Driving Forward: Securing a Car Loan Right After Chapter 7 Bankruptcy

Driving Forward: Securing a Car Loan Right After Chapter 7 Bankruptcy Carloan.Guidemechanic.com

Navigating life after Chapter 7 bankruptcy can feel like walking through a dense fog, especially when a crucial need like reliable transportation arises. Many people believe that getting a car loan right after Chapter 7 is an impossible feat, a financial door slammed shut. However, based on my extensive experience in the financial landscape and working with countless individuals rebuilding their credit, I can confidently tell you that this isn’t necessarily true. While challenging, securing an auto loan post-bankruptcy is absolutely achievable with the right strategy, patience, and realistic expectations.

This comprehensive guide is designed to empower you with the knowledge and actionable steps needed to drive away in a new (or new-to-you) vehicle, even with a recent Chapter 7 discharge on your credit report. We’ll dive deep into what lenders look for, how to prepare, where to find financing, and most importantly, how to use this opportunity to rebuild your financial future.

Driving Forward: Securing a Car Loan Right After Chapter 7 Bankruptcy

Understanding Chapter 7 and Its Immediate Impact

Chapter 7 bankruptcy, often referred to as "liquidation bankruptcy," provides a fresh start by discharging most unsecured debts. This can include credit card debt, medical bills, and personal loans. While it offers immense relief, it also leaves a significant mark on your credit report, typically remaining for ten years from the filing date.

The immediate aftermath of a Chapter 7 discharge often sees a substantial drop in your credit score. Lenders view a recent bankruptcy as a high-risk indicator because it signals a past inability to repay debts. This doesn’t mean you’re unlendable; it means lenders will scrutinize your current financial situation much more closely. Your creditworthiness takes a hit, but it’s not a permanent sentence.

Is Getting a Car Loan Immediately Possible? Setting Realistic Expectations

The short answer is yes, getting a car loan right after Chapter 7 bankruptcy is possible. Many individuals find themselves approved for auto financing within weeks or months of their discharge. However, "possible" doesn’t mean "easy" or "ideal."

Pro tips from us: The key here is managing expectations. Don’t anticipate prime interest rates or zero-down offers. Your first post-bankruptcy car loan will likely come with a higher interest rate and stricter terms. This is a common part of the rebuilding process. Think of it as an investment in re-establishing your credit profile.

The Waiting Game: How Long Should You Wait?

While immediate approval is possible, strategically waiting can significantly improve your chances and potentially secure better terms.

- Immediately After Discharge (0-6 months): This is the riskiest period for lenders. Your credit file is fresh off bankruptcy, with little new positive payment history established. Approvals are typically from subprime lenders with the highest interest rates.

- A Few Months Post-Discharge (6-12 months): As time passes, your credit report begins to show a "clean slate" from new defaults. If you’ve started rebuilding credit responsibly (more on this soon), lenders will see positive activity. This period offers slightly better prospects than immediately after discharge.

- One Year or More Post-Discharge: This is often the sweet spot. With a year or more of responsible financial behavior post-bankruptcy, you’ll have a stronger case. Lenders prefer to see a sustained period of on-time payments and stability.

Based on my experience, waiting at least 6-12 months post-discharge, if feasible, provides the best balance between immediate need and improving loan terms. However, if a car is essential for work or family, don’t delay your search, just be prepared for the realities of the market.

Key Factors Lenders Consider Post-Bankruptcy

When you apply for a car loan after Chapter 7, lenders aren’t just looking at your bankruptcy filing. They’re assessing your current financial health and your commitment to responsible financial management.

1. Income Stability and Employment History

Lenders want to see a steady, verifiable source of income. This demonstrates your ability to make consistent monthly payments. A long, stable employment history with the same employer is highly favorable.

- What lenders look for: Consistent paychecks, full-time employment, and a history of job stability.

- Common mistakes to avoid are: Frequent job changes or gaps in employment history, which can make lenders wary. If you’ve recently changed jobs, be prepared to explain the circumstances, especially if it was for career advancement.

2. Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to cover new loan payments. Lenders typically prefer a DTI under 40-45%.

- Pro tips from us: After Chapter 7, many of your unsecured debts are discharged, which should theoretically lower your DTI significantly. This is a major advantage you have post-bankruptcy. Focus on keeping any new debt minimal.

3. New Credit History (Post-Discharge)

This is perhaps the most crucial factor for proving your renewed creditworthiness. Lenders want to see how you’ve handled credit since your bankruptcy discharge.

- How to build it: This might involve a secured credit card, a small personal loan from a credit union, or even being added as an authorized user on a trusted family member’s credit card (if they have excellent credit and you make a formal agreement to pay your portion).

- Based on my experience: Consistently making on-time payments on these new credit lines for at least 6-12 months will significantly boost your appeal to auto lenders. It shows you’re committed to financial responsibility.

4. Down Payment

A substantial down payment is one of the most powerful tools you have to secure a car loan after Chapter 7. It reduces the amount you need to borrow, thereby lowering the lender’s risk.

