Driving Your Dream: A Comprehensive Guide on How to Get a Bank Loan for a Car

Driving Your Dream: A Comprehensive Guide on How to Get a Bank Loan for a Car Carloan.Guidemechanic.com

Purchasing a car is a significant milestone for many, offering unparalleled freedom and convenience. However, for most of us, buying a vehicle outright isn’t feasible. This is where car loans, particularly those from banks, become essential. Navigating the world of auto financing can seem daunting, but with the right knowledge and preparation, securing a bank loan for your car can be a smooth and straightforward process.

As an expert in automotive financing and a professional SEO content writer, I understand the nuances of securing favorable loan terms. This article will serve as your ultimate guide, breaking down every step, offering invaluable insights, and equipping you with the confidence to drive away in your new (or new-to-you) vehicle. We’ll explore exactly how you get a bank loan for a car, ensuring you’re well-prepared for every stage of the journey.

Driving Your Dream: A Comprehensive Guide on How to Get a Bank Loan for a Car

Why Consider a Bank Loan for Your Car?

When you’re looking to finance a vehicle, several options typically present themselves. Dealership financing is common, and sometimes direct from manufacturer. However, based on my experience, bank loans often stand out as a preferred choice for many savvy buyers. They offer distinct advantages that can significantly impact your overall cost and experience.

Banks and credit unions are financial institutions primarily focused on lending. This specialization often translates into competitive interest rates and flexible terms. Unlike a dealership, which might have preferred lenders or marked-up rates, banks are often vying for your business directly, leading to more transparent and potentially lower interest rates.

Moreover, obtaining a bank loan for your car allows you to walk into a dealership as a cash buyer. This empowers you to negotiate the car’s price without the added pressure or confusion of simultaneously negotiating financing terms. It separates the transaction, putting you in a stronger bargaining position for the vehicle itself.

Laying the Groundwork: Essential Preparation Before Applying

Before you even think about submitting a car loan application, thorough preparation is key. This initial phase is critical for improving your chances of car loan approval and securing the most favorable terms. Skipping these steps is a common mistake that can lead to higher costs and unnecessary stress.

Understanding Your Credit Score and Report

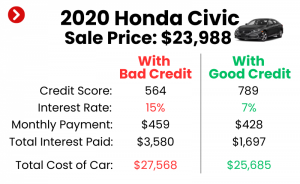

Your credit score is arguably the most crucial factor in determining your eligibility and the interest rates you’ll be offered. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay the loan. A higher score typically means lower risk for the lender, translating to better rates for you.

Pro tip from us: Before applying, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion). Review it carefully for any inaccuracies or errors. Disputing and correcting these can sometimes significantly boost your score. You can get a free report annually from AnnualCreditReport.com.

A strong credit history, demonstrated by timely payments on existing debts, contributes positively to your score. Conversely, missed payments, bankruptcies, or high credit utilization can negatively impact it. Knowing where you stand allows you to either work on improving your score or manage your expectations.

Assessing Your Financial Health

Beyond your credit score, lenders will scrutinize your overall financial situation. They want to ensure you have the stable income required to comfortably make your monthly payments. This involves looking at your employment history, income level, and existing debt obligations.

Your debt-to-income (DTI) ratio is particularly important. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover new loan payments, making you a more attractive borrower. Lenders generally prefer a DTI ratio below 36%, though some may approve loans with higher ratios depending on other factors.

Common mistakes to avoid are underestimating your current expenses or overestimating your ability to take on new debt. Be realistic about what you can truly afford each month without straining your finances.

Determining Your Budget and Down Payment

Before you start browsing cars, establish a clear budget. This isn’t just about the monthly payment; it includes the total cost of ownership, such as insurance, maintenance, fuel, and registration fees. A car loan is a significant financial commitment that extends beyond the initial purchase price.

A substantial down payment car loan can dramatically improve your loan terms. A larger down payment reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid over the life of the loan. It also reduces your loan-to-value (LTV) ratio, making the loan less risky for the bank.

Based on my experience, aiming for at least 10-20% of the car’s purchase price as a down payment is a solid strategy. For used cars, a larger down payment might be even more beneficial due to faster depreciation.

Knowing the Type of Car You Want

While you don’t need to pick the exact car before seeking financing, having a general idea is helpful. Are you looking for a new car or a used one? The age and mileage of the vehicle can affect loan terms. Banks often offer better rates for newer cars because they are less risky collateral.

New cars typically qualify for longer loan terms and sometimes promotional interest rates from manufacturers. Used cars, while often more affordable upfront, might come with slightly higher interest rates or shorter loan terms due to their higher depreciation rate and potential for unforeseen issues. Having a clear idea helps you narrow down potential lenders and understand the typical terms associated with your chosen vehicle type.

The Step-by-Step Process: How to Get a Bank Car Loan

Once you’ve done your homework and prepared your finances, you’re ready to dive into the application process. Following these steps will guide you through successfully obtaining a bank financing for your vehicle.

