Driving Your Dream: A Comprehensive Guide to Navigating a 20k Monthly Car Loan

Driving Your Dream: A Comprehensive Guide to Navigating a 20k Monthly Car Loan Carloan.Guidemechanic.com

The allure of a new car is undeniable – that fresh scent, the latest technology, and the promise of new adventures. For many, a car represents freedom, a necessity, or even a statement. As you consider financing your next vehicle, you might be looking at a significant monthly commitment, perhaps even a 20k monthly car loan payment. This figure, while substantial, opens up a world of possibilities for luxury, performance, or even practicality.

But what does a 20k monthly car loan truly entail? Is it a realistic goal for you, and what steps do you need to take to secure such a loan? This super comprehensive guide will dive deep into every aspect of managing and securing a high-value car loan, ensuring you make an informed decision and drive away with confidence. We’ll explore everything from financial feasibility to application strategies, providing real value and expert insights to help you navigate this significant financial commitment.

Driving Your Dream: A Comprehensive Guide to Navigating a 20k Monthly Car Loan

Understanding the "20k Monthly Car Loan" Scenario: What Does it Really Mean?

When we talk about a 20k monthly car loan payment, we’re discussing a considerable financial outlay. This kind of payment typically implies either a very high-value vehicle, a shorter loan term for a moderately priced car, or a combination of both. It’s crucial to understand the underlying mechanics that contribute to such a substantial monthly figure.

The primary factors influencing your monthly car loan payment are the principal loan amount, the interest rate, and the loan term (duration). A higher principal, a higher interest rate, or a shorter loan term will all increase your monthly payment. Conversely, a larger down payment directly reduces the principal, thereby lowering your monthly outgo.

For instance, a 20k monthly payment could finance a luxury sedan over 5 years (60 months) with a competitive interest rate, or it could be for a premium SUV over a slightly longer term. It’s also possible that this figure represents a local currency where 20,000 units is a common, albeit high, car payment, such as in certain Asian markets. Regardless of the specific currency, the principles of affordability and loan approval remain universal.

Deconstructing Your Monthly Payment

Your monthly car loan payment isn’t just a number; it’s a carefully calculated sum. It primarily comprises two elements: the repayment of the principal amount you borrowed and the interest charged by the lender for providing that money. Over the life of the loan, especially in the initial stages, a larger portion of your payment often goes towards interest.

As the loan progresses, more of your payment starts to chip away at the principal. Understanding this amortization schedule can help you see how your money is being allocated each month. It’s a transparent way to track your progress towards full ownership and can sometimes influence decisions about early repayments.

Is a 20k Monthly Car Loan Payment Feasible for You? Budgeting Realities

Before you even begin to dream about specific car models, the most critical step is an honest assessment of your financial situation. Can you genuinely afford a 20k monthly car loan without compromising your other essential financial obligations or future goals? This isn’t just about having enough income; it’s about sustainable affordability.

Based on my experience, many people overestimate what they can comfortably afford, focusing solely on their gross income. However, true affordability comes from your net income – what you actually take home after taxes and deductions. This is the money available to cover all your expenses, including a car loan.

Comprehensive Income Assessment

Start by listing all your sources of income. This includes your salary, any bonuses, freelance earnings, or other regular inflows. Then, meticulously subtract all your fixed monthly expenses: rent/mortgage, utilities, existing loan payments (personal loans, student loans, credit cards), insurance premiums, and essential groceries. What remains is your disposable income.

This disposable income is the pool from which your 20k monthly car loan payment would need to come. If this payment consumes a disproportionately large chunk of your remaining funds, it might be a sign that it’s too high. You need to ensure there’s still enough left for emergencies, savings, and discretionary spending.

The Debt-to-Income (DTI) Ratio

Lenders extensively use your Debt-to-Income (DTI) ratio to assess your ability to manage monthly payments and repay debt. Your DTI is calculated by dividing your total monthly debt payments by your gross monthly income. For a 20k monthly car loan, lenders will be scrutinizing this number very closely.

A general guideline suggests that your total DTI, including the new car loan, should ideally be below 36-40%. Some lenders might be more flexible, but exceeding this threshold significantly can flag you as a high-risk borrower. Pro tips from us: Calculate your DTI before applying to get a realistic picture of your standing.

Beyond the Payment: The Hidden Costs of Car Ownership

A common mistake to avoid is focusing solely on the monthly car loan payment. Car ownership comes with a host of additional expenses that can quickly add up, especially for a higher-value vehicle. These "hidden" costs must be factored into your budget to truly understand affordability.

