Driving Your Dream: A Comprehensive Guide to Capital One Car Loans

Driving Your Dream: A Comprehensive Guide to Capital One Car Loans Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a complex journey, but with the right guide, it becomes much clearer. For many car buyers across the United States, Capital One has emerged as a prominent player, offering a range of auto loan solutions designed to get you behind the wheel. Whether you’re eyeing a brand-new sedan, a reliable used SUV, or looking to refinance your current vehicle, understanding Capital One’s offerings is a crucial first step.

This in-depth article will serve as your ultimate resource, breaking down everything you need to know about Capital One car loans. We’ll explore their unique process, eligibility requirements, benefits, and even potential drawbacks. Our goal is to equip you with the knowledge to make an informed decision, ensuring your car buying experience is as smooth and stress-free as possible. Let’s dive in and unlock the secrets to securing your next auto loan with Capital One.

Driving Your Dream: A Comprehensive Guide to Capital One Car Loans

Why Consider Capital One for Your Auto Loan?

Capital One stands out in the competitive auto financing landscape for several compelling reasons, primarily their commitment to making car buying accessible and transparent. They’ve built a reputation for working with a wide spectrum of credit profiles, from excellent to those with less-than-perfect scores. This inclusivity means more people have a chance to secure the financing they need.

One of their most lauded features is the pre-qualification process, which allows you to see your potential loan terms without impacting your credit score. This revolutionary approach empowers buyers by giving them real financial clarity before stepping foot in a dealership. Furthermore, Capital One boasts an extensive network of approved dealerships, simplifying the car search once you have your pre-qualification in hand.

Understanding the Capital One Auto Loan Process: A Step-by-Step Journey

Securing a car loan through Capital One is designed to be a streamlined experience, centered around their innovative Auto Navigator tool. This process differs from traditional direct lending, focusing on empowering you at the dealership. Based on my experience, following these steps carefully can save you time, money, and a lot of stress.

Step 1: Pre-qualification (The Smart Start)

The journey begins with pre-qualification, a crucial first step that sets Capital One apart. This isn’t a full loan application; instead, it’s a quick, soft credit inquiry that doesn’t affect your credit score. You simply provide some basic personal and financial information, and within minutes, you’ll receive personalized offers outlining your potential interest rate and monthly payment range.

This pre-qualification gives you a significant advantage. It allows you to understand what you can realistically afford before you start shopping, eliminating guesswork and potential disappointment. You’ll know your estimated terms, empowering you to shop with confidence and focus on vehicles within your budget.

Step 2: Finding Your Dream Car with Auto Navigator

Once pre-qualified, Capital One’s Auto Navigator tool becomes your best friend. This online platform allows you to browse vehicles from approved dealerships within your pre-qualified terms. You can filter by make, model, price, and even estimated monthly payment, making your car search incredibly efficient.

The beauty of Auto Navigator is that it shows you real cars at real dealerships that fit your pre-qualified loan. This prevents you from falling in love with a car that’s outside your financial reach. When you find a car you like, the tool will update your estimated loan terms for that specific vehicle, providing unparalleled transparency.

Step 3: Visiting the Dealership and Finalizing Your Loan

With your pre-qualification offer and a car in mind, you’re ready to visit an approved dealership. Make sure to bring your pre-qualification offer, along with standard documents like your driver’s license, proof of income, and proof of residence. The dealership will then work with Capital One to finalize your loan.

This stage involves a hard credit inquiry, which is standard for any final loan application. However, because you’re already pre-qualified, the process is much smoother and faster. Common mistakes to avoid here include not thoroughly reviewing the final loan agreement for any discrepancies and feeling rushed into signing. Take your time, ask questions, and ensure all terms match your expectations.

Who is a Capital One Car Loan For? (Eligibility & Credit Scores)

Capital One prides itself on offering auto loan solutions to a broad spectrum of consumers. While specific eligibility criteria can vary, they generally look at a combination of factors including your credit history, income, and debt-to-income ratio. This holistic approach means even those with past credit challenges might find a path to financing.

- Excellent Credit: If you have a stellar credit history (typically FICO scores 780+), you’ll likely qualify for Capital One’s most competitive rates. You represent a low risk, and Capital One rewards that with favorable terms.

- Good Credit: Borrowers with good credit (FICO scores 670-739) are also strong candidates. You’ll still secure attractive rates, though perhaps not the absolute lowest, and have a wide range of vehicle options available.

- Average/Fair Credit: Capital One is known for its willingness to work with individuals in this range (FICO scores 580-669). While rates might be higher than for prime borrowers, the opportunity to get approved and rebuild credit is invaluable.

