Driving Forward: Your Definitive Guide to Navigating Bad Credit Car Loans

Driving Forward: Your Definitive Guide to Navigating Bad Credit Car Loans Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle when your credit score isn’t where you want it to be. Many people facing financial challenges believe that owning a reliable vehicle is simply out of reach. This common misconception, however, often leads to unnecessary frustration and missed opportunities.

The truth is, obtaining a car loan with bad credit is not only possible but can also be a strategic step towards rebuilding your financial future. It requires understanding the process, knowing your options, and approaching the journey with careful planning and realistic expectations. This comprehensive guide will demystify bad credit car loans, providing you with the knowledge and strategies to drive away with a vehicle and a brighter financial outlook.

Driving Forward: Your Definitive Guide to Navigating Bad Credit Car Loans

Understanding Bad Credit and Its Impact on Your Car Loan Prospects

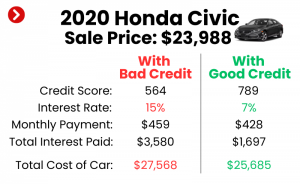

Before diving into the specifics of obtaining a loan, it’s crucial to understand what "bad credit" truly means in the eyes of lenders. Your credit score is a numerical representation of your creditworthiness, largely determined by your payment history, amounts owed, length of credit history, new credit, and credit mix. A FICO score, for instance, typically ranges from 300 to 850, with scores below 600-620 often categorized as "subprime" or "bad credit."

Lenders use your credit score as a primary tool to assess risk. A low score signals a higher likelihood of default, making them more hesitant to lend money or prompting them to offer less favorable terms. This isn’t a personal judgment, but a data-driven calculation of potential financial exposure.

Based on my experience, many people mistakenly believe that a low credit score instantly closes all doors. While it certainly presents challenges, it primarily influences the terms of the loan rather than the outright availability. Expect higher interest rates, potentially larger down payments, and stricter qualification criteria compared to someone with excellent credit. Lenders need to mitigate the increased risk they’re taking on.

Can You Really Get a Car Loan with Bad Credit? The Short Answer: Absolutely, But With Caveats

The resounding answer is yes, you can absolutely get a car loan even if you have bad credit. This is a common situation for millions of individuals across the country, and the financial industry has evolved to meet this specific need. There’s a dedicated segment of the lending market, often referred to as "subprime lenders," that specializes in offering auto loans to those with less-than-perfect credit histories.

These lenders understand that life happens, and a low credit score doesn’t always reflect a person’s current ability or willingness to pay. They look beyond just the credit score, considering other factors that paint a more complete picture of your financial stability. However, it’s important to set realistic expectations from the outset.

You likely won’t qualify for the advertised 0% APR deals, and your monthly payments might be higher than you’d prefer. The goal here isn’t necessarily to get the absolute best deal on the market, but to secure reliable transportation while also using the loan as an opportunity to rebuild your credit. This is a stepping stone, not necessarily the final destination.

Preparing for Your Bad Credit Car Loan Journey: Laying the Groundwork

Success in securing a bad credit car loan heavily relies on thorough preparation. Walking into a dealership or approaching a lender without doing your homework is a common mistake that can lead to unfavorable terms or outright rejection. A little groundwork can significantly improve your chances and potentially save you money in the long run.

1. Know Your Credit Score and Report Inside Out

Your credit score is your financial report card. Before you even start looking at cars, pull your latest credit reports from all three major bureaus – Equifax, Experian, and TransUnion. You can do this for free annually at AnnualCreditReport.com. This is your first and most critical step.

Review each report meticulously for any errors or inaccuracies. Mistakes happen, and disputing them can potentially boost your score, even if only by a few points. Every point counts when you have bad credit, as it can influence the interest rate you’re offered.

2. Master Your Budget: What Can You Truly Afford?

This is perhaps the most crucial financial step. Determine your maximum affordable monthly car payment by honestly assessing your income and expenses. Don’t forget to factor in other car-related costs like insurance, fuel, maintenance, and registration fees, which can add hundreds to your monthly outlay.

Pro tips from us: Before you even step foot in a dealership, create a detailed budget. Use a spreadsheet or a budgeting app to track every dollar coming in and going out. This clarity will prevent you from overcommitting and ensure your car payment is sustainable.

3. The Power of a Down Payment

Saving up a down payment is one of the most impactful actions you can take to improve your loan prospects. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also typically results in lower monthly payments and less interest paid over the life of the loan.

Even 10-20% of the car’s value can make a significant difference. It shows lenders your commitment and financial discipline, often making them more willing to work with you. If you’re looking for more ways to boost your financial health, check out our guide on .

4. Needs Versus Wants: Choose Wisely

With bad credit, practicality should be your guiding principle when selecting a vehicle. Focus on reliable, affordable transportation that meets your essential needs, rather than aspiring to a luxury model. A less expensive car means a smaller loan amount, which is easier to qualify for and easier to pay off.