- Insurance: Higher-value cars often come with significantly higher insurance premiums. Get quotes early in your car search.

- Fuel: More powerful engines or larger vehicles typically consume more fuel. Consider your daily commute and expected mileage.

- Maintenance & Repairs: Luxury or performance vehicles can have specialized parts and service requirements, leading to higher maintenance costs.

- Registration & Taxes: Annual registration fees and potentially luxury taxes can be substantial depending on your location and the car’s value.

- Parking & Tolls: Don’t forget these everyday costs if they apply to your routine.

Key Factors for Car Loan Approval: Paving Your Way to a 20k Monthly Car Loan

Securing a significant loan like a 20k monthly car loan requires demonstrating financial responsibility and stability to lenders. They evaluate several key factors to determine your creditworthiness and the likelihood of you repaying the loan. Understanding these factors is your first step towards approval.

Your Credit Score: The Financial Report Card

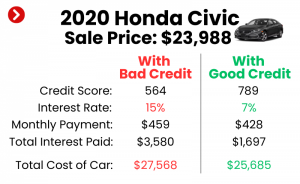

Your credit score is arguably the most critical factor lenders consider. It’s a three-digit number that summarizes your credit history, reflecting your payment behavior, outstanding debts, and credit utilization. A higher credit score (generally above 700) indicates lower risk to lenders and often qualifies you for the best interest rates.

For a 20k monthly car loan, a strong credit score is almost non-negotiable if you want competitive terms. Lenders want assurance that you have a proven track record of managing debt responsibly. If your score is lower, you might still get approved, but expect higher interest rates, which will further increase your monthly payment. .

Income Stability and Employment History

Lenders need to see a consistent and reliable source of income that can comfortably cover your potential 20k monthly car loan payment. They typically look for a stable employment history, ideally with the same employer for at least two years. Freelancers or self-employed individuals might need to provide more extensive documentation, such as tax returns for the past two to three years.

The amount of your income is also crucial. It directly impacts your Debt-to-Income (DTI) ratio, as discussed earlier. A high income makes a 20k monthly payment seem more manageable in the eyes of a lender. They want confidence that your job isn’t precarious and your earnings won’t suddenly disappear.

The Power of a Down Payment

A substantial down payment can significantly boost your chances of approval and improve your loan terms. When you put down a larger sum upfront, you reduce the principal amount you need to borrow, which in turn lowers your monthly payments or allows you to opt for a shorter loan term.

Pro tips from us: Aim for at least 20% of the car’s purchase price as a down payment, especially for a higher-value vehicle. This not only makes you a more attractive borrower but also helps mitigate depreciation, reducing the risk of being "upside down" on your loan (owing more than the car is worth).

Loan Term: The Duration of Your Commitment

The loan term, or the length of time you have to repay the loan, directly impacts your monthly payment. Shorter terms mean higher monthly payments but less interest paid over the life of the loan. Conversely, longer terms offer lower monthly payments but accumulate more interest.

For a 20k monthly car loan, you might be looking at a relatively shorter term (e.g., 3-5 years) to keep the total interest manageable, especially if the car is high-value. While a longer term might make the payment seem more accessible, common mistakes to avoid include extending the term too much, as this can lead to paying significantly more interest than the car is worth.

Vehicle Choice: New vs. Used, and Depreciation

The type of car you choose also plays a role. Lenders view new cars differently than used cars. New cars typically have lower interest rates due to their higher value and slower initial depreciation. Used cars, while often more affordable upfront, can sometimes come with slightly higher interest rates depending on their age and mileage.

The vehicle’s value and depreciation rate are also considered. Lenders are more comfortable financing cars that hold their value well, as this provides better collateral for the loan. Researching a car’s resale value can be a smart move before committing to a purchase.

The Role of a Co-signer

If your credit score or income stability isn’t strong enough to secure a 20k monthly car loan on your own, a co-signer can be a valuable asset. A co-signer, typically a family member or close friend with excellent credit, agrees to be equally responsible for the loan.

This significantly reduces the lender’s risk, as they have another party to pursue if you default. However, it’s a serious commitment for the co-signer, as any missed payments will negatively impact their credit score too. Ensure both parties fully understand the implications before proceeding.

Strategies to Secure a 20k Monthly Car Loan (and Get Approved)

Getting approved for a significant car loan isn’t just about meeting minimum requirements; it’s about presenting yourself as the ideal borrower. By strategically optimizing your financial profile and intelligently shopping for a loan, you can significantly increase your chances of securing favorable terms for your 20k monthly car loan.

