Driving Dreams: Your Ultimate Guide to Securing Car Loans With No Credit History

Driving Dreams: Your Ultimate Guide to Securing Car Loans With No Credit History Carloan.Guidemechanic.com

Embarking on the journey to purchase your first car is an exciting milestone, a symbol of newfound freedom and independence. However, for many aspiring car owners, this excitement can quickly turn into apprehension when confronted with a common hurdle: a lack of credit history. The phrase "no credit" often feels like a brick wall, making you question how you can ever secure a car loan for those with no credit.

But here’s the good news: having no credit doesn’t mean you’re out of options. In fact, countless individuals successfully navigate this very path every year. This comprehensive guide is designed to empower you, providing an in-depth roadmap to understanding, applying for, and ultimately securing an auto loan even without an established credit score. We’ll delve into the nuances of buying a car with no credit, explore viable financing avenues, and equip you with the knowledge to make informed decisions.

Driving Dreams: Your Ultimate Guide to Securing Car Loans With No Credit History

Navigating the No-Credit Landscape: Why It’s a Challenge (and How to Overcome It)

When it comes to lending money, financial institutions operate on a principle of trust and predictability. They need to assess the risk involved in loaning funds to an applicant. This assessment largely relies on a borrower’s credit history, which provides a detailed record of their past financial behavior.

Lenders use this history to predict how likely you are to repay a new loan. Without any credit history, you’re essentially an unknown entity. This doesn’t mean you’re untrustworthy; it simply means there’s no data for them to analyze, making you appear as a higher risk. This is the primary reason why securing a no credit car loan can be challenging.

However, recognizing this challenge is the first step towards overcoming it. By understanding the lender’s perspective, you can proactively address their concerns and present yourself as a reliable borrower, even without a lengthy credit file. The key is to demonstrate your financial responsibility through other means.

Understanding Your Starting Point: What "No Credit" Truly Means

Before we dive into solutions, let’s clarify what "no credit" actually signifies. It’s crucial to distinguish between "no credit" and "bad credit."

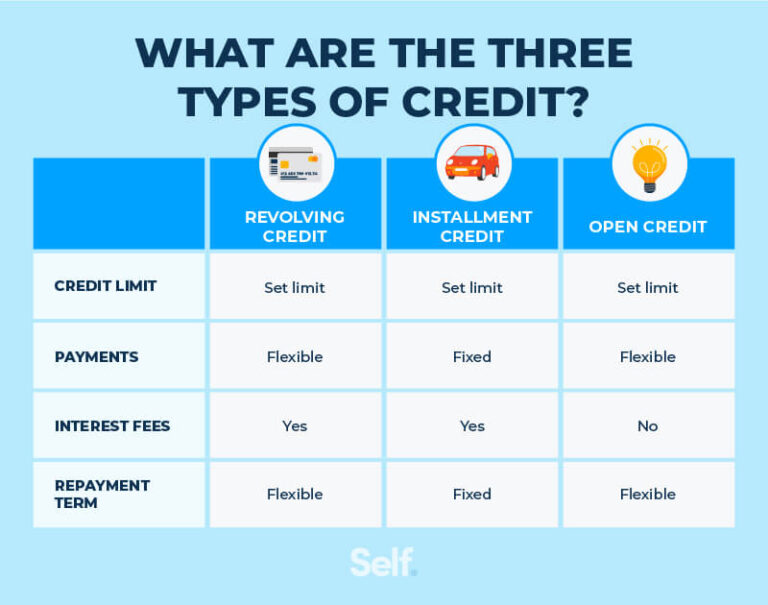

- No Credit: This means you haven’t yet used credit products like credit cards, mortgages, or previous loans that report to credit bureaus. As a result, you don’t have a FICO score or any credit file for lenders to review. This is common for young adults, recent immigrants, or anyone who has always paid cash for everything.

- Bad Credit: This refers to having a credit history, but one that is marred by late payments, defaults, bankruptcies, or high debt utilization. Lenders see this as a history of not managing credit responsibly, which can be even more difficult to overcome than having no credit at all.

For someone with no credit, the task isn’t about repairing past mistakes but rather establishing a positive financial footprint for the very first time. This is a journey that an auto loan can effectively kickstart, helping you build a solid foundation for future financial endeavors.

Essential Steps Before You Apply: Laying the Groundwork for Approval

Based on my experience, thorough preparation is paramount when seeking car financing with no credit. Rushing into applications without understanding your financial standing or the process itself can lead to rejections and frustration. Here are the crucial steps to take before you even set foot in a dealership or fill out an online form.

