Driving Your Dream: A Comprehensive Guide to Navigating a $70,000 Car Loan Payment

Driving Your Dream: A Comprehensive Guide to Navigating a $70,000 Car Loan Payment Carloan.Guidemechanic.com

Dreaming of a new luxury sedan, a high-performance SUV, or an eco-friendly electric vehicle with all the latest tech? For many, this dream comes with a price tag around $70,000. Financing such a significant purchase requires careful planning and a deep understanding of the loan process. It’s not just about the car; it’s about making a smart financial decision that fits your lifestyle.

As an expert blogger and SEO content writer with years of experience in personal finance and automotive insights, I understand the complexities involved. This comprehensive guide will equip you with everything you need to know about securing and managing a $70,000 car loan payment, ensuring you drive away with confidence and financial peace of mind. We’ll explore the critical factors, break down the numbers, and share invaluable strategies to make this substantial investment a wise one.

Driving Your Dream: A Comprehensive Guide to Navigating a $70,000 Car Loan Payment

Understanding the Landscape of a $70,000 Car Loan

A $70,000 car loan is a significant financial commitment. This price point often indicates a vehicle that offers advanced features, superior performance, or luxury branding. Whether it’s a high-end electric vehicle, a premium family SUV, or an entry-level luxury sports car, the loan amount demands a thorough financial review.

This isn’t a decision to take lightly. It impacts your monthly budget, long-term financial goals, and overall debt profile. Therefore, understanding all facets of such a loan is paramount before you even step foot in a dealership.

What Does a $70,000 Vehicle Signify?

Vehicles in the $70,000 range typically represent a step up in quality, technology, and prestige. You’re likely looking at brands known for their engineering prowess, innovative safety features, or opulent interiors. This segment includes a wide array of options, from high-performance sedans to spacious, feature-rich SUVs and cutting-edge electric cars.

Investing in such a vehicle often means you’re prioritizing specific features, driving dynamics, or brand appeal. It’s an investment in a certain level of comfort, performance, or environmental consciousness. However, the price tag also brings higher associated costs beyond just the loan payment, which we will delve into later.

Key Factors Influencing Your $70k Car Loan Payment

Several crucial elements coalesce to determine the size of your monthly $70,000 car loan payment. Understanding each of these factors is the first step toward effective budgeting and negotiation. Based on my experience, overlooking any of these can lead to unexpected financial strain down the line.

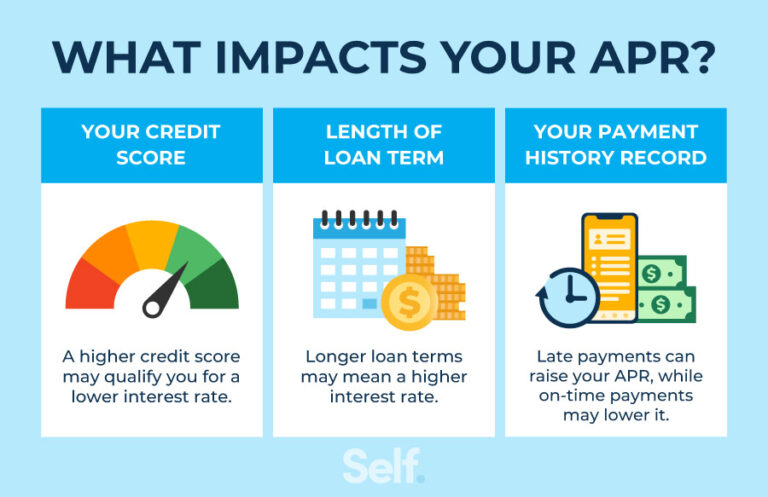

1. The Interest Rate (APR)

The interest rate, often expressed as an Annual Percentage Rate (APR), is arguably the most significant factor affecting your total loan cost and monthly payment. This is the cost you pay to borrow the money. A lower APR directly translates to less money spent over the life of the loan and a smaller monthly obligation.

Your credit score plays a colossal role in determining the interest rate you qualify for. Lenders view borrowers with excellent credit as lower risk, offering them the most favorable rates. Conversely, those with lower credit scores will face higher interest rates to compensate lenders for the perceived increased risk. Market conditions and the specific lender you choose also influence available rates.