Optimizing Your Financial Profile

Before you even step foot in a dealership or apply online, take proactive steps to strengthen your financial standing. This preparation can save you thousands in interest over the life of the loan.

- Boost Your Credit Score: Review your credit report for errors and dispute any inaccuracies. Make sure all your existing bills are paid on time, and try to pay down revolving credit balances (like credit cards) to improve your credit utilization ratio. Even a few points increase can make a difference.

- Reduce Existing Debt: Actively work to pay off smaller debts or reduce the balances on high-interest credit cards. A lower Debt-to-Income (DTI) ratio signals to lenders that you have more capacity to take on new debt. This demonstrates fiscal responsibility.

- Save for a Larger Down Payment: As discussed, a larger down payment reduces the loan amount and makes you a less risky borrower. It also shows foresight and discipline. Consider delaying your purchase slightly to accumulate more funds.

Shopping for the Best Loan: Don’t Settle!

Many car buyers make the mistake of only getting financing options from the dealership. While convenient, this often means missing out on potentially better rates elsewhere. Pro tips from us: Always shop around for your car loan.

- The Pre-approval Process: This is a crucial step. Apply for pre-approval with several different lenders – banks, credit unions, and online lenders. Pre-approval gives you a concrete loan offer (including the interest rate and maximum loan amount) before you visit the dealership. It empowers you to negotiate the car price as a cash buyer.

- Comparing Lenders: Don’t just look at the interest rate. Compare Annual Percentage Rate (APR), which includes all fees, and look at the loan terms. Credit unions often have very competitive rates due to their non-profit structure. Online lenders can also offer quick approvals and good rates.

- Negotiating Interest Rates: With multiple pre-approval offers in hand, you have leverage. Use a better offer from one lender to negotiate a lower rate with another, including the dealership’s finance department. Competition works in your favor.

Understanding Loan Offers: APR vs. Interest Rate

It’s vital to differentiate between the interest rate and the Annual Percentage Rate (APR). The interest rate is the cost of borrowing money, expressed as a percentage of the principal. The APR, however, includes the interest rate plus any additional fees associated with the loan, such as origination fees or processing charges.

Always compare APRs when evaluating loan offers, as this provides a more accurate picture of the total cost of borrowing. A lower interest rate might look appealing, but a higher APR due to hidden fees could mean you’re paying more overall. Transparency is key.

Common Mistakes to Avoid When Applying for a High Monthly Car Loan

Navigating a significant financial commitment like a 20k monthly car loan can be complex. There are several pitfalls that many applicants fall into, which can lead to higher costs, rejection, or even financial strain down the road. Being aware of these common mistakes can help you steer clear of them.

- Underestimating Total Car Ownership Costs: As mentioned earlier, focusing solely on the monthly payment without budgeting for insurance, fuel, maintenance, and registration is a recipe for financial stress. This is perhaps the biggest oversight for many car buyers.

- Ignoring Your Credit Report: Not reviewing your credit report before applying is a major misstep. Errors can drag down your score, and unawareness of your credit standing means you won’t know what kind of rates to expect or how to improve your position.

- Only Looking at the Monthly Payment: While important, the monthly payment alone doesn’t tell the whole story. A low monthly payment achieved by extending the loan term excessively means you’ll pay significantly more in interest over time. Always consider the total cost of the loan.

- Applying to Too Many Lenders at Once Haphazardly: Each hard inquiry on your credit report can slightly lower your score. While shopping for rates within a short window (typically 14-45 days) counts as a single inquiry, spreading applications out over months can be detrimental. Be strategic in your applications.

- Skipping the Pre-approval Step: Going into a dealership without pre-approval leaves you at the mercy of their financing options. You lose significant negotiation power on both the car price and the loan terms. Always get pre-approved first.

- Not Reading the Fine Print: Loan agreements can be complex. Common mistakes to avoid are signing without fully understanding all terms, conditions, and potential penalties (e.g., for early repayment). Always take the time to read and ask questions.

Alternatives if a 20k Monthly Payment is Too High (or Approval is Difficult)

Sometimes, despite your best efforts, a 20k monthly car loan might simply not be feasible, or you might find the approval process challenging. It’s important to have alternative strategies in mind rather than forcing a financial commitment that could lead to hardship. There are always other paths to car ownership.

Lowering Your Car Budget: Realistic Expectations

The most straightforward alternative is to reassess your car budget. If a 20k monthly payment is straining your finances, consider a less expensive vehicle. The market offers a vast range of reliable and feature-rich cars at various price points. Prioritize your needs over wants if affordability is a concern.

