Driving Forward: Your Comprehensive Guide to Securing a Car Loan with an Open Chapter 13 Bankruptcy

Driving Forward: Your Comprehensive Guide to Securing a Car Loan with an Open Chapter 13 Bankruptcy Carloan.Guidemechanic.com

Life throws unexpected curveballs, and sometimes, navigating them means making difficult financial decisions like filing for Chapter 13 bankruptcy. While this process offers a path to financial reorganization, it often brings a new set of challenges – one of the most pressing being the need for reliable transportation. Many assume that getting a car loan with an active Chapter 13 is impossible, but based on my experience, that’s simply not true. It requires a specific approach, understanding, and the right guidance.

This in-depth guide is designed to demystify the process of securing a car loan while you’re still in an open Chapter 13 bankruptcy. We’ll explore everything from understanding your bankruptcy plan to navigating court approvals and finding the right lender. Our goal is to provide you with the knowledge and confidence to drive forward, literally and figuratively, toward your financial recovery.

Driving Forward: Your Comprehensive Guide to Securing a Car Loan with an Open Chapter 13 Bankruptcy

Understanding Chapter 13 Bankruptcy: A Foundation for Your Car Loan Journey

Before diving into car loans, it’s essential to grasp what Chapter 13 bankruptcy entails. Unlike Chapter 7, which often involves the liquidation of assets, Chapter 13 is a reorganization bankruptcy. It allows individuals with regular income to develop a plan to repay all or part of their debts over a period of three to five years. During this time, you make scheduled payments to a bankruptcy trustee, who then distributes these funds to your creditors.

This structured repayment plan provides a shield from creditors, offering a chance to catch up on missed payments and regain financial stability. However, while you’re under the protection of the bankruptcy court, your financial decisions, particularly incurring new debt, are subject to court oversight. This oversight is precisely why getting a car loan during an open Chapter 13 requires a different pathway than a standard application.

Your ongoing repayment plan is the central piece of your financial puzzle during Chapter 13. Every new financial commitment, like a car loan, must fit within the framework of this plan and not jeopardize your ability to make your scheduled bankruptcy payments. The court’s primary concern is the successful completion of your bankruptcy, ensuring creditors receive what they’re owed according to the plan.

Why Securing a Car Loan During Chapter 13 Is Unique

Applying for a car loan when you have an open Chapter 13 bankruptcy isn’t like walking into any dealership and picking out a vehicle. The key difference lies in the mandatory requirement for court approval. Because your financial affairs are under the supervision of the bankruptcy court, you cannot simply incur new significant debt without their permission. This is a critical safeguard designed to protect both you and your creditors.

Lenders also view open bankruptcy cases with a degree of caution. You’re considered a higher risk because of your past financial struggles and the ongoing legal process. However, many specialized lenders recognize that people in Chapter 13 are often highly motivated to rebuild their credit and are making consistent payments to the trustee, which can indicate financial responsibility. This makes them a viable, albeit unique, borrower segment.

The involvement of your bankruptcy trustee is another distinguishing factor. The trustee plays a crucial role in reviewing your request to incur new debt. They act as an impartial party, ensuring that any new car loan is necessary, affordable, and won’t derail your existing bankruptcy plan. Their recommendation is often pivotal in the court’s final decision.

The Step-by-Step Process: Your Roadmap to a Chapter 13 Car Loan

Navigating the path to a car loan with an open Chapter 13 can seem daunting, but by breaking it down into manageable steps, it becomes much clearer. Here’s a comprehensive roadmap to guide you:

Step 1: Assess Your True Need and Financial Budget

Before you even think about looking at cars, you need to conduct an honest self-assessment. Why do you need a car? Is it for essential transportation to work, medical appointments, or to care for your family? Or is it a desire for an upgrade or a luxury item? The court is far more likely to approve a loan for essential transportation than for a discretionary purchase.

