Driving Forward: Your Comprehensive Guide to Securing a Car Loan While In Chapter 13 Bankruptcy

Driving Forward: Your Comprehensive Guide to Securing a Car Loan While In Chapter 13 Bankruptcy Carloan.Guidemechanic.com

Navigating life under Chapter 13 bankruptcy can feel like walking a tightrope. Every financial decision, big or small, comes under scrutiny, and for good reason. Your repayment plan is designed to help you regain control, but what happens when an essential need like reliable transportation arises? Can you get a car loan while still in Chapter 13? The answer, while not a simple yes, is definitively yes, it is possible.

Based on my extensive experience in financial guidance and SEO content creation, I understand the unique challenges and opportunities that exist for individuals in your situation. This isn’t just about finding a lender; it’s about understanding the entire process, from legal requirements to practical strategies, to ensure you make an informed decision that supports your long-term financial recovery.

Driving Forward: Your Comprehensive Guide to Securing a Car Loan While In Chapter 13 Bankruptcy

This super comprehensive guide will walk you through every critical step, shedding light on how to secure car loans for people in Chapter 13. We’ll cover everything from consulting your attorney to finding the right lender and navigating court approvals. Our ultimate goal is to provide you with the knowledge and confidence to drive forward, even with the complexities of bankruptcy.

Understanding Chapter 13 Bankruptcy: A Quick Overview

Before diving into car loans, it’s crucial to grasp what Chapter 13 bankruptcy entails. Unlike Chapter 7, which often involves liquidation of assets, Chapter 13 is a reorganization bankruptcy. It allows individuals with regular income to keep their property while repaying all or a portion of their debts over a period of three to five years.

During this time, you operate under a strict repayment plan approved by the bankruptcy court and overseen by a trustee. This plan dictates your monthly payments to creditors. The very nature of this structured plan means that any new significant debt, such as a car loan, must be carefully considered and typically approved by the court.

The court’s primary concern is to ensure that any new financial obligation does not jeopardize your ability to complete your Chapter 13 repayment plan. This is why securing new credit during this period requires a specific legal process and careful planning.

The Unique Challenge: Why Car Loans in Chapter 13 Are Different

Getting a car loan when you’re in Chapter 13 isn’t like applying for a loan with good credit. Several factors make it a distinct process, primarily due to the ongoing bankruptcy proceedings and the watchful eye of the court.

Firstly, your finances are under court supervision. This means you can’t simply take on new debt without permission. Every dollar you earn and every significant financial commitment you make is part of your approved repayment plan. Introducing a new car payment directly impacts your disposable income and your ability to adhere to that plan.

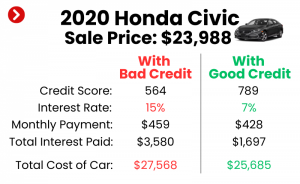

Secondly, lenders perceive you as a higher risk. While Chapter 13 demonstrates a commitment to repaying debts, your credit report still reflects the bankruptcy filing. This often translates to higher interest rates and stricter approval criteria from potential lenders. They need to be confident you can manage the new payment alongside your existing obligations.

Lastly, the involvement of your bankruptcy trustee and the court adds an extra layer of bureaucracy. You’ll need to file a "Motion to Incur Debt" and obtain court approval before any new car loan can be finalized. This legal step is designed to protect both you and your creditors, ensuring the new debt is necessary and affordable.

When Do You Need a Car Loan During Chapter 13?

Life doesn’t stop because you’re in Chapter 13. Unexpected situations can arise where a car loan becomes an absolute necessity. Understanding these common scenarios can help you build a stronger case for approval.

Perhaps your existing vehicle, which was part of your bankruptcy filing, has broken down beyond repair. Or maybe you didn’t own a car when you filed, and now you need reliable transportation for work, school, or medical appointments. In some unfortunate cases, a car might have been repossessed, leaving you stranded.

