Driving Your Business Forward: The Ultimate Guide to Car Loan LLCs

Driving Your Business Forward: The Ultimate Guide to Car Loan LLCs Carloan.Guidemechanic.com

The hum of a new engine, the gleam of polished chrome – for many entrepreneurs, a reliable vehicle isn’t just a convenience, it’s a critical tool for success. Whether you’re making client visits, delivering products, or simply need dependable transportation for your team, how you finance that vehicle can have significant implications for your business and personal finances. This is where the concept of a "Car Loan LLC" comes into play, a strategic approach many business owners explore.

Navigating the world of business financing can feel like a labyrinth, but understanding how a Limited Liability Company (LLC) can factor into your vehicle acquisition is a game-changer. This comprehensive guide will demystify the Car Loan LLC, exploring its profound benefits, potential pitfalls, and the step-by-step process to leverage this powerful business structure. Our goal is to provide you with the in-depth knowledge needed to make an informed decision, ensuring your wheels keep turning smoothly, both on the road and in your balance sheet.

Driving Your Business Forward: The Ultimate Guide to Car Loan LLCs

What Exactly is a Car Loan LLC? Deconstructing the Concept

When we talk about a "Car Loan LLC," it’s crucial to clarify what this phrase truly signifies. It doesn’t mean the LLC provides the car loan itself. Instead, it refers to the strategic decision to have your Limited Liability Company (LLC) be the borrower and the legal owner of a vehicle, rather than you as an individual.

An LLC is a popular business structure that combines the pass-through taxation of a partnership or sole proprietorship with the limited liability of a corporation. This means your personal assets are generally shielded from business debts and liabilities. When an LLC takes out a car loan, the loan is in the company’s name, and the vehicle is registered to the LLC. This distinction is foundational to understanding all the subsequent benefits and challenges.

The car, in this scenario, becomes a business asset, fully integrated into your company’s operations and financial records. This separation between personal and business ownership is a cornerstone of responsible business management and offers a host of strategic advantages we’ll delve into shortly. It’s about leveraging a formal business entity to manage a significant business expense.

Why Consider Using an LLC for Your Car Loan? Unveiling the Benefits

The decision to finance a vehicle through your LLC is rarely made on a whim. It’s a calculated move designed to offer specific advantages that can significantly impact your financial health and operational efficiency. Let’s explore the key benefits in detail.

1. Robust Limited Liability Protection

One of the most compelling reasons to use an LLC for your car loan is the inherent limited liability protection it offers. This structure legally separates your personal assets from your business debts and obligations. If your LLC defaults on the car loan, or if the vehicle is involved in an accident that results in a lawsuit exceeding your insurance coverage, your personal assets – such as your home, personal savings, or other non-business investments – are generally protected.

Without an LLC, if you personally own and finance a vehicle used for business, you are personally liable for any debts or legal judgments. This means creditors could pursue your individual assets. By having the LLC own the car, you create a vital legal shield, reinforcing the separation between you and your business.

Based on my experience, this protection provides invaluable peace of mind for business owners. It allows you to take calculated risks in your business without putting your entire personal financial future on the line for every business asset.

2. Significant Tax Advantages

The tax benefits associated with an LLC-owned vehicle can be substantial, making it a powerful financial planning tool. When a vehicle is a legitimate business asset, a range of expenses related to its operation and ownership can often be deducted from your business income. These deductions can significantly reduce your overall tax liability.

Deductible Expenses Typically Include:

- Loan Interest: The interest paid on the car loan itself can often be fully deducted as a business expense.

- Depreciation: The value of the vehicle can be depreciated over several years, allowing you to deduct a portion of its cost each year. This is a non-cash expense that reduces taxable income.

- Operating Costs: Fuel, oil, maintenance, repairs, tires, and even car washes can all be legitimate business deductions.

- Insurance Premiums: The cost of insuring a business-owned vehicle is a standard operating expense.

- Registration and License Fees: Annual fees for vehicle registration can also be deducted.

It’s crucial to understand that these deductions are generally only applicable for the percentage of time the vehicle is used for business purposes. Meticulous record-keeping of mileage and usage is paramount to justify these deductions to the IRS. Pro tips from us: Always consult with a qualified tax professional to understand the specific rules and limits applicable to your situation, as tax laws can be complex and vary.

3. Enhanced Professional Image and Credibility

Operating your business with professionally acquired assets, including vehicles, can significantly bolster your professional image and credibility. When clients or partners see your company vehicle, branded and clearly belonging to your LLC, it projects an image of stability, organization, and commitment. This can be particularly impactful for service-based businesses or those requiring frequent client interactions.

