Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Bankruptcy Discharge

Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Bankruptcy Discharge Carloan.Guidemechanic.com

Navigating the financial landscape after bankruptcy can feel like traversing a dense fog. You’ve faced significant challenges, made tough decisions, and now, with a bankruptcy discharge behind you, you’re ready for a fresh start. One of the most common hurdles people encounter on this new path is securing reliable transportation – specifically, getting a car loan.

Many believe that a bankruptcy discharge instantly slams the door shut on future credit, especially for a major purchase like a car. This simply isn’t true. While it presents a unique set of challenges, obtaining a car loan after bankruptcy discharge is absolutely achievable with the right strategy, patience, and commitment. This in-depth guide is designed to empower you with the knowledge and tools you need to successfully finance a vehicle, rebuild your credit, and drive confidently into your financial future.

Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Bankruptcy Discharge

Understanding Bankruptcy Discharge: A True New Beginning

Before diving into car loans, let’s clarify what a bankruptcy discharge truly signifies. A bankruptcy discharge is a court order that releases you from the legal obligation to pay most of your debts. It’s not just a temporary reprieve; it’s a permanent injunction prohibiting creditors from taking any collection action on those specific debts.

For you, this means a clean slate in many respects. From a lender’s perspective, it indicates that you are no longer burdened by the overwhelming debts that led to bankruptcy. This can, surprisingly, make you a more attractive borrower than someone teetering on the brink of bankruptcy, as your debt-to-income ratio is likely much lower post-discharge. Based on my experience working with countless individuals post-bankruptcy, the discharge date is a pivotal moment, signaling the end of one chapter and the definite start of another.

There are two main types of consumer bankruptcy: Chapter 7 and Chapter 13. A Chapter 7 discharge typically occurs within a few months of filing, offering a swift resolution. Chapter 13, on the other hand, involves a repayment plan over three to five years, with discharge happening only after all plan payments are successfully completed. The timing of your discharge, and which chapter it was, can subtly influence how lenders view your readiness for a new auto loan.

The Immediate Aftermath: Credit Score Realities and Rebuilding

It’s no secret that bankruptcy significantly impacts your credit score. Immediately after filing, you’ll likely see a substantial drop, and the bankruptcy will remain on your credit report for seven to ten years, depending on the chapter. This reality can be disheartening, but it’s crucial to understand it’s not a permanent sentence.

Lenders are naturally cautious when they see a bankruptcy on a credit report. It signifies a past inability to manage debts. However, what they also look for is what you’ve done since the discharge. A bankruptcy can be seen as a "reset button" for your financial life. The key is to demonstrate that you’ve learned from the experience and are now a responsible borrower.

Pro tips from us: Immediately after discharge, obtain copies of your credit reports from all three major bureaus – Equifax, Experian, and TransUnion. You can do this for free annually at AnnualCreditReport.com. Scrutinize them for any errors and dispute them promptly. Understanding your baseline is the first critical step in your credit rebuilding journey.

When Is The Right Time? Assessing Your Readiness for an Auto Loan

There’s no universal "magic number" of months or a specific credit score that dictates when you’re truly ready for a car loan after bankruptcy discharge. Instead, it’s about demonstrating financial stability and a renewed commitment to responsible credit management. While some lenders might consider you almost immediately, a more strategic approach will yield better results and more favorable terms.

Key indicators of your readiness include:

- Stable Income: Lenders want to see consistent, verifiable income. This demonstrates your ability to make regular loan payments.

- Post-BK Credit Rebuilding: Have you taken steps to establish new, positive credit? Even small accounts can make a big difference.

- Budgetary Control: Can you comfortably afford a car payment, insurance, fuel, and maintenance without stretching your finances thin?

- Down Payment Saved: This is perhaps the single most impactful factor for securing a car loan after bankruptcy.

Common mistakes to avoid are applying for a loan too soon after discharge without any credit rebuilding efforts, or before you have a stable financial footing. Rushing into an application can lead to multiple hard inquiries on your credit report, which can further depress your score, and result in higher interest rates or outright rejections. Patience and preparation are your strongest allies.