Step 1: Get Pre-Approved

This is perhaps the most crucial step in the entire process. Pre-approval for a car loan means a bank has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate, before you’ve even chosen a car. It’s a conditional offer, typically valid for a certain period (e.g., 30-60 days).

Why is pre-approval so important? It gives you immense negotiating power at the dealership. You walk in knowing exactly how much you can afford and what your interest rate will be. This allows you to focus solely on negotiating the car’s price, rather than getting caught up in financing discussions. It’s like having cash in hand.

To get pre-approved, you’ll typically submit an online or in-person application to various banks or credit unions. They will perform a "hard inquiry" on your credit report, which will temporarily lower your score by a few points. However, if you shop for rates within a short window (usually 14-45 days, depending on the scoring model), multiple inquiries for the same type of loan will often be treated as a single inquiry, minimizing the impact.

Step 2: Gather Required Documentation

Banks require specific documents to verify your identity, income, and residency. Having these ready will streamline your car loan application process and prevent delays. While requirements can vary slightly between lenders, here’s a common list:

- Proof of Identity: Government-issued photo ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, tax returns (especially if self-employed), or bank statements.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements showing your current address.

- Social Security Number: For credit checks.

- Vehicle Information (if applicable): If you’ve already found a car, you’ll need its VIN (Vehicle Identification Number), make, model, and mileage.

Based on my experience, having digital copies of these documents readily accessible can speed up online applications significantly.

Step 3: Compare Offers from Different Lenders

Do not settle for the first offer you receive. This is a common pitfall. Once you have your pre-approval offers (or if you’re directly applying without pre-approval), take the time to compare them thoroughly. Look beyond just the interest rate.

Consider traditional banks, local credit unions, and online lenders. Credit unions, being member-owned, often offer very competitive rates. Online lenders have streamlined processes and can also be very competitive. Each lender has its own criteria and risk assessment models, so their offers can vary widely.

Pro tip: Use an online comparison tool or spreadsheet to track offers side-by-side. Pay attention to the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing.

Step 4: Choose the Right Loan and Lender

After comparing offers, select the vehicle loan that best fits your financial situation. This means looking at more than just the lowest interest rate. Consider the entire loan package.

- Annual Percentage Rate (APR): This is the true cost of the loan, including interest and any fees. Always compare APRs, not just interest rates.

- Loan Term: How long will you be making payments? Shorter terms mean higher monthly payments but less total interest paid. Longer terms mean lower monthly payments but more interest over time. Find a balance that suits your budget and financial goals.

- Fees: Are there origination fees, application fees, or prepayment penalties? Some lenders charge these, which can add to your overall cost.

- Customer Service and Reputation: Research the lender’s reputation. Read reviews. You want a lender that is responsive and transparent.

Once you’ve made your decision, formally accept the loan offer. This usually involves signing a loan agreement.

Step 5: Finalize the Loan and Purchase Your Car

With your chosen bank loan in hand, you’re ready to make your purchase. If you have a pre-approval, you can confidently negotiate the car’s price, knowing your financing is secured.

The dealership will handle the final paperwork, which typically involves verifying your loan details with the bank. The bank will then disburse the funds directly to the dealership (or sometimes to you, to then pay the dealership). You’ll sign the final loan documents with the bank, solidifying your commitment to repay the auto loan. Ensure you read all documents carefully before signing anything.

Key Factors Influencing Car Loan Approval

Understanding what lenders look for can significantly increase your chances of car loan approval. These factors are the pillars of a strong application.

Credit Score

As mentioned, your credit score is paramount. FICO scores above 670 are generally considered good, while scores above 740 are excellent and qualify for the best car loan rates. Lenders use these scores to predict your repayment behavior.

A lower credit score doesn’t necessarily mean denial, but it will likely result in a higher interest rate to compensate the lender for the increased risk.

Income and Employment Stability

Lenders want assurance that you have a consistent and sufficient income source to meet your monthly loan obligations. They typically look for a stable employment history, ideally with the same employer for at least two years.

Self-employed individuals may need to provide more extensive documentation, such as several years of tax returns and bank statements, to prove income stability.

Debt-to-Income (DTI) Ratio

Your DTI ratio directly impacts your ability to take on new debt. A high DTI ratio signals that a significant portion of your income is already committed to existing debts, leaving less for a new car payment.

Aim to keep your total monthly debt payments, including the potential car loan, below 36-40% of your gross monthly income. This shows lenders you have ample financial breathing room.

Down Payment Amount

A larger down payment car loan acts as a buffer for the lender. It reduces their risk because you have more equity in the vehicle from day one. It also signals your commitment to the purchase.

Lenders see a substantial down payment as a positive indicator of your financial responsibility and ability to save.

Loan-to-Value (LTV) Ratio

The LTV ratio compares the amount you’re borrowing to the car’s actual value. For example, if a car is worth $20,000 and you borrow $18,000, your LTV is 90%. Lenders prefer a lower LTV because it means they are financing less of the car’s value, reducing their exposure if you default.