Next, and perhaps most critically, determine what you can realistically afford. This isn’t just about the monthly car payment. Factor in insurance, fuel, maintenance, and potential repair costs. Remember, these new expenses must fit comfortably within your existing budget without jeopardizing your Chapter 13 payments. Being overly ambitious here is a common mistake that can lead to denial or further financial strain.

Consider making a down payment if at all possible. Even a modest down payment can significantly improve your chances of approval, reduce the loan amount, and potentially lower your interest rate. It signals to both the lender and the court that you’re serious about this commitment and have some financial stability.

Step 2: The Most Critical Hurdle – Obtaining Court and Trustee Approval

This is the non-negotiable step. You must get permission from the bankruptcy court to take on new debt. Attempting to get a car loan without this approval can lead to severe consequences, including the dismissal of your bankruptcy case. Your bankruptcy attorney is your most valuable asset here.

Your attorney will file a "Motion to Incur Debt" with the bankruptcy court. This motion will outline the necessity of the car, the proposed loan terms, the vehicle details (make, model, year, VIN, purchase price), and how the new payment will fit into your existing budget. You’ll likely need to provide proof of income, your current Chapter 13 plan, and details of your proposed car purchase.

The bankruptcy trustee will review your motion carefully. They’ll scrutinize the purchase price, interest rate, and monthly payment to ensure they are reasonable and won’t negatively impact your ability to complete your Chapter 13 plan. The trustee’s recommendation carries significant weight with the judge, so presenting a well-reasoned, affordable plan is crucial. Common reasons for denial include an overly expensive vehicle, an exorbitant interest rate, or an inability to demonstrate the necessity of the purchase.

Step 3: Finding the Right Lender Specializing in Bankruptcy Loans

Not all lenders are equipped or willing to work with individuals in an open Chapter 13 bankruptcy. You’ll need to seek out specialized lenders who understand the unique legal landscape involved. These often include subprime auto lenders, some credit unions, and dealerships with dedicated "special finance" departments.

Online platforms can also be a good starting point, as many specialize in connecting borrowers with challenging credit histories to appropriate lenders. When researching, look for lenders who explicitly mention their experience with Chapter 13 bankruptcy. Don’t waste your time with mainstream banks or lenders who aren’t familiar with the court approval process.

When you engage with potential lenders, be upfront about your Chapter 13 status. Transparency is key. They will need to understand that court approval is pending and that the loan cannot be finalized until that approval is secured. A lender who tries to circumvent this process should be avoided, as they may not be reputable.

Step 4: Understanding and Negotiating Loan Terms and Conditions

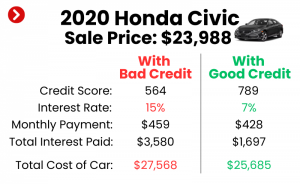

Given the higher perceived risk, expect interest rates on a Chapter 13 car loan to be higher than what someone with excellent credit would receive. This is standard practice in subprime lending. However, this doesn’t mean you should accept the first offer you receive without question. Shop around and compare offers from multiple lenders.

Pay close attention to all aspects of the loan: the annual percentage rate (APR), the loan term (length of the repayment period), and any associated fees. Shorter loan terms might mean higher monthly payments but less interest paid over the life of the loan. Longer terms reduce monthly payments but increase the total interest. Weigh these factors carefully against your budget and the court’s likely approval.

Pro tips from us: Be wary of excessive fees or add-ons that significantly inflate the loan amount. While gap insurance or extended warranties might be offered, evaluate their necessity and cost carefully. Always read the fine print thoroughly before agreeing to any terms.

Step 5: Finalizing the Purchase and Vehicle Registration

Once you have secured conditional approval from a lender and, most importantly, obtained the official court order granting permission to incur the debt, you can proceed with the vehicle purchase. Ensure that all the details of the final loan agreement precisely match what was approved by the court. Any discrepancies could cause issues.