1. Determine Your Budget: What Can You Truly Afford?

This isn’t just about the monthly car payment; it’s about the total cost of car ownership. Many first-time buyers overlook the additional expenses.

- Monthly Payment: Be realistic about what fits comfortably into your budget alongside all other living expenses.

- Insurance: Car insurance can be surprisingly expensive, especially for new drivers or those with no credit history. Get quotes before you buy.

- Fuel Costs: Factor in your daily commute and weekend trips.

- Maintenance & Repairs: Even new cars require regular servicing. Used cars might need more frequent attention.

- Registration & Taxes: These upfront costs can add significantly to your initial outlay.

Pro tips from us: Create a detailed monthly budget. List all your income sources and all your fixed and variable expenses. This will give you a clear picture of how much wiggle room you have for a car payment and related costs. Don’t stretch yourself too thin; financial stability will be a key factor for lenders.

2. Save a Substantial Down Payment

A down payment is one of your most powerful tools when you have no credit. It demonstrates your financial commitment and reduces the amount you need to borrow, which in turn lowers the lender’s risk.

- Reduce Risk for Lenders: A larger down payment means less money loaned, making the deal more attractive to lenders who are hesitant due to your lack of credit history.

- Lower Monthly Payments: Borrowing less money directly translates to smaller monthly payments.

- Better Interest Rates: Lenders may offer more favorable interest rates if you put down a significant amount, seeing you as a less risky borrower.

- Avoid Negative Equity: A good down payment helps prevent you from owing more than the car is worth, especially in the early years of ownership when depreciation is highest.

Aim for at least 10-20% of the car’s purchase price. The more you can put down, the better your chances of approval and securing more favorable terms for your auto loan with no credit history.

3. Gather All Necessary Documentation

Lenders will need to verify your identity, income, and residence. Having these documents organized and ready will streamline the application process.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms, or tax returns (if self-employed).

- Proof of Residence: Utility bills (electricity, gas, water) with your name and address, or a lease agreement.

- Identification: Driver’s license or state-issued ID.

- Bank Statements: Lenders might request recent bank statements to verify your financial stability and cash flow.

Presenting a complete and organized package shows lenders you are responsible and serious about the loan.

4. Know Your "Credit Status" (Even if it’s "None")

While you might believe you have no credit, it’s always wise to double-check. There’s a slight chance you might have an old utility bill or a student loan that has started building a file.

- Request Credit Reports: You can get free copies of your credit reports from AnnualCreditReport.com. Review them to confirm there’s truly no history or to identify any potential errors.

- Understand What Lenders See: If there’s no report, lenders will rely solely on the other information you provide. If there’s a thin file, they might use alternative data.

This step ensures you’re fully aware of your starting point and can address any discrepancies before they become an issue during the loan application.

Exploring Your Car Loan Options with No Credit History

Now that you’re well-prepared, let’s explore the specific avenues available for first-time car buyers with no credit. Each option comes with its own set of advantages and considerations.

1. Dealership Financing: Special Finance Departments

Many dealerships, especially larger ones, have "special finance" departments designed to help customers with challenging credit situations, including those with no credit. They work with a network of lenders who specialize in subprime or no-credit loans.

- Convenience: You can apply for financing directly at the dealership, often completing the entire purchase in one location.

- Multiple Lenders: Dealerships submit your application to several lenders, increasing your chances of finding an approval.

- Higher Interest Rates: Be prepared for higher interest rates than someone with excellent credit. This is the trade-off for the increased risk lenders are taking.

- "Buy Here, Pay Here" (BHPH) Dealerships: These dealerships act as both the seller and the lender. While they are often a last resort for those with no credit or very bad credit, they come with significant caveats.

- Pros: High approval rates, even with no credit.

- Cons: Extremely high interest rates, limited car selection (often older, higher mileage vehicles), and they may not report payments to all three credit bureaus, limiting your ability to build credit.

- Pro Tip: Based on my experience, approach BHPH dealerships with extreme caution. Scrutinize every detail of the contract and be aware of the total cost. This option should generally be considered only if all other avenues have been exhausted.

2. Credit Unions: A Community-Focused Alternative

Credit unions are non-profit financial cooperatives owned by their members. They often have more flexible lending standards than traditional banks, making them an excellent option for financing options no credit.

- Member-Centric Approach: Credit unions prioritize their members’ financial well-being. They might be more willing to work with individuals who have no credit history if they can demonstrate stability.

- Potentially Better Rates: Due to their non-profit nature, credit unions often offer more competitive interest rates and fees compared to traditional banks.