- Benefits: A larger down payment can lead to lower monthly payments, a better interest rate, and a higher chance of approval. It also shows the lender you have "skin in the game" and are financially invested in the purchase.

- Pro tips from us: Aim for at least 10-20% of the vehicle’s price. The more you can put down, the better your position.

5. Co-signer

If you have a trusted friend or family member with excellent credit who is willing to co-sign your loan, this can significantly improve your chances of approval and potentially secure a lower interest rate.

- Considerations: A co-signer takes on equal responsibility for the loan. If you default, their credit will be negatively impacted. Only pursue this option if you are absolutely confident in your ability to make payments.

- Common mistakes to avoid are: Assuming a co-signer is a magic bullet. While helpful, lenders still assess your individual financial situation.

6. Vehicle Choice

The type of vehicle you choose can also impact your loan approval. Lenders are more comfortable financing practical, affordable cars rather than luxury or high-performance models.

- What to look for: A reliable, moderately priced used car (typically 3-5 years old with reasonable mileage) is often the most sensible choice for a post-bankruptcy auto loan. Avoid vehicles that depreciate rapidly or are known for expensive repairs.

- Based on my experience: Lenders may be hesitant to finance an older, high-mileage vehicle because the risk of mechanical breakdown (and thus, non-payment) increases. A sweet spot is often a reliable used car that’s still relatively new.

Steps to Prepare for a Post-Bankruptcy Car Loan

Preparation is paramount when seeking a car loan after Chapter 7. Taking these steps will not only increase your approval chances but also help you secure the best possible terms.

1. Get Your Credit Report & Score (and Understand It)

Even after bankruptcy, it’s vital to know exactly where you stand. Obtain your free credit reports from AnnualCreditReport.com (one from each of the three major bureaus: Experian, Equifax, and TransUnion).

- What to check for: Ensure the bankruptcy discharge is accurately reported. Look for any remaining errors or old accounts that should have been included in the bankruptcy but are still showing as active. Dispute any inaccuracies immediately.

- Pro tips from us: Understanding your credit score (even if it’s low) helps you anticipate what lenders will see and allows you to track your progress as you rebuild.

2. Establish New Credit Responsibly

As mentioned, building new, positive credit history post-discharge is critical.

- Secured Credit Cards: These require a cash deposit, which becomes your credit limit. Use it for small, regular purchases you can pay off in full each month. This demonstrates responsible usage. For more in-depth advice, you might find our article on "The Ultimate Guide to Secured Credit Cards" helpful. (Internal Link 1)

- Small Installment Loans: Some credit unions offer "credit builder" loans. You make payments into a savings account, and once the loan is paid off, you receive the funds. This shows you can handle installment debt.

3. Save for a Down Payment

Start saving as much as you can. As we discussed, a down payment is your best friend in this scenario.

- Strategy: Set a specific savings goal based on the type of car you’re targeting. Even small, consistent contributions add up.

- Based on my experience: Showing a lender you have disciplined savings habits for a down payment can impress them more than you might think, signaling financial maturity.

4. Create a Realistic Budget

Before you even start car shopping, know exactly how much you can comfortably afford each month for a car payment, insurance, fuel, and maintenance.

- Don’t overextend: A common mistake post-bankruptcy is falling into old habits of overspending. Stick to a budget that leaves room for emergencies.

- Pro tips from us: Remember that higher interest rates mean more of your payment goes towards interest initially. Factor this into your budget calculations.

5. Gather Necessary Documents

Being prepared with all required paperwork will streamline the application process.

- Typical documents: Proof of income (pay stubs, tax returns), proof of residence (utility bills), identification, bankruptcy discharge papers, and bank statements.

- Common mistakes to avoid are: Showing up unprepared. Having everything ready demonstrates your seriousness and organization.

Finding the Right Lender

Not all lenders are created equal, especially when you have a recent bankruptcy on your record. Knowing where to look is key.

1. Specialized Lenders (Subprime or Bad Credit Lenders)

These lenders specialize in working with individuals who have less-than-perfect credit. They are often more willing to approve post-bankruptcy applicants.

- Pros: Higher approval rates.

- Cons: Generally higher interest rates and fees.

- Based on my experience: These lenders are often a necessary stepping stone. Use them to get your car, make payments consistently, and then aim to refinance later.

2. Credit Unions

Credit unions are member-owned financial institutions known for their more personalized approach and often more flexible lending criteria than traditional banks.

- Pros: Potentially lower interest rates than subprime lenders, more understanding of individual circumstances.

- Cons: You usually need to be a member to apply for a loan.

- Pro tips from us: If you’re not already a member, consider joining one. Many have open membership requirements.

3. Dealership Financing

Many dealerships have relationships with multiple lenders, including those specializing in bad credit. They can often submit your application to several lenders at once.

- Pros: Convenience, one-stop shopping.

- Cons: May not always offer the absolute best rates, as they might add their own fees.

- Common mistakes to avoid are: Only letting the dealership run your credit through their preferred lenders. It’s always wise to get pre-approved elsewhere first.

4. Online Lenders

A growing number of online lenders specialize in bad credit auto loans. They offer quick pre-approvals and convenient application processes.

