Driving Towards Simplicity: Your Ultimate Guide to Combining Car Loans

Driving Towards Simplicity: Your Ultimate Guide to Combining Car Loans Carloan.Guidemechanic.com

Are you juggling multiple car payments each month, feeling the strain of different due dates, varying interest rates, and the sheer mental load of keeping track? You’re not alone. Many individuals find themselves in a similar situation, whether it’s from upgrading vehicles, taking out a second loan for a family member, or simply acquiring cars at different stages of their financial journey.

The good news is there’s a powerful financial strategy that can help you regain control: combining car loans. This isn’t just about refinancing a single vehicle; it’s about strategically merging multiple auto debts into one streamlined, manageable payment. This comprehensive guide will delve deep into everything you need to know about this often-overlooked financial tool.

Driving Towards Simplicity: Your Ultimate Guide to Combining Car Loans

Our mission is to provide you with an in-depth, easy-to-understand roadmap. We’ll explore the benefits, illuminate the potential pitfalls, and walk you through the entire process, empowering you to make an informed decision about simplifying your auto debt. Let’s hit the road to financial clarity!

What Exactly Does "Combining Car Loans" Mean?

At its core, combining car loans, often referred to as auto loan consolidation, involves taking out a new, larger loan to pay off two or more existing car loans. Think of it as hitting the "reset" button on your vehicle financing. Instead of sending checks or making online payments to multiple lenders, you’ll make just one single payment to a new lender.

This new loan effectively "absorbs" your previous debts. The old loan accounts are closed, and a fresh account with new terms, a new interest rate, and a new payment schedule is established. It’s a strategic move designed to simplify your financial life and, in many cases, improve your overall financial standing.

Based on my experience, many people confuse combining car loans with simply refinancing a single vehicle. While refinancing is a part of the process, consolidating multiple car loans is a more complex undertaking with distinct advantages and considerations. It’s about unifying your auto debt, not just adjusting the terms of one loan.

Why Would Someone Consider Combining Car Loans? The Core Benefits

The appeal of consolidating car loans isn’t just about convenience; it offers several tangible benefits that can significantly impact your financial well-being. Let’s break down the primary advantages of this strategic approach.

1. Simplified Financial Management

Imagine having just one bill to remember instead of two, three, or even more. This is arguably the most immediate and impactful benefit of combining car loans. You’ll have a single due date and a single payment amount to track each month.

This simplification drastically reduces the mental load of managing multiple financial obligations. It minimizes the risk of missing a payment due to oversight, which in turn protects your credit score from late payment penalties.

2. Potentially Lower Monthly Payments

One of the most attractive aspects of refinancing multiple car loans into one is the potential to reduce your overall monthly outflow. This can happen in a couple of ways. Firstly, if your credit score has improved since you took out your original loans, you might qualify for a significantly lower interest rate on the new consolidated loan.

Secondly, you might choose to extend the loan term. While extending the term means you’ll pay for a longer period, it can dramatically decrease your required monthly payment, freeing up cash flow for other expenses or savings. This can be a lifesaver for those feeling stretched financially.

3. Reduced Overall Interest Paid (If Done Right)

While extending your loan term can sometimes lead to paying more interest over the long run, combining loans can actually save you money on interest if you secure a much lower Annual Percentage Rate (APR). If your existing loans carry high interest rates, a new consolidated loan with a significantly lower APR can translate into substantial savings over the life of the loan.

Pro tips from us: Always compare the total cost of the new consolidated loan, including any fees, against the remaining total cost of your current individual loans. This ensures you’re truly saving money and not just lowering your monthly payment at the expense of long-term savings.

4. Improved Cash Flow

Lowering your monthly payments directly translates to improved cash flow. With more discretionary income each month, you gain greater financial flexibility. This extra money can be directed towards other financial goals, such as building an emergency fund, paying down higher-interest debt (like credit cards), or investing for the future.

This enhanced liquidity can provide a sense of financial breathing room. It reduces stress and empowers you to make more proactive financial decisions, rather than constantly feeling reactive to bills.

5. Opportunity for Better Loan Terms

When you apply for a new consolidated loan, you have the chance to negotiate or secure entirely new loan terms. This means you’re not just getting a new interest rate; you might also get more favorable clauses, fewer fees, or a more flexible payment structure. It’s an opportunity to reset and align your auto financing with your current financial standing and future goals.

Lenders are always competing for business, especially for borrowers with good credit. This competition works in your favor when you’re seeking to simplify finances through consolidation.

Is Combining Car Loans Right for You? Key Considerations

While the benefits are compelling, combining car loans isn’t a one-size-fits-all solution. It’s crucial to assess your personal financial situation carefully. Here are the key factors to weigh before proceeding.

1. Your Current Interest Rates vs. Potential New Rates

The primary driver for many considering consolidation is the hope of securing a lower interest rate. If your existing car loans have high APRs, perhaps because your credit wasn’t as strong when you first purchased the vehicles, then a new loan with a significantly lower rate can be highly advantageous. However, if your current rates are already very low, the savings might be minimal or non-existent.