2. The Loan Term (Repayment Period)

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 60 months, 72 months, 84 months). This factor directly impacts your monthly payment amount. A shorter loan term means higher monthly payments but less interest paid over time.

Conversely, a longer loan term will result in lower monthly payments, making the car seem more "affordable" on a month-to-month basis. However, this convenience comes at a cost: you’ll pay significantly more in total interest over the life of the loan. Common mistakes to avoid include extending the loan term too far just to reduce the monthly payment, as this can lead to being "upside down" on your loan (owing more than the car is worth).

3. Your Down Payment

A down payment is the initial amount of money you pay upfront toward the purchase of the vehicle. This reduces the principal amount you need to borrow, directly lowering your monthly payments and the total interest accrued. For a $70,000 car loan, a substantial down payment can make a significant difference.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment. Not only does this reduce your loan burden, but it also signals financial stability to lenders, potentially helping you secure a better interest rate. A larger down payment can also provide a buffer against depreciation, helping you avoid negative equity.

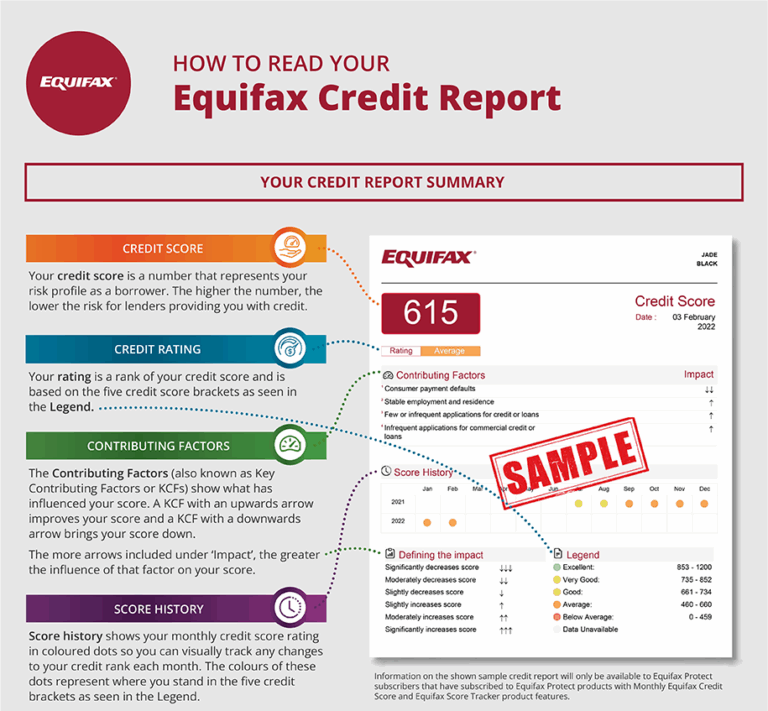

4. Your Credit Score

Your credit score is a numerical representation of your creditworthiness. Lenders use this score to assess the risk of lending money to you. Scores typically range from 300 to 850, with higher scores indicating better credit. For a substantial loan like $70,000, an excellent credit score (typically 720+) is almost essential for securing the best rates.

A strong credit history demonstrates responsible financial behavior, making lenders more willing to offer competitive interest rates and terms. If your credit score isn’t where you want it to be, taking steps to improve it before applying for a car loan can save you thousands of dollars in interest over the loan term.

5. Debt-to-Income (DTI) Ratio

Lenders also scrutinize your Debt-to-Income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. It gives lenders an idea of how much of your income is already committed to existing debts. A lower DTI ratio indicates that you have more disposable income to cover new debt payments, making you a more attractive borrower.

Generally, lenders prefer a DTI ratio below 36%, with some allowing up to 43%. If your DTI is too high, even with a good credit score, a lender might hesitate to approve a $70,000 car loan or might offer less favorable terms. This ensures you can comfortably manage your new $70,000 car loan payment without overextending your finances.

Calculating Your $70k Car Loan Payment: The Math Behind the Monthly Bill

Understanding how your monthly car loan payment is calculated is crucial for budgeting. While online car loan calculators are incredibly useful tools, knowing the underlying principles empowers you to make more informed decisions. The primary components are the principal loan amount, the interest rate, and the loan term.

