Driving Forward: Your Comprehensive Guide to Bad Credit Repo Car Loans

Driving Forward: Your Comprehensive Guide to Bad Credit Repo Car Loans Carloan.Guidemechanic.com

Life throws curveballs, and sometimes those curveballs come in the form of a car repossession. It’s a tough situation that can leave a significant dent in your credit score, making the prospect of securing a new car loan seem like an impossible dream. Many people believe that once your car has been repossessed and your credit is damaged, you’re permanently out of the running for new auto financing. However, based on my extensive experience in the auto finance industry, I can tell you this isn’t necessarily true. While challenging, securing a car loan after a repossession with bad credit is often achievable, provided you approach it with the right strategy and realistic expectations.

This super comprehensive guide is designed to empower you with the knowledge and tools needed to navigate the complex world of bad credit repo car loans. We’ll delve deep into understanding the impact of repossession, exploring your financing options, and providing actionable steps to help you get back on the road. Our ultimate goal is to equip you with the insights to not only get approved but to do so responsibly, setting you up for future financial success.

Driving Forward: Your Comprehensive Guide to Bad Credit Repo Car Loans

Understanding the Aftermath: How Repossession Impacts Your Credit

Before we discuss solutions, it’s crucial to understand the problem. A repossession occurs when a lender takes back an item, typically a vehicle, that was used as collateral for a loan, usually because the borrower defaulted on payments. This event has a severe and long-lasting impact on your credit report and score.

When a repossession is reported to the major credit bureaus, it immediately lowers your credit score, often by a significant margin. This negative mark can remain on your credit report for up to seven years. During this period, lenders view you as a higher risk, making it more difficult to obtain new credit, including auto loans, mortgages, and even some rental agreements. The mere presence of a repossession signals to potential lenders that there was a past failure to meet financial obligations.

Furthermore, a repossession often leads to a "deficiency balance." This happens if the sale price of the repossessed vehicle doesn’t cover the remaining loan balance, plus any associated fees like towing, storage, and auction costs. If you still owe money after the car is sold, that deficiency balance can be sent to collections, creating yet another negative mark on your credit report and further complicating your financial recovery. Addressing this deficiency balance is often a critical first step in rebuilding your financial standing.

Is a Repo Car Loan Even Possible with Bad Credit? Dispelling the Myths

The short answer is yes, securing a car loan after a repossession with bad credit is absolutely possible. However, it’s not without its challenges and often requires a different approach than traditional financing. Many people wrongly assume that one repossession means they’re blacklisted from auto loans forever. This is simply not the case. While it undeniably makes the process more difficult, it doesn’t close the door entirely.

The key is to understand that "bad credit" is a broad term. A credit score that has taken a hit from a repossession is certainly bad, but lenders often look at the overall picture, not just one negative event. They want to understand the circumstances, your current financial stability, and your commitment to making future payments on time. It’s about demonstrating that despite past difficulties, you are now a reliable borrower.

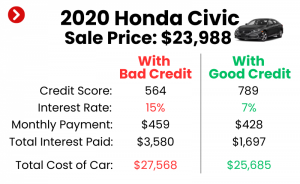

What you can expect is that the terms of such a loan will likely be less favorable than what someone with excellent credit would receive. This typically means higher interest rates and potentially shorter repayment periods. The lending landscape for individuals with bad credit, especially after a repossession, is designed to mitigate risk for the lender. Understanding this reality is the first step toward setting realistic expectations and finding a manageable solution.

Beyond the Score: Key Factors Lenders Consider

When your credit score is low due to a repossession, lenders will scrutinize other aspects of your financial life even more closely. They are looking for reasons to approve you, not just reasons to deny you. Based on my experience working with numerous clients in similar situations, these are the critical factors that can make or break your application:

1. Stable Income and Employment History:

Lenders want to see a consistent and reliable source of income. This demonstrates your ability to make regular loan payments. They will typically ask for proof of income, such as recent pay stubs, tax returns, or bank statements. A long history with the same employer, or at least consistent employment without significant gaps, signals stability and reliability. Even if your credit score is bruised, a steady job for several years can significantly bolster your application.

2. A Substantial Down Payment:

This is perhaps one of the most powerful tools you have. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. It also shows your commitment to the purchase and your financial discipline. Pro tips from us: aiming for at least 10-20% of the vehicle’s purchase price can make a huge difference in approval chances and even secure a lower interest rate. The more skin you have in the game, the more comfortable lenders become.

