Driving Dreams: Your Ultimate Guide to Securing an Educators Car Loan

Driving Dreams: Your Ultimate Guide to Securing an Educators Car Loan Carloan.Guidemechanic.com

As an educator, you dedicate your life to shaping the future. From early mornings to late nights, you invest countless hours and immense passion into your students. Yet, despite your invaluable contributions, the financial realities can sometimes be challenging, especially when it comes to significant purchases like a new vehicle. This is where the concept of an Educators Car Loan becomes a beacon of opportunity.

Imagine a financial product designed specifically with your unique professional journey in mind. An educator auto financing solution that acknowledges your stable employment, even if your income doesn’t always reflect your monumental impact. This comprehensive guide will illuminate every aspect of securing a car loan as a teacher, administrator, or support staff member, helping you navigate the process with confidence and clarity.

Driving Dreams: Your Ultimate Guide to Securing an Educators Car Loan

We’ll delve into the distinct advantages, application nuances, and expert tips to ensure you drive away with the best possible deal. Our goal is to make this complex topic straightforward, empowering you with the knowledge to make informed financial decisions. Let’s unlock the road to your next vehicle, tailored for the heroes in our classrooms.

Why Special Car Loans for Educators? Understanding the "Why"

The idea of a specialized loan might seem niche, but it’s rooted in a deep understanding of the education sector. Educators, from kindergarten teachers to university professors and administrative staff, form the backbone of our communities. Their employment is generally stable, providing a reliable income stream, even if the pay scale might not always match the effort.

Financial institutions, based on my experience, recognize this stability and the vital role educators play. They understand that while a teacher’s salary might not be as high as some other professions, the likelihood of consistent employment and repayment is strong. This understanding paves the way for specific loan programs designed to offer better terms.

These tailored programs are not just a marketing gimmick; they are a genuine effort by some lenders to support the educational community. They aim to bridge the gap between modest incomes and the need for reliable transportation, often providing more favorable conditions than general consumer loans. It’s a way for the financial sector to give back to those who give so much.

What Makes an Educators Car Loan Different? Unpacking the Benefits

When you hear about special car loans for teachers, you might wonder what truly sets them apart. These aren’t just standard loans with a different label. They often come bundled with distinct advantages designed to benefit the educational community.

Lower Interest Rates (APR)

One of the most significant benefits of teacher car finance programs is the potential for lower interest rates. Lenders offering these programs often provide rates that are a notch below what a general borrower with a similar credit profile might receive. This is a direct result of recognizing the stable employment and dedication of educators.

Even a slight reduction in the Annual Percentage Rate (APR) can translate into substantial savings over the life of your loan. Over several years, these savings can add up to hundreds or even thousands of dollars, making your vehicle purchase more affordable in the long run. It’s a tangible way to acknowledge your profession.

Flexible Repayment Terms

Educators often experience unique pay cycles, especially those on a 9- or 10-month contract who might spread their pay over 12 months, or those who receive lump sums. Some educator auto financing options offer flexible repayment schedules that can align better with these specific income patterns. This could mean options for deferred payments during summer breaks or adjusted monthly due dates.

Pro tips from us: Always inquire about the flexibility of repayment terms. A loan that seamlessly integrates with your personal finance calendar can significantly reduce stress and improve your overall financial management. Don’t assume a standard monthly payment is your only option.

Relaxed Credit Requirements

While a good credit score always helps, some specialized car loan benefits for educators might feature slightly more lenient credit requirements. This doesn’t mean credit checks are skipped entirely, but lenders might be more understanding of past credit challenges or limited credit history, especially if you have a strong employment record as an educator.

They might weigh factors like your job stability and the nature of your profession more heavily than a traditional lender. This can be a huge advantage for newer educators or those who are still building their credit profile, opening doors to car ownership that might otherwise be closed.

Special Perks and Discounts

Beyond the core loan terms, some programs for educator car loans might include additional perks. These could range from waived application fees, reduced processing charges, or even partnerships with car dealerships offering specific educator discounts on vehicle purchases. These added benefits can sweeten the deal further.

It’s always worth asking about any bundled services or additional savings that might be available. These extra incentives are part of the holistic approach some financial institutions take to support the teaching community.

Who Qualifies for an Educators Car Loan? Defining Eligibility

Understanding who is eligible for these specialized loans is crucial. While the term "educator" is broad, most programs aim to cover a wide range of professionals within the educational system.

Broad Definition of "Educator"

Generally, qualifying individuals include:

- Teachers: From pre-kindergarten to university level, including substitute teachers.

- Administrators: Principals, assistant principals, deans, superintendents.

- Support Staff: Counselors, librarians, teaching assistants, school nurses, bus drivers, cafeteria staff, and administrative assistants working in schools or educational institutions.

- Retired Educators: Some programs extend benefits to those who have dedicated their careers to education.

The key is typically proof of employment within an accredited educational institution. This ensures the benefits are directed to those actively contributing to the education sector.

Proof of Employment

Lenders will require verification of your employment status. This usually involves:

- Recent pay stubs.

- An official employment letter from your school or district.