Key Factors Lenders Consider Beyond Your Score

While your credit score is undoubtedly a significant factor, especially after bankruptcy, it’s far from the only thing lenders scrutinize. They adopt a holistic view, evaluating various aspects of your financial profile to assess risk. Understanding these factors can help you better prepare and present yourself as a reliable borrower.

1. Income and Employment Stability:

Lenders want assurance that you have the consistent financial capacity to repay the loan. This means they will look at your employment history. A long tenure at your current job, or a history of stable employment in a particular field, speaks volumes about your reliability. They will typically request pay stubs, W-2s, or tax returns to verify your income.

2. Debt-to-Income (DTI) Ratio:

Even post-bankruptcy, your current debt obligations are important. Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income available to cover new loan payments, making you a less risky borrower. Aim for a DTI below 40-45%, if possible, including your projected car payment.

3. Down Payment:

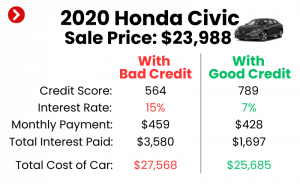

This is arguably the "golden ticket" for securing a car loan after bankruptcy. A substantial down payment significantly reduces the amount you need to borrow, thereby decreasing the lender’s risk. It also demonstrates your commitment and financial discipline. The more you put down, the better your chances of approval and potentially more favorable interest rates.

4. Vehicle Choice:

Lenders prefer to finance vehicles that hold their value well. Choosing a reasonably priced, reliable used car rather than a brand-new luxury model will be viewed more favorably. Overly expensive or niche vehicles can be harder to finance, as their resale value might be less predictable, increasing the lender’s risk in case of default.

5. Co-signer (Optional):

Bringing in a co-signer with good credit can dramatically improve your chances of approval and secure a better interest rate. A co-signer essentially pledges their own creditworthiness to guarantee the loan if you default. While beneficial, it’s a serious commitment for the co-signer, as their credit will also be impacted if you miss payments. Discuss this option thoroughly with potential co-signers, ensuring they understand the full implications.

6. Post-Bankruptcy Credit History:

This is where your rebuilding efforts truly shine. Lenders will look for any new lines of credit opened since your discharge – even small ones, like a secured credit card or a credit builder loan. A consistent history of on-time payments on these new accounts demonstrates your renewed financial responsibility and helps offset the negative impact of the bankruptcy.

Strategies for Boosting Your Approval Chances

Securing a car loan after bankruptcy discharge requires a proactive and strategic approach. By focusing on these key areas, you can significantly improve your eligibility and secure more manageable loan terms.

A. Rebuilding Your Credit Proactively

This is paramount. While bankruptcy remains on your report, you can start building a new, positive credit history almost immediately.

- Secured Credit Cards: These are an excellent starting point. You deposit money into an account, and that deposit becomes your credit limit. Use it for small, regular purchases and pay the balance in full and on time every month. This demonstrates responsible credit usage to the credit bureaus. Based on my experience, consistently making small, on-time payments on secured credit cards is the fastest way to signal responsibility to lenders.

- Credit Builder Loans: Offered by some credit unions and community banks, these loans work in reverse. The loan amount is held in a savings account while you make payments. Once the loan is paid off, you get access to the funds. These are specifically designed to help people build credit.

- Reporting Rent and Utilities: Services exist that report your on-time rent and utility payments to credit bureaus. This can add positive payment history to your report, especially if you have limited other credit accounts.

- Authorized User Status (with caution): If a trusted family member with excellent credit is willing to add you as an authorized user on one of their credit cards, their positive payment history can appear on your report. However, ensure they have a spotless record, and you should not use the card unless agreed upon.

B. Saving a Substantial Down Payment

As mentioned, a down payment is incredibly powerful. For post-bankruptcy car loans, aiming for 10-20% of the vehicle’s purchase price, or even more, is highly recommended.

- Why it’s crucial: A larger down payment reduces the loan amount, lowers your monthly payments, and most importantly, signals to lenders that you have "skin in the game." It shows you’re serious about your commitment and have the financial discipline to save.

- Benefits: It directly reduces the lender’s risk, making them more willing to approve your loan, potentially with a lower interest rate than you might otherwise receive.

C. Creating a Realistic Budget

Before even looking at cars, sit down and create a detailed budget. This isn’t just about qualifying for a loan; it’s about ensuring you can comfortably afford the entire cost of vehicle ownership.