3. Manageable Debt-to-Income (DTI) Ratio:

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess whether you can comfortably take on additional debt. If your DTI is too high, it indicates that too much of your income is already allocated to existing debts, leaving little room for a new car payment. Aim for a DTI ratio below 43%, though lower is always better. This ratio provides a clear picture of your financial capacity.

4. Responsible Payment History (Since the Repossession):

While the repossession is a significant negative mark, lenders will also look at your payment behavior since that event. Have you been making all your other payments on time? Are there any new collection accounts or missed payments? Demonstrating a period of consistent, on-time payments on other bills (credit cards, utilities, rent) shows that you are actively working to improve your financial habits. This recent positive history can help offset the older negative information.

5. Choice of Vehicle:

The type of vehicle you choose can impact your loan approval. Lenders are often more willing to finance a moderately priced, reliable used car than a brand new, expensive luxury vehicle when dealing with bad credit. A less expensive car means a smaller loan amount, which again, reduces their risk. They also prefer vehicles that hold their value well, as this provides better collateral for the loan. Focus on affordability and practicality rather than aspirations at this stage.

Your Options: Types of Lenders for Bad Credit Repo Car Loans

Finding the right lender is crucial when you have a repossession on your credit history. Traditional banks, while often offering the best rates, are typically the most hesitant. However, a whole segment of the lending industry specializes in helping individuals with challenging credit.

1. Subprime Lenders:

These are financial institutions or divisions of larger banks that specialize in lending to borrowers with lower credit scores. They understand the nuances of bad credit and are more willing to take on higher-risk applicants. Subprime lenders have specific criteria for bad credit repo car loans and often focus heavily on your current income and stability. While their interest rates will be higher than prime rates, they represent a viable pathway to approval. They assess risk differently, often using proprietary scoring models that consider more than just a FICO score.

2. Buy Here Pay Here (BHPH) Dealerships:

BHPH dealerships offer in-house financing, meaning the dealership itself is the lender. This can be a convenient option because the approval process is often faster and less stringent regarding credit scores. They focus heavily on your income and your ability to make payments directly to them. However, common mistakes to avoid are not thoroughly understanding the terms. BHPH loans often come with significantly higher interest rates, shorter repayment terms, and sometimes less protection than traditional loans. Always read the fine print and compare their offers carefully.

3. Credit Unions:

Sometimes, credit unions can be a surprisingly good option, especially if you’re already a member or meet their membership criteria. Credit unions are member-owned and often have more flexible lending standards than large banks, as they prioritize serving their members. They might be more willing to look beyond a repossession if you have a strong relationship with them and demonstrate current financial responsibility. Their rates are often more competitive than subprime lenders or BHPH dealerships.

4. Online Lenders Specializing in Bad Credit:

The digital age has brought forth numerous online lenders that cater specifically to individuals with bad credit. These platforms often have streamlined application processes and can connect you with multiple lenders, increasing your chances of finding an offer. They use advanced algorithms to assess risk and can often provide pre-qualification without a hard credit inquiry, allowing you to shop around more freely. Always ensure any online lender you consider is reputable and has positive customer reviews.

The Application Process: A Step-by-Step Guide

Navigating the application process for bad credit repo car loans can feel daunting, but a structured approach can significantly improve your experience and outcome.

Step 1: Assess Your Current Financial Standing:

Before you even look at cars, take an honest look at your budget. How much can you realistically afford for a monthly car payment, including insurance, fuel, and maintenance? This step is crucial to avoid getting into another difficult financial situation. Understand your income, expenses, and what you can comfortably commit to.

Step 2: Save for a Down Payment:

As discussed, a larger down payment is your best friend. Start saving diligently. Even a few extra hundred dollars can make a difference in your loan terms and approval chances. This also shows lenders your commitment and financial discipline.

Step 3: Obtain Your Credit Reports and Scores:

Access your credit reports from all three major bureaus (Experian, Equifax, TransUnion) and check your scores. Review your reports for any errors and dispute them immediately. Understanding exactly what lenders will see is the first step in addressing any issues. This also helps you prepare to explain any negative marks proactively.