The dealership or lender will then finalize the paperwork. The car will be registered in your name, with the lienholder (the lender) noted on the title. Congratulations, you’ve successfully navigated the complex process! Remember to make all your payments on time, both for your car loan and your Chapter 13 plan, to continue rebuilding your financial standing.

Factors Influencing Your Chapter 13 Car Loan Approval

Several elements come into play when the court and lenders evaluate your car loan request. Understanding these can help you strengthen your application:

- Your Bankruptcy Plan’s Status: How far along are you in your Chapter 13 plan? If you’re nearing the end and have a consistent payment history, it demonstrates reliability. If you’ve just started, the court and trustee might be more cautious.

- Income Stability and Debt-to-Income (DTI) Ratio: Lenders and the court need assurance that you have a stable, verifiable income that can comfortably cover the new car payment in addition to your existing Chapter 13 payments and living expenses. Your DTI ratio will be closely examined.

- The Vehicle’s Value and Practicality: The court is less likely to approve a loan for a luxury vehicle. A reasonably priced, reliable car that serves a practical purpose (e.g., getting to work) stands a much better chance. Lenders also prefer vehicles that retain their value, as it reduces their risk.

- Your Down Payment: As mentioned, a down payment is a powerful indicator of your commitment and ability to manage your finances. It also reduces the amount you need to borrow, which can lead to better loan terms.

- Your Bankruptcy Attorney’s Support: An experienced bankruptcy attorney is indispensable. Their ability to present a compelling case to the court and trustee, along with their knowledge of local court preferences, can significantly impact your approval odds.

- Payment History (Pre- and Post-Bankruptcy): While your pre-bankruptcy payment history led to the filing, a consistent and timely payment record during your Chapter 13 plan demonstrates your renewed financial responsibility.

Pro Tips for Success in Getting a Chapter 13 Car Loan

Based on my experience guiding individuals through this process, here are some actionable tips to boost your chances of success:

- Work Hand-in-Hand with Your Bankruptcy Attorney: This cannot be stressed enough. Your attorney is your legal expert and advocate. They understand the nuances of the court system and can advise you on the best approach, prepare the necessary motions, and represent you if needed. Do not try to go it alone.

- Be Realistic About Your Vehicle Choice and Loan Terms: Aim for a practical, reliable, and affordable used car rather than a brand-new luxury model. Accept that your interest rate will likely be higher than prime rates. Your focus should be on getting approved for essential transportation and completing your bankruptcy.

- Shop Around for Both Lenders and Vehicles: Don’t settle for the first offer. Compare interest rates, terms, and fees from several specialized lenders. Similarly, research different car models to find the best value within your approved budget.

- Consider a Co-signer (With Caution): If you have a trusted friend or family member with good credit willing to co-sign, it could significantly improve your loan terms. However, understand that a co-signer is equally responsible for the debt, so ensure both parties are fully aware of the implications.

- Focus on Affordability Over Desire: The goal here is to secure necessary transportation without jeopardizing your Chapter 13 plan. Every dollar saved on interest or a lower monthly payment contributes to your overall financial health and ability to successfully emerge from bankruptcy.

- Gather All Documents Proactively: Have your proof of income, Chapter 13 plan documents, and any other relevant financial information ready. This speeds up the process for both your attorney and potential lenders.

Common Mistakes to Avoid When Seeking a Car Loan in Chapter 13

Navigating an open bankruptcy is complex, and it’s easy to make missteps. Here are common mistakes to avoid:

- Attempting to Secure a Loan Without Court Approval: This is the biggest and most serious error. As mentioned, it can lead to the dismissal of your bankruptcy case and leave you vulnerable to creditors. Always obtain court approval before finalizing any loan.

- Buying an Overly Expensive or Impractical Car: The court and trustee are looking for necessity and prudence. An expensive car, especially one with a high interest rate, will likely be rejected as it could jeopardize your repayment plan.