An LLC car also contributes to the perception of your business as a serious, established entity. This professional appearance can indirectly lead to greater trust, easier client acquisition, and even better terms with vendors and suppliers. It signals that you are invested in your operations and committed to long-term growth.

4. Clear Asset Segregation and Financial Management

One of the golden rules of sound business practice is to keep personal and business finances strictly separate. Using an LLC for your car loan naturally enforces this segregation. The loan payments come directly from your business bank account, and all related expenses are recorded under the LLC’s financial records.

This clear separation simplifies bookkeeping, tax preparation, and financial analysis. It makes it much easier to track the true cost of operating your business and to present clear financial statements to potential investors or for future loan applications. Common mistakes to avoid are commingling funds, which can blur the lines between personal and business, potentially undermining the liability protection an LLC offers.

5. Potential for Streamlined Estate Planning

While perhaps not the primary driver for most, owning business assets like vehicles within an LLC can simplify future estate planning. If something happens to you, the LLC’s assets, including the vehicle, are governed by the LLC’s operating agreement. This can provide a clearer path for asset transfer or business continuation compared to individually owned assets. It ensures a smoother transition and less complexity for your heirs.

Navigating the Challenges: Potential Downsides to an LLC Car Loan

While the benefits are compelling, financing a car through your LLC isn’t without its potential drawbacks and complexities. Acknowledging these challenges upfront is essential for making a truly informed decision.

1. Increased Complexity and Setup Costs

Establishing and maintaining an LLC involves more administrative overhead than simply buying a car in your personal name. There are initial setup costs, which include state filing fees for forming the LLC, and potentially attorney fees if you seek legal assistance. Beyond the initial formation, LLCs often require annual report filings, registered agent fees, and adherence to specific state compliance regulations.

This ongoing administrative burden and associated costs must be weighed against the potential benefits. For very small businesses or those just starting out, the added complexity might seem daunting and potentially outweigh the advantages in the short term. It requires a commitment to proper business governance.

2. The Inevitable Personal Guarantee Requirement

This is perhaps the most significant "gotcha" for many new or small LLCs. While the LLC is a separate legal entity, most lenders will still require a personal guarantee from the business owner when the LLC is applying for its first few loans, especially for a vehicle. A personal guarantee means that if the LLC defaults on the loan, you, as the individual guarantor, become personally responsible for the debt.

The requirement for a personal guarantee can dilute the limited liability protection for the specific loan in question. However, it still provides liability protection against other business debts or general operational liabilities, and it still allows for the tax advantages. Based on my experience, very few lenders will provide an unsecured loan to a newly formed LLC without a solid credit history or significant existing business assets.

3. Loan Qualification Hurdles and Higher Rates

Newer LLCs, or those without a well-established business credit history, may find it more challenging to qualify for favorable car loan terms. Lenders often view new businesses as higher risk. This can translate into higher interest rates, stricter collateral requirements, or a lower loan amount than you might receive as an individual with excellent personal credit.

Building business credit takes time and a track record of responsible financial management. Until your LLC has a robust credit profile, you might find that lenders lean heavily on your personal credit score and require that personal guarantee, as mentioned above.

4. Strict Business Use Documentation and Scrutiny

To fully realize the tax benefits of an LLC-owned vehicle, you must meticulously document its business use. The IRS has strict rules regarding what constitutes a legitimate business expense. Any personal use of the vehicle must be clearly separated and potentially factored back into your personal income or disallowed as a business deduction.

This means keeping detailed mileage logs, receipts for all vehicle-related expenses, and clear records demonstrating the business purpose of each trip. Failing to maintain accurate records can lead to disallowance of deductions during an audit, potentially resulting in back taxes, penalties, and interest. Common mistakes to avoid are assuming that because the car is "in the business," all use is business use – this is a common misconception.

5. Potential for Personal Use Scrutiny and Tax Implications

If an LLC-owned vehicle is used for personal purposes, the IRS may view this as a taxable benefit to the owner. This could mean that the value of the personal use is considered "income" to you, or that a portion of the vehicle’s expenses must be disallowed as a business deduction. This requires careful tracking and potential adjustments at tax time.

The line between business and personal use can sometimes be blurry, and it’s an area the IRS pays close attention to. Mismanaging this aspect can lead to significant tax complications and headaches.

The Step-by-Step Process: Securing a Car Loan Through Your LLC

Successfully obtaining a car loan through your LLC involves a methodical approach. It’s more involved than simply walking into a dealership and applying for a personal loan.

Step 1: Form Your LLC and Get Organized

Before you even think about a loan, your LLC must be properly established and in good standing. This involves:

- Choosing a Unique Business Name: That complies with your state’s naming conventions.

- Appointing a Registered Agent: An individual or entity designated to receive legal documents on behalf of your LLC.