Most car loans use a simple interest calculation method. This means interest is calculated on the remaining principal balance. As you make payments, a portion goes to interest, and a portion reduces the principal. Early in the loan, more of your payment goes toward interest, while later, more goes toward the principal.

Simplified Payment Calculation Example

Let’s assume a few scenarios for a $70,000 car loan (without a down payment for simplicity in this example, but always factor one in!).

The formula for a fixed-rate loan payment is:

M = P /

Where:

- M = Monthly payment

- P = Principal loan amount ($70,000)

- i = Monthly interest rate (annual rate / 12)

- n = Number of months (loan term)

Pro Tip: While understanding the formula is good, for practical purposes, always use a reliable online car loan calculator. They account for nuances and are much quicker. Sites like Bankrate or NerdWallet offer excellent tools for this purpose.

What Will Your Monthly Payment Be? Example Scenarios

To give you a clearer picture, let’s explore a few realistic scenarios for a $70,000 car loan payment, factoring in different interest rates and loan terms. These examples assume no down payment for illustrative purposes, but remember that a down payment will significantly reduce these figures.

Scenario 1: Excellent Credit, Shorter Term (60 Months)

- Loan Amount: $70,000

- Interest Rate (APR): 4.5% (for excellent credit)

- Loan Term: 60 months (5 years)

- Estimated Monthly Payment: Approximately $1,304

- Total Interest Paid: Approximately $8,240

In this scenario, the monthly payment is substantial, but you’re paying significantly less in interest over the loan’s life. This option is ideal for those with strong cash flow who want to pay off their car quickly.

Scenario 2: Good Credit, Average Term (72 Months)

- Loan Amount: $70,000

- Interest Rate (APR): 6.0% (for good credit)

- Loan Term: 72 months (6 years)

- Estimated Monthly Payment: Approximately $1,164

- Total Interest Paid: Approximately $13,808

Here, the monthly payment is more manageable, but the total interest paid increases by over $5,000 compared to Scenario 1. This is a common choice, balancing monthly affordability with a reasonable total cost.

Scenario 3: Fair Credit, Longer Term (84 Months)

- Loan Amount: $70,000

- Interest Rate (APR): 8.0% (for fair credit)

- Loan Term: 84 months (7 years)

- Estimated Monthly Payment: Approximately $1,085

- Total Interest Paid: Approximately $21,140

This scenario demonstrates the impact of a higher interest rate and a longer loan term. While the monthly payment is the lowest, the total interest paid is dramatically higher, adding over $21,000 to the original $70,000 loan. This highlights why focusing solely on the monthly payment can be a common mistake. It’s crucial to consider the total cost of the loan.

Beyond the Monthly Payment: The True Cost of Ownership

When considering a $70,000 car loan payment, it’s vital to look beyond just the loan itself. The true cost of owning a high-value vehicle extends far beyond the principal and interest. Ignoring these additional expenses can lead to budget surprises and financial stress.

1. Car Insurance Premiums

A $70,000 vehicle typically comes with significantly higher insurance premiums. Its higher value means more expensive repairs or replacement costs for the insurer. Factors like the car’s make, model, safety features, your driving record, and even where you live will influence the exact cost.

It’s wise to get insurance quotes for specific models before you finalize your purchase. This upfront research can prevent sticker shock when it comes to your monthly or bi-annual insurance bill. A car that looks affordable on paper might become a budget buster once insurance is factored in.

2. Maintenance and Repairs

Luxury or high-performance vehicles, which often fall into the $70,000 price range, generally have higher maintenance and repair costs. Specialized parts, advanced technology, and skilled labor contribute to this. Even routine services like oil changes can be more expensive.

Based on my experience, many buyers overlook this aspect. Always research the typical maintenance schedule and expected costs for your desired vehicle. Some brands offer prepaid maintenance plans, which might be worth considering if they align with your anticipated usage.

3. Fuel or Charging Costs

While not exclusive to $70,000 cars, fuel or charging costs are ongoing expenses that need to be budgeted. High-performance vehicles often require premium fuel, which costs more per gallon. Electric vehicles, while saving on gas, will add to your electricity bill, especially if you charge at home.

Consider your daily commute and typical driving habits. Even small differences in fuel efficiency can add up over time, impacting your overall monthly expenditure.

4. Registration and Taxes

Vehicle registration fees and sales taxes vary significantly by state and local jurisdiction. For a $70,000 vehicle, these upfront costs can be substantial. Some states also have annual property taxes on vehicles, which are based on the car’s value.

