Driving Forward: Your Comprehensive Guide to Bad Credit Car Loans in Spokane, WA

Driving Forward: Your Comprehensive Guide to Bad Credit Car Loans in Spokane, WA Carloan.Guidemechanic.com

Navigating the journey of purchasing a car can be exhilarating, but for many in Spokane, Washington, the path can feel blocked by the roadblock of bad credit. The thought of securing a car loan when your credit score isn’t perfect often brings a wave of anxiety and doubt. You might feel like your options are limited, or worse, non-existent.

But here’s the empowering truth: obtaining a car loan with bad credit in Spokane, WA, is not only possible but can also be a crucial step toward rebuilding your financial future. This isn’t just about getting a set of wheels; it’s about regaining independence, improving your daily life, and strategically repairing your credit score. As expert bloggers and professional SEO content writers, our mission is to provide you with an incredibly detailed, unique, and actionable guide that demystifies the process, empowers your decisions, and ultimately helps you drive away in a vehicle that meets your needs. We’ll show you how to find the right solutions, avoid common pitfalls, and make the most informed choices, all while aiming for Google AdSense approval and top search engine rankings.

Driving Forward: Your Comprehensive Guide to Bad Credit Car Loans in Spokane, WA

Understanding the Landscape: What Exactly is "Bad Credit"?

Before we dive into solutions, let’s clearly define what "bad credit" typically means in the financial world. Your credit score, most commonly the FICO score, is a three-digit number ranging from 300 to 850 that lenders use to assess your creditworthiness. This score is a snapshot of your financial history, including your payment history, amounts owed, length of credit history, new credit, and credit mix.

Based on my experience, a credit score below 620 is generally considered "subprime" or "bad credit." This range usually falls between 300 and 579 (Very Poor) or 580 and 669 (Fair). Lenders view individuals in this range as higher-risk borrowers because their credit history might show late payments, defaults, collections, bankruptcies, or a high debt-to-income ratio. It’s not just a number; it’s a story your financial past tells to potential lenders.

The impact of bad credit on a car loan is significant. Lenders mitigate their increased risk by offering loans with higher interest rates, stricter terms, and sometimes requiring a larger down payment or a co-signer. This isn’t meant to punish you, but rather to offset the perceived risk of you not being able to repay the loan. Understanding this reality upfront is the first step toward navigating the market successfully.

Why a Car is Essential in Spokane, WA

Spokane, a vibrant city in Eastern Washington, presents unique transportation challenges and opportunities. While downtown offers some public transit options, many residents find a personal vehicle indispensable. Commuting to work, accessing healthcare, taking advantage of outdoor recreational activities like skiing at Mount Spokane, or simply running errands across the city’s spread-out neighborhoods often necessitates a reliable car.

Imagine trying to navigate Spokane’s winter weather without your own transportation, or missing out on a job opportunity because you can’t reliably get there. For many, a car isn’t a luxury; it’s a necessity that impacts their quality of life, employment prospects, and overall independence. This makes securing a car loan, even with bad credit, a critical goal for many Spokane residents.

The Reality Check: What to Expect with Bad Credit Car Loans

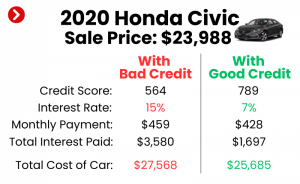

It’s important to approach the bad credit car loan process with realistic expectations. As mentioned, higher interest rates are almost a certainty. While someone with excellent credit might secure a loan with an interest rate below 5%, individuals with bad credit might see rates anywhere from 10% to 25% or even higher, depending on their specific credit profile, the lender, and the vehicle.

Pro tips from us: Don’t let the initial sticker shock deter you. Focus on the long-term goal of obtaining a reliable vehicle and, more importantly, using this loan as a tool to rebuild your credit. Every on-time payment you make will positively impact your credit score, potentially opening doors to better financial opportunities down the road, including refinancing your car loan at a lower rate in the future.

Furthermore, loan terms might be longer, potentially stretching to 60, 72, or even 84 months. While longer terms mean lower monthly payments, they also mean you’ll pay more in interest over the life of the loan. It’s a delicate balance that requires careful consideration of your budget and future financial goals.