- Relationship Building: Establishing a relationship with a credit union by opening a checking or savings account first can sometimes help your loan application.

- Membership Requirements: You’ll need to meet specific criteria to join a credit union, such as living in a certain area, working for a particular employer, or being part of a specific organization.

It’s highly recommended to explore credit unions in your area. Their personalized approach can make a significant difference for a first-time borrower.

3. Co-Signer Loans: Leveraging Someone Else’s Credit

If you have a trusted friend or family member with good credit, asking them to co-sign your loan can dramatically improve your chances of approval and help you secure a better interest rate.

- How it Works: A co-signer legally agrees to take on the responsibility of repaying the loan if you fail to do so. Their good credit history mitigates the risk for the lender.

- Benefits: Increased approval odds, lower interest rates, and an opportunity for you to build your own credit history.

- Risks for Co-Signer: If you miss payments, it negatively impacts their credit score. If you default, they are legally obligated to repay the entire loan. This can strain relationships.

- Choosing a Co-Signer: Select someone who understands the responsibility and whom you trust implicitly. Ensure you communicate openly about your financial plan and commitment to on-time payments.

This is a powerful option, but it requires careful consideration and a strong foundation of trust.

4. Online Lenders Specializing in No/Low Credit

The digital age has brought forth a number of online lenders who specialize in working with borrowers who have limited or no credit history. These platforms often use alternative data points to assess risk.

- Accessibility: Easy to apply online from anywhere, often with quick approval decisions.

- Specialized Algorithms: They might look beyond traditional credit scores, considering factors like employment history, education, and banking activity.

- Variety of Options: Some platforms act as marketplaces, connecting you with multiple lenders.

- Vigilance is Key: Research the lender’s reputation, read reviews, and be wary of any promises that seem too good to be true. Ensure they are legitimate and transparent about their terms and fees.

Always compare offers from different online lenders to find the most favorable terms for your car loan for those with no credit.

The Application Process: What to Expect and How to Maximize Your Chances

Once you’ve identified potential lenders, the application process itself requires strategy and transparency.

1. Be Honest and Transparent About Your Financial Situation

Don’t try to hide any financial details or exaggerate your income. Lenders will verify the information you provide.

- Build Trust: Honesty fosters trust, which is crucial when you’re already starting with no credit history.

- Avoid Delays: Inaccuracies will lead to delays or outright rejections.

2. Show Proof of Stability: Employment and Residence

Lenders are looking for signs of stability. A consistent job history and a stable residence indicate a reliable borrower.

- Long-Term Employment: If you’ve been at the same job for a significant period (e.g., 6 months to a year or more), highlight this.

- Stable Residence: Living at the same address for a while also signals stability.

- Alternative Income: If you have alternative income sources (e.g., side gigs), be prepared to provide documentation.

3. Keep Applications Limited

Each time you apply for a loan, a "hard inquiry" is typically placed on your credit report. While you might not have a credit score, too many inquiries in a short period can look like you’re desperate for credit, which future lenders might view negatively if a file eventually forms.

- Targeted Approach: Focus on 2-3 promising lenders rather than applying everywhere.

- Pre-Qualification: If available, opt for pre-qualification processes first. These often use a "soft inquiry" which doesn’t affect your credit.

4. Negotiating Terms: Don’t Just Accept the First Offer

Even with no credit, there’s often room for negotiation, especially on the interest rate and loan term.

- Focus on APR: The Annual Percentage Rate (APR) is the true cost of borrowing, including interest and fees. Compare APRs, not just interest rates.

- Loan Term: A shorter loan term means higher monthly payments but less interest paid overall. A longer term lowers monthly payments but increases total interest. Balance what you can afford with minimizing total cost.

- Total Cost: Always calculate the total cost of the loan (principal + interest) over the entire term.

Don’t be afraid to walk away if the terms are unfavorable. There are usually other options available.

Building Credit While You Drive: The Long-Term Benefits of a Car Loan

Securing a car loan with no credit is not just about getting a car; it’s a strategic move to establish and build your credit history. This is where the long-term value truly shines.

- On-Time Payments: The single most important factor in building a good credit score is making all your payments on time, every time. A car loan, with its fixed monthly payments, provides an excellent opportunity to demonstrate this financial discipline.

- Credit Mix: As you build credit, having a mix of different types of credit (e.g., an installment loan like a car loan, and later, revolving credit like a credit card) can positively impact your score.

- Credit Age: The longer your credit accounts are open and in good standing, the better. A car loan can be the start of a long and positive credit history.