Remember, this first car loan is a tool to rebuild your credit. You can always upgrade to your dream car once your financial standing has improved. Prioritize function and reliability over flashy features.

Finding the Right Lender for Bad Credit Car Loans: Not All Lenders Are Created Equal

The lending landscape for individuals with bad credit is diverse, and knowing where to look can save you time and frustration. Not every financial institution is equipped or willing to provide subprime auto loans, so targeting the right type of lender is key.

1. Specialized Subprime Lenders

These are companies whose primary business is lending to individuals with lower credit scores. They have specific programs and underwriting criteria designed for bad credit situations. While their interest rates will be higher, they are often more understanding of past financial difficulties. You can often find them through online search or by asking for recommendations.

2. Dealership Financing (Including "Buy Here, Pay Here")

Many dealerships offer in-house financing, often referred to as "buy here, pay here" (BHPH) lots. These dealerships finance the car themselves, bypassing traditional banks or lenders. They are often very willing to work with bad credit, but buyer beware: interest rates can be exceptionally high, and car selection might be limited.

Common mistakes to avoid are rushing into the first offer from a BHPH lot without understanding the full terms. Always compare their offer to others, and be prepared for potentially higher prices on the vehicles themselves.

3. Credit Unions

Credit unions are member-owned financial cooperatives, often known for being more flexible and sympathetic than traditional banks. If you’re already a member or can join one, it’s worth exploring their auto loan options. They might offer slightly better rates or more personalized service for bad credit applicants.

4. Online Lenders and Lending Marketplaces

The internet has opened up a world of options. Many online lenders specialize in bad credit car loans, and online lending marketplaces allow you to submit one application and receive offers from multiple lenders. This can be a great way to compare rates and terms without visiting numerous physical locations. Always ensure the online lender is reputable and secure.

5. Traditional Banks (Though Less Likely)

While harder, it’s not impossible to get a bad credit car loan from a traditional bank, especially if you have an existing relationship with them. They might be more willing to consider your application if you’re a long-time customer with a history of managing other accounts well. However, their criteria for bad credit often remain stricter than subprime lenders.

The Application Process for Bad Credit Car Loans: What Lenders Look For

Once you’ve identified potential lenders, the application process will require you to provide specific information. Lenders specializing in bad credit look beyond just your score; they want to assess your current ability and stability to repay the loan.

You’ll typically need:

- Proof of Income: Recent pay stubs, bank statements, or tax returns to verify stable employment and income.

- Proof of Residence: Utility bills or a lease agreement to confirm your address.

- Proof of Identity: Driver’s license or state ID.

- References: Sometimes required, especially for higher-risk loans.

Lenders will scrutinize your income stability, your debt-to-income (DTI) ratio (how much of your income goes towards existing debts), and your employment history. A steady job and consistent income are powerful indicators of your ability to make payments, even with a low credit score. From my perspective, many applicants overlook the long-term cost of a loan, focusing only on the monthly payment. Be prepared to discuss your financial situation openly and honestly.

Consider getting pre-approved before you start shopping for a car. Pre-approval gives you a clear idea of how much you can borrow, at what interest rate, and provides valuable leverage when negotiating with dealerships. It separates the financing from the car purchase, allowing you to focus on getting the best deal on each separately.

Understanding the Terms of Your Bad Credit Car Loan: Read the Fine Print

When you receive loan offers, it’s critical to understand every aspect of the terms presented. Don’t just focus on the monthly payment; delve into the details that will impact your total cost and financial commitment.

- Interest Rates (APR): For bad credit car loans, expect a higher Annual Percentage Rate (APR). This is the true cost of borrowing, encompassing the interest rate and certain fees. Compare APRs, not just interest rates, between different offers. A high APR can significantly increase the total amount you pay over the loan term.

- Loan Term: This is the length of time you have to repay the loan, typically in months (e.g., 36, 48, 60, 72 months). A longer term means lower monthly payments but often results in paying much more in interest over the life of the loan. Conversely, a shorter term has higher monthly payments but saves you money on interest.

- Down Payment: As discussed, a larger down payment reduces the loan amount and your overall cost.

- Fees: Be aware of any origination fees, processing fees, or other charges added to the loan. These can vary widely between lenders.

- Collateral: The car itself serves as collateral for the loan. This means if you fail to make payments, the lender has the right to repossess the vehicle.

Strategies to Improve Your Chances and Get Better Terms

Even with bad credit, there are actionable steps you can take to make your application more appealing to lenders and potentially secure more favorable terms. These strategies demonstrate your commitment and reduce the lender’s perceived risk.

- Increase Your Down Payment: This is consistently the most effective strategy. The more money you put down upfront, the less you need to borrow, directly reducing the lender’s exposure. It sends a strong signal of financial responsibility.

