Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Chapter 13 Discharge

Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Chapter 13 Discharge Carloan.Guidemechanic.com

For many, the dream of reliable transportation feels out of reach after navigating the complexities of Chapter 13 bankruptcy. You’ve worked hard, completed your payment plan, and finally received that coveted discharge letter. Now, a new challenge arises: securing a car loan. It’s a common misconception that your financial journey ends with discharge; in reality, it’s just beginning a new, more empowered chapter.

Based on my experience in the financial landscape, I can tell you unequivocally that getting a car loan after Chapter 13 discharge is absolutely possible. It requires a strategic approach, a clear understanding of your financial standing, and a commitment to demonstrating renewed creditworthiness. This isn’t just about getting approved; it’s about getting the best possible terms to propel your financial recovery even further. In this comprehensive guide, we’ll peel back the layers, offering you an in-depth roadmap to confidently navigate the process and drive away with the vehicle you need.

Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Chapter 13 Discharge

Understanding Chapter 13 Discharge and Its True Impact

Before diving into loan applications, it’s crucial to grasp what Chapter 13 discharge signifies. Unlike Chapter 7, which liquidates non-exempt assets, Chapter 13 involves a court-approved repayment plan, typically lasting three to five years. During this period, you make regular payments to a trustee, who then distributes funds to your creditors.

A Chapter 13 discharge means you have successfully completed this repayment plan. The remaining eligible debts are wiped clean, providing you with a fresh financial slate. This is a monumental achievement and a testament to your commitment to financial responsibility.

However, it’s important to differentiate discharge from dismissal. A dismissal means your Chapter 13 case was closed without completion, often leaving you with the original debts. A discharge, on the other hand, signals a successful conclusion, which lenders view much more favorably. Your discharge letter is your official proof of this success, a vital document for any future loan applications.

While the discharge itself marks a positive turning point, your credit report will still reflect the bankruptcy for up to seven years from the filing date. This initial impact can be daunting, but it doesn’t mean your credit is permanently broken. It simply means you need to demonstrate new patterns of responsible financial behavior to rebuild it.

The New Financial Landscape: What Lenders See

After a Chapter 13 discharge, lenders look at your financial profile through a unique lens. They understand you’ve been through a challenging period, but they also want to see evidence of stability and a commitment to future financial health. Here’s what’s on their radar:

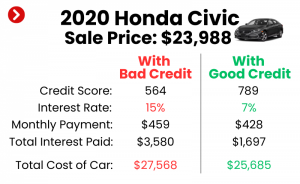

Firstly, your credit score will likely be low. This is an unavoidable consequence of bankruptcy. However, the good news is that scores begin to improve steadily once the discharge is processed, especially if you’ve been making other payments on time. Lenders specializing in bad credit understand this trajectory.

Secondly, your Debt-to-Income (DTI) ratio often looks much more attractive post-discharge. With many unsecured debts eliminated or significantly reduced, your monthly debt obligations are considerably lower. This indicates you have more disposable income available to manage new debt, such as a car loan.

Thirdly, lenders meticulously examine your payment history since the discharge. Any new credit accounts, even small ones like a secured credit card or a utility bill paid punctually, demonstrate your ability to handle financial commitments responsibly. This fresh payment history is incredibly powerful in signaling a positive change.

Finally, stability in your employment and residence plays a significant role. A consistent job history and a stable living situation reassure lenders that you have the means and the foundation to make regular car loan payments. Lenders are looking for reliability, not just current income.

Pro tips from us: Focus on establishing and maintaining these elements of stability. Even small steps, like ensuring your rent or mortgage is paid on time, contribute to a positive overall picture for lenders.

Essential Steps Before Applying for a Car Loan

Before you even think about stepping onto a car lot or filling out an online application, there are several critical preparatory steps you must take. These actions will not only increase your chances of approval but also help you secure better loan terms.

Step 1: Get Your Credit Report in Order

Your credit report is your financial resume, and it’s imperative that it’s accurate and up-to-date. Obtain a copy of your credit report from all three major bureaus: Equifax, Experian, and TransUnion. You can do this annually for free through AnnualCreditReport.com.

Once you have your reports, review them meticulously for any inaccuracies or errors. Sometimes, creditors fail to update the bankruptcy status correctly, or old debts might still appear. Dispute any errors immediately; correcting these can positively impact your score. Understanding your credit score, even if it’s low, gives you a baseline for improvement and helps manage your expectations.

Step 2: Build a Strong Financial Foundation

This step is about demonstrating financial maturity and foresight. Establishing a realistic budget is paramount. Track your income and expenses to clearly understand where your money goes and identify areas where you can save.

One of the most impactful actions you can take is saving for a significant down payment. Lenders view a substantial down payment as a sign of your commitment and reduces their risk. It also lowers the amount you need to borrow, which can lead to more favorable interest rates and lower monthly payments. Aim for at least 10-20% of the car’s value if possible.

Furthermore, building an emergency fund, even a small one, shows financial prudence. It signals to lenders that you are prepared for unexpected expenses without jeopardizing your loan payments.

