Driving Your Dream: How to Secure a Car Loan With a 660 Credit Score

Driving Your Dream: How to Secure a Car Loan With a 660 Credit Score Carloan.Guidemechanic.com

A 660 credit score often sits in what’s known as the "fair" credit range. While it might not open the doors to the absolute lowest interest rates, it’s a far cry from "bad" credit and certainly doesn’t mean your dream of a new (or new-to-you) car is out of reach. In fact, countless individuals with scores in this range successfully secure car loans every day.

Based on my experience working with countless individuals navigating the auto loan landscape, a 660 credit score presents a unique opportunity. It requires a strategic approach, a bit of preparation, and a clear understanding of your financial standing. This comprehensive guide will walk you through every step, equipping you with the knowledge to not only get approved but also to secure the best possible terms for your next vehicle.

Driving Your Dream: How to Secure a Car Loan With a 660 Credit Score

Understanding Your 660 Credit Score: What It Means for a Car Loan

Before diving into the application process, it’s crucial to understand what a 660 credit score signifies to lenders. Most credit scoring models, like FICO and VantageScore, categorize scores between 580-669 as "Fair" or "Good." This places you in a position where lenders will likely see you as a moderate risk.

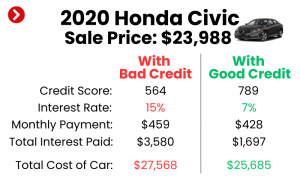

While a higher score, say above 700, would typically qualify you for prime rates, a 660 indicates you have a history of managing credit, even if there have been a few bumps along the road. Lenders will still be willing to offer you financing, but they might offset the perceived risk by offering slightly higher interest rates or requiring a larger down payment. The key is to demonstrate reliability and a commitment to responsible borrowing.

The Good News: A 660 Score Isn’t a Deal Breaker

Let’s be clear: a 660 credit score is absolutely sufficient to get a car loan. It’s a common misconception that anything less than "excellent" credit shuts you out of significant borrowing opportunities. The reality is far more nuanced.

Many lenders specialize in working with borrowers in the fair credit range, recognizing that life happens and credit scores can fluctuate. Your 660 score shows you’ve made efforts to manage your finances, and with the right strategy, you can leverage that history to your advantage. Our ultimate goal here is to help you present yourself as the most attractive borrower possible, even with a fair credit standing.

Preparation is Key: Essential Steps Before You Apply

The secret to securing a favorable car loan with a 660 credit score lies in thorough preparation. Walking into a dealership or bank without doing your homework is a common mistake that can lead to less-than-ideal outcomes. By taking these proactive steps, you’ll not only increase your chances of approval but also potentially secure better terms.

1. Know Your Credit Report Inside Out

This is perhaps the most critical first step. Your credit score is a snapshot, but your full credit report tells the story behind it. Based on my experience, many people overlook errors on their reports that could be negatively impacting their score.

Obtain a copy of your credit report from all three major bureaus (Equifax, Experian, and TransUnion). You are entitled to a free report from each bureau once every 12 months via the official Annual Credit Report website. Carefully review every entry for inaccuracies, such as incorrect late payments, accounts you don’t recognize, or incorrect balances. Dispute any errors immediately, as correcting them could give your score a crucial boost.

2. Budget Realistically: What Can You Truly Afford?

Before you even look at cars, sit down and create a detailed budget. This isn’t just about the monthly car payment; it’s about the total cost of ownership. Consider fuel, insurance, maintenance, registration fees, and potential repair costs.

Pro tips from us: Aim for your total car expenses (payment, insurance, fuel) to be no more than 10-15% of your gross monthly income. This ensures you’re not overextending yourself and can comfortably make payments without stressing your other financial obligations. Understanding your affordability limits upfront prevents you from falling in love with a car you simply cannot sustain. If you’re unsure about budgeting, our comprehensive article on Mastering Your Monthly Budget can provide invaluable insights.

3. Save for a Down Payment: Your Best Friend with Fair Credit

A significant down payment is your most powerful tool when applying for a car loan with a 660 credit score. It immediately reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

Lenders view a larger down payment favorably because it demonstrates your financial commitment and reduces their risk. A common recommendation is to put down at least 10-20% of the car’s purchase price. For used cars, aiming for 10% is a good start, while 20% is ideal for new vehicles. The more you put down, the better your chances of approval and securing a competitive interest rate.

