Driving Towards a Brighter Financial Future: Your Comprehensive Guide to Credit Building Car Loans

Driving Towards a Brighter Financial Future: Your Comprehensive Guide to Credit Building Car Loans Carloan.Guidemechanic.com

For many, owning a car is more than just convenience; it’s a necessity that opens doors to employment, education, and personal freedom. However, for individuals navigating the complexities of a less-than-perfect credit score, securing an auto loan can feel like an insurmountable challenge. This is where the credit building car loan steps in, offering a strategic pathway not only to vehicle ownership but also to a significantly improved financial standing.

As an expert in automotive financing and a dedicated advocate for financial literacy, I’ve seen firsthand how a responsibly managed car loan can transform a person’s credit profile. This article is designed to be your definitive guide, offering an in-depth exploration of how these loans work, what to expect, and how to leverage them effectively to build a strong credit foundation. We’ll delve deep into every aspect, providing you with the knowledge and confidence to make informed decisions and steer your financial future in the right direction.

Driving Towards a Brighter Financial Future: Your Comprehensive Guide to Credit Building Car Loans

What Exactly Is a Credit Building Car Loan?

At its core, a credit building car loan is an auto financing product specifically designed for individuals with poor credit, limited credit history, or those looking to actively improve their credit score. Unlike traditional prime auto loans, which are reserved for borrowers with excellent credit, these loans acknowledge a borrower’s past financial struggles or lack of history. They focus on providing an opportunity to prove creditworthiness.

Lenders offering these types of loans often specialize in subprime financing. This means they are willing to take on a higher perceived risk. In exchange for this risk, the terms of these loans, particularly the interest rates, tend to be higher than those offered to borrowers with strong credit. However, the ultimate goal for the borrower isn’t just to buy a car, but to use the loan as a tool for financial rehabilitation.

The fundamental principle behind a credit building car loan is simple: consistent, on-time payments demonstrate financial responsibility. Every payment you make on time is reported to the major credit bureaus. This positive reporting helps to gradually strengthen your credit profile over the loan’s term. It’s a strategic move to address immediate transportation needs while simultaneously investing in your long-term financial health.

Why Consider a Credit Building Car Loan? The Double Benefit

The decision to pursue a credit building car loan often stems from a dual need: the immediate requirement for reliable transportation and the long-term desire to improve one’s credit score. This type of financing addresses both challenges simultaneously, making it a powerful financial tool when used wisely. Let’s explore the significant benefits.

Firstly, having a car can be life-changing. It can significantly expand job opportunities, reduce commute times, and provide greater independence. Without a car, accessing better-paying jobs outside public transport routes or handling family responsibilities can become incredibly difficult. A credit building car loan can bridge this gap, putting you behind the wheel of a reliable vehicle.

Secondly, and perhaps most importantly from a financial perspective, these loans are an active way to repair or establish credit. Many people with poor credit find themselves in a catch-22: they can’t get credit without a good score, but they can’t build a good score without getting credit. A car loan breaks this cycle. It provides a structured payment plan that, when adhered to, directly contributes to a positive credit history.

Based on my experience working with countless individuals, successfully managing a credit building car loan often marks a turning point in their financial journey. It demonstrates to future lenders that you are capable of handling significant debt responsibly. This positive track record can open doors to better interest rates on future loans, credit cards, and even housing opportunities down the line. It’s an investment not just in a vehicle, but in your financial future.

Understanding Your Credit Score: The Foundation of Lending

Before diving into the specifics of obtaining a loan, it’s crucial to understand what lenders look at: your credit score and credit report. These financial snapshots are primary indicators of your creditworthiness. A credit building car loan is precisely for those whose snapshot isn’t perfect yet.

Your credit score, typically a FICO Score or VantageScore, is a three-digit number that summarizes your credit risk. It ranges from 300 to 850, with higher numbers indicating lower risk. Lenders use this score to quickly assess how likely you are to repay borrowed money. For credit building loans, lenders are generally looking at scores in the "subprime" or "deep subprime" categories, which are typically below 620.