Common mistakes to avoid are rushing this step. Many individuals are eager to get a car, but skipping the financial preparation can lead to higher interest rates, unaffordable payments, or even loan denial. Patience here pays dividends.

Step 3: Understand Your Affordability

Don’t just think about the monthly car payment; consider the total cost of ownership. This includes insurance premiums, fuel costs, routine maintenance, and potential repairs. Use an online car loan calculator to play with different down payment amounts, interest rates, and loan terms to see what fits comfortably within your budget.

Remember, a car payment should not strain your finances. A general rule of thumb is that your total car expenses (payment, insurance, fuel) should not exceed 10-15% of your take-home pay. Being realistic about what you can afford prevents future financial stress.

Step 4: Secure Your Discharge Letter

This document is your golden ticket. Lenders will require official proof that your Chapter 13 case has been successfully discharged. Keep a copy readily accessible, both digitally and physically. It’s a non-negotiable item for your loan application.

Navigating the Application Process: Finding the Right Lender

With your preparations complete, it’s time to explore your lending options. Not all lenders are created equal, especially when you’re seeking a car loan after Chapter 13 discharge. Knowing where to look can save you time and frustration.

Option 1: Subprime Lenders/Specialized Lenders

These lenders specialize in working with individuals who have less-than-perfect credit, including those with recent bankruptcies. They understand the challenges and are more willing to take on higher risk.

While they offer a viable path to approval, be prepared for higher interest rates compared to traditional loans. Their business model is built around mitigating this increased risk. However, securing a loan through a subprime lender and making timely payments is an excellent way to rebuild your credit.

Pro tips from us: Research reputable subprime lenders online. Look for those with positive customer reviews and transparent terms. Avoid "guaranteed approval" scams, as they often come with predatory rates and fees.

Option 2: Credit Unions

Credit unions are often more forgiving than large banks. As member-owned institutions, they frequently prioritize member relationships and individual circumstances over strict credit score cut-offs.

If you are already a member of a credit union, or if there’s one you can join, it’s worth exploring their auto loan options. They might offer more competitive rates or more flexible terms than subprime lenders, even with a post-bankruptcy credit profile. Their personal approach can make a significant difference.

Option 3: Dealership Financing (Direct & Indirect)

Many dealerships offer financing directly or through a network of lenders they partner with. When you apply for a loan at a dealership, they often submit your application to multiple banks and finance companies, including those specializing in subprime loans.

Be cautious with "Buy Here, Pay Here" (BHPH) dealerships. While they often approve individuals regardless of credit history, their interest rates are typically very high, and the cars they sell might be older and less reliable. They can be a last resort, but not usually the best first option.

Option 4: Online Lenders

A growing number of online lenders specialize in bad credit auto loans. They offer convenience, quick pre-approval processes, and often a wide range of options. You can compare rates from multiple lenders without leaving your home, which can be very efficient.

Just like with subprime lenders, scrutinize online lenders for their reputation and transparency. Read reviews and ensure they are legitimate. Pre-approval from an online lender can give you leverage when negotiating at a dealership.

Key Factors That Influence Your Loan Approval & Terms

Several elements will weigh heavily on a lender’s decision to approve your loan and the terms they offer. Understanding these can help you strengthen your application.

- Down Payment: As mentioned, a larger down payment significantly reduces the lender’s risk and shows your financial commitment. It can lead to lower interest rates and a better chance of approval.

- Debt-to-Income (DTI) Ratio: Lenders want to see that you have enough disposable income to comfortably make your car payments. A lower DTI ratio, which is often improved post-discharge, works in your favor.

- Employment Stability: A steady job history, ideally for at least six months to a year, demonstrates a reliable income stream. Lenders prefer applicants who show consistency in their employment.

- Vehicle Choice: Lenders are often more willing to finance newer, lower-mileage used cars or even new cars. These vehicles typically hold their value better and are less prone to immediate repair issues, reducing the risk of you defaulting due to unexpected maintenance costs. Avoid older, high-mileage vehicles that are harder to finance.

- Co-signer: If you have a trusted friend or family member with excellent credit who is willing to co-sign your loan, this can dramatically improve your chances of approval and secure more favorable interest rates. A co-signer shares the legal responsibility for the loan, offering an additional layer of security for the lender.

- Payment History Post-Discharge: Any new credit accounts you’ve opened and managed responsibly since your discharge—even a secured credit card with a small limit—will demonstrate your renewed creditworthiness. This recent, positive payment history is a powerful indicator.

The Power of Pre-Approval

One of the most effective strategies you can employ is to get pre-approved for a car loan before you visit any dealerships. This step provides immense benefits and puts you in a much stronger negotiating position.

When you’re pre-approved, you know exactly how much money you qualify for and at what interest rate. This allows you to shop for a car with a clear budget in mind, preventing you from falling in love with a vehicle you can’t truly afford.

Based on my experience, walking into a dealership with a pre-approval letter is like having cash in hand. Dealers view you as a serious buyer and will often work harder to either match or beat the pre-approved rate to earn your business. This leverage can save you thousands of dollars over the life of the loan.