Common mistakes to avoid are missing payments, paying late, or defaulting on the loan. These actions will severely damage your newly forming credit history and make it much harder to obtain credit in the future. Treat your car loan as a serious financial commitment and an investment in your future creditworthiness.

Common Pitfalls to Avoid When Getting a No-Credit Car Loan

While opportunities exist, the no-credit landscape can also be fraught with potential traps. Being aware of these common pitfalls will help you make smarter decisions.

1. Falling for Exorbitant Interest Rates

Lenders take a higher risk with no-credit borrowers, which often translates to higher interest rates. However, some lenders may try to charge rates that are predatory.

- Research Average Rates: Understand what a "high but fair" rate is versus an "exorbitantly high" one. For no-credit loans, rates can be significantly higher than prime rates, but there are limits.

- Compare Offers: Don’t jump at the first approval. Shop around and compare APRs from multiple lenders.

2. Agreeing to Overly Long Loan Terms

A longer loan term (e.g., 72 or 84 months) might offer lower monthly payments, but it has significant drawbacks.

- Increased Total Interest: You’ll pay much more in interest over the life of the loan.

- Negative Equity: Cars depreciate rapidly. With a long loan term, you’re likely to owe more than the car is worth for a significant portion of the loan. This means if the car is totaled or you need to sell it, you could still owe money on a vehicle you no longer own.

- Older Car, Newer Loan: You could still be paying for a car that’s 6-7 years old, while the car itself might be nearing the end of its reliable life.

3. Unnecessary "Add-Ons" and Extras

Dealerships often try to sell extended warranties, GAP insurance (though sometimes beneficial), rustproofing, paint protection, and other services.

- Question Everything: Ask if these are truly necessary and how much they add to your total loan amount and monthly payment.

- Research Value: Many add-ons are overpriced or offer little real value.

- GAP Insurance: This can be useful if you have a small down payment, as it covers the difference between what you owe and what your insurance pays if your car is totaled. However, don’t just accept it without understanding the cost.

4. Not Reading the Fine Print

Every loan contract has terms and conditions. It’s easy to overlook crucial details when you’re excited about getting a car.

- Understand All Clauses: Read every section carefully. Ask questions about anything you don’t understand, especially regarding penalties for late payments, prepayment penalties, or repossession clauses.

- Don’t Rush: Take your time. Don’t feel pressured to sign immediately.

Pro Tips for First-Time Car Buyers with No Credit

To wrap up, here are some actionable pro tips that can significantly smooth your path to securing a first-time car buyer no credit loan.

- Start Small and Affordable: Your first car doesn’t need to be your dream car. Focus on a reliable, affordable vehicle that meets your basic needs. This makes the loan more manageable and helps you build credit without excessive financial strain.

- Consider a Used Car: Used cars are generally much cheaper than new ones, making them a more accessible option for someone with no credit. They also depreciate slower after the initial drop, helping you avoid negative equity.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, or the terms are too burdensome, be prepared to walk away. There will always be other cars and other lenders. Patience can save you a lot of money and stress.

- Get Pre-Approved (If Possible): Some lenders offer pre-approval processes that give you an idea of how much you can borrow and at what rate, without committing to the loan. This gives you negotiating power at the dealership.

- Focus on Building a Relationship: If you have a good experience with a credit union or a specific lender, consider maintaining that relationship. Future loans or financial products might be easier to secure.

- Use a Secured Credit Card to Build Credit Simultaneously: While getting a car loan, consider opening a secured credit card. You put down a deposit (which acts as your credit limit), and responsible use helps build your credit profile alongside your car payments. (You can learn more about building credit effectively in our article: ).

Remember, this first auto loan is not just about transportation; it’s a stepping stone to a stronger financial future.

Conclusion: Your Road to Car Ownership and Credit Building Starts Now

Securing a car loan for those with no credit might seem like a daunting task, but as we’ve explored, it’s an entirely achievable goal with the right approach and preparation. By understanding the lending landscape, diligently preparing your finances, exploring diverse financing options, and navigating the application process strategically, you can successfully drive off the lot in your new vehicle.

This journey is not just about acquiring a car; it’s about laying the foundation for a robust financial future. Your consistent, on-time payments on this auto loan will be instrumental in building a positive credit history, opening doors to better financial opportunities down the road.

Don’t let the absence of a credit score deter you. With this comprehensive guide, you are now equipped with the knowledge and strategies to overcome the challenge. Start planning, researching, and preparing today. Your path to car ownership and credit empowerment begins now.