2. Your Current Credit Score

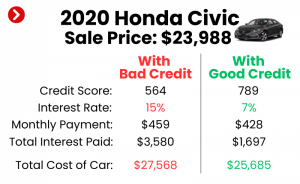

Your credit score plays a monumental role in the interest rate you’ll be offered. If your credit score has improved substantially since you took out your original car loans, you’re in an excellent position to qualify for better terms on a consolidated loan. Lenders view borrowers with higher scores as less risky, translating to more favorable rates.

Conversely, if your credit score has declined, combining loans might result in a higher interest rate, making it an unfavorable move. Understanding your credit standing is the first step. For a deeper dive into improving your credit score before applying, check out .

3. The Age and Value of Your Vehicles

Lenders consider the collateral value of your vehicles when approving auto loans. If your cars are significantly older or have high mileage, their market value might have depreciated considerably. This can make it challenging to secure a new loan that covers the remaining balances, especially if you owe more than the cars are worth (negative equity). Lenders are less willing to finance an asset that provides insufficient collateral.

4. Remaining Loan Balances and Terms

Take a close look at how much you still owe on each car loan and how many payments are left. If you’re nearing the end of one or more loan terms, the administrative effort and potential fees of consolidation might not outweigh the benefits. The biggest impact comes when you consolidate loans with substantial remaining balances and longer terms.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost over the full life of the loan. Always calculate the long-term implications, especially if you’re extending the loan term.

5. Your Financial Goals

What are you hoping to achieve by combining your car loans? Are you primarily looking for lower monthly payments to free up cash flow? Or is your main objective to reduce the total interest paid over time? Your goals will dictate the best approach. A longer loan term might achieve lower payments but could increase total interest, while a shorter term might save interest but result in higher monthly payments. Be clear on your priorities.

The Process: How to Combine Your Car Loans Step-by-Step

Navigating the world of auto loan consolidation might seem daunting, but by following a structured approach, you can successfully merge your car loans. Here’s a detailed, step-by-step guide based on my years of experience in financial management.

Step 1: Assess Your Current Financial Situation

Before you even think about contacting a lender, gather all the necessary information about your existing car loans. This includes:

- Current loan balances for each vehicle.

- Interest rates (APRs) for each loan.

- Monthly payment amounts and due dates.

- Remaining loan terms (how many months left).

- Any prepayment penalties associated with your current loans.

Also, obtain your latest credit report and score. Knowing your current credit standing is crucial, as it directly impacts the rates you’ll be offered on a new loan. Websites like AnnualCreditReport.com allow you to get a free report from each of the three major credit bureaus once a year.

Step 2: Research Potential Lenders

Not all lenders specialize in or offer specific debt consolidation auto loans. You’ll need to do some research to find institutions that provide this service. Consider a variety of lenders:

- Banks: Traditional financial institutions often have competitive rates for well-qualified borrowers.

- Credit Unions: Known for member-focused services and often lower interest rates due to their non-profit status.

- Online Lenders: Many modern fintech companies specialize in auto refinancing and consolidation, offering quick applications and approvals.

Look for lenders that specifically mention "auto loan consolidation" or "refinancing multiple vehicles" on their websites.

Step 3: Get Pre-Approved (Soft Inquiry)

Once you’ve identified a few potential lenders, inquire about pre-approval. Many lenders offer a pre-qualification process that involves a "soft" credit inquiry. This allows them to give you an estimate of the interest rate and loan terms you might qualify for, without negatively impacting your credit score.

This step is incredibly valuable. It helps you understand what’s realistically available to you before committing to a formal application, which typically involves a "hard" credit inquiry.

Step 4: Compare Offers Diligently

This is a critical step where attention to detail pays off. Do not simply jump at the lowest advertised APR. You need to compare the full spectrum of each offer:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and some fees.

- Loan Term: How many months will you be paying back the new loan?

- Total Interest Paid: Calculate this over the entire loan term for each offer.

- Fees: Look for origination fees, application fees, or any other charges.

- Prepayment Penalties: Ensure the new loan doesn’t have penalties for paying it off early.

Based on my years of observing financial trends, a thorough comparison is non-negotiable. Use a spreadsheet to list out all the details from each lender.

Step 5: Apply for the New Consolidated Loan

Once you’ve selected the best offer, proceed with a formal application. This will involve a "hard" credit inquiry, which might temporarily dip your credit score by a few points. However, if you apply with multiple lenders within a short window (typically 14-45 days, depending on the scoring model), credit bureaus often count these as a single inquiry for rate shopping purposes.

You’ll need to provide documentation, which typically includes:

- Proof of income (pay stubs, tax returns).

- Vehicle information (VINs, mileage, year, make, model).

- Current loan statements for all vehicles you wish to consolidate.

- Personal identification (driver’s license).

Step 6: Pay Off Old Loans

Once your new consolidated loan is approved and funded, the new lender will typically handle the payoff of your existing car loans directly. They will send the funds to your previous lenders, closing those accounts. It’s crucial to confirm with your old lenders that the accounts have been fully paid off and closed. Request a confirmation letter for your records.