Step 4: Gather Necessary Documents:

Lenders will require documentation to verify your identity, income, and residency. Be prepared with:

- Proof of income (pay stubs, tax returns, bank statements).

- Proof of residence (utility bills, lease agreement).

- Proof of identity (driver’s license, social security card).

- Banking information.

- Trade-in title (if applicable).

Having these ready will expedite the application process.

Step 5: Get Pre-Qualified (Where Possible):

Many lenders, especially online ones, offer pre-qualification that involves a "soft" credit inquiry. This allows you to see potential loan terms without impacting your credit score. Pre-qualification gives you a realistic idea of what you can afford before you commit to a specific vehicle or dealership. This helps you shop smarter and avoid unnecessary hard inquiries.

Step 6: Shop Around for Lenders:

Don’t settle for the first offer. Contact multiple subprime lenders, credit unions, and reputable online lenders. Compare interest rates, loan terms, fees, and any other conditions. Pro tips from us: applying to several lenders within a short timeframe (typically 14-45 days, depending on the credit scoring model) will usually only count as one hard inquiry for FICO scoring purposes, as the bureaus recognize you’re rate shopping for a single loan.

Step 7: Choose an Affordable Vehicle:

Once you have pre-approval or a good understanding of what you can borrow, choose a reliable, affordable vehicle that fits your budget. Remember, this first car after a repossession is often a stepping stone to rebuilding your credit, not necessarily your dream car. Focus on practicality and lower overall cost.

Step 8: Review and Understand the Loan Terms:

Before signing anything, meticulously review the loan agreement. Pay close attention to the interest rate (APR), the total amount you will pay over the life of the loan, any hidden fees, and the repayment schedule. Ask questions until you fully understand every clause. This is where an external link to a trusted source like the Consumer Financial Protection Bureau (CFPB) can be incredibly helpful for understanding your rights and responsibilities: https://www.consumerfinance.gov/consumer-tools/auto-loans/

Pro Tips for Increasing Your Approval Chances

Even with a repossession on your record, there are concrete steps you can take to significantly improve your likelihood of approval for a car loan.

- Save for a Larger Down Payment: This cannot be stressed enough. A substantial down payment directly reduces the lender’s risk and can lead to more favorable loan terms. It shows financial responsibility and reduces the loan-to-value ratio, making the loan more secure for the lender.

- Find a Co-Signer with Good Credit: If you have a trusted friend or family member with good credit who is willing to co-sign for you, this can dramatically increase your approval chances and potentially secure a lower interest rate. A co-signer shares the legal responsibility for the loan, providing an additional layer of security for the lender. Ensure both parties understand the full implications.

- Choose an Affordable and Practical Vehicle: Lenders are more comfortable financing a moderately priced, reliable used car. Avoid trying to purchase a luxury vehicle or something beyond your immediate needs. The goal here is to get approved, build credit, and eventually upgrade.

- Show Proof of Stability: Lenders value stability. This includes a consistent work history (preferably with the same employer for a year or more) and a stable residence. Providing utility bills in your name or a rental agreement can help demonstrate this.

- Be Honest and Transparent: Don’t try to hide your past repossession or any other credit issues. Be upfront with lenders about your financial history. Explain the circumstances surrounding the repossession if there were mitigating factors (e.g., job loss, medical emergency). Lenders appreciate honesty and a willingness to address past challenges.

- Improve Your Credit Score (Even Slightly) Before Applying: While a full credit overhaul takes time, even small improvements can help. Pay down small debts, make all current payments on time, and keep credit card balances low. Every point matters when you’re on the edge of approval. For more detailed strategies, consider checking out our guide on .

Common Mistakes to Avoid

Navigating bad credit repo car loans can be tricky. Avoiding these common pitfalls will save you time, stress, and potentially money.

- Applying Everywhere Indiscriminately: Each time you apply for credit, a "hard inquiry" is typically placed on your credit report. Too many hard inquiries in a short period can further lower your credit score and make you appear desperate to lenders. Instead, use pre-qualification options first and strategically apply to a select few lenders within a short timeframe.

- Settling for the First Offer: Just because you have bad credit doesn’t mean you have to accept the first loan offer that comes your way. Always shop around and compare terms from at least 3-5 different lenders. You might be surprised at the variation in rates and fees.