- Get a Co-signer: If you have a trusted family member or friend with good credit who is willing to co-sign, it can significantly improve your chances. A co-signer legally agrees to take responsibility for the loan if you default. However, this is a serious commitment for the co-signer, as their credit will also be affected if payments are missed.

- Choose an Affordable Car: Opting for a less expensive, used vehicle that meets your basic transportation needs will result in a smaller loan amount. This reduces your monthly payments and makes you a less risky borrower.

- Provide Proof of Stable Income and Employment: Lenders prioritize consistent income. Demonstrating a steady job history and a reliable income stream is often more important than your credit score alone for bad credit loans.

- Show Longevity at Residence/Employment: Stability in your living situation and work history can reassure lenders. It suggests you are a reliable individual unlikely to suddenly disappear.

- Negotiate (Carefully): While your negotiation power is limited with bad credit, you can still try to negotiate certain aspects. Focus on the total loan amount, the APR, and any fees. Don’t be afraid to walk away if the terms are simply not viable for your budget. A pro tip that can significantly impact your loan approval and terms is to present a strong case for your current financial stability, even if your past credit history is weak.

The Benefits of Successfully Managing Your Bad Credit Car Loan

Securing a bad credit car loan isn’t just about getting a vehicle; it’s a powerful opportunity to improve your financial standing. Successfully managing this loan can have far-reaching positive effects on your credit and overall financial health.

- Credit Score Improvement: Making every payment on time, every month, is the most effective way to build positive payment history, which accounts for 35% of your FICO score. As you consistently make timely payments, your credit score will gradually increase.

- Building a Payment History: This loan establishes a new, positive credit line on your report. Future lenders will see this responsible behavior, making it easier to qualify for other loans (like mortgages) or credit cards at better rates.

- Financial Discipline: Managing a car loan instills valuable financial discipline. You learn to budget, prioritize payments, and understand the consequences of missed deadlines. This experience is invaluable for future financial decisions.

- Transportation: Beyond the financial benefits, having a reliable car opens up opportunities for better jobs, educational pursuits, and simply navigating daily life with greater ease. It’s a practical necessity that contributes to overall stability.

What to Do After Getting Your Bad Credit Car Loan: Maintaining Momentum

The work doesn’t stop once you drive off the lot. To maximize the benefits of your bad credit car loan, you need to remain diligent and strategic.

- Make Payments On Time, Every Time: This cannot be stressed enough. Set up automatic payments, mark your calendar, or do whatever it takes to ensure payments are never late. Late payments hurt your credit score and can incur additional fees.

- Consider Refinancing: Once you’ve made 6-12 months of on-time payments and your credit score has improved, explore refinancing options. You might qualify for a lower interest rate, which can significantly reduce your monthly payment and the total cost of the loan. For a deeper dive into budgeting before your big purchase, explore our article on .

- Avoid New Debt: While focusing on paying off your car loan, try to avoid taking on new significant debt. This allows you to allocate more resources to your current obligations and maintain a healthy debt-to-income ratio.

- Monitor Your Credit: Continue to check your credit reports regularly to track your progress and ensure there are no new errors. Watching your score improve can be a great motivator.

Common Pitfalls and How to Avoid Them

The bad credit car loan market, unfortunately, can have its share of predatory practices. Being informed allows you to protect yourself and make sound decisions.

- High-Pressure Sales Tactics: Some dealerships might try to rush you into a deal or make you feel like this is your only option. Take your time, ask questions, and never sign anything you don’t fully understand.

- "Yo-yo" Financing: This occurs when a dealer lets you drive off with a car, only to call you back days later claiming the financing fell through and demanding a higher interest rate or different terms. Always ensure your financing is 100% approved before leaving the lot.

- Excessive Add-ons: Dealers often push expensive add-ons like extended warranties, gap insurance, or paint protection. While some, like gap insurance, might be beneficial, others can be overpriced and unnecessary. Evaluate each add-on carefully and don’t feel pressured to accept them. Based on my observations in the industry, these are common traps that significantly inflate the cost of your vehicle.

- Not Reading the Fine Print: Every clause in your loan agreement matters. Understand the APR, repayment schedule, penalties for late payments, and any pre-payment penalties. If something is unclear, ask for clarification before signing.

Drive Your Future: Taking Control of Your Financial Destiny

Navigating bad credit car loans can seem daunting, but with the right approach, it becomes a clear path to both reliable transportation and improved financial health. This journey is about empowerment – understanding your situation, preparing diligently, making informed choices, and committing to responsible financial behavior.

Remember, a bad credit car loan isn’t just a transaction; it’s an opportunity. It’s your chance to rewrite your credit story, build a positive payment history, and gain access to future financial opportunities that might currently seem out of reach. By following the strategies outlined in this guide, you can confidently secure the transportation you need and drive towards a more stable and prosperous financial future. Start preparing today, take control, and embark on this journey with confidence.