Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Chapter 7 Bankruptcy

Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Chapter 7 Bankruptcy Carloan.Guidemechanic.com

Navigating life after Chapter 7 bankruptcy can feel like starting a new chapter, often with a clean slate but also with significant challenges, especially when it comes to major financial commitments like buying a car. The thought of getting a car loan during Chapter 7 or shortly after discharge might seem daunting, even impossible, to many. However, based on my experience as a financial expert and working with countless individuals, I can confidently tell you it’s not only possible but also a crucial step towards rebuilding your financial future.

This isn’t just about getting a car; it’s about reclaiming your independence, improving your daily life, and strategically leveraging a car loan as a powerful tool to re-establish your creditworthiness. In this super comprehensive guide, we’ll demystify the process, equip you with the knowledge, and provide actionable strategies to secure the car financing you need, even with a recent Chapter 7 discharge on your record. Let’s drive into the details.

Driving Forward: Your Comprehensive Guide to Getting a Car Loan After Chapter 7 Bankruptcy

The Aftermath of Chapter 7: Understanding Its Impact on Car Loans

Chapter 7 bankruptcy, often referred to as "liquidation bankruptcy," offers a fresh start by discharging most unsecured debts. While it provides immense relief, it also leaves a significant mark on your credit report, typically remaining for up to 10 years. This immediate credit score drop is the primary reason why lenders view post-bankruptcy applicants with heightened caution.

Lenders assess risk, and a recent bankruptcy signals a history of financial distress. They might perceive you as a higher risk borrower, leading to initial skepticism. However, what many don’t realize is that for some lenders, a Chapter 7 discharge can actually be seen in a unique light: you’re no longer burdened by old debts, making your disposable income potentially more stable.

The Two Sides of the Chapter 7 Coin for Lenders

On one hand, your credit score has taken a hit, indicating past financial difficulties. This naturally raises a red flag for traditional lenders who rely heavily on credit scores to gauge reliability. They might worry about your ability to manage new debt responsibly.

On the other hand, a Chapter 7 discharge means you’ve legally shed most of your previous financial obligations. You’re effectively debt-free from those old accounts, which can be an attractive prospect for specialized lenders. These lenders understand that your financial slate is cleaner, and you’re less likely to file for bankruptcy again in the immediate future. This makes you a potentially more stable borrower for new, manageable debt.

The Myth vs. Reality: Can You Really Get a Car Loan After Chapter 7?

Let’s address the elephant in the room directly: Yes, you can absolutely get a car loan after Chapter 7 bankruptcy. This isn’t a myth; it’s a reality that thousands of people experience every year. The key difference lies in how you approach it and what you should expect.

The notion that you’re blacklisted from borrowing for a decade is simply false. While the process might be different and initially more challenging than for someone with pristine credit, the doors to auto financing are not closed. Many lenders specialize in helping individuals rebuild their credit after bankruptcy.

However, it’s crucial to set realistic expectations. You likely won’t qualify for the lowest interest rates or the most luxurious vehicles right away. Your first post-bankruptcy car loan is primarily a tool for rebuilding, not for indulgence. It’s about demonstrating renewed financial responsibility.

Setting Realistic Expectations for Your First Post-Bankruptcy Loan

Expect higher interest rates than what someone with excellent credit would receive. This is the lender’s way of mitigating the increased risk they’re taking on. Don’t be discouraged by this; view it as a necessary step. The goal is to get a manageable loan, make timely payments, and then potentially refinance at a lower rate down the line.

Also, prepare for potentially stricter loan terms. This might include a requirement for a larger down payment or a shorter loan term to reduce the overall risk for the lender. Being prepared for these conditions will help you approach the process with confidence and clarity.

Timing is Everything: When to Apply for a Car Loan After Chapter 7

The timing of your car loan application after Chapter 7 can significantly influence your chances of approval and the terms you receive. While it’s technically possible to apply immediately after your discharge, there’s often a "sweet spot" that yields better results.

Applying too soon might mean your credit report hasn’t had enough time to reflect any positive changes you’ve started making. Waiting a little while allows you to demonstrate some renewed financial stability and responsibility, which lenders appreciate.

The "Sweet Spot": 6 Months to a Year Post-Discharge

Based on my experience, waiting approximately 6 months to a year after your Chapter 7 discharge can be highly beneficial. During this period, you can take proactive steps to start rebuilding your credit and demonstrate responsible financial habits. This gives lenders more positive data points to consider beyond just the bankruptcy filing.

