reliable used car is a much more realistic goal when you have no credit and no money down. Lenders are more comfortable taking a risk on a smaller loan amount.

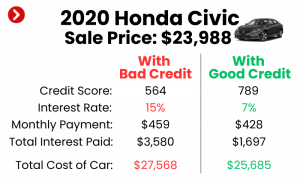

- Look for Older, Reliable Models: Research cars known for their longevity and low maintenance costs. Think Honda Civics, Toyota Corollas, or older Ford F-150s.

- Reduce the Loan Amount: A lower purchase price means a smaller loan, which translates to lower monthly payments and less risk for the lender. This strategy makes "no money down" a much easier pill for lenders to swallow.

4. Build Some Credit First: Even a Little Bit Helps

While the goal is "no credit," even a few months of positive credit activity can make a significant difference. It shifts you from being a complete unknown to having at least a minimal financial footprint.

- Secured Credit Card: This type of card requires a cash deposit, which acts as your credit limit. Use it responsibly for small purchases and pay it off in full every month.

- Credit Builder Loan: Offered by some credit unions and community banks, these loans involve you making payments into a savings account before receiving the funds. It’s a structured way to demonstrate payment reliability.

- Become an Authorized User: If a trusted family member has a credit card with a long history of on-time payments, they might add you as an authorized user. This can help you piggyback on their good credit history, though not all creditors report authorized user activity the same way.

- Internal Link Opportunity: If you’re looking to understand the nuances of building credit from scratch, you might find our guide on Starting Your Credit Journey: A First-Time Buyer’s Guide particularly helpful.

5. Save for a Small Down Payment (Even if It’s Not "No Money Down")

While this article focuses on "no money down," even a small down payment can dramatically improve your chances of approval and secure better loan terms. If you can save even 5-10% of the car’s value, it signals responsibility and reduces the lender’s risk.

- Psychological Impact: A down payment shows the lender you’re committed and have some financial discipline.

- Reduced Loan Amount: Even a few hundred dollars can shave a significant amount off the total interest paid over the life of the loan.

6. Dealership Special Programs

Some dealerships, especially larger chains, occasionally offer programs designed for first-time buyers or those with limited credit. These are often tied to specific manufacturers or promotional periods.

- Manufacturer Incentives: Keep an eye out for incentives from car manufacturers, particularly at the end of a model year or during specific sales events.

- Ask Directly: Don’t be afraid to ask the finance manager if they have any programs for individuals with no credit history or for first-time buyers. Be upfront about your situation.

7. Subprime Lenders

These lenders specialize in providing loans to individuals with less-than-perfect credit or no credit history. They take on higher risk, which means their interest rates will be higher, but they are an option when traditional banks decline.

- Vetting Subprime Lenders: Be cautious and research any subprime lender thoroughly. Look for reviews, check their standing with the Better Business Bureau, and compare offers from multiple sources.

- Understand the Terms: Ensure you fully grasp the interest rate, fees, and any prepayment penalties before signing.

Navigating the Application Process

Once you’ve identified potential strategies, the application process itself requires careful attention.

1. Gather Your Documentation

Lenders will want to verify your identity, income, and residence. Be prepared with:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs, bank statements, or tax returns. Lenders want to see a stable, verifiable income.

- Proof of Residence: Utility bills, lease agreement, or mortgage statements.

- References: Some lenders, especially BHPH, might ask for personal references.

2. Understand Terms & Conditions

This is where many first-time buyers, especially those eager to get a car, make mistakes.

- Interest Rate (APR): This is the cost of borrowing money, expressed as an annual percentage. A higher APR means you pay more over the life of the loan.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but more interest paid overall.

- Total Cost of the Loan: Always calculate the total amount you will pay, including the principal and all interest, over the loan term.

- Fees: Look out for origination fees, documentation fees, or prepayment penalties.