Whatever the reason, the need for a functioning vehicle is often non-negotiable for maintaining employment and managing daily life. The court and your trustee generally understand this, provided you can demonstrate a genuine need and a feasible plan for repayment.

The Essential Steps to Getting a Car Loan While in Chapter 13

Securing a car loan during Chapter 13 is a multi-step process that requires careful attention to detail and collaboration with legal and financial professionals. Skipping any of these steps can lead to delays or outright denial.

Step 1: Consult Your Bankruptcy Attorney – Your First and Most Crucial Move

This cannot be stressed enough: your bankruptcy attorney is your primary resource and the first person you should speak with. Do not approach lenders or dealerships before discussing your situation with your lawyer.

Your attorney understands the intricacies of your specific Chapter 13 plan, local court rules, and the preferences of your trustee. They will advise you on the feasibility of obtaining a loan, guide you through the required legal procedures, and help you prepare the necessary paperwork. Based on my experience, attempting to navigate this process alone is a common mistake that often leads to frustration and wasted time.

They will also help you determine how a new car payment might impact your existing repayment plan and what modifications, if any, might be needed. This initial consultation sets the foundation for a successful application.

Step 2: Understand the "Motion to Incur Debt"

Once your attorney confirms that pursuing a car loan is a viable option, the next critical step is filing a "Motion to Incur Debt" with the bankruptcy court. This is a formal request asking the judge to approve your ability to take on new financing.

The motion will outline several key pieces of information. It will detail your current income and expenses, explain the necessity of the vehicle, and present the proposed terms of the car loan (e.g., amount, interest rate, monthly payment, and the vehicle you intend to purchase). The court needs to be convinced that the new debt is necessary, affordable, and will not jeopardize your Chapter 13 plan.

Pro tips from us: The more thoroughly you and your attorney prepare this motion, the smoother the approval process will be. Include as much supporting documentation as possible to demonstrate your need and your capacity to pay.

Step 3: Finding the Right Lender

Not all lenders are equipped or willing to provide car loans for people in Chapter 13. You’ll need to focus your search on specialized lenders who work with individuals in bankruptcy or those with subprime credit.

These lenders understand the unique legal requirements and risks involved. You might find them through online search platforms specializing in bad credit auto loans, or through dealerships that have specific programs for bankruptcy clients. Avoid simply walking into any dealership and applying, as multiple hard inquiries can further impact your credit score.

Common mistakes to avoid are applying with too many lenders at once or falling for "guaranteed approval" scams. Instead, seek out lenders who offer pre-qualification options, which can give you an idea of potential terms without a hard credit pull. Your attorney might also have recommendations for reputable lenders they’ve worked with in the past.

Step 4: Preparing Your Application

Once you’ve identified a potential lender and received pre-approval, you’ll need to gather a comprehensive set of documents for your full application. Organization is key here to demonstrate your reliability.

This typically includes proof of income (recent pay stubs, tax returns), proof of residence (utility bills, lease agreement), and all your bankruptcy paperwork, including your Chapter 13 plan and your attorney’s contact information. You’ll also need to clearly articulate why the car is necessary for you.

Lenders want to see stability and a clear understanding of your financial situation. Having all your documents neatly organized and readily available will make the application process much more efficient and professional.

Step 5: Court Approval and Loan Closing

After your application is complete and the lender has given you a conditional offer, your attorney will present the Motion to Incur Debt to the bankruptcy court. A hearing may be scheduled where you, your attorney, and sometimes the trustee, will discuss the necessity and affordability of the loan.

If the judge approves the motion, you’ll receive a court order allowing you to proceed with the loan. This order is a crucial document that you will provide to your lender. Only then can you finalize the loan agreement and take possession of your new vehicle.

It’s a process that requires patience, but following these steps diligently significantly increases your chances of a positive outcome.

What Lenders Look For (and How to Prepare)

When evaluating car loans for people in Chapter 13, lenders focus on a few key areas to assess risk. Understanding these can help you better prepare and present yourself as a reliable borrower.

