Driving Your Dream: How to Secure a Car Loan with a 619 Credit Score

Driving Your Dream: How to Secure a Car Loan with a 619 Credit Score Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is exciting, but for many, the path can feel daunting, especially when a less-than-perfect credit score is involved. If your credit score hovers around the 619 mark, you’re not alone. This score falls into what’s typically considered the "fair" or "subprime" range, and while it presents some unique challenges, securing a 619 credit score car loan is absolutely within reach.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to navigate the car loan process successfully. We’ll delve deep into what a 619 credit score means for auto financing, explore actionable steps to improve your chances of approval, and uncover the best practices for securing favorable terms. Our ultimate goal is to help you drive away in the car you need, without getting stuck in a financial dead end.

Driving Your Dream: How to Secure a Car Loan with a 619 Credit Score

Understanding Your 619 Credit Score and Its Impact on Car Loans

Before we dive into strategies, let’s clarify what a 619 credit score signifies in the world of auto lending. Credit scores, like those from FICO, typically range from 300 to 850. A score of 619 places you in the "Fair" category. While this isn’t considered "bad" credit, it’s also not "good" or "excellent."

Lenders use your credit score as a primary indicator of your creditworthiness and the likelihood that you’ll repay a loan. A 619 score suggests to lenders that you might have had some past credit challenges, such as late payments, high credit utilization, or limited credit history. This can make them more cautious.

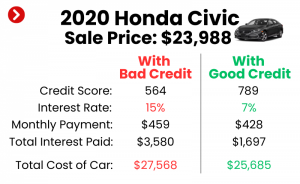

The most significant impact of a 619 credit score on a car loan is often seen in the interest rates you’ll be offered. Borrowers with higher credit scores typically qualify for the lowest Annual Percentage Rates (APRs), meaning they pay less in interest over the life of the loan. With a 619 score, you should expect to be offered higher interest rates compared to someone with a score in the 700s or 800s.

Higher interest rates translate directly to higher monthly payments and a greater total cost for the vehicle over the loan term. While it’s still possible to get approved, understanding this reality is the first step toward managing your expectations and preparing effectively. Don’t let this discourage you; instead, let it motivate you to implement the strategies we’ll discuss.

The Reality: Can You Get a Car Loan with a 619 Credit Score?

Yes, absolutely! Getting a 619 credit score car loan is definitely possible. Many lenders specialize in working with individuals who have fair or subprime credit. The auto lending market is vast, and there are options for nearly every credit profile.

However, the experience will likely differ from someone with excellent credit. You might face stricter lending criteria, require a larger down payment, or need a co-signer. The key is to be prepared, persistent, and strategic in your approach.

Based on my experience in the lending industry, lenders are primarily looking for two things: your ability to repay the loan and your willingness to do so. While your credit score reflects your past willingness, your current income, employment stability, and the amount of your down payment demonstrate your present ability.

It’s crucial to understand that not all lenders are created equal, and some are more equipped to handle applicants with credit scores in the fair range. Finding these lenders and presenting yourself as a reliable borrower will be paramount to your success. We’ll explore where to look for these opportunities shortly.

Strategic Steps to Boost Your Approval Chances

Securing a 619 credit score car loan with favorable terms requires a proactive approach. Here are several powerful strategies you can employ to significantly improve your likelihood of approval and potentially lower your interest rate.

1. Polish Your Credit Report: A Quick Credit Boost

Before you even start looking at cars, take some time to review your credit reports from all three major bureaus: Experian, Equifax, and TransUnion. You can get a free copy annually from AnnualCreditReport.com. This step is critical.

Look for any inaccuracies or errors that could be dragging your score down. This could include accounts that aren’t yours, incorrect payment statuses, or outdated negative information. Disputing and correcting these errors can sometimes give your score an immediate, albeit small, bump.

Beyond errors, identify areas for quick improvement. If you have any outstanding small debts, paying them off can reduce your credit utilization ratio, which is a significant factor in your credit score. Even paying down a credit card balance by a small amount can make a difference in a few weeks.

2. Save for a Substantial Down Payment

This is perhaps the single most impactful strategy for someone seeking a 619 credit score car loan. A significant down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk.