Laying the Foundation: Essential Steps Before Applying

Preparation is key when seeking a bad credit car loan. Rushing into applications without understanding your financial standing or market options can lead to frustration and potentially even more damage to your credit score through multiple hard inquiries.

1. Know Your Credit Score and Report Inside Out

Before speaking to any lender, pull your credit report from all three major bureaus (Experian, Equifax, and TransUnion). Websites like AnnualCreditReport.com allow you to get a free report from each bureau once every 12 months. Review these reports meticulously for any errors or inaccuracies.

Common mistakes to avoid are not checking your credit report before applying. Errors, such as accounts that aren’t yours or incorrect late payment notations, can unfairly drag down your score. Disputing and correcting these errors can significantly improve your credit standing, even by a few points, which can make a difference in loan approval and interest rates. Understanding the negative marks also helps you explain your situation to a lender if asked.

2. Create a Realistic Budget

This step is non-negotiable. Beyond the monthly car payment, factor in fuel costs, insurance (which can be higher for newer cars or drivers with a spotty financial history), maintenance, and potential registration fees in Spokane. Use a budget planner to assess how much you can truly afford to pay each month without straining your finances.

A general rule of thumb is that your total car expenses (payment, insurance, fuel) shouldn’t exceed 10-15% of your take-home pay. Be honest with yourself about your financial capacity. Overextending yourself now could lead to missed payments later, undoing any credit-building efforts.

3. Save for a Down Payment

A substantial down payment is one of the most powerful tools you have when applying for a bad credit car loan. It signals to lenders that you’re serious and committed, and it directly reduces the amount you need to borrow. This, in turn, lowers your monthly payments and the total interest you’ll pay over the life of the loan.

Based on my experience, even 10-20% of the vehicle’s price can significantly improve your chances of approval and secure a more favorable interest rate. If you can save more, do it. A larger down payment reduces the lender’s risk and demonstrates your financial responsibility.

4. Gather All Necessary Documentation

Be prepared to provide lenders with a range of documents to verify your identity, income, and residency. This typically includes:

- Government-issued photo ID (driver’s license or state ID)

- Proof of residency (utility bill, lease agreement)

- Proof of income (recent pay stubs, bank statements, tax returns if self-employed)

- Proof of insurance (you’ll need this before driving off the lot)

- References (sometimes required by subprime lenders)

Having these documents organized and ready will streamline the application process and show the lender you are a serious and organized applicant.

Finding Your Match: Lenders Specializing in Bad Credit Car Loans in Spokane, WA

Spokane offers several avenues for individuals with bad credit to secure a car loan. Each type of lender has its own advantages and disadvantages.

1. Dealerships with Special Finance Departments

Many larger car dealerships in Spokane have dedicated "special finance" or "subprime" departments. These departments work with a network of lenders who specialize in loans for individuals with less-than-perfect credit. They act as intermediaries, helping you find a loan that fits your situation.

Pros: Convenience (one-stop shop for car and loan), experience with bad credit applicants, often have relationships with multiple lenders, potentially leading to competitive offers.

Cons: May have higher interest rates or markups on vehicles, could push you towards specific vehicles where they have better financing deals.

2. Local Credit Unions

Credit unions in Spokane, such as Spokane Teachers Credit Union (STCU) or Numerica Credit Union, are often more community-focused and member-centric than traditional banks. They might be more willing to work with individuals who have bad credit, especially if you have an existing relationship with them or can demonstrate a stable income and a clear path to improvement.

Pros: Potentially more flexible terms and lower interest rates than other subprime lenders, personalized service, often prioritize member well-wellbeing.

Cons: May require membership (which is usually easy to obtain), approval criteria can still be stringent depending on the severity of your bad credit.

3. Online Lenders

A growing number of online lenders specialize in bad credit auto loans. Companies like Capital One Auto Finance, Carvana, or local online brokers can offer pre-qualification options, which allow you to see potential loan terms without a hard inquiry on your credit report. This is a great way to shop around and compare offers from the comfort of your home.

Pros: Convenience, ability to compare multiple offers quickly, pre-qualification doesn’t hurt your credit, potentially competitive rates.

Cons: Less personalized service, can be overwhelming with too many options, need to be wary of predatory lenders.

4. "Buy Here, Pay Here" (BHPH) Dealerships

These dealerships, common in Spokane and elsewhere, are unique because they are both the seller and the lender. This means they finance the vehicle directly to you, often without a traditional credit check. Approval is generally easier, as they focus more on your income and ability to make payments directly to them.