- Beyond the monthly payment: Factor in insurance (which might be higher after bankruptcy), fuel, maintenance, and unexpected repairs.

- Avoid overextending: Don’t let the excitement of a new car lead you to commit to payments that strain your budget. A reliable, affordable car that you can pay for on time is far better than a luxury vehicle that causes financial stress.

D. Shopping Smart for Your Loan

Don’t just walk into the first dealership and accept their initial offer. Smart shopping can save you thousands over the life of the loan.

- Credit Unions: Often, credit unions are more community-focused and may be more willing to work with members who have a past bankruptcy, especially if you have a history with them. Their rates can also be more competitive.

- Dealerships (Subprime Lenders): Many dealerships have relationships with "subprime" lenders who specialize in bad credit auto loans. While convenient, be prepared for potentially higher interest rates. Always understand the full terms before signing.

- Online Lenders: There are online lenders that specifically cater to individuals with less-than-perfect credit. Research reputable ones, read reviews, and compare their offerings.

- Pre-qualification: Seek pre-qualification from multiple lenders. This allows you to see potential loan terms and interest rates without a hard inquiry impacting your credit score. This is a soft pull and helps you shop with confidence. Common mistake: Only applying at one place. Comparison shopping is vital.

E. Understanding Interest Rates and Terms

After bankruptcy, expect that your initial interest rate will be higher than what someone with excellent credit would receive. This is the reality of increased risk for the lender.

- Focus on affordability: While a lower interest rate is always desirable, your primary focus should be on securing an affordable monthly payment that fits your budget.

- Shorter vs. Longer Terms: Shorter loan terms mean higher monthly payments but less interest paid over time. Longer terms reduce monthly payments but significantly increase the total interest cost. Balance these factors with your budget and long-term financial goals.

- The bigger picture: Remember, this first loan is a stepping stone. Your goal is to make all payments on time to rebuild your credit, which will open doors to better rates in the future.

The Application Process: What to Expect

Once you’ve done your homework and chosen a few potential lenders, it’s time for the application. Being prepared can make the process much smoother and increase your chances of approval.

- Gathering Documents: Lenders will typically require proof of income (pay stubs, tax returns), proof of residency (utility bills), identification (driver’s license), and most importantly, your bankruptcy discharge papers. Having these readily available will save time.

- Being Transparent: Don’t try to hide your bankruptcy. Lenders will find it on your credit report. Be honest and explain your situation calmly and confidently, highlighting the steps you’ve taken since discharge to improve your financial standing. This transparency builds trust.

- Patience and Persistence: It’s possible you might face a rejection or two. Don’t get discouraged. Use it as an opportunity to ask the lender why you were denied and what steps you can take to improve your chances next time. Based on my experience, being fully prepared with all necessary documentation can significantly smooth out the application process.

The Future: Refinancing and Continuous Improvement

Securing your first car loan after bankruptcy discharge is a significant achievement, but it’s often just the beginning of your journey toward regaining financial strength. View this initial loan as a strategic tool to rebuild your credit.

After 6 to 12 months of consistent, on-time payments, you’ll likely be in a much stronger position. At this point, you should explore refinancing your car loan. With a solid payment history and an improved credit score, you can often qualify for a lower interest rate, which will reduce your monthly payments or the total interest paid over the life of the loan.

Don’t stop your credit rebuilding efforts once you have the car. Continue to manage your finances responsibly, make all payments on time, and keep your credit utilization low. Each positive financial action you take further strengthens your credit profile, paving the way for even better financial opportunities in the future.

Conclusion: Your Road to Financial Recovery

Getting a car loan after bankruptcy discharge is not merely a possibility; it’s a tangible goal that many individuals successfully achieve. It requires diligence, strategic planning, and a steadfast commitment to rebuilding your financial life. While the path might have its challenges, each step you take – from understanding your discharge to meticulously rebuilding your credit and shopping wisely for a loan – brings you closer to your objective.

Remember, bankruptcy marks an end, but more importantly, it signifies a new beginning. By following the comprehensive advice outlined in this guide, you are not just securing a car loan; you are actively taking control of your financial narrative. Drive forward with confidence, knowing that a fresh start is truly within your reach.