- Filing Articles of Organization: With your state’s Secretary of State or equivalent office.

- Obtaining an Employer Identification Number (EIN): From the IRS, even if you don’t have employees, as it acts as your LLC’s tax ID.

- Creating an Operating Agreement: This vital document outlines the ownership, management, and operational procedures of your LLC.

- Opening a Business Bank Account: This is non-negotiable for maintaining financial separation.

For a deeper dive into forming your LLC, you might find our article, "How to Set Up an LLC for Your Business: A Comprehensive Guide," particularly helpful.

Step 2: Establish and Build Business Credit

Lenders will assess your LLC’s creditworthiness. If your LLC is new, it likely won’t have a significant credit history. This means you’ll need to start building it.

Tips for Building Business Credit:

- Obtain a Business Credit Card: Use it responsibly and pay it off in full each month.

- Secure Small Business Loans: Even a small, short-term loan that is paid back on time can help.

- Establish Vendor Credit: Work with suppliers who report to business credit bureaus.

- Ensure Timely Payments: Pay all your business bills on time, every time.

Pro tips from us: Building business credit takes time and consistent effort. Start early, even before you need a major loan, to put your LLC in the best position.

Step 3: Find the Right Lender for Business Auto Loans

Not all banks or financial institutions offer dedicated business auto loans, especially for smaller businesses or new LLCs. You’ll need to research lenders that specialize in small business financing or have specific programs for business vehicle acquisition.

Look for:

- Traditional Banks: Many offer commercial lending divisions.

- Credit Unions: Often have competitive rates for business members.

- Online Lenders: A growing number specialize in small business loans.

- Dealership Financing: Some dealerships have business financing departments, but always compare their offers.

Compare interest rates, loan terms, down payment requirements, and any associated fees. Don’t be afraid to shop around.

Step 4: Prepare Your Application and Documentation

When you apply for a car loan through your LLC, lenders will require more extensive documentation than for a personal loan. Be prepared to provide:

- Your LLC’s Formation Documents: Articles of Organization, Operating Agreement.

- EIN Confirmation Letter.

- Business Bank Statements: Usually for the last 6-12 months.

- Business Financial Statements: Profit and Loss (P&L) statements, balance sheets.

- Business Tax Returns: For the past 2-3 years, if applicable.

- Personal Financial Information: Lenders will almost certainly request your personal tax returns, personal bank statements, and credit report, especially if a personal guarantee is required.

- A Detailed Business Plan: Especially for newer LLCs, outlining how the vehicle will be used and how it contributes to revenue.

- Vehicle Information: Make, model, VIN, purchase price.

Gathering all this information proactively will streamline the application process.

Step 5: Understand the Loan Agreement

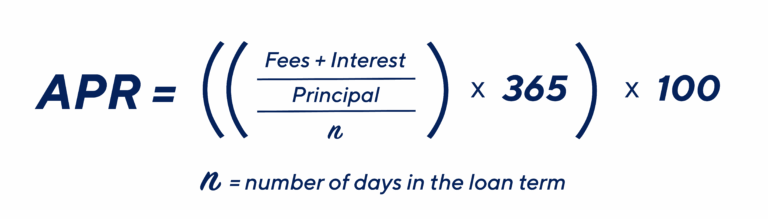

Before signing anything, meticulously review the loan agreement. Pay close attention to:

- Interest Rate and APR: Understand the true cost of borrowing.

- Loan Term: How long you have to repay the loan.

- Payment Schedule: Monthly payment amount and due dates.

- Collateral: The vehicle itself will serve as collateral, but understand if any other business assets are pledged.

- Covenants: Any conditions the lender imposes (e.g., maintaining certain financial ratios).

- Prepayment Penalties: Check if you can pay off the loan early without penalty.

- Default Clauses: Understand the consequences of missing payments.

Don’t hesitate to ask questions and seek clarification on any confusing terms.

Key Considerations Before You Dive In

Beyond the process, there are crucial strategic questions to ponder before committing to an LLC car loan.

1. Purpose of the Vehicle: Is it Genuinely for Business?

This is arguably the most critical question. The entire rationale for an LLC car loan – particularly the tax advantages – hinges on the vehicle being primarily and genuinely used for business purposes. If the car is largely for personal commuting or family errands, and only occasionally for business, the benefits diminish significantly, and the risks of IRS scrutiny increase.

Be honest about the vehicle’s intended use. If it’s 80-90% business, then an LLC loan makes sense. If it’s 80-90% personal, it might be better to finance it personally and simply claim mileage deductions.

2. Your Business Structure: Is an LLC the Best Fit?

While an LLC is excellent for many, it’s not the only business structure. Sole proprietorships, partnerships, S-Corps, and C-Corps all have different implications for asset ownership, liability, and taxation. For example, a sole proprietor can still deduct business vehicle expenses without the overhead of an LLC.