- Pros: Fast process, can compare multiple offers easily.

- Cons: Less personal interaction. Always check their reputation.

Avoiding Predatory Lenders

Be extremely cautious of "buy here, pay here" dealerships or lenders that promise guaranteed approval without a credit check. These often come with exorbitant interest rates, hidden fees, and unfavorable terms that can lead you back into a debt cycle.

- Red flags: Pressure tactics, refusal to disclose full terms, very high fees, or requiring you to install GPS trackers or "starter interrupt" devices.

- Pro tips from us: Always read the fine print. If a deal sounds too good to be true, it probably is.

The Application Process: What to Expect

Once you’ve done your homework and found potential lenders, it’s time to apply.

1. Be Honest and Transparent

Don’t try to hide your bankruptcy. Lenders will see it on your credit report. Being upfront about your situation and explaining your plan for financial recovery can actually build trust.

- What to explain: Briefly discuss the circumstances leading to bankruptcy (if comfortable) and, more importantly, what you’ve learned and how you’re managing your finances differently now.

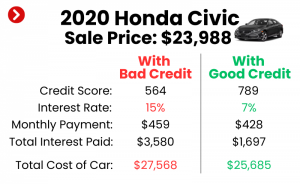

2. Expect Higher Interest Rates

This is a reality of post-bankruptcy financing. Your interest rate will be higher than someone with excellent credit. This reflects the increased risk the lender is taking.

- Average rates: While rates vary wildly, expect to see rates anywhere from 10% to 25% or even higher, depending on your specific credit profile and the market.

- Pro tips from us: Focus on getting approved first, making payments on time, and then strategizing for a refinance later when your credit score improves.

3. Negotiating Terms

Even with a bankruptcy on your record, there’s still room for negotiation.

- Focus on the total cost: Don’t just look at the monthly payment. Consider the total interest paid over the life of the loan.

- Negotiate the down payment, interest rate, and loan term. A shorter loan term means higher monthly payments but less interest paid overall.

- Common mistakes to avoid are: Focusing solely on the monthly payment without considering the total cost of the vehicle and loan.

Rebuilding Your Credit After Car Loan Approval

Getting approved for a car loan is a huge step. Now, it’s time to leverage this opportunity to rebuild your credit even stronger.

1. Making On-Time Payments

This is the most critical component of credit rebuilding. Every single on-time payment reported to the credit bureaus will positively impact your score.

- Strategy: Set up automatic payments or calendar reminders. Do not miss a payment.

- Based on my experience: A consistent 12-24 months of on-time car payments can significantly improve your credit score, often by hundreds of points.

2. Avoiding New Debt

While rebuilding credit, be mindful of taking on additional debt. Overextending yourself can quickly lead back to financial difficulties.

- Focus: Your primary focus should be on your car loan and any other small, secured credit lines you’ve established.

- Pro tips from us: If you’re interested in understanding the nuances of how various financial decisions impact your credit, our article "Understanding Your Credit Score After Bankruptcy" could offer valuable insights. (Internal Link 2)

3. Monitoring Your Credit

Continue to monitor your credit reports regularly (at least annually from all three bureaus) for accuracy and to track your progress.

- Tools: Many credit card companies and banks offer free credit score monitoring services.

4. Refinancing Later

Once you’ve made 12-24 months of on-time payments and your credit score has improved, you may be eligible to refinance your car loan at a lower interest rate.

- Benefits: Refinancing can significantly reduce your monthly payments and the total amount of interest you pay over the life of the loan. This is often the goal after securing that initial post-bankruptcy loan.

Pro Tips for Success in Getting a Car Loan After Chapter 7

- Don’t Settle for the First Offer: Always shop around and compare offers from multiple lenders. This can save you thousands over the life of the loan.

- Consider a Used Car: New cars depreciate rapidly. A reliable used car is a more financially sensible choice post-bankruptcy.

- Be Patient: Rebuilding credit takes time. Don’t get discouraged if the first few months are slow. Consistency is key.

- Educate Yourself: The more you know about the lending process and your own financial standing, the better equipped you’ll be.

- Leverage Technology: Use budgeting apps and financial tools to stay on track with your payments and savings.

- External Resource: For more detailed guidance on managing debt and improving your financial health, the Consumer Financial Protection Bureau (CFPB) offers excellent resources: Consumer Financial Protection Bureau (CFPB). (External Link 1)

Conclusion: Driving Towards a Brighter Financial Future

Getting a car loan right after Chapter 7 bankruptcy is not just a possibility; it’s a powerful opportunity to demonstrate your renewed financial responsibility and actively rebuild your credit. While the journey may start with higher interest rates and more stringent terms, each on-time payment you make is a brick in the foundation of your new, stronger credit profile.

By understanding what lenders look for, diligently preparing your finances, and approaching the process strategically, you can secure the transportation you need and pave the way for a brighter financial future. Remember, bankruptcy is a fresh start, not a permanent roadblock. Take control, stay disciplined, and you’ll be well on your way to driving forward with confidence.