Pros: Very high approval rates, especially for those with very poor credit or no credit history.

Cons: Significantly higher interest rates (often the maximum allowed by state law), limited vehicle selection (usually older, higher-mileage used cars), and frequently do not report payments to credit bureaus, which defeats the purpose of rebuilding credit. Pro tips from us: We generally recommend BHPH as a last resort. If you do go this route, ensure they report to at least one major credit bureau so your on-time payments can help improve your score. For more insights on choosing the right lender and avoiding common pitfalls, check out our article on .

The Application Process: Navigating the Details

Once you’ve identified potential lenders, the application process will begin. If you’ve pre-qualified with an online lender or a credit union, you’ll move to the full application. This involves providing all the documentation you gathered earlier.

Lenders will assess several factors beyond your credit score. They’ll look at your debt-to-income ratio (DTI), which measures how much of your gross monthly income goes towards debt payments. A lower DTI indicates you have more disposable income to cover new loan payments. They will also consider your employment history and stability, your residency stability, and your overall financial picture. Honesty and transparency are paramount here; trying to hide information will only complicate matters.

Negotiating Your Bad Credit Car Loan: Empowering Yourself

Even with bad credit, you still have room to negotiate. Remember, the goal is not just to get approved, but to get the best possible terms.

- Focus on the Total Cost: Don’t get fixated solely on the monthly payment. A low monthly payment might mean a longer loan term and much more interest paid over time. Ask for the total cost of the loan, including interest, over its lifetime.

- Interest Rate: This is where you’ll pay the most. If you have multiple offers, leverage them against each other.

- Loan Term: Shorter terms mean higher monthly payments but less interest. Balance this against your budget.

- Down Payment: If you can increase your down payment, it’s worth exploring how that impacts the interest rate and monthly payment.

- Consider a Co-signer: If you have a trusted family member or friend with good credit who is willing to co-sign, it can significantly improve your chances of approval and secure a lower interest rate. However, understand that a co-signer is equally responsible for the loan, and their credit will be affected if you miss payments. This is a serious commitment for both parties.

Choosing the Right Vehicle for Your Situation

With bad credit, it’s crucial to be practical about your vehicle choice. Focus on reliable, affordable used cars rather than brand-new, expensive models. A newer car depreciates quickly, and the added cost can put unnecessary strain on your budget.

Look for vehicles that have a strong reputation for reliability and lower maintenance costs. A good choice would be a few years old, with reasonable mileage, and a clean vehicle history report (like CarFax or AutoCheck). Remember, this first car loan is a stepping stone. Your primary goal is to secure reliable transportation and build a positive payment history.

The Path to Financial Recovery: Rebuilding Credit with Your New Car Loan

This is perhaps the most valuable aspect of securing a bad credit car loan. Your car loan can become a powerful tool for credit repair.

Pro tips from us: Make every single payment on time, every time. Payment history accounts for 35% of your FICO score, making it the most significant factor. Even one late payment can undo months of positive progress. Set up automatic payments or calendar reminders to ensure you never miss a due date.

As you consistently make on-time payments, your credit score will gradually improve. After 12-18 months of responsible payments, you might be in a position to explore refinancing your car loan at a lower interest rate. This can save you a significant amount of money over the remaining term of the loan. To understand more about improving your credit score and the factors involved, resources like Experian offer valuable insights into credit building strategies.

Conclusion: Your Road to Financial Freedom Starts Now

Securing a bad credit car loan in Spokane, WA, is more than just a transaction; it’s an opportunity for a fresh start. While the process may seem daunting, by understanding your credit, preparing diligently, exploring the right lenders, and making informed decisions, you can successfully navigate the journey. Remember, this isn’t just about getting a car; it’s about establishing a positive payment history, rebuilding your credit score, and opening doors to a more stable financial future.

Don’t let past financial missteps define your present or future. Take control, leverage the insights provided in this comprehensive guide, and confidently pursue your goal of securing reliable transportation and building a stronger financial foundation. The road to financial freedom might have a few bumps, but with the right approach, you can drive forward with confidence. Start your preparation today and take the first step toward getting that essential car loan in Spokane, WA, even with bad credit.