A larger down payment directly leads to a lower LTV, making your loan more attractive to banks.

Vehicle Age and Type

The type and age of the vehicle you intend to purchase also play a role. Banks generally prefer to finance newer vehicles with lower mileage because they are less likely to break down and hold their value better as collateral.

Financing an older or high-mileage vehicle might come with stricter terms, higher interest rates, or a requirement for a larger down payment, as the collateral is considered riskier.

Common Mistakes to Avoid When Applying for a Car Loan

Based on my experience working with countless car buyers, certain missteps frequently occur. Being aware of these can save you time, money, and frustration.

- Not Checking Your Credit Report: Failing to review your credit report for errors before applying can lead to a lower score and less favorable loan terms. Always verify your credit information.

- Applying to Too Many Lenders Simultaneously (Incorrectly): While shopping around is crucial, applying to many different lenders over an extended period can negatively impact your credit score due to multiple hard inquiries. Group your applications within a short window to minimize this effect.

- Not Getting Pre-Approved: As discussed, skipping pre-approval weakens your negotiating position at the dealership and can lead to you accepting less favorable financing terms offered on the spot.

- Focusing Only on the Monthly Payment: While important, fixating solely on the monthly payment can lead to accepting longer loan terms or higher overall interest, costing you more in the long run. Always look at the total cost of the loan.

- Ignoring Additional Fees: Be aware of any origination fees, processing fees, or prepayment penalties. These can add significantly to the overall cost of your loan.

- Buying More Car Than You Can Afford: It’s easy to get carried away at the dealership. Stick to your budget. Buying a car that stretches your finances too thin can lead to financial strain and potential default.

Pro Tips for Securing the Best Car Loan Terms

To truly optimize your chances of getting the best car loan rates and terms, consider these expert recommendations.

- Improve Your Credit Score: If you have time before buying, work on improving your credit. Pay bills on time, reduce credit card balances, and avoid opening new credit accounts. Even a few points can make a difference.

- Save for a Larger Down Payment: The more you put down, the less you borrow, and the better your loan terms will likely be. A larger down payment also builds equity faster.

- Shop Around Aggressively for Rates: Don’t just check one or two banks. Get quotes from multiple banks, credit unions, and reputable online lenders. This competition works in your favor.

- Consider a Co-signer (If Necessary): If your credit isn’t ideal, a co-signer with excellent credit can significantly improve your chances of approval and secure better terms. However, remember this person is equally responsible for the loan.

- Negotiate the Car Price Separately from the Financing: This is where pre-approval shines. With your financing secured, you can focus all your energy on getting the best possible price for the vehicle itself.

Understanding Loan Terms and Jargon

Navigating car loan discussions requires understanding some key terminology. Here’s a quick breakdown:

- APR (Annual Percentage Rate): This is the total cost of borrowing money for one year, expressed as a percentage. It includes both the interest rate and any additional fees associated with the loan. Always compare APRs for a true comparison.

- Interest Rate: The percentage charged by the lender for the money you borrow, not including other fees.

- Loan Term: The length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months).

- Principal: The original amount of money borrowed, excluding interest and fees.

- Secured Loan: A loan backed by collateral. A car loan is a secured loan because the car itself serves as collateral. If you default, the lender can repossess the vehicle.

- Unsecured Loan: A loan not backed by collateral. Personal loans are often unsecured.

- Origination Fees: A fee charged by a lender for processing a new loan application.

- Prepayment Penalties: Some loans might charge a fee if you pay off your loan early. Always check for this clause.

What to Do If Your Car Loan Application Is Denied

A denial can be disheartening, but it’s not the end of the road. It’s an opportunity to understand and improve your financial standing.

First, lenders are legally required to provide you with an adverse action notice, explaining the specific reasons for the denial. This is invaluable information. Common reasons include a low credit score, high debt-to-income ratio, insufficient income, or a short credit history.

Once you understand the reason, you can take steps to address it. This might involve working on improving your credit score, paying down existing debts to lower your DTI, or saving for a larger down payment. You might also consider applying with a co-signer or looking for a less expensive vehicle. Don’t be afraid to ask the lender for clarification or advice on what you can do to improve your chances in the future.

Conclusion: Your Path to a Successful Car Loan

Securing a bank loan for a car doesn’t have to be a stressful endeavor. By understanding the process, preparing diligently, and making informed decisions, you can confidently navigate the world of auto loan financing. From understanding your credit score to getting pre-approved and comparing offers, each step is designed to empower you with the knowledge and leverage needed for the best car loan approval.

Remember, your goal is not just to get a loan, but to get the right loan – one with competitive rates, manageable terms, and a reputable lender. By following the comprehensive advice outlined in this guide, you’re well on your way to driving off in your desired vehicle with a financial plan that truly works for you. Happy driving!