Driving Your Dream Car: The Ultimate Guide to Securing a 0% Interest Car Loan

Driving Your Dream Car: The Ultimate Guide to Securing a 0% Interest Car Loan Carloan.Guidemechanic.com

Imagine driving off the lot in a brand-new car, knowing that every single payment you make goes directly towards the principal. No interest charges, no hidden fees eating away at your budget – just pure equity building with every dollar. This isn’t a fantasy; it’s the enticing promise of a 0% interest car loan, also known as 0% APR (Annual Percentage Rate) financing.

While these deals sound incredibly appealing, they’re not handed out to just anyone. Securing a car loan with 0 interest requires a strategic approach, a solid financial foundation, and a keen understanding of the fine print. As an expert blogger and professional SEO content writer, I’ve delved deep into the automotive financing world, and I’m here to share everything you need to know. This comprehensive guide will equip you with the knowledge and tactics to significantly increase your chances of getting approved for one of these coveted loans.

Driving Your Dream Car: The Ultimate Guide to Securing a 0% Interest Car Loan

The Allure of 0% APR Car Loans: More Than Just a Gimmick

At its core, a 0% APR car loan means you pay absolutely no interest on the money you borrow to purchase a vehicle. If you borrow $30,000, you pay back exactly $30,000 over the life of the loan. This can translate into significant savings, potentially thousands of dollars, compared to a loan with even a low single-digit interest rate.

So, why do dealerships and manufacturers offer such seemingly generous deals? It’s a powerful marketing tool designed to attract buyers, clear out specific inventory (especially end-of-model-year vehicles), or boost sales during slower periods. For them, it’s about moving units and creating buzz. For you, it’s an opportunity to acquire a vehicle at a much lower total cost.

The benefits are undeniable. Your monthly payments become more manageable because they aren’t inflated by interest. You build equity faster, and your total cost of ownership is reduced. This makes a 0% interest loan one of the most financially advantageous ways to finance a new car, provided you meet the stringent requirements.

The Truth Behind the "Free" Money: Understanding the Catch

While the idea of a 0% interest car loan is incredibly attractive, it’s crucial to understand that these offers aren’t truly "free money." There are often trade-offs and specific conditions that make them work for both the buyer and the seller. Based on my experience in the automotive industry, many people get fixated on the "0%" and overlook these critical details.

One common scenario is that a 0% APR offer might come with a higher sticker price for the vehicle, or it might preclude you from taking advantage of other incentives, such as cash rebates. Sometimes, manufacturers offer either a 0% APR deal or a substantial cash rebate, but not both. It’s essential to compare these options thoroughly to determine which ultimately saves you more money.

Furthermore, these loans typically come with very strict eligibility criteria. Lenders and dealerships aren’t just giving away money without interest to everyone. They reserve these premium offers for their lowest-risk borrowers, meaning individuals with exceptional credit profiles and strong financial stability. Don’t be surprised if the terms are also shorter, leading to higher monthly payments, which you must be able to comfortably afford.