Several key factors contribute to your credit score. Payment history is by far the most impactful, accounting for about 35% of your FICO score. This is why consistent, on-time payments on your car loan are so critical for rebuilding credit. Other factors include credit utilization (how much credit you’re using compared to your limits), length of credit history, new credit, and credit mix (having different types of credit like installment loans and revolving credit).

Pro tips from us: Regularly checking your credit report is essential. You can get a free copy from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once a year at AnnualCreditReport.com. Reviewing it helps you identify errors and understand exactly what lenders see. Knowing your starting point empowers you to track your progress and celebrate improvements as you manage your credit building car loan.

Navigating the Application Process: What to Expect

Applying for a credit building car loan requires a slightly different approach than a standard loan application. Lenders specializing in these loans understand that your credit history might have blemishes. They will often look beyond just your score, focusing on your current ability to pay and your commitment to financial improvement.

The first step is often pre-qualification. This process involves a soft credit pull, which doesn’t affect your credit score, and gives you an idea of what loan terms you might qualify for. It’s a great way to gauge your options without committing. During this stage, lenders will usually ask about your income, employment history, and housing situation.

Once you decide to move forward, you’ll undergo a full application, which involves a hard credit inquiry. This will temporarily ding your credit score by a few points, but the impact is usually minor and short-lived. Be prepared to provide documentation such as proof of income (pay stubs, bank statements), proof of residence (utility bills), and identification. Lenders want to ensure you have a stable income to support the monthly payments.

Common mistakes to avoid are applying to too many lenders within a short period. While multiple inquiries for the same type of loan within a 14-45 day window are usually counted as one by FICO, spreading them out too much can harm your score. Research thoroughly and apply strategically.

The Role of a Co-signer

If you’re struggling to get approved on your own, or if the interest rates offered are excessively high, a co-signer might be an option. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you default. This can significantly improve your chances of approval and potentially secure better terms.

However, choosing a co-signer requires careful consideration. This person is putting their own credit on the line for you. If you miss payments, it negatively impacts their credit score, too. Based on my experience, co-signing should only be pursued if you are absolutely confident in your ability to make every payment on time. It’s a serious commitment for both parties.

Dealerships vs. Lenders Specializing in Bad Credit

When seeking a credit building car loan, you have a few avenues. Many dealerships have "special finance" departments that work with a network of subprime lenders. They can often streamline the process, helping you find a car and financing in one place. However, it’s always wise to compare their offers with those from independent lenders.

There are also banks, credit unions, and online lenders that specialize in bad credit auto loans. These institutions often have more flexible underwriting criteria and might offer competitive rates for your situation. Pro tips from us: Don’t limit yourself to the first offer. Shop around and compare interest rates, loan terms, and fees from at least three different sources to ensure you’re getting the best possible deal for your financial situation.

Key Factors in Your Credit Building Car Loan

Understanding the key components of your loan agreement is paramount, especially when your primary goal is credit improvement. These factors directly influence your financial commitment and the effectiveness of the loan as a credit-building tool.

Interest Rates: A Necessary Compromise

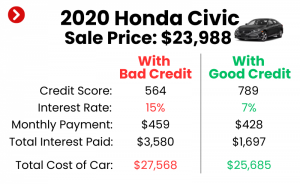

For credit building car loans, interest rates will almost certainly be higher than for prime borrowers. This higher rate reflects the increased risk lenders perceive when financing individuals with poor or limited credit. It’s a reality you must accept, but also one you should work to mitigate.

While a higher interest rate means you’ll pay more over the life of the loan, it’s often the price of admission to rebuild your credit. Your focus should be on making payments on time to eventually qualify for lower rates in the future. Pro tips from us: Even with a higher rate, avoid predatory lenders charging exorbitant rates (e.g., above 25-30% APR, depending on your state’s laws). Always compare rates and understand the total cost of the loan.

Loan Term: Balancing Payments and Interest

The loan term refers to the length of time you have to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer loan term means lower monthly payments, which can make the loan more affordable. However, it also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter loan term results in higher monthly payments but less total interest paid. For a credit building loan, finding the right balance is crucial. Based on my experience, aiming for the shortest term you can comfortably afford is usually the best strategy. This minimizes interest costs and helps you pay off the loan faster, accelerating your credit improvement.