This waiting period isn’t about sitting idly. It’s about actively preparing yourself for a successful loan application. It allows you to build a small financial cushion, establish new credit accounts, and prove that the bankruptcy was a one-time event, not a pattern of behavior.

Why Waiting Can Improve Your Odds and Terms

Waiting allows your credit score to begin its slow climb upward. Even small improvements can make a difference in a lender’s perception. More importantly, it gives you time to build a positive payment history on any new credit accounts you’ve opened, such as a secured credit card or a credit builder loan.

Furthermore, a slightly longer post-bankruptcy period shows lenders that you’ve had time to adjust to your new financial situation. It demonstrates that you’re managing your finances effectively without the burden of past debts, making you a more attractive candidate for new credit.

Rebuilding Your Financial Foundation: Essential Steps Before Applying

Before you even think about stepping onto a car lot or filling out a loan application, it’s crucial to lay a strong financial foundation. This preparation phase is where you actively work to improve your financial standing and present yourself as a reliable borrower. Skipping these steps can severely hinder your chances of approval or lead to unfavorable loan terms.

Think of this as preparing your financial resume. You want to highlight all the positive changes you’ve made since your bankruptcy discharge. This proactive approach shows lenders you’re serious about managing your money responsibly.

1. Credit Monitoring and Report Review

Your credit report is your financial history, and it’s imperative that it’s accurate. Obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and meticulously review them for any errors. Ensure that all discharged debts are correctly listed as such.

Dispute any inaccuracies immediately. An error on your report, no matter how small, could negatively impact your credit score and your loan application. This step ensures lenders are seeing the most accurate reflection of your financial situation.

2. Establishing New, Positive Credit

This is perhaps the most critical step in your post-bankruptcy credit rebuilding journey. Lenders want to see a history of recent, responsible borrowing. Since your old accounts were discharged, you need to start fresh.

Consider opening a secured credit card. With this type of card, you deposit a sum of money, which becomes your credit limit. Use it for small, regular purchases and pay the balance in full and on time every month. This demonstrates responsible credit usage without taking on significant risk.

Another excellent option is a credit builder loan. These loans are designed specifically to help you establish or rebuild credit. You make regular payments into a locked savings account, and once the loan term is complete, you receive the money. Both options report your payment history to credit bureaus, positively impacting your score over time.

3. Creating and Sticking to a Realistic Budget

A solid budget is the bedrock of financial stability. After bankruptcy, it’s more important than ever to know exactly where your money is going. Create a detailed budget that tracks all your income and expenses. This will help you identify how much you can realistically afford for a car payment, insurance, fuel, and maintenance.

Sticking to your budget demonstrates financial discipline. When lenders see a stable income and controlled expenses, it reassures them that you have the capacity to manage new debt without overextending yourself. Pro tips from us: Factor in all car-related expenses, not just the loan payment.

4. Building a Down Payment and Emergency Savings

A significant down payment is one of the most powerful tools you have when getting a car loan during Chapter 7 or after. It reduces the amount you need to borrow, thereby lowering your monthly payments and the overall interest paid. More importantly, it signals to lenders that you’re financially committed to the purchase and have the discipline to save.

Lenders view a substantial down payment as a direct reduction of their risk. It shows you have skin in the game. Furthermore, building an emergency fund is crucial. This fund acts as a buffer against unexpected expenses, preventing you from missing car payments if an unforeseen event occurs. Common mistakes to avoid are neglecting to save and jumping into a loan without a financial cushion.

The Application Process: Navigating Lenders After Chapter 7

Once you’ve diligently prepared your financial foundation, it’s time to approach lenders. This stage requires a strategic mindset and an understanding of which types of lenders are most likely to work with you. Not all lenders are created equal when it comes to post-bankruptcy financing.

1. Identifying the Right Lenders

Traditional banks may be hesitant, but many lenders specialize in subprime auto loans or work with borrowers rebuilding their credit.

- Subprime Lenders: These financial institutions specifically cater to individuals with lower credit scores or challenging credit histories, including bankruptcy. They understand the nuances of post-bankruptcy financing.

- Credit Unions: Often more flexible and community-focused than large banks, credit unions may be more willing to work with members who have faced bankruptcy, especially if you have an existing relationship.

- Dealerships with Special Finance Departments: Many car dealerships have dedicated finance departments that work with a network of lenders, including those who specialize in subprime loans. They can often match you with a lender willing to approve your application.