To get pre-approved, you’ll typically fill out an application with a bank, credit union, or online lender. They will review your credit history, income, and DTI ratio. This process usually involves a "soft" credit inquiry, which doesn’t harm your credit score, or a "hard" inquiry if you proceed with a full application, which is a small, temporary dip.

What to Expect During the Loan Application

Even with meticulous preparation, the reality of applying for a car loan after Chapter 13 discharge means you should set realistic expectations.

You should anticipate higher interest rates initially. This is a common consequence of a lower credit score post-bankruptcy. The goal is to get approved, establish a positive payment history, and then potentially refinance at a lower rate down the line.

Lenders might also offer shorter loan terms. Instead of a 72-month loan, you might be offered a 48 or 60-month term. While this means higher monthly payments, it also means you pay less interest over time and build equity faster.

Be prepared to provide a range of required documents, including your discharge letter, proof of income (pay stubs, tax returns), proof of residence (utility bills, lease agreement), and potentially bank statements. Having these ready will streamline the process.

Focus on the long-term goal. This first car loan is not just about transportation; it’s a crucial stepping stone in rebuilding your credit. Every on-time payment will contribute positively to your credit score, paving the way for better financial opportunities in the future.

Rebuilding Your Credit Through Your Car Loan

This car loan is more than just a means to get around; it’s a powerful tool for credit rehabilitation. The single most important action you can take to rebuild your credit is to make every single payment on time, every single month.

A car loan is an installment loan, meaning you pay a fixed amount over a set period. Successfully managing this type of debt demonstrates stability and reliability to future creditors. As your payment history grows with consistent on-time payments, your credit score will steadily improve.

This improved credit score will open doors to better financial products. Within 12-24 months of consistent payments, you might be in a position to refinance your car loan at a lower interest rate, saving you money. You’ll also find it easier to qualify for other forms of credit, such as mortgages or credit cards, with more favorable terms. This loan is an investment in your financial future.

Common Mistakes to Avoid

Even with the best intentions, it’s easy to stumble. Being aware of common pitfalls can help you avoid them.

- Applying everywhere: Each time you apply for credit, it typically results in a "hard inquiry" on your credit report, which can slightly lower your score. Spreading out applications too much can make it look like you’re desperate for credit. Instead, target a few lenders you’ve researched.

- Buying more car than you can afford: It’s tempting to get the latest model, but overextending yourself financially can lead to payment struggles and even repossession. Stick to your budget, even if it means a more modest vehicle initially.

- Skipping the down payment: While some lenders offer zero down payment options, this is rarely a good idea, especially after bankruptcy. A down payment reduces your loan amount, lowers your monthly payments, and provides you with immediate equity in the vehicle.

- Not reading the fine print: Always review the loan agreement thoroughly. Understand the interest rate, loan term, total cost of the loan, and any prepayment penalties or fees. If something is unclear, ask for clarification.

- Ignoring insurance costs: Car insurance can be a significant monthly expense, especially for newer vehicles or if you have a less-than-perfect driving record. Factor this into your overall budget before committing to a car purchase.

Common mistakes to avoid are letting emotions override logical financial decisions. A car is a necessity for many, but it’s also a major financial commitment that requires careful planning.

Pro Tips for Success

Here are some additional insights to help you secure the best possible car loan after Chapter 13 discharge and continue your financial ascent.

- Negotiate, negotiate, negotiate! Don’t be afraid to haggle on the car’s price, trade-in value (if applicable), and even the interest rate. Having a pre-approval gives you powerful leverage.

- Be transparent with lenders. Explain your situation honestly and concisely. Lenders appreciate honesty and a clear plan for financial recovery. This builds trust.

- Consider a reliable used car first. A slightly older, well-maintained used car can be a more affordable and practical option, allowing you to establish credit without a massive financial burden. You can always upgrade later.

- Keep actively improving your credit score. Beyond the car loan, continue to pay all your bills on time, keep credit utilization low on any credit cards, and periodically check your credit report for errors. For more detailed strategies, read our guide on How to Improve Your Credit Score After Bankruptcy.

- Understand your Debt-to-Income (DTI) ratio. Knowing this number and how it impacts loan approvals is crucial. Dive deeper into this topic with our article on Understanding Debt-to-Income Ratio for Loan Applications.

- Seek financial education: Continuously educate yourself on personal finance. Reputable sources like the Consumer Financial Protection Bureau (consumerfinance.gov) offer invaluable free resources on managing debt, understanding credit, and making informed financial decisions.

Driving Towards a Brighter Future

Getting a car loan after Chapter 13 discharge is not a sprint; it’s a marathon of financial rebuilding. While the path may seem challenging, it is undeniably achievable with diligent preparation, strategic decision-making, and a commitment to responsible financial habits. Your discharge letter is a symbol of a fresh start, and securing a car loan can be the next powerful step in demonstrating your renewed creditworthiness.

By understanding what lenders look for, meticulously preparing your finances, exploring the right lending avenues, and consistently making on-time payments, you can not only get the reliable transportation you need but also significantly improve your credit score. This journey is about empowering yourself, taking control of your financial narrative, and driving confidently towards a future of stability and opportunity. You’ve earned this fresh start; now go out and make the most of it.