- Ignoring Your Attorney’s Advice: Your attorney is there to protect your interests and ensure compliance with bankruptcy law. Disregarding their guidance can lead to delays, denials, or even legal complications.

- Accepting the First Loan Offer Without Comparison: Just because a lender offers you a loan doesn’t mean it’s the best or only offer. Always compare terms, interest rates, and fees to ensure you’re getting a fair deal for your situation.

- Forgetting About the "Total Cost of Ownership": Beyond the monthly payment, a car comes with insurance, fuel, maintenance, and potential repair costs. Failing to budget for these additional expenses can quickly create a new financial burden.

- Being Dishonest or Omitting Information: Transparency is paramount. Providing false or incomplete information to your attorney, the court, or a lender can have severe legal repercussions.

Rebuilding Your Credit While in Chapter 13

Successfully obtaining and managing a car loan during your Chapter 13 bankruptcy is a significant step toward rebuilding your credit. Each on-time payment you make on your car loan, along with your consistent Chapter 13 payments, will be reported to credit bureaus. This demonstrates a renewed sense of financial responsibility and helps to slowly improve your credit score.

While your credit report will still show the bankruptcy, a positive payment history on new debt, especially a secured loan like an auto loan, signals to future lenders that you are capable of managing credit responsibly. This can be invaluable as you complete your Chapter 13 plan and look towards a post-bankruptcy financial life. Continue to monitor your credit report regularly to ensure accuracy and track your progress. Understanding your credit score is vital; learn more in our article: .

Frequently Asked Questions (FAQs) About Car Loans in Open Chapter 13

Let’s address some common questions you might have:

Q: Can I get a new car or only a used car during Chapter 13?

A: While it’s possible to get a loan for a new car, it’s generally much harder to get court approval. New cars depreciate rapidly and are typically more expensive. The court usually prefers a reasonably priced used vehicle that meets your essential transportation needs.

Q: Will my interest rate be very high?

A: Yes, generally, interest rates for car loans during an open Chapter 13 will be higher than for borrowers with excellent credit. This reflects the increased risk lenders perceive. However, shopping around can help you find the most competitive rates available for your situation.

Q: How long does the approval process take?

A: The timeline can vary. Once your attorney files the "Motion to Incur Debt," it typically takes a few weeks to a month or more for the court to review and issue an order, depending on the court’s calendar and whether any objections are filed. Factor this into your planning.

Q: What if my trustee or the court denies my request?

A: If your initial request is denied, it’s usually because the proposed loan terms are deemed too expensive or the car isn’t considered a necessity. Your attorney can help you understand the reasons for denial and advise if you can revise your request with a more affordable vehicle or better loan terms.

Q: Can I refinance my car loan later, after my Chapter 13 is discharged?

A: Absolutely. Once your Chapter 13 is successfully discharged, your credit score will begin to improve more rapidly. You may then be in a much better position to refinance your car loan at a lower interest rate, potentially saving you a significant amount of money over the remaining loan term.

Q: Where can I find more general information about Chapter 13 bankruptcy?

A: For official and comprehensive details on Chapter 13 bankruptcy, you can refer to trusted sources such as the U.S. Courts website. For example, the U.S. Courts’ Bankruptcy Basics provides an excellent overview: .

Driving Towards a Brighter Financial Future

Securing a car loan with an open Chapter 13 bankruptcy is a testament to your resilience and commitment to rebuilding your financial life. While the path is more intricate than a standard loan application, it is absolutely achievable with careful planning, clear communication, and the indispensable guidance of your bankruptcy attorney.

Remember, this process is not just about getting a car; it’s about making a responsible financial decision that supports your overall Chapter 13 plan and paves the way for a stronger financial future. By following these steps, avoiding common pitfalls, and making informed choices, you can successfully navigate this challenge and drive forward with confidence. For more information on managing your finances during bankruptcy, check out our guide on .