Always factor these one-time and recurring government fees into your budget. They are non-negotiable and can represent a significant chunk of change, especially the initial sales tax on such a high-value purchase.

5. Depreciation

Depreciation is the decline in a car’s value over time. It’s a "hidden" cost because you don’t write a check for it directly, but it impacts your equity in the vehicle. High-end cars can depreciate quickly, especially in the first few years. This means the car’s market value can fall faster than you pay down your loan, leading to negative equity.

Understanding depreciation is crucial, particularly if you plan to trade in or sell your car in a few years. It affects your ability to easily upgrade without rolling over negative equity into your next loan.

Strategies for Securing the Best $70k Car Loan

Navigating the world of car financing can be daunting, especially for a substantial amount like $70,000. However, with the right strategies, you can significantly improve your chances of securing favorable terms and a manageable $70,000 car loan payment.

1. Improve Your Credit Score

As discussed, your credit score is paramount. Before applying for a loan, check your credit report for errors and dispute any inaccuracies. Pay down existing debts, especially high-interest credit card balances, and make all payments on time. A higher credit score will open doors to lower interest rates.

Even a slight improvement in your score can save you thousands in interest over the life of a $70,000 loan. This proactive step is one of the most impactful actions you can take.

2. Save for a Larger Down Payment

A larger down payment immediately reduces the amount you need to borrow, thus lowering your monthly payments and total interest. It also demonstrates financial responsibility to lenders. For a $70,000 car, aiming for a 20% down payment ($14,000) is an excellent goal.

A substantial down payment also provides a cushion against depreciation, helping you avoid negative equity. This is particularly important for vehicles that tend to lose value quickly.

3. Shop Around for Lenders

Never settle for the first loan offer you receive, especially at a dealership. Explore options from various sources:

- Banks: Traditional banks offer competitive rates to their customers.

- Credit Unions: Often known for offering lower interest rates and more flexible terms than traditional banks.

- Online Lenders: Companies like LightStream or Capital One Auto Finance provide convenient online application processes and competitive rates.

- Dealership Financing: While convenient, dealership rates might not always be the best. Use their offer as a negotiation point.

Pro tips from us: Get pre-approved by at least two or three external lenders before you visit the dealership. This gives you leverage and a benchmark against which to compare the dealership’s offer.

4. Get Pre-Approved for a Loan

Pre-approval is a game-changer. It means a lender has conditionally agreed to lend you a specific amount at a certain interest rate, based on a preliminary review of your credit. This turns you into a cash buyer at the dealership, allowing you to focus solely on negotiating the car’s price.

Being pre-approved removes the stress of loan negotiations at the dealership, as you already know your financing options. It also helps you set a realistic budget for your car purchase.

5. Negotiate the Car Price

Even for a $70,000 vehicle, there’s often room for negotiation on the sticker price. Every dollar you shave off the purchase price is a dollar you don’t have to borrow, directly reducing your loan amount and subsequent payments. Do your research on fair market values using sites like Kelley Blue Book (KBB) or Edmunds.

Don’t be afraid to walk away if the deal isn’t right. Patience and preparedness are your best allies in car negotiations.

6. Consider a Co-Signer (If Necessary)

If your credit score is fair or you have a high DTI, a co-signer with excellent credit can help you secure a better interest rate or even get approved for the loan. However, this comes with significant responsibility for the co-signer, as they are equally responsible for the debt if you default.

Common mistakes to avoid: Only consider a co-signer if you are absolutely confident in your ability to make payments. A default will damage both your credit scores.

7. Refinancing Your Car Loan

If you’ve already secured a $70,000 car loan but your financial situation has improved (e.g., higher credit score, lower DTI), or interest rates have dropped, consider refinancing. Refinancing involves taking out a new loan to pay off your existing one, ideally with a lower interest rate or more favorable terms.

This can significantly reduce your monthly payment and the total interest you pay over time. It’s a strategy worth exploring a few months or a year after your initial purchase.

Common Mistakes to Avoid When Financing a $70k Car

Making a substantial financial commitment like a $70,000 car loan comes with potential pitfalls. Based on my experience, many individuals fall into common traps that can lead to financial strain and regret. Being aware of these can help you steer clear of them.