Step 7: Enjoy Simplified Payments

With the old loans settled, you now have one single, manageable monthly payment. Set up automatic payments to ensure you never miss a due date. This helps you avoid late fees and maintain a healthy payment history, which is vital for your credit score.

Potential Risks and Downsides of Combining Car Loans

While combining car loans offers compelling advantages, it’s not without its potential drawbacks. Being aware of these risks is essential for making a truly informed decision.

1. Higher Overall Cost If Terms are Extended

This is perhaps the most significant risk. While extending your loan term can drastically lower your monthly payment, it often means you’ll pay more in total interest over the life of the loan. Even with a slightly lower APR, a significantly longer repayment period can negate any interest savings and even increase your total cost.

Pro tips from us: Always calculate the total interest paid for both scenarios – keeping your current loans versus the new consolidated loan – before committing. Don’t let a lower monthly payment blind you to a higher long-term cost.

2. Temporary Impact on Your Credit Score

Applying for a new loan involves a "hard" inquiry on your credit report, which can cause a slight, temporary dip in your credit score. Additionally, when your old accounts are closed and a new one is opened, this can also temporarily affect your credit utilization and average age of accounts. These impacts are usually minor and recover over time with responsible payments.

3. Prepayment Penalties on Existing Loans

Some older car loan agreements include prepayment penalties. These are fees charged by the lender if you pay off your loan early. If your existing loans have such clauses, these fees could eat into any potential savings from consolidation. Carefully review your current loan documents before proceeding.

4. Eligibility Challenges

Not everyone will qualify for the best interest rates or even for consolidation. Lenders base their decisions on your credit score, income, debt-to-income ratio, and the value of the collateral (your vehicles). If your financial profile isn’t strong, you might not be offered terms that are genuinely beneficial.

5. Potential for Negative Equity

If you owe more on your vehicles than they are currently worth (negative equity), it can be difficult to find a lender willing to consolidate the loans. Lenders are reluctant to finance a loan where the collateral doesn’t cover the debt. In such cases, you might need to make a down payment to cover the negative equity, or the consolidated loan might carry a higher interest rate to offset the increased risk for the lender.

Alternative Strategies to Manage Multiple Car Loans

If combining car loans doesn’t seem like the right fit for your situation, or if you want to explore other options, several alternative strategies can help you manage multiple auto debts.

- Aggressive Repayment Strategy: Focus on paying down the loan with the highest interest rate first, while making minimum payments on the others. Once that high-interest loan is paid off, roll the money you were paying into the next highest interest loan. This is often called the "debt avalanche" method and can save you a significant amount in interest over time.

- Budgeting and Cutting Expenses: A thorough review of your monthly budget can reveal areas where you can cut back, freeing up more cash to make extra payments on your car loans. Even small additional payments can shorten your loan term and reduce total interest.

- Selling a Vehicle: If you have multiple cars and one is less essential, selling it could be a viable option. This allows you to pay off one loan entirely, eliminating a payment and potentially freeing up funds for other debts. This is a drastic step, but can provide immediate relief.

- Refinancing Individual Loans: If only one of your car loans has a particularly high interest rate, you might consider refinancing just that single loan. This is less complex than consolidating multiple loans but can still achieve significant savings on that specific debt.

Choosing the Right Lender for Your Combined Car Loan

Selecting the right lender is as crucial as understanding the consolidation process itself. Different types of financial institutions offer varying benefits and terms.

- Credit Unions: Often lauded for their competitive interest rates and personalized customer service. Since they are member-owned, their focus is on providing value to their members. If you’re eligible to join one, they are definitely worth considering.

- Traditional Banks: Large banks offer convenience and a wide range of services. They can be a good option, especially if you have an existing relationship with them, but their rates might be less flexible than credit unions.

- Online Lenders: These platforms have revolutionized the lending landscape. They offer speed, convenience, and often streamlined application processes. Many specialize in auto refinancing and consolidation, making them a strong contender if you value efficiency and digital solutions.

When making your choice, look beyond just the interest rate. Consider customer reviews, responsiveness, and the clarity of their loan terms. For more guidance on choosing an auto loan lender, a trusted resource like the Consumer Financial Protection Bureau offers excellent advice on what to look for and questions to ask.

Driving Towards Financial Freedom

Combining car loans can be a powerful financial strategy, offering a clear path to simplified payments, potentially lower interest rates, and improved cash flow. It’s a method that can significantly reduce the stress associated with managing multiple debts, allowing you to focus on your broader financial goals.

However, like any major financial decision, it requires careful consideration and due diligence. Take the time to assess your current situation, understand the potential benefits and risks, and diligently compare offers from various lenders. By doing so, you can ensure that you’re making a choice that truly aligns with your financial well-being.

Remember, the ultimate goal is not just to consolidate debt, but to gain greater control and peace of mind over your finances. Whether you choose to combine your loans or explore alternative strategies, the journey towards financial freedom begins with informed decisions. For more strategies on managing various forms of debt, explore our article on .