An LLC offers a good balance of liability protection and simplified taxation for many small businesses. However, it’s wise to discuss your specific business needs and long-term goals with an attorney or accountant to ensure an LLC is indeed the optimal choice for your situation.

3. Your Personal vs. Business Credit Score

Even if your LLC is the borrower, your personal credit score will likely play a significant role, especially for newer businesses. Lenders will assess both. A strong personal credit score can help you secure better rates and terms for your LLC’s first loans. Conversely, a poor personal credit score can hinder your LLC’s ability to get approved, even if the business itself is profitable.

Understand how these two credit profiles interact and take steps to improve both. A strong personal credit history is a valuable asset for your business.

4. Long-Term Financial Planning

Consider how this car loan fits into your overall business and personal financial strategy. Does it align with your cash flow projections? Are the monthly payments sustainable? How will this asset impact your balance sheet and future borrowing capacity?

Think beyond the immediate purchase. A vehicle is a depreciating asset, and its operational costs are ongoing. Ensure it’s a strategic investment that supports your business growth, rather than a financial burden.

5. Consulting Professionals: Your Essential Advisors

We cannot stress this enough: always consult with a qualified attorney and a tax professional (CPA or enrolled agent) before making major financial decisions like taking out a car loan through your LLC.

- An attorney can advise on the legal implications, proper LLC formation, and review loan documents.

- A tax professional can guide you through the intricate tax laws, ensure you maximize legitimate deductions, and help you avoid common pitfalls. For official guidance on business expenses, you can always refer to the IRS website.

These professionals are invaluable resources who can save you significant time, money, and stress in the long run.

Common Misconceptions About LLC Car Loans

Several myths often circulate around LLCs and vehicle financing. Let’s debunk a few:

Myth 1: An LLC Car Loan Automatically Shields You from All Liability.

Reality: While an LLC provides general liability protection, the common requirement for a personal guarantee on business loans for smaller entities means you are still personally responsible for that specific debt if the LLC defaults. The protection primarily extends to other business debts and operational liabilities, not necessarily the guaranteed loan itself.

Myth 2: It’s a Guaranteed Tax Dodge.

Reality: This is a dangerous misconception. The tax advantages are real, but they are contingent on strict adherence to IRS rules regarding business use and meticulous record-keeping. It’s not a loophole to avoid taxes on a personal vehicle; it’s a mechanism to deduct legitimate business expenses. Misuse can lead to severe penalties.

Myth 3: Any Car Can Be an LLC Car.

Reality: While you can technically title any car in your LLC’s name, to truly reap the benefits, especially the tax ones, the car must genuinely be used for business purposes. Buying a luxury sports car primarily for personal enjoyment and titling it under your LLC will likely raise red flags and may not stand up to audit scrutiny for its business deduction claims.

Maintaining Compliance and Maximizing Benefits

Once you’ve secured your car loan through your LLC, the journey isn’t over. Ongoing diligence is key to ensuring compliance and fully realizing the benefits.

- Separate Bank Accounts: Reiterate the importance of paying the loan and all vehicle expenses directly from your business bank account.

- Meticulous Record-Keeping: Maintain detailed mileage logs (digital apps are excellent for this), keep all receipts for fuel, maintenance, insurance, and repairs. Document the business purpose of each trip. Our article, "Essential Record-Keeping for Small Businesses: Your Blueprint for Success," offers practical advice on this.

- Annual Reports and Fees: Ensure your LLC remains in good standing with your state by filing annual reports and paying any required fees on time.

- Regular Review with Tax Advisor: Schedule annual or semi-annual meetings with your tax professional to review your vehicle’s use, deductions, and any changes in tax law that might affect your situation.

Conclusion: Driving Smart with Your Car Loan LLC

The decision to finance a vehicle through your Limited Liability Company is a strategic one, offering a powerful blend of liability protection, significant tax advantages, and enhanced professional credibility. It’s a move that can fundamentally change how your business manages a key operational asset, driving both efficiency and financial health.

However, it’s not a decision to be taken lightly. The complexities of LLC formation, the common requirement for personal guarantees, the meticulous record-keeping, and the absolute necessity of genuine business use demand careful consideration. It requires a commitment to proper business governance and a clear understanding of the regulatory landscape.

Ultimately, a Car Loan LLC can be an incredibly valuable tool for the discerning entrepreneur. By understanding the intricacies, meticulously following the process, and most importantly, consulting with trusted legal and tax professionals, you can navigate this path successfully. Make an informed decision that puts your business in the driver’s seat for sustainable growth and long-term success.