1. Not Budgeting Properly

One of the biggest mistakes is failing to create a comprehensive budget that accounts for all car-related expenses, not just the monthly loan payment. As discussed, insurance, maintenance, fuel, and registration can add hundreds of dollars per month to your overall cost. Overlooking these can quickly lead to an overextended budget.

Pro tip: Use the "20/4/10 Rule" as a guideline – a 20% down payment, a loan term no longer than four years, and total car expenses (including payment, insurance, fuel) should not exceed 10% of your gross monthly income. While a $70,000 car might stretch the 10% rule, it’s a good benchmark for financial health.

2. Extending the Loan Term Too Long

While longer loan terms (e.g., 84 months) result in lower monthly payments, they dramatically increase the total interest paid and keep you in debt longer. This also makes you more susceptible to negative equity, where you owe more on the car than it’s worth, especially in the early years.

Resist the temptation to stretch the loan out just for a lower monthly payment. It’s often a false economy that costs you more in the long run.

3. Skipping the Pre-Approval Process

Going into a dealership without pre-approved financing puts you at a disadvantage. You lose your negotiation leverage and might feel pressured into taking the dealer’s financing, which may not be the most competitive offer available.

Always secure at least one pre-approval from an external lender before you start test driving. This empowers you to make a deal on your terms.

4. Not Factoring in Total Cost of Ownership

As detailed earlier, the purchase price is just one piece of the puzzle. Ignoring depreciation, higher insurance for a luxury car, and potentially specialized maintenance can lead to financial surprises. A $70,000 car is not just a loan; it’s an ecosystem of ongoing expenses.

Always get an estimated total cost of ownership before committing to such a purchase. Sites like Edmunds or KBB offer tools for this.

5. Ignoring Your Credit Score

Your credit score is your financial passport. Neglecting to check it, improve it, or correct errors before applying for a loan can result in significantly higher interest rates. This oversight can cost you thousands over the life of the loan.

Make credit health a priority before any major financing decision. For those looking to improve their credit score, consider reading our detailed guide on (hypothetical internal link).

Is a $70k Car Loan Right for You? Financial Prudence is Key

Before committing to a $70,000 car loan payment, it’s crucial to perform a candid self-assessment of your financial situation. A high-value vehicle should enhance your life, not become a source of stress.

Assess Your Budget and Income

Can your current income comfortably support the estimated monthly payment, insurance, maintenance, and other associated costs? Be realistic. If the car payments will strain your budget or force you to cut back significantly on other financial goals (like saving for a home, retirement, or emergencies), it might not be the right time.

Pro tips from us: Create a detailed monthly budget that includes all your income and expenses. Ensure the new car costs don’t push you into a financially precarious position.

Prioritize Needs vs. Wants

While a $70,000 car is often a "want," ensure it aligns with your broader financial priorities. Is it a sensible purchase given your current savings, investment goals, and other debt obligations? Sometimes, delaying a luxury purchase to strengthen your financial foundation can be a wiser long-term decision.

Consider if there are more affordable alternatives that meet most of your needs without the significant financial commitment. For a deeper dive into budgeting for a luxury vehicle, read our article on (hypothetical internal link).

External Resource for Financial Planning:

For additional guidance on managing personal finances and making smart borrowing decisions, the Consumer Financial Protection Bureau (CFPB) offers valuable resources and tools. Their website provides impartial advice on loans, credit, and budgeting, which can be incredibly helpful for making informed decisions about a large purchase like a car. Visit the CFPB website for financial tools and resources (external link placeholder).

Conclusion: Driving Away with Confidence

Securing a $70,000 car loan payment is a significant financial undertaking that requires meticulous planning and a strategic approach. By understanding the core factors influencing your loan (interest rate, term, down payment, credit score, DTI), and by diligently shopping for the best rates, you can position yourself for success. Remember, the true cost of ownership extends far beyond the monthly payment, encompassing insurance, maintenance, fuel, and depreciation.

Don’t rush the process. Take the time to improve your credit, save for a substantial down payment, get pre-approved, and negotiate effectively. By avoiding common mistakes and exercising financial prudence, you can transform the dream of owning a $70,000 vehicle into a financially sound reality. Drive confidently, knowing you’ve made a smart, informed decision that aligns with your long-term financial well-being.