Proof of Income & Stability

Lenders want to see a steady, verifiable source of income that is sufficient to cover both your Chapter 13 plan payments and the proposed new car loan payment. They’ll scrutinize your employment history and income stability.

To prepare, ensure you have several recent pay stubs, W-2s, or tax returns if you’re self-employed. If your income has recently changed, be ready to explain the circumstances. A stable job history demonstrates your ability to generate income consistently.

Affordability: Your Debt-to-Income Ratio

The new car payment absolutely must not jeopardize your ability to complete your Chapter 13 plan. Lenders, and more importantly, the court and your trustee, will carefully analyze your budget. They want to see that your debt-to-income ratio (DTI) remains manageable with the added car payment.

You and your attorney should calculate your post-loan DTI before even applying. This proactive step ensures you’re looking for a vehicle that genuinely fits within your approved budget. Be realistic about what you can afford.

Reasonable Loan Terms

While interest rates for individuals in Chapter 13 are typically higher due to the increased risk, lenders still want to see reasonable loan terms. This means avoiding excessively long repayment periods (which can lead to negative equity) or interest rates that seem predatory.

Focus on a loan that offers the best possible terms for your situation, understanding that "best" in this context might still mean higher than average. A shorter loan term with slightly higher payments, if affordable, is often preferable in the long run.

Down Payment

Making a down payment, even a modest one, significantly increases your chances of approval. A down payment reduces the amount you need to finance, lowers your monthly payments, and demonstrates your commitment to the loan.

It also reduces the lender’s risk, as you’ll have instant equity in the vehicle. If you have any available funds (approved by your attorney and trustee), using them for a down payment is a very smart strategy.

Necessity

Lenders and the court need to understand why you need this vehicle. Is it for work? Medical appointments? Transporting children to school? A clear, well-articulated explanation of necessity can weigh heavily in your favor.

Document any specific requirements, such as a longer commute or the need for a larger vehicle for family. The more compelling your case for necessity, the better.

Maximizing Your Chances of Approval

Securing car loans for people in Chapter 13 requires strategic planning and a realistic approach. Here are some pro tips to help you maximize your chances of getting approved.

- Be Realistic About Your Vehicle Choice: This is not the time to buy a luxury car. Focus on reliable, affordable, and practical transportation. A modest, well-maintained used car is often the most sensible choice and easier to get approved for.

- Build a Strong Case for Necessity: As mentioned, clearly articulate and document why this car is essential. Your attorney will help you present this effectively in your motion.

- Offer a Down Payment: Even a small down payment of 5-10% can make a significant difference. It shows commitment and reduces the loan amount.

- Maintain Your Chapter 13 Payments: Your payment history on your existing Chapter 13 plan is a powerful indicator of your financial responsibility. Consistent, on-time payments demonstrate to both your trustee and potential lenders that you are serious about meeting your obligations.

- Shop Smart for the Car: Research reliable used car models that fit your budget. Knowing the fair market value of the car you intend to buy helps ensure you’re not overpaying, which is another factor the court considers.

- Understand Your Budget Thoroughly: Don’t just consider the car payment. Factor in insurance, fuel costs, maintenance, and registration fees. These additional expenses must also fit within your approved budget.

Based on my experience, the more prepared and realistic you are, the smoother the process will be. Lenders and courts appreciate borrowers who have done their homework and present a clear, viable plan.

Common Pitfalls and How to Avoid Them

Even with the best intentions, individuals seeking car loans for people in Chapter 13 can stumble. Being aware of these common mistakes can help you steer clear of them.

- Applying for Too Much Car: This is perhaps the most frequent error. Overestimating what you can afford or trying to purchase a vehicle that is deemed excessive by the court will likely lead to denial. Stick to what is truly necessary and affordable.

- Not Consulting Your Attorney First: As highlighted, this is a non-negotiable first step. Making moves without your lawyer’s guidance can complicate your bankruptcy case and delay or prevent loan approval.