There’s no shame in choosing a car that fits comfortably within your budget. A more affordable car means lower monthly payments, potentially lower insurance costs, and less financial stress overall. It allows you to save for other goals and build a stronger financial foundation.

Extending the Loan Term (with Caution)

While we generally advise against excessively long loan terms due to increased interest, extending the term slightly could make a 20k monthly payment more manageable if you’re just a little off. For example, moving from a 4-year loan to a 5-year loan might reduce the monthly payment enough to fit your budget.

However, proceed with caution. Weigh the benefit of a lower monthly payment against the increased total interest paid. Ensure you won’t be "upside down" on the loan for too long, meaning the car’s value depreciates faster than you pay off the loan. This is especially risky with longer terms.

Leasing a Car: A Different Approach to Driving

Leasing is an alternative to buying that might offer lower monthly payments for a similar vehicle. When you lease, you’re essentially paying for the car’s depreciation during the lease term, plus taxes and fees. You don’t own the car, but you get to drive a new vehicle for a set period, typically 2-4 years.

Leasing can be attractive for those who enjoy driving new cars frequently and don’t want the hassle of selling. However, there are mileage restrictions, and you don’t build equity. At the end of the lease, you can return the car, buy it, or lease another one.

Exploring the Used Car Market

The used car market offers incredible value, especially for vehicles that have already taken their initial depreciation hit. You can often find a well-maintained, slightly older model of a car that would be out of budget as new. This could significantly reduce your overall loan amount and thus your monthly payment.

Based on my experience, a certified pre-owned (CPO) vehicle from a dealership can offer a good balance of value and peace of mind, often coming with extended warranties and rigorous inspections. This option can allow you to drive a premium car for a much more manageable monthly payment.

Saving More First: Delaying the Purchase

If none of the above options feel right, the most financially prudent choice might be to delay your car purchase. Use this time to save for a larger down payment, pay down existing debts, and improve your credit score. A stronger financial position will open up better loan terms and more favorable monthly payments when you are ready.

Patience is a virtue in financial planning. Waiting a few months or even a year can significantly reduce the long-term cost of your car and make your 20k monthly car loan goal, or a more affordable alternative, much more attainable and less stressful.

Pro Tips for a Smooth Car Loan Journey

Beyond the application process, there are several expert tips that can ensure your entire car loan journey, especially with a significant commitment like a 20k monthly car loan, is as smooth and financially sound as possible. These insights come from years of guiding individuals through complex financing decisions.

- Read Every Word of the Fine Print: This cannot be stressed enough. Loan documents are legally binding. Understand the interest rate, APR, loan term, prepayment penalties (if any), late payment fees, and any other clauses. If something isn’t clear, ask for clarification.

- Get Insurance Quotes Early: Before finalizing your car choice, get actual insurance quotes for the specific model. As mentioned, insurance costs vary wildly based on the car’s value, make, model, and your personal driving history. Don’t let insurance premiums surprise you after the purchase.

- Consider Gap Insurance: If you’re financing a high-value car with a relatively small down payment, gap insurance is worth considering. In the event your car is totaled or stolen, gap insurance covers the "gap" between what your standard insurance pays out (the car’s depreciated value) and the remaining balance on your loan. This prevents you from owing money on a car you no longer possess.

- Don’t Be Afraid to Walk Away: This is a powerful negotiation tactic. If a deal doesn’t feel right, if the terms are unfavorable, or if you feel pressured, be prepared to walk away. There will always be other cars and other deals. Your financial well-being is paramount.

- Keep Excellent Records: Maintain copies of all loan documents, purchase agreements, and communication with lenders or dealerships. This provides a clear paper trail should any disputes or questions arise in the future.

Conclusion: Driving Forward with Confidence

Embarking on the journey to secure a 20k monthly car loan is a significant financial decision that requires careful planning, thorough research, and an honest assessment of your financial capabilities. This article has provided you with an in-depth look at every aspect, from understanding what such a payment entails to the critical factors for approval, strategic approaches, and common pitfalls to avoid.

Remember, the ultimate goal is not just to get approved for a loan, but to secure a loan that is sustainable, affordable, and aligns with your long-term financial health. By focusing on building a strong financial profile, diligently shopping for the best loan terms, and being aware of all associated costs, you can confidently navigate the process. Drive forward with knowledge, make informed choices, and enjoy the journey in your new vehicle, knowing you’ve made a smart financial decision.