- Buy Here Pay Here (BHPH) Dealerships: While an option, proceed with caution. BHPH lots finance cars directly, often without traditional credit checks. However, they typically charge very high interest rates and their reporting to credit bureaus can be inconsistent. Use them as a last resort.

2. Gathering Necessary Documentation

Be prepared to provide comprehensive documentation to support your application. This includes:

- Proof of Identity: Driver’s license, social security card.

- Proof of Income: Recent pay stubs (last 2-3 months), tax returns if self-employed, bank statements. Lenders need to verify you have a stable income to make payments.

- Proof of Residence: Utility bills, lease agreement, mortgage statements.

- Chapter 7 Discharge Papers: This is critical. It shows that your bankruptcy is complete and you’re legally free from previous debts.

- Proof of Insurance: You’ll need this before driving off the lot.

- References: Sometimes required, especially for subprime loans.

Having all these documents organized and ready will streamline the application process and demonstrate your preparedness.

3. The Power of a Down Payment

As mentioned, a down payment is your secret weapon. The more you put down, the less you need to borrow, and the less risk the lender assumes. This significantly increases your chances of approval and can lead to more favorable terms. Aim for at least 10-20% of the car’s purchase price, if possible.

Based on my experience, a solid down payment often makes the difference between an approval and a denial for post-bankruptcy applicants. It shows commitment and reduces the loan-to-value ratio, which lenders love.

4. Considering a Co-signer

If you have a trusted family member or friend with good credit who is willing to co-sign your loan, this can dramatically improve your chances of approval and potentially secure a lower interest rate. A co-signer’s creditworthiness acts as a guarantee for the lender.

However, understand the implications for your co-signer. They are equally responsible for the debt, and any missed payments will negatively impact their credit. Only consider this option if you are absolutely confident in your ability to make all payments on time.

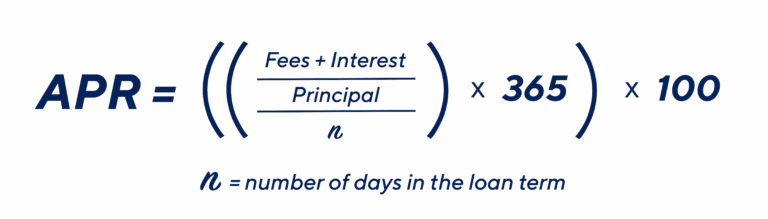

5. Understanding Interest Rates

Prepare for higher interest rates initially. This is a reality for anyone getting a car loan during Chapter 7 or with a low credit score. These rates reflect the increased risk lenders take. Focus on securing a manageable payment and demonstrating consistent on-time payments.

Your primary goal for this first loan is to rebuild your credit, not necessarily to get the lowest rate. With diligent payments, you can improve your credit score and potentially refinance to a lower rate in 12-18 months.

Strategies for a Successful Car Loan Application

Beyond the foundational steps, there are specific strategies you can employ during the application process to maximize your success. These tips are designed to make you a more attractive borrower in the eyes of lenders.

1. Know Your Affordability Limit

Before you even start looking at cars, determine your absolute maximum affordable monthly payment, including insurance, fuel, and maintenance. Don’t let a salesperson talk you into a car that stretches your budget too thin. Overextending yourself now could lead to financial distress again.

Pro tips from us: Use an online car loan calculator to factor in different interest rates and loan terms. This will give you a clear picture of what you can comfortably afford.

2. Get Pre-Approved First

Instead of walking into a dealership and letting them run multiple credit inquiries (which can further ding your credit score), try to get pre-approved from a few different lenders beforehand. This allows you to shop for financing independently and gives you leverage at the dealership.

Pre-approval tells you how much you can borrow and at what interest rate, transforming you into a cash buyer in the eyes of the dealership. This puts you in a stronger negotiating position for the car’s price.

3. Choose the Right Car (Sensibly)

Resist the temptation for a brand new, expensive car. Focus on a reliable, affordable, and practical vehicle that meets your needs. A used car, perhaps 2-5 years old, often offers the best value and lower insurance costs.

Remember, this first loan is about rebuilding your credit. A sensible car choice demonstrates financial prudence to lenders and ensures your monthly payments are manageable.

4. Thoroughly Review Your Credit Report (Again)

Before submitting any final applications, pull your credit reports one last time. Ensure there are no new errors and that your recent positive credit activity (secured card payments, etc.) is being reported accurately. This final check can prevent unexpected issues.