- Challenged/Bad Credit: Even if your credit score is below 580, Capital One might still offer options, particularly through their specialized programs. This demonstrates their commitment to financial inclusion, understanding that everyone deserves a chance to improve their situation. However, expect higher interest rates and potentially stricter loan terms in these scenarios.

Beyond credit score, Capital One typically requires you to be at least 18 years old and have a verifiable income. While there isn’t a universally published minimum income, it needs to be sufficient to comfortably cover the monthly payment in addition to your other financial obligations. Your debt-to-income (DTI) ratio, which measures your total monthly debt payments against your gross monthly income, is also a significant factor. A lower DTI generally indicates a healthier financial picture.

Types of Capital One Auto Loans

Capital One offers versatile financing options tailored to different car buying needs, ensuring you can find the right fit for your situation.

- New Car Loans: For those seeking the latest models, Capital One provides financing for brand-new vehicles. These loans often come with the most competitive interest rates due to the vehicle’s higher value and lower depreciation risk.

- Used Car Loans: If a pre-owned vehicle is more your style, Capital One offers robust financing for used cars as well. They typically have specific requirements for the age and mileage of the used vehicle, which you can check through their Auto Navigator tool.

- Auto Loan Refinancing: This is a fantastic option if you already have a car loan but believe you could get a better deal. Refinancing allows you to replace your existing loan with a new one, potentially lowering your interest rate, reducing your monthly payments, or shortening your loan term. Pro tips from us: consider refinancing if your credit score has improved since you took out your original loan or if market interest rates have dropped significantly.

Key Factors Affecting Your Capital One Car Loan Rate

Several critical elements come into play when Capital One determines your interest rate. Understanding these can help you position yourself for the best possible terms.

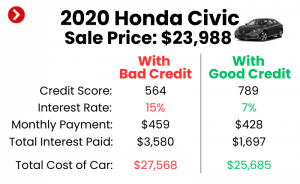

- Credit Score: This is perhaps the most significant factor. A higher credit score signals to lenders that you are a responsible borrower, leading to lower interest rates.

- Loan Term: The length of your loan also impacts the rate. Shorter loan terms (e.g., 36 or 48 months) often come with lower interest rates because the lender’s risk is reduced over a shorter period. Longer terms (e.g., 60 or 72 months) typically have higher rates.

- Down Payment: Making a substantial down payment reduces the amount you need to borrow, which can translate into a lower interest rate. It also shows the lender you’re committed to the purchase and have less risk of owing more than the car is worth.

- Vehicle Type and Age: Newer vehicles with lower mileage often qualify for better rates than older, higher-mileage cars. Certain types of vehicles, like luxury cars or those with poor resale value, might also see slightly different rates.

- Current Market Rates: The broader economic environment and the Federal Reserve’s interest rate policies can influence all lending rates, including auto loans. Rates fluctuate, so what might be a good rate today could be different next year.

Advantages of Choosing Capital One

When considering your auto financing options, Capital One brings several distinct advantages to the table that make them a popular choice.

- Pre-qualification Without Hard Inquiry: This is a game-changer. Knowing your potential terms before impacting your credit score is invaluable for smart shopping. It truly puts the power back in the buyer’s hands.

- Extensive Dealer Network: Capital One partners with thousands of dealerships nationwide, making it easy to find a participating seller for your chosen vehicle. This broad network increases your chances of finding the exact car you want within your pre-qualified terms.

- User-Friendly Tools (Auto Navigator): The Auto Navigator platform is intuitive and highly effective. It simplifies the car search by integrating financing directly into the vehicle browsing experience.

- Options for Various Credit Profiles: As discussed, Capital One is committed to serving a wide range of credit scores, including those with challenged credit. This inclusivity is a major benefit for many consumers.

- Competitive Rates: For qualified borrowers, Capital One offers highly competitive interest rates, ensuring you get a fair deal on your financing. Their transparency throughout the process helps build trust.

Potential Disadvantages & Considerations

While Capital One offers many benefits, it’s important to be aware of potential limitations or factors that might not suit every buyer.

- No Direct-to-Consumer Loans (Must Go Through Dealer): Capital One does not offer direct-to-consumer auto loans where you receive a check to buy a car anywhere. Their process is specifically tied to their network of approved dealerships. This means you can’t use a Capital One pre-qualification to buy a car from a private seller.

- Specific Vehicle Requirements: For used car loans, Capital One often has age and mileage restrictions on the vehicles they will finance. This could limit your choices if you’re looking at older or very high-mileage cars.