4. Understand Interest Rates and What to Expect

With a 660 credit score, you’ll likely face higher interest rates compared to someone with excellent credit. This is simply how lenders mitigate risk. While someone with a 750+ score might get a 3-5% APR, you might see offers in the 7-12% range, or even higher depending on the market and your overall financial profile.

Don’t let this discourage you, but be prepared for it. Your goal is to get the best rate available to you, given your credit situation. Knowing what to expect prevents sticker shock and helps you evaluate offers more effectively. Focus on the total cost of the loan over its lifetime, not just the monthly payment.

5. Gather Necessary Documents

Being organized saves time and shows lenders you’re serious. Before you apply, have all your essential documents ready. This typically includes:

- Proof of Identity: Driver’s license, passport.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2s, tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, mortgage statement.

- Bank Statements: To show financial stability.

- Trade-in Information (if applicable): Title, registration, loan payoff amount.

Having these documents readily accessible streamlines the application process and can even speed up approval times.

Where to Get Your Car Loan: Exploring Your Options

With your preparations complete, it’s time to explore where to apply for your loan. Don’t limit yourself to just the dealership; exploring various lenders can significantly impact the terms you receive.

1. Credit Unions: Often a Great Starting Point

Credit unions are frequently recommended for borrowers with fair credit. They are member-owned institutions, which often translates to more flexible lending criteria and potentially lower interest rates compared to traditional banks.

They tend to prioritize their members’ financial well-being and may be more willing to work with you, especially if you have an existing relationship or are willing to open an account. It’s always a good idea to check with local credit unions first.

2. Traditional Banks: Leverage Existing Relationships

If you have a long-standing banking relationship, your bank could be another viable option. They already have access to your financial history and may offer you a more favorable rate or terms due to your existing loyalty.

However, be prepared that their approval criteria can sometimes be stricter for fair credit scores than credit unions. It’s still worth getting a quote, especially if you’ve been a loyal customer with a good track record of managing your accounts.

3. Dealership Financing: Convenience vs. Cost

Dealerships offer the convenience of a "one-stop shop" for buying a car and securing financing. They work with multiple lenders and can sometimes find options for various credit profiles. However, their primary goal is to sell you a car, and they may mark up interest rates to increase their profit.

While convenient, it’s crucial to compare their offers with pre-approvals you’ve secured elsewhere. Never assume the dealer’s first offer is the best; always negotiate.

4. Online Lenders: Quick and Diverse Options

The digital age has brought a plethora of online lenders specializing in auto loans for a wide range of credit scores. Many offer quick pre-approvals with soft credit inquiries, allowing you to shop for rates without impacting your credit score.

These lenders can be a good source for competitive rates and often have streamlined application processes. Just ensure you’re dealing with reputable companies and read reviews before committing.

The Application Process: Maximizing Your Chances

Once you’ve chosen your potential lenders, a strategic approach to the application process can significantly improve your outcome.

1. Get Pre-Approved: Your Negotiating Powerhouse

This cannot be stressed enough: get pre-approved before you step foot in a dealership. Pre-approval means a lender has reviewed your credit and financial situation and has provisionally agreed to lend you a specific amount at a specific interest rate.

This gives you immense negotiating power at the dealership. You walk in as a cash buyer, knowing exactly how much you can spend and what your interest rate will be. This allows you to focus on negotiating the car’s price, rather than being pressured into unfavorable financing terms. It’s one of the best pro tips from us for any car buyer, especially those with fair credit.

2. Consider a Co-signer: When It Makes Sense

If you’re struggling to get a competitive rate or even approval, a co-signer could be a game-changer. A co-signer, typically someone with excellent credit, agrees to be equally responsible for the loan. Their strong credit history can help you secure a lower interest rate and improve your chances of approval.

However, this comes with significant risks for the co-signer. If you miss payments, their credit score will also be negatively impacted, and they will be legally obligated to repay the debt. Only consider this option with someone you trust implicitly and who fully understands the responsibilities involved.

3. Be Strategic with Applications: The Rate Shopping Window

When applying for loans, lenders perform a "hard inquiry" on your credit report, which can temporarily lower your score by a few points. However, credit scoring models are smart enough to recognize "rate shopping" for auto loans.

Most models will treat multiple hard inquiries for the same type of loan within a specific timeframe (usually 14-45 days, depending on the model) as a single inquiry. This means you can shop around and get quotes from several lenders within this window without excessive damage to your credit score. Use