- Accepting Predatory Loan Terms: Because you are considered a higher risk, some lenders might offer loans with extremely high interest rates or unfavorable terms. Work with your attorney to scrutinize all loan offers and ensure they are reasonable and sustainable.

- Not Understanding the Full Cost: Beyond the monthly payment, remember to factor in insurance, maintenance, and fuel. These can quickly add up and strain your budget if not properly accounted for.

- Missing Court Dates or Not Providing Required Documentation: The legal process requires punctuality and thoroughness. Missing deadlines or failing to provide necessary documents can cause significant delays or even outright denial of your motion.

The Benefits Beyond Transportation: Rebuilding Your Credit

While the immediate goal is reliable transportation, securing and successfully managing a car loan while in Chapter 13 offers a significant long-term benefit: it can help you rebuild your credit.

Making timely payments on a new car loan, even one approved during bankruptcy, demonstrates to credit bureaus that you are capable of handling new credit responsibly. Each on-time payment can contribute positively to your credit score, laying a foundation for improved financial health post-bankruptcy. This is a powerful step towards a stronger financial future.

(This is a placeholder for an internal link to a hypothetical article on the blog about credit rebuilding.)

Life After the Loan: Managing Your Payments

Once you’ve secured your car loan and driven off the lot, the real work of financial discipline continues. Managing your new car payments alongside your Chapter 13 plan payments is crucial for your long-term success.

- Prioritize Payments: Ensure both your Chapter 13 trustee payment and your car loan payment are made on time, every time. Missing payments can have severe consequences, impacting both your bankruptcy plan and your credit score.

- Set Up Reminders: Use calendar alerts, banking apps, or other tools to remind you of upcoming payment due dates.

- Communicate with Your Lender: If you foresee any difficulty in making a payment, contact your car loan lender immediately. Open communication is always better than simply missing a payment.

- Automate Payments: If possible and comfortable, set up automatic payments from your bank account. This minimizes the risk of missing a due date and helps you stay consistent.

Pro tips from us: Treat your car loan as an investment in your financial future. Each successful payment brings you closer to completing your Chapter 13 plan and establishing a stronger credit profile.

Frequently Asked Questions

Q: Can I get a brand new car during Chapter 13?

A: While technically possible, it’s generally more challenging to get approval for a brand new vehicle. Courts and trustees usually prefer you purchase a reliable, affordable used car to minimize the debt incurred and ensure it doesn’t strain your repayment plan.

Q: How long does the approval process take?

A: The timeline can vary depending on your court’s schedule, your attorney’s efficiency, and the responsiveness of the lender. It can take anywhere from a few weeks to a couple of months from the initial consultation to finalizing the loan.

Q: What if my trustee or the judge denies my motion?

A: If your motion is denied, your attorney will review the reasons for the denial. It might be possible to amend the motion, seek a different car, or adjust the proposed loan terms and resubmit. It’s important not to get discouraged but to work with your attorney on the next steps.

For official information on bankruptcy procedures and legal guidelines, you can visit trusted sources like the U.S. Courts website.

Conclusion: Driving Towards a Brighter Financial Future

Securing car loans for people in Chapter 13 is undoubtedly a complex process, but it is far from impossible. With the right knowledge, preparation, and professional guidance, you can navigate the legal and financial hurdles to obtain the reliable transportation you need.

Remember, the journey begins with your bankruptcy attorney. Their expertise is invaluable in understanding your specific situation and guiding you through the intricate steps of filing a Motion to Incur Debt and securing court approval. By being realistic, organized, and persistent, you can not only get a car loan but also take a significant step towards rebuilding your credit and achieving your financial goals.

Don’t let the challenges of Chapter 13 deter you from addressing essential needs. With careful planning and a strategic approach, you can drive forward with confidence towards a brighter, more stable financial future. We encourage you to share this comprehensive guide with anyone who might benefit from this information.