The Power of a Down Payment

Making a down payment is one of the most effective strategies for anyone, but especially for those with poor credit seeking an auto loan. A down payment reduces the amount of money you need to borrow, which directly translates to lower monthly payments and less interest paid over the loan’s term.

More importantly, a significant down payment signals to lenders that you are a serious and responsible borrower. It reduces their risk, making them more likely to approve your loan and potentially offer more favorable terms, even with a lower credit score. Common mistakes to avoid: Skipping the down payment entirely. Even a modest amount, like 10-20% of the vehicle’s price, can make a substantial difference in your loan terms and approval chances.

Monthly Payments: Affordability is Key

Before signing any loan agreement, meticulously evaluate whether the monthly payments are truly affordable within your budget. It’s not just about getting approved; it’s about successfully making every payment on time, every month, for the entire loan term. Overextending yourself is a common pitfall that can lead to missed payments and further damage to your credit.

Pro tips from us: Create a detailed budget that includes all your income and expenses. Be realistic about what you can comfortably afford each month without stressing your finances. Remember, your goal is not just to get a car, but to use this loan as a stepping stone to better credit. For more tips on budgeting effectively, check out our guide on Budgeting for Your First Car.

Pro Tips for Securing and Managing Your Loan

Successfully using a credit building car loan to your advantage involves more than just getting approved. It requires strategic planning and diligent management throughout the loan term. Here are some expert insights to guide you.

Research and Compare: Don’t Settle

As mentioned earlier, never take the first offer you receive. Research different lenders, including banks, credit unions, online lenders, and dealership finance departments. Gather multiple quotes and compare the Annual Percentage Rate (APR), which includes both the interest rate and any fees, as well as the loan term and total cost.

Based on my experience, a little extra effort in shopping around can save you hundreds, if not thousands, of dollars over the life of the loan. This due diligence also empowers you to negotiate better terms, as you’ll have competing offers.

Budgeting: Your Financial Anchor

We cannot stress this enough: a solid budget is your most important tool for success. Before you even apply for a loan, understand your income, fixed expenses (rent, utilities), and variable expenses (food, entertainment). Factor in potential car-related costs beyond the loan payment, such as insurance, fuel, maintenance, and registration.

Pro tips from us: Use a spreadsheet or a budgeting app to track every dollar. This helps you ensure that your monthly car payment is truly sustainable. Missing payments because of poor budgeting is a common mistake that undermines the entire purpose of a credit building loan.

Make Payments On Time, Every Time: The Golden Rule

This is the single most critical piece of advice for anyone with a credit building car loan. Your payment history accounts for the largest portion of your credit score. Every on-time payment contributes positively to your credit report, slowly but surely improving your score.

Common mistakes to avoid: Setting up automatic payments can be a lifesaver. If possible, schedule payments a few days before the due date to account for any processing delays. If you anticipate a problem making a payment, communicate with your lender immediately. Many lenders are willing to work with you if you reach out proactively.

Avoid Excessive New Credit

While you are actively building credit with your car loan, it’s wise to limit opening new lines of credit, such as new credit cards or personal loans. Each new credit application can result in a hard inquiry on your credit report, which can temporarily lower your score.

Furthermore, taking on too much new debt can make your existing car loan payments feel more burdensome. Focus on successfully managing your current loan first. Based on my experience, waiting until your car loan is well established and your credit score has significantly improved is a much smarter strategy for seeking additional credit.

Read the Fine Print: No Surprises

Before you sign any loan agreement, read every single word. Understand the interest rate, the total loan amount, any fees (origination fees, prepayment penalties), and all the terms and conditions. If anything is unclear, ask questions until you fully understand.

Pro tips from us: Pay close attention to clauses about late payment fees, repossession policies, and how additional payments are applied. Knowledge is power, and being fully informed prevents unpleasant surprises down the road.