- Your educator certification or license.

They want to confirm your current role and your consistent income, which is a primary factor in loan approval. This documentation helps them assess your financial stability.

Other General Requirements

Like any loan, you’ll also need to meet standard qualifications:

- Age: You must be at least 18 years old (or 19 in some states).

- Residency: Proof of U.S. residency is typically required.

- Income: While flexible, you still need to demonstrate a steady income sufficient to cover the loan payments, in addition to your other financial obligations.

- Credit History: Even with relaxed requirements, a reasonable credit history will always improve your chances of securing the best possible terms.

The Application Process: Your Step-by-Step Guide to How to Get a Car Loan as a Teacher

Securing an educators car loan doesn’t have to be daunting. By following a structured approach, you can navigate the process efficiently and confidently.

Step 1: Assess Your Needs and Budget

Before you even look at cars, define your needs. What kind of vehicle suits your lifestyle and daily commute? More importantly, determine what you can genuinely afford. Consider not just the monthly loan payment, but also insurance, fuel, maintenance, and potential parking costs.

Based on my experience, many educators overlook these ancillary costs, leading to financial strain later. Create a realistic budget that accounts for all vehicle-related expenses.

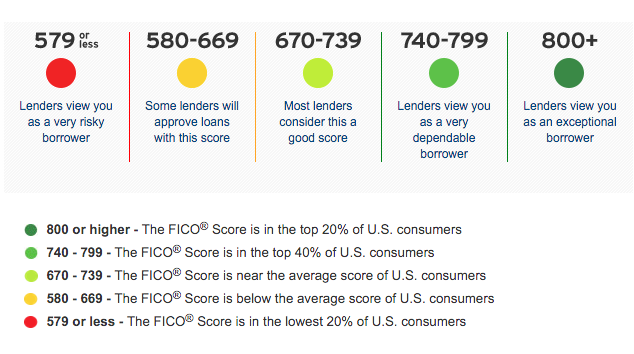

Step 2: Check Your Credit Score

Your credit score is a crucial factor in determining the interest rate you’ll receive. Obtain a free copy of your credit report from one of the three major credit bureaus (Equifax, Experian, TransUnion). Review it for any errors and understand your current standing.

For a deeper dive into improving your credit score, check out our guide on . A higher score will almost always lead to better loan terms.

Step 3: Gather Necessary Documents

Being prepared saves time and reduces stress. Have the following documents ready before you apply:

- Government-issued photo ID (driver’s license).

- Proof of income (recent pay stubs, employment contract).

- Proof of employment as an educator (letter from school, teaching certificate).

- Proof of residency (utility bill, lease agreement).

- Social Security Number.

- Information about your current debts and assets.

Having these on hand will streamline the application process considerably.

Step 4: Research Lenders Specializing in Educator Loans

Don’t settle for the first offer you find. Actively seek out financial institutions that specifically advertise special car loans for teachers or educator auto financing. These often include:

- Credit Unions: Many credit unions have strong ties to local communities and often offer excellent rates and personalized service, sometimes with specific programs for educators.

- Banks: Some larger banks have dedicated programs or preferred rates for certain professional groups, including teachers.

- Online Lenders: A growing number of online platforms specialize in matching borrowers with specific loan products, and some cater to educators.

Common mistakes to avoid are applying to too many lenders at once, which can slightly ding your credit, or only checking with your primary bank without exploring other options.

Step 5: Compare Offers and Apply

Once you’ve identified potential lenders, get pre-approved for a loan. Pre-approval gives you a clear understanding of the loan amount, interest rate, and terms you qualify for, allowing you to shop for a car with confidence. Compare these offers carefully, looking beyond just the monthly payment.

When you’re ready, submit your formal application. Be honest and thorough with all information provided.

Step 6: Understand the Terms and Conditions

Before signing anything, meticulously read and understand the entire loan agreement. Pay close attention to:

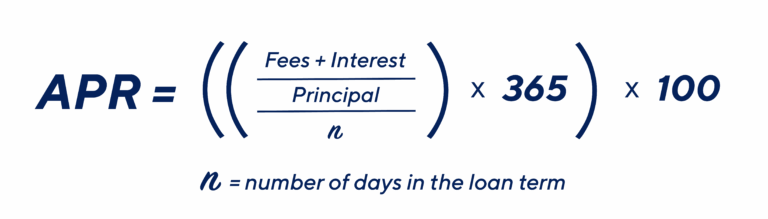

- The APR: The true cost of borrowing.

- Loan Term: How long you have to repay the loan.

- Fees: Are there any origination fees, application fees, or prepayment penalties?

- Late Payment Penalties: What happens if you miss a payment?

If anything is unclear, ask for clarification. It’s your right to understand every clause.

Key Factors to Consider When Choosing Your Loan: Beyond the Basics

Selecting the right educator car loan involves more than just finding the lowest interest rate. A holistic approach ensures you make a financially sound decision.

Interest Rate (APR) vs. Total Cost

While a low APR is attractive, always consider the total cost of the loan over its entire term. A longer loan term might offer lower monthly payments but could result in paying significantly more in interest over time. Balance affordability with the overall expense.