- Rates May Not Always Be the Absolute Lowest for Prime Borrowers: While competitive, for individuals with excellent credit, credit unions or other lenders might occasionally offer slightly lower rates, especially if you have a long-standing relationship with them. It always pays to compare.

- Limited Choice of Dealerships for Some: While the network is vast, it’s not every dealership in the country. If you have a very specific, small local dealer in mind, they might not be part of Capital One’s approved network.

Pro Tips for a Smooth Capital One Auto Loan Experience

Based on my experience in the auto financing world, a few key strategies can significantly enhance your Capital One car loan journey.

- Know Your Budget Before You Start: Before even looking at cars, determine how much you can comfortably afford for a monthly payment, insurance, and maintenance. Your pre-qualification is a guide, but your personal budget is the ultimate decider. For more details on mastering your car budget, check out our guide on .

- Get Pre-Qualified: We can’t stress this enough. It’s free, doesn’t hurt your credit, and provides invaluable information. This step empowers you to negotiate with confidence at the dealership.

- Don’t Skip the Test Drive: A car looks great online, but how does it feel to drive? Ensure the car meets your needs and expectations before committing to the financing.

- Read the Fine Print: Always, always read the entire loan agreement before signing. Understand the APR, total loan amount, any fees, and the full repayment schedule. Don’t be afraid to ask for clarification on anything you don’t understand.

- Consider a Down Payment: Even a small down payment can reduce your monthly payments, lower the total interest paid, and give you immediate equity in the vehicle. It’s a smart financial move if you can manage it.

- Evaluate Add-Ons Carefully: Dealerships often offer extended warranties, GAP insurance, and other add-ons. While some can be valuable, others may not be necessary. Understand what you’re buying and how it impacts your total loan amount.

Common Mistakes to Avoid When Applying for a Car Loan

Even with a reputable lender like Capital One, there are common pitfalls that buyers often encounter. Being aware of these can save you from costly errors.

- Not Getting Pre-Qualified: This is perhaps the biggest mistake. Without pre-qualification, you walk into the dealership blind, giving them more control over your financing options.

- Only Looking at the Monthly Payment: Focusing solely on the monthly payment can lead you to accept a longer loan term or a higher interest rate, ultimately costing you more over the life of the loan. Always consider the total cost.

- Ignoring the Total Cost of the Loan: The APR, loan term, and total amount financed all contribute to the overall cost. A seemingly low monthly payment over a very long term can result in paying significantly more in interest.

- Failing to Check Your Credit Report: Errors on your credit report can negatively impact your score, leading to higher interest rates. Always review your report for accuracy before applying for any loan. For more insights into how your credit score impacts your finances, read our article on .

- Buying More Car Than You Can Afford: It’s easy to get carried away by shiny new vehicles. Stick to your budget and avoid the temptation to overspend, even if a lender approves you for a higher amount. Just because you can get approved doesn’t mean you should take that much.

Alternatives to Capital One Auto Loans

While Capital One is an excellent option for many, it’s always wise to explore alternatives to ensure you’re getting the best possible deal.

- Local Banks and Credit Unions: These institutions often offer competitive rates, especially if you’re an existing member. Credit unions, in particular, are known for their customer-centric approach and favorable loan terms.

- Dealership Financing (Without Capital One Pre-qualification): While Capital One works with dealerships, you can also explore direct financing through the dealership itself. They work with various lenders, and sometimes special manufacturer incentives can offer very attractive rates.

- Online Lenders: Numerous online-only lenders specialize in auto loans. Companies like LightStream, Carvana, or others might offer direct-to-consumer loans or unique financing structures. Comparing their offers is a good way to ensure you’re getting the best deal.

Conclusion: Driving Forward with Confidence

Securing a car loan is a significant financial decision, and Capital One has positioned itself as a valuable partner in this journey for countless drivers. Their commitment to transparency, a user-friendly pre-qualification process, and an extensive dealer network make them a strong contender for your auto financing needs. By understanding their unique approach, leveraging their Auto Navigator tool, and being mindful of the factors influencing your loan, you can navigate the car buying process with confidence and clarity.

Remember, the ultimate goal is to find a vehicle you love at a price you can comfortably afford, financed on terms that make financial sense for you. Armed with the knowledge from this comprehensive guide, you are well-prepared to make an informed decision about a Capital One car loan and drive away in your dream car.

For more information and to begin your pre-qualification, visit the official Capital One Auto Navigator page: Capital One Auto Navigator