5. Be Honest and Transparent with Lenders

When discussing your financial situation, be upfront about your Chapter 7 discharge. Lenders appreciate honesty and transparency. Explain briefly how you’ve addressed your past financial issues and what steps you’ve taken to rebuild.

This open communication can help build trust. Lenders are often more willing to work with someone who is candid about their financial history and demonstrates a clear path forward.

6. Negotiate Wisely

When it comes to negotiation, focus on the total cost of the loan, not just the monthly payment. High interest rates can inflate the total cost significantly. Also, be wary of add-ons and extended warranties that might not be necessary.

If you have a pre-approval, use it as leverage. If the dealership can beat your pre-approved rate, fantastic! If not, you have a solid offer to fall back on.

Common Pitfalls to Avoid When Seeking a Post-Chapter 7 Car Loan

While the path to a car loan after Chapter 7 is navigable, there are common mistakes that can derail your efforts or lead to a less favorable outcome. Being aware of these pitfalls can help you steer clear of them.

1. Falling for High-Pressure Sales Tactics

Some dealerships might try to rush you into a deal or push you towards a car that’s outside your budget. Don’t succumb to pressure. Take your time, read all paperwork carefully, and don’t sign anything you don’t fully understand or agree with.

Common mistakes to avoid are feeling obligated to buy on the first visit or believing that "today only" deals are your only chance.

2. Ignoring the Total Cost of the Loan

As mentioned, don’t just focus on the monthly payment. A low monthly payment spread over a very long term with a high interest rate can result in you paying significantly more for the car than it’s worth. Always calculate the total amount you will pay over the life of the loan.

3. Co-signing for Others (After Your Own Bankruptcy)

While a co-signer can help you, avoid co-signing for someone else, especially while you are actively rebuilding your own credit. Taking on responsibility for someone else’s debt can put your own fragile financial recovery at risk.

4. Taking on Too Much Debt Too Soon

Your goal is to rebuild credit responsibly, not to accumulate new debt. Be conservative with your loan amount. Don’t borrow more than you absolutely need or can comfortably afford. A second bankruptcy is far more damaging and harder to recover from.

Long-Term Benefits: Using Your Car Loan to Rebuild Credit

The car loan you secure after Chapter 7 is more than just a means of transportation; it’s a powerful tool for credit rebuilding. By managing this loan responsibly, you can significantly improve your credit score and open doors to better financial opportunities in the future.

1. Consistent On-Time Payments

This is the golden rule of credit rebuilding. Every single on-time payment you make on your car loan will be reported to the credit bureaus. A consistent history of timely payments demonstrates reliability and financial responsibility, which are key factors in calculating your credit score.

This positive payment history will slowly but surely overshadow the negative impact of the bankruptcy over time.

2. Impact on Your Credit Score

As you make regular, on-time payments, you’ll see your credit score steadily increase. This improvement will make you eligible for better interest rates on future loans, whether it’s for another car, a mortgage, or even a personal loan.

It’s a virtuous cycle: responsible borrowing leads to a better credit score, which leads to more favorable borrowing terms.

3. Opportunities for Refinancing

After 12-18 months of consistent on-time payments, your credit score will likely have improved significantly. At this point, you may qualify to refinance your car loan at a lower interest rate. Refinancing can save you a substantial amount of money over the remaining life of the loan.

Shop around for refinancing options, just as you did for your initial loan. This is a tangible reward for your diligence and a clear sign of your financial progress. For more insights on how to proactively manage and improve your credit score, you might find our article on helpful.

Conclusion: Driving Towards a Brighter Financial Future

Getting a car loan during Chapter 7 or shortly after discharge is not just a possibility; it’s a pivotal step on your journey to financial recovery. While the road may have a few bumps, with careful planning, strategic execution, and a commitment to responsible financial habits, you can absolutely secure the financing you need.

Remember, your first post-bankruptcy car loan is an opportunity to prove your creditworthiness and demonstrate your ability to manage debt responsibly. Embrace the process, educate yourself, and be patient. Every on-time payment is a step forward, rebuilding your credit score and paving the way for a more stable and prosperous financial future. For more general guidance on navigating life after bankruptcy, consider exploring resources like to understand legal frameworks and consumer rights.

You have the power to turn a challenging situation into a powerful comeback story. Drive forward with confidence!