Communicate with Your Lender

Life happens, and sometimes unexpected financial difficulties arise. If you find yourself in a situation where you might struggle to make a payment, do not ignore it. Contact your lender as soon as possible.

Many lenders offer options like payment deferrals or modified payment plans for borrowers facing temporary hardship. Based on my experience, lenders are often more willing to work with you if you are proactive and transparent. Hiding from the problem will only make it worse and can lead to severe negative impacts on your credit.

Common Mistakes to Avoid with Credit Building Car Loans

While a credit building car loan can be a fantastic tool, it’s not without its pitfalls. Being aware of common mistakes can help you navigate the process successfully and avoid setbacks on your journey to better credit.

Firstly, taking on too much debt is a significant trap. Just because a lender approves you for a certain amount doesn’t mean you should borrow that much. Overextending yourself with high monthly payments that strain your budget is a recipe for disaster. This leads to missed payments, which severely damage the very credit you’re trying to build.

Secondly, ignoring the interest rate is a costly error. While higher rates are expected with a credit building loan, some lenders may offer predatory rates. Always calculate the total cost of the loan over its entire term. A low monthly payment might seem attractive, but if it comes with an extremely long term and a sky-high interest rate, you could end up paying double or triple the car’s value.

Thirdly, and perhaps most damagingly, missing payments defeats the entire purpose of the loan. A single missed payment can drop your credit score by dozens of points and stay on your credit report for up to seven years. This undoes all the positive work you’ve put in. Make timely payments your absolute top financial priority.

Another mistake is not checking your credit report regularly. After securing your loan and making several payments, you should be seeing positive changes. If you’re not, or if you spot errors, you need to address them immediately. Monitoring your credit helps you ensure your efforts are being properly reported and allows you to catch any fraudulent activity.

Finally, falling for predatory lending is a serious concern. Be wary of lenders who pressure you into signing immediately, refuse to disclose all terms, or offer "guaranteed approval" regardless of your situation. If a deal sounds too good to be true, it probably is. Always verify a lender’s reputation and legitimacy.

What Happens After Your Loan is Paid Off?

Successfully paying off a credit building car loan is a monumental achievement and a significant milestone on your financial journey. It’s not just about owning your car free and clear; it’s about the profound positive impact it has on your credit profile and future financial opportunities.

Once your final payment is made, the lender will report the loan as "paid in full" to the credit bureaus. This positive entry will remain on your credit report for many years, serving as strong evidence of your financial responsibility. Your credit score will likely see a substantial boost, reflecting your proven ability to manage and repay a significant debt.

This improved credit score opens up a world of new possibilities. You’ll likely qualify for better interest rates on future loans, whether it’s another car loan, a mortgage, or a personal loan. You might also gain access to premium credit cards with lower interest rates and better rewards. Based on my experience, this is the moment where all the hard work truly pays off, transforming you from a high-risk borrower to a more desirable client in the eyes of lenders.

However, the journey doesn’t end there. Maintaining good credit habits is crucial. Continue to monitor your credit report, pay all your bills on time, and manage any other credit accounts responsibly. The skills and discipline you developed while managing your credit building car loan are lifelong assets that will serve you well in all your financial endeavors.

Expert Insights & Final Thoughts

Navigating the world of automotive financing with less-than-perfect credit can seem daunting, but a credit building car loan offers a beacon of hope and a clear path forward. It’s a strategic financial tool that, when used responsibly, delivers dual benefits: reliable transportation and a significantly improved credit score.

Having guided many through this process, I can tell you that success hinges on three core principles: thorough research, realistic budgeting, and unwavering commitment to on-time payments. These aren’t just suggestions; they are the bedrock of credit improvement. Remember, this isn’t just about buying a car; it’s about making a conscious decision to invest in your financial future and build a foundation for greater financial freedom.

Don’t let past credit challenges define your future. With the right approach and the valuable information provided in this guide, you are empowered to take control. Start by understanding your current credit situation, research reputable lenders, and prepare a solid budget. Your journey to a stronger credit score and reliable transportation begins now. The road ahead may have a few bumps, but with diligence and smart choices, you’ll be driving towards a brighter financial future.