Based on my experience, many educators focus solely on the monthly payment. Calculate the total amount you will pay back, including all interest, to get the full picture.

Loan Term: Short vs. Long

- Shorter Terms (e.g., 36-48 months): Higher monthly payments, but you pay less interest overall and own the car sooner.

- Longer Terms (e.g., 60-84 months): Lower monthly payments, but you pay more interest over time, and the car’s value depreciates faster than you pay it off (potentially leading to negative equity).

Choose a term that balances your budget with your long-term financial goals.

Fees and Penalties

Scrutinize the fine print for any hidden fees. Common ones include:

- Origination Fees: A charge for processing the loan.

- Prepayment Penalties: Some lenders charge a fee if you pay off your loan early. While less common now, it’s worth checking.

- Late Payment Fees: Standard penalties for missed or late payments.

Transparency regarding fees is a hallmark of a reputable lender.

Down Payment Considerations

Making a down payment, even a small one, offers several advantages:

- Reduces Loan Amount: You borrow less, meaning less interest paid.

- Lower Monthly Payments: Makes the loan more affordable.

- Builds Equity Faster: You start with some ownership in the vehicle.

- Better Loan Terms: Lenders often view borrowers who make down payments as less risky.

Even 5-10% down can make a significant difference in your loan terms and overall cost.

Lender Reputation and Customer Service

Choose a lender with a strong reputation for ethical practices and excellent customer service. Read reviews, check their ratings with consumer protection agencies, and ensure they are responsive to inquiries. You want a financial partner you can trust throughout the life of your loan.

A trusted external source like the Consumer Financial Protection Bureau (CFPB) offers excellent resources on understanding car loans and your rights as a borrower. (External Link: https://www.consumerfinance.gov/consumer-tools/auto-loans/)

Beyond the Loan: Maximizing Your Educator Benefits

Securing a great educators car loan is just one piece of the puzzle. There are other avenues where your profession can yield additional savings.

Dealer Discounts and Programs

Many car manufacturers and dealerships offer specific discounts or incentive programs for educators. These can include:

- Cash Back Offers: A direct rebate on the purchase price.

- Reduced Pricing: Special pricing tiers not available to the general public.

- Preferred Financing Rates: Even if you don’t use their direct financing, they might match or beat competitor rates due to your profession.

Always ask if they have any programs for teachers or educators before negotiating the price.

Car Insurance Discounts

Don’t forget to inquire about auto insurance discounts. Many insurance providers recognize educators as a low-risk group and offer special rates or discounts. It’s always worth comparing quotes from multiple providers and specifically mentioning your profession.

These savings, combined with a favorable car loan, can significantly reduce your overall cost of vehicle ownership.

Vehicle Choice and Maintenance

While not directly a loan benefit, choosing a reliable, fuel-efficient vehicle can save you money in the long run. Lower fuel costs, reduced maintenance expenses, and higher resale value contribute to your financial well-being. Proactive maintenance, like regular oil changes and tire rotations, will extend your car’s life and prevent costly repairs.

To help manage your finances as an educator, explore our article on .

Common Misconceptions and Smart Financial Practices

Navigating the world of car loans can be tricky. Let’s debunk some myths and highlight smart practices.

Misconception 1: "All educator loans are the same."

This is simply not true. Just like any financial product, educators car loan programs vary significantly between lenders. Some might offer slightly better rates, others more flexible terms, and some might include additional perks. It’s crucial to compare multiple offers to find the best fit for your situation.

Misconception 2: "I don’t need good credit if I’m an educator."

While some programs are more lenient, having good credit will always give you access to the best possible rates and terms. Lenders still use your credit score to assess risk, and a strong score signals reliability. Focus on maintaining a healthy credit profile.

Smart Financial Practice: Build an Emergency Fund

Beyond your car loan, building an emergency fund is paramount. Unexpected car repairs, medical emergencies, or job changes can derail your finances. Having 3-6 months of living expenses saved can provide a vital safety net, preventing you from defaulting on your car loan or accumulating high-interest debt.

Smart Financial Practice: Review Your Budget Regularly

Life changes, and so should your budget. Regularly review your income and expenses to ensure your car payments remain affordable. This proactive approach helps you stay on track and make adjustments before financial difficulties arise.

Conclusion: Driving Forward with Confidence

Securing an Educators Car Loan is more than just obtaining financing; it’s about recognizing and rewarding the invaluable contributions you make to society. These specialized programs are designed to offer financial advantages that acknowledge your dedication and stable employment. By understanding the unique benefits, navigating the application process effectively, and applying smart financial practices, you can confidently drive toward your next vehicle.

From lower interest rates and flexible terms to potential discounts and a streamlined application, the path to vehicle ownership can be smoother for educators. Remember to do your research, compare offers, and ask the right questions. Your commitment to education deserves a financial partner who understands and supports your journey.

Take the wheel of your financial future. Explore the options for teacher car finance today, and discover how your profession can open doors to better deals and a more comfortable commute. You’ve earned it.