When you put down a larger sum, you’re signaling to the lender that you have skin in the game and are committed to the purchase. It also helps to prevent you from being "upside down" on your loan (owing more than the car is worth) early on.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment. If you can manage more, even better. This can directly influence the interest rate you’re offered and make lenders much more willing to approve your application. For example, on a $20,000 car, a $2,000 to $4,000 down payment would be ideal.

3. Consider a Co-signer

If you’re struggling to get approved or are only offered extremely high interest rates, a co-signer could be a game-changer. A co-signer is someone with good credit who agrees to take on legal responsibility for the loan if you default.

Their strong credit profile can offset your 619 score, making the loan less risky for the lender. This often results in better approval odds and significantly lower interest rates. A co-signer can be a parent, a trusted friend, or another family member.

Common mistakes to avoid are choosing a co-signer who isn’t financially stable or failing to understand the full implications for both parties. Remember, if you miss payments, it impacts both your credit and your co-signer’s credit. Ensure you and your co-signer have a clear understanding of the commitment.

4. Explore All Your Lending Options

Don’t settle for the first offer you receive, especially with a 619 credit score. It’s crucial to shop around and compare offers from various types of lenders.

- Traditional Banks and Credit Unions: Start with institutions where you already have a banking relationship. They might be more willing to work with you due based on your history with them. Credit unions, in particular, are often known for more flexible lending criteria and competitive rates for their members.

- Online Lenders: Many online lenders specialize in subprime auto loans. They use different algorithms than traditional banks and can sometimes offer more tailored solutions for fair credit borrowers. Websites like Capital One Auto Finance, LightStream, and others are worth exploring.

- Dealership Financing: Dealerships work with a network of lenders, sometimes including those who specialize in lower credit scores. While convenient, always compare their offers to what you might find elsewhere. Be wary of "buy here, pay here" lots, which often come with very high interest rates, though they are an option of last resort.

From years of observing the market, I’ve seen that getting pre-approved from multiple sources before stepping onto a dealership lot gives you immense leverage. This way, you know what kind of rates you qualify for and can negotiate confidently.

5. Know Your Budget and Be Realistic

Before you even start looking at cars, determine what you can genuinely afford. This isn’t just about the monthly payment. Consider the total cost of ownership, which includes insurance, fuel, maintenance, and potential repairs.

Lenders will look at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments (including the potential car loan) to your gross monthly income. A lower DTI indicates you have more disposable income to cover your loan payments, making you a less risky borrower.

Pro tips from us: Aim for a car payment that doesn’t strain your budget. A good rule of thumb is that your total car expenses (payment, insurance, fuel) shouldn’t exceed 10-15% of your net monthly income. Being realistic about the type of car you can afford will prevent financial stress down the line.

6. Get Pre-approved Before Visiting the Dealership

This step cannot be overstated. Getting pre-approved for a car loan before you set foot on a dealership lot is one of the most powerful tools in your arsenal when seeking a 619 credit score car loan.

Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a certain amount at a specific interest rate. This empowers you in several ways:

- You know your budget: You’ll know exactly how much you can spend, preventing you from falling in love with a car outside your financial reach.

- You become a cash buyer: From the dealership’s perspective, you’re walking in with financing already secured. This allows you to focus solely on negotiating the car’s price, rather than getting tangled in financing discussions.

- Leverage for better rates: If the dealership can beat your pre-approved rate, great! If not, you have a solid offer to fall back on. This competitive environment can save you a lot of money.

Remember that pre-approvals usually involve a "soft inquiry" on your credit, which doesn’t harm your score. Once you formally apply, it becomes a "hard inquiry." However, multiple hard inquiries for the same type of loan within a short period (typically 14-45 days) are often treated as a single inquiry by credit scoring models, so shop around efficiently.

7. Consider a Used Car

While the allure of a new car is strong, considering a used vehicle can significantly ease the burden of securing a 619 credit score car loan. Used cars are generally less expensive, which means you’ll need to borrow less money.

A lower loan amount reduces the lender’s risk and can make approval easier. Furthermore, depreciation hits new cars hardest in their first few years. Opting for a slightly used car allows you to avoid this initial sharp drop in value.

Many reliable used cars are available, and modern vehicles are built to last. Focus on well-maintained used cars from reputable dealerships or private sellers. A lower purchase price also means potentially lower insurance premiums and taxes.