The Golden Ticket: Your Credit Score is Paramount

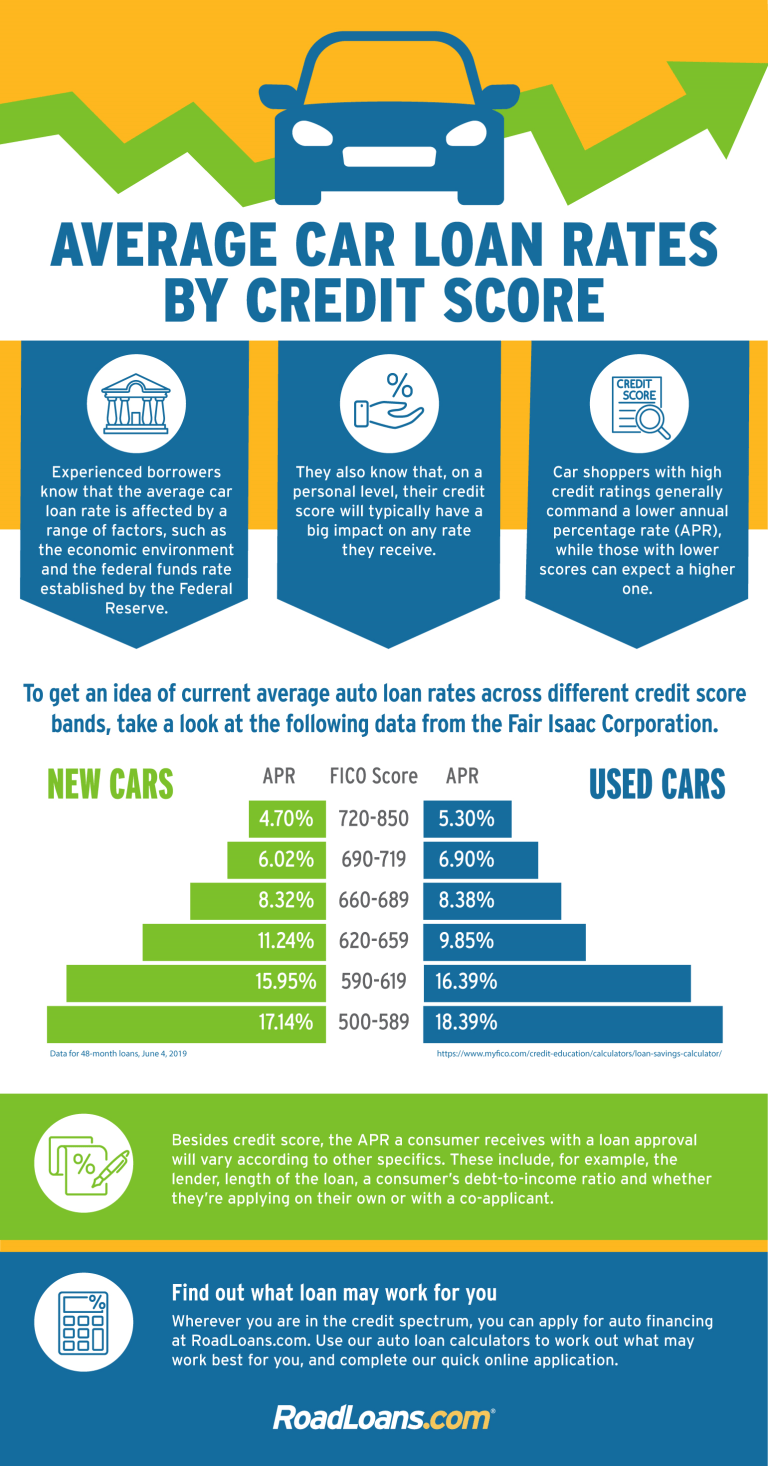

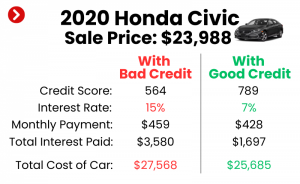

Without a doubt, the single most critical factor in securing a 0% interest car loan is an excellent credit score. This is your "golden ticket" and often the first hurdle you’ll encounter. Lenders use your credit score as a primary indicator of your financial reliability and your likelihood of repaying the loan on time.

What constitutes "excellent" credit? While the exact cutoff can vary slightly between lenders and manufacturers, generally, you’ll need a FICO score in the range of 740 to 800 or higher. Some of the most competitive 0% APR deals are reserved for those with scores comfortably above 780. Anything below this threshold significantly reduces your chances of approval for the best rates.

Pro tips from us: Don’t wait until you’re at the dealership to check your credit. Access your credit reports from all three major bureaus (Experian, Equifax, TransUnion) well in advance. Review them meticulously for any errors or inaccuracies that could be dragging your score down. Disputing errors can take time, so start this process early. For more detailed advice on improving your credit score, you might find our article "Boosting Your Credit Score: A Comprehensive Guide" helpful.

Beyond Credit: Other Key Eligibility Factors

While an impeccable credit score is non-negotiable, it’s not the only factor lenders consider when evaluating your application for a 0% APR loan. They look at your overall financial picture to ensure you can comfortably handle the monthly payments. Understanding these additional requirements will further strengthen your application.

1. A Substantial Down Payment

Lenders love a good down payment. Putting down a significant portion of the car’s purchase price reduces the amount you need to borrow, which in turn reduces the lender’s risk. While there’s no fixed rule, aiming for at least 20% of the vehicle’s price can make your application much more attractive.

A larger down payment also shows the lender your commitment and financial discipline. It demonstrates that you have skin in the game and are less likely to default on the loan. For a 0% APR loan, where the lender isn’t making money on interest, minimizing their risk through a strong down payment is even more crucial.

2. Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another critical metric. This ratio compares your total monthly debt payments (including the potential new car payment) to your gross monthly income. Lenders want to see a low DTI, typically below 36%, indicating that you have ample income to cover your existing obligations plus the new car payment without being overextended.

A high DTI suggests that you might struggle to meet your financial commitments, making you a riskier borrower in the eyes of a lender, especially for a premium 0% APR offer. Before applying, calculate your DTI and, if it’s high, look for ways to pay down existing debts to improve this ratio.

3. Stable Employment and Income Verification

Lenders need assurance that you have a steady and reliable source of income to make your monthly payments. This usually means demonstrating stable employment history, often for at least two years with the same employer. They will typically request pay stubs, W-2s, or tax returns to verify your income.

Self-employed individuals or those with fluctuating incomes might face additional scrutiny and may need to provide more extensive financial documentation. Consistency and sufficient income are key to proving your ability to repay the loan.

4. Shorter Loan Term Restrictions

0% APR offers are often tied to specific, shorter loan terms. You’ll commonly see offers for 36, 48, or 60 months, rather than the longer 72 or 84-month terms available with standard loans. While this means higher monthly payments, it also means you pay off the car faster.

It’s a trade-off: higher monthly payment for zero interest. Ensure that these higher payments fit comfortably within your budget. If a shorter term pushes your monthly payment beyond what you can reasonably afford, a 0% APR loan might not be the best fit for you, even if you qualify.

5. Specific Vehicle Eligibility

It’s rare to find 0% APR financing on every single vehicle on a dealership lot. These offers are almost always restricted to specific new models, trims, or even particular vehicle identification numbers (VINs). They are commonly used to clear out previous model year inventory or boost sales of less popular models.

Always verify which vehicles qualify for the 0% APR offer you’re interested in. Don’t assume your desired car will be eligible. Do your research online on manufacturer websites before heading to the dealership.

Your Strategic Game Plan for Securing a 0% APR Loan

Getting a 0% interest car loan isn’t about luck; it’s about meticulous preparation and smart negotiation. Here’s a step-by-step game plan, informed by years of observing successful car buyers.

Step 1: Credit Score Check-Up and Repair

As discussed, your credit score is foundational. Months before you plan to buy, obtain your credit reports from AnnualCreditReport.com. Scrutinize every detail for errors and dispute anything inaccurate immediately. Pay down high-interest credit card debt to lower your credit utilization, which can quickly boost your score. Ensure all your payments are on time – even one late payment can severely impact your chances.

Step 2: Budgeting and Aggressive Down Payment Saving

Determine your absolute maximum comfortable monthly payment. Then, work backward to see how much car that translates into, especially with shorter 0% APR terms. Simultaneously, start saving aggressively for a down payment. The more you put down, the less you borrow, and the more attractive you appear to lenders. Aim for at least 20%, but more is always better.

Step 3: Research Qualifying Vehicles and Offers

Before setting foot in a dealership, spend time online. Visit the websites of car manufacturers you’re interested in. They typically advertise their current special financing offers, including 0% APR deals, and specify which models qualify. This research will give you a clear picture of your options and prevent you from being swayed by non-qualifying vehicles.

Step 4: Understand All Your Financing Options (Even if You Aim for 0%)

Even when targeting 0% APR, it’s wise to understand what other financing options are available to you. Get pre-approved for a standard car loan from your bank or a credit union before visiting the dealership. This gives you a baseline interest rate to compare against and provides leverage in negotiations. If for some reason you don’t qualify for 0% APR, you’ll already have an alternative financing offer in hand.

Step 5: Negotiate Wisely – Focus on the Out-the-Door Price

Common mistakes to avoid are: getting so excited about the 0% APR that you forget to negotiate the actual price of the car. Remember, a 0% loan on an overpriced car might cost you more in the long run than a low-interest loan on a well-negotiated vehicle. Always negotiate the vehicle’s price first, separate from the financing. Once you agree on a price, then discuss the 0% APR offer.

Be prepared to walk away if the dealer isn’t willing to budge on the car’s price just because they’re offering 0% financing. Sometimes, they might try to recoup the "lost" interest by refusing to negotiate the sticker price or by pushing expensive add-ons.

Step 6: Read Every Line of the Fine Print

Before signing anything, meticulously read the entire loan agreement. Pay close attention to clauses regarding late payments. Many 0% APR loans revert to a much higher standard interest rate (e.g., 15-20%) if you miss even a single payment or are late. Understand any associated fees, penalties, and all the terms and conditions. If something is unclear, ask for clarification. Don’t let excitement cloud your judgment. For a deeper dive into car loan terms, check out this guide from the Consumer Financial Protection Bureau.

Common Pitfalls and How to Avoid Them

Even with the best intentions, it’s easy to make mistakes when chasing a 0% APR car loan. Being aware of these common pitfalls can save you significant money and stress.

1. Focusing Solely on APR, Ignoring Total Cost

As mentioned, the biggest mistake is tunnel vision on the 0% APR. A car loan with zero interest but a higher purchase price or fewer rebates might actually cost you more than a low-interest loan on a vehicle with a heavily negotiated price and generous incentives. Always calculate the "out-the-door" price for all options.

2. Ignoring Loan Terms and Monthly Payments

While a 0% APR is fantastic, if it’s only available on a 36-month term and your budget can only comfortably handle a 60-month payment, you could be setting yourself up for financial strain. Don’t stretch your budget beyond its limits just for the 0% rate. High monthly payments can lead to missed payments, which, as noted, can revert your loan to a high-interest rate.

3. Not Comparing Cash Rebates vs. 0% APR

Often, manufacturers offer a choice: take the 0% APR financing or a significant cash rebate. Do the math! Sometimes, taking a $2,000 or $3,000 cash rebate and financing at a low, standard interest rate (e.g., 2-3%) can result in a lower total cost than taking the 0% APR on the full sticker price. Use an online car loan calculator to compare these scenarios thoroughly.

4. Overlooking Add-ons and Extended Warranties

Dealerships make a good portion of their profit from add-ons like extended warranties, paint protection, fabric guard, and GAP insurance. While some of these might be valuable, they are often marked up significantly. When you’re focused on securing 0% APR, it’s easy to let your guard down on these extras. Scrutinize every add-on and only purchase what you truly need and understand.

5. Not Understanding Late Payment Penalties

This is a critical point that bears repeating. Many 0% APR contracts explicitly state that if you miss a payment or are late, the promotional 0% rate can be revoked, and your loan balance will revert to a much higher, standard interest rate, often retroactive to the start of the loan. This can turn a fantastic deal into a financial nightmare very quickly. Set up automatic payments to avoid this severe penalty.

When a 0% APR Loan Isn’t the Best Option

Despite their appeal, 0% APR loans aren’t always the best choice for everyone. Sometimes, other financing avenues might be more suitable for your financial situation or car preferences.

If your credit score isn’t in the excellent range, pursuing a 0% APR loan will likely lead to rejection, which can temporarily ding your credit score with hard inquiries. In such cases, focusing on a low APR loan from a bank or credit union might be a more realistic and less stressful option. You might secure a rate of 3-5%, which is still very competitive and achievable with good, but not perfect, credit.

Furthermore, 0% APR offers are almost exclusively for new vehicles. If you’re in the market for a used car, these deals are virtually non-existent. For used car purchases, your best bet will be securing the lowest possible interest rate from a reputable lender based on your creditworthiness. You can explore more about used car financing options in our blog post, "Navigating Used Car Loans: What You Need to Know."

Finally, as discussed, if a significant cash rebate is available as an alternative to the 0% APR, it’s crucial to crunch the numbers. A large rebate can sometimes offset the interest on a standard low-rate loan, resulting in a lower overall cost. Always compare the total cost of ownership under both scenarios before making a decision.

Conclusion: Your Roadmap to 0% Interest Success

Securing a 0% interest car loan is an exceptional opportunity to save a substantial amount of money on your next vehicle purchase. It’s a testament to your financial health and a reward for diligent credit management. However, it’s not a shortcut. It demands careful planning, thorough research, and smart negotiation.

By focusing on an impeccable credit score, preparing a significant down payment, understanding all the eligibility criteria, and meticulously reading the fine print, you can position yourself for success. Remember, the goal isn’t just to get 0% APR; it’s to get the best overall deal on the car you want. Approach the process strategically, and you could soon be driving off in your dream car, knowing you’ve made a truly financially savvy decision.

Have you ever secured a 0% interest car loan? What tips would you share with others? Let us know in the comments below!