- Ignoring the Fine Print: Loan agreements can be complex, but it’s vital to read and understand every single clause. Pay attention to prepayment penalties, late fees, and what happens in case of default. Don’t be afraid to ask for clarification on anything you don’t understand.

- Overstretching Your Budget: It’s tempting to want a nicer car, but committing to a payment you can’t comfortably afford is a recipe for disaster and can lead to another repossession. Be realistic about your budget, including insurance, fuel, and maintenance costs, not just the monthly car payment.

- Not Understanding Interest Rates and Fees: With bad credit, interest rates will be higher. Make sure you understand the Annual Percentage Rate (APR) and how it translates to the total cost of the loan over time. Also, be aware of any origination fees, documentation fees, or other charges that might be added to the loan amount.

Rebuilding Your Credit After Repossession: Your Long-Term Strategy

Securing a car loan after repossession is a significant step, but it’s also an opportunity to fundamentally rebuild your credit and financial health. This loan can be a powerful tool for improvement if managed correctly.

The most critical step in rebuilding your credit is making every single loan payment on time, every month. Consistent, on-time payments are the most influential factor in your credit score. This demonstrates to future lenders that you are a reliable borrower. Set up automatic payments if possible, and always ensure you have sufficient funds in your account.

Beyond your car loan, look for other ways to establish positive credit history. Consider a secured credit card, where you deposit funds as collateral, which then becomes your credit limit. Or explore a credit builder loan, which helps you save money and build credit simultaneously. These tools, combined with responsible management of your car loan, can accelerate your credit recovery. Regularly monitor your credit report to ensure all payments are reported correctly and to spot any errors that need disputing.

Understanding the Costs and Risks

While bad credit repo car loans offer a second chance, it’s essential to be fully aware of the associated costs and potential risks. These loans are designed for higher-risk borrowers, which means lenders mitigate their risk through less favorable terms.

The most prominent cost will be the higher interest rate. Your Annual Percentage Rate (APR) will likely be significantly higher than what someone with excellent credit would receive. This translates to a higher total cost of the loan over its lifetime. It’s not uncommon for bad credit car loans to have APRs in the double digits.

Additionally, loan terms might be shorter, leading to higher monthly payments, or conversely, longer terms that spread out the payments but increase the total interest paid. Some lenders might also require additional collateral or a GPS tracking device on the vehicle. Be vigilant about potential predatory lending practices, such as excessive fees, extremely high interest rates that feel usurious, or pressure to sign without fully understanding the terms. Always work with reputable lenders and review all documentation thoroughly.

The "Second Chance" Opportunity: Turning a Negative into a Positive

Ultimately, securing a bad credit repo car loan isn’t just about getting a vehicle; it’s about seizing a second chance to prove your financial reliability. Many individuals who successfully navigate this path view it as a pivotal moment in their financial journey. It’s an opportunity to transform a negative credit event into a stepping stone for future financial stability.

By making consistent, on-time payments, you are actively demonstrating to credit bureaus and future lenders that you are a responsible borrower. This positive payment history will slowly but surely overshadow the past repossession, leading to a gradual improvement in your credit score. As your score improves, you’ll gain access to better financial products, lower interest rates, and more opportunities down the line.

Pro tips from us: View this loan as a tool for rebuilding. Don’t just focus on the car, but on the credit-building potential it offers. Once your credit score improves significantly, you might even be able to refinance your car loan at a lower interest rate, further reducing your overall costs. This proactive approach is what truly unlocks the value of a second chance. For more insights on leveraging such opportunities, explore our guide on .

Conclusion: Driving Towards a Brighter Financial Future

Securing a car loan after a repossession with bad credit is undoubtedly a challenging endeavor, but it is far from impossible. By understanding the impact of repossession, knowing your lending options, and meticulously preparing for the application process, you can significantly increase your chances of approval. Remember, the journey begins with realistic expectations, a commitment to financial responsibility, and a willingness to put in the necessary effort.

While the terms of a bad credit repo car loan might not be ideal, view it as a valuable opportunity. This loan can serve as a powerful vehicle (pun intended!) for rebuilding your credit, demonstrating your newfound financial discipline, and ultimately paving the way for a more secure financial future. Don’t let past setbacks define your future. With diligent research, strategic planning, and consistent effort, you can get back on the road and drive towards a brighter financial horizon. Start today by assessing your budget, pulling your credit report, and exploring your lender options. Your future self will thank you.