Navigating the Car Loan Application Process

Once you’ve done your homework and chosen a strategy, it’s time to apply for your 619 credit score car loan. Being prepared with the right documentation will streamline the process.

Lenders will typically ask for:

- Proof of Identity: Driver’s license, passport.

- Proof of Income: Recent pay stubs (usually 2-3 months), tax returns if self-employed, bank statements.

- Proof of Residency: Utility bill, lease agreement.

- Employment Verification: Contact information for your employer.

- Social Security Number: For credit checks.

- Down Payment: Proof of funds for your down payment.

Be honest and thorough with your application. Any discrepancies can delay approval or lead to rejection. When you receive loan offers, pay close attention to the Annual Percentage Rate (APR), the loan term (number of months), and any associated fees. The APR is the most critical figure as it represents the true annual cost of borrowing, including interest and fees.

Don’t be afraid to ask questions about anything you don’t understand. A reputable lender will be transparent and willing to explain all aspects of the loan agreement.

Common Pitfalls to Avoid with a 619 Credit Score Car Loan

While the goal is to get approved, it’s equally important to avoid common mistakes that can lead to bad deals or financial strain.

- High-Pressure Sales Tactics: Dealerships want to sell cars. Some might try to rush you into a decision or add unnecessary extras. Stick to your budget and walk away if you feel pressured.

- "Buy Here, Pay Here" Dealerships: These dealerships often cater specifically to individuals with low credit scores and can be a last resort. However, they typically charge extremely high interest rates (sometimes 25% or more) and may have very strict payment schedules. While they offer easy approval, the long-term cost can be devastating. Understand the terms thoroughly before committing.

- Focusing Only on Monthly Payments: Don’t let a low monthly payment distract you from the total cost of the loan. A longer loan term might mean lower monthly payments but significantly more interest paid over time. Always consider the APR and the total amount you will pay back.

- Not Reading the Fine Print: Every loan document has terms and conditions. Read them carefully, especially sections on prepayment penalties, late fees, and what happens in case of default. If you don’t understand something, ask for clarification.

Common mistakes to avoid are signing a loan agreement that feels uncomfortable or that you don’t fully comprehend. Your financial future depends on this decision.

After Approval: Building a Better Financial Future

Congratulations, you’ve secured your 619 credit score car loan! This isn’t just about getting a car; it’s also a significant opportunity to improve your credit standing.

- Make On-Time Payments: This is paramount. Every on-time payment you make will be reported to the credit bureaus and will positively impact your credit score. Consistency is key to rebuilding your credit.

- Consider Refinancing: After 6-12 months of consistent, on-time payments, your credit score is likely to improve. At that point, you might qualify to refinance your car loan at a lower interest rate. This can save you a substantial amount of money over the remaining life of the loan.

- Monitor Your Credit: Keep an eye on your credit reports regularly. Ensure all your payments are being reported correctly and watch your score climb. This vigilance helps you spot any new errors or potential identity theft.

- Build an Emergency Fund: Having an emergency fund can prevent you from missing car payments if an unexpected expense arises. Even a small cushion can make a big difference.

By consistently managing your car loan responsibly, you’re not just paying for a vehicle; you’re investing in a stronger financial future. This journey can transform your 619 credit score into a much healthier one, opening doors to better financial products and opportunities down the line.

Conclusion: Driving Forward with Confidence

Securing a 619 credit score car loan is a realistic and achievable goal. While it requires a bit more effort and strategic planning than for those with pristine credit, the rewards of responsible car ownership and credit rebuilding are well worth it.

By understanding your credit score, implementing strategies like a significant down payment or a co-signer, diligently shopping for lenders, and being a smart consumer, you can navigate the process successfully. Remember to focus on the total cost of the loan, not just the monthly payment, and always read the fine print.

Your 619 credit score is a stepping stone, not a permanent roadblock. Use this car loan as an opportunity to demonstrate your creditworthiness and propel yourself toward a stronger financial future. With the right approach, you’ll be driving away with confidence, knowing you’ve made a smart financial decision.

External Resource: For a deeper understanding of how FICO scores are calculated and what each range means, visit the official FICO website: External Link: FICO Score Ranges Explained