3. Avoiding Predatory Lenders

Unfortunately, the market for "no credit, no money down" loans can attract unscrupulous lenders.

- Red Flags: Be wary of lenders who guarantee approval without checking anything, pressure you into signing immediately, or offer terms that seem too good to be true.

- High Pressure Sales: A legitimate lender will give you time to review the contract and ask questions.

- Unrealistic Terms: Extremely high interest rates (sometimes well above 20-30% APR, depending on state limits) or hidden fees are major warning signs.

- External Resource: Understanding your rights as a consumer is paramount. The Consumer Financial Protection Bureau (CFPB) offers excellent resources on auto loans and consumer protection, helping you identify and avoid predatory practices.

Post-Loan Management: Building Your Financial Future

Securing the loan is just the first step. The real victory lies in managing it responsibly to build a strong financial foundation.

1. Build Credit Responsibility

Every on-time payment you make is a brick in your credit-building wall.

- On-Time Payments: This is the single most important factor in your credit score. Set up automatic payments to avoid missing due dates.

- Don’t Default: Missing payments or having the car repossessed will severely damage your credit for years.

- Keep the Loan Open: Once paid off, the positive payment history remains on your credit report, contributing to your credit length.

2. Refinancing Options

After 6-12 months of consistent, on-time payments, your credit score should start to improve. This opens up the possibility of refinancing.

- Lower Interest Rate: With a better credit score, you can apply for a new loan with a lower interest rate, saving you a significant amount of money over the remaining loan term.

- Improved Terms: You might also be able to adjust the loan term to better suit your financial situation.

Common Mistakes to Avoid When Seeking a Car Loan No Credit No Money Down

Based on my experience counseling numerous first-time buyers, here are some common pitfalls:

- Ignoring the Total Cost: Focusing only on the monthly payment without considering the total amount paid over the loan’s life. A lower monthly payment over a very long term can mean significantly more interest.

- Accepting the First Offer: Never take the first loan offer you receive. Shop around, compare terms from multiple lenders, and use competitive offers to negotiate.

- Not Understanding the Contract: Signing a contract without reading every word and understanding all the terms, fees, and conditions. If you don’t understand something, ask for clarification.

- Overspending: Getting approved for a certain amount doesn’t mean you should spend it all. Stick to a budget that comfortably fits your income.

- Failing to Budget for Ownership Costs: Beyond the loan payment, remember to budget for insurance, gas, maintenance, and potential repairs. These can add hundreds of dollars to your monthly expenses.

Pro Tips from Us: Your Experts on the Road Ahead

As expert bloggers and professional SEO content writers, our goal is to provide real, actionable value. Here are some final pro tips:

- Be Patient and Persistent: This isn’t a quick process. It takes time to research, apply, and potentially build some initial credit. Don’t get discouraged.

- Be Honest with Lenders: Transparency about your financial situation is crucial. Lenders appreciate honesty and are more likely to work with you if you’re upfront.

- Leverage Relationships: If you bank at a local credit union or community bank where you have a checking account, start there. Your existing relationship might give you an edge.

- Consider a Pre-Approval: Some lenders offer pre-approval processes that don’t impact your credit score significantly (soft inquiry). This helps you understand what you qualify for before stepping onto a dealership lot.

- Don’t Go Alone: If you’re unsure, bring a trusted friend or family member with financial literacy to review contracts and offers with you. Two sets of eyes are better than one.

Conclusion: Your Journey to Car Ownership Starts Here

Securing a car loan with no credit and no money down is undoubtedly a challenge, but it is far from an impossible dream. By understanding the lending landscape, exploring alternative financing avenues, and meticulously preparing your application, you can significantly increase your chances of success.

Remember, this isn’t just about getting a car; it’s about making a responsible financial decision that will serve you well for years to come. Use this opportunity to not only gain transportation but also to establish and build a strong credit history for your future. Start your journey today with knowledge, caution, and a clear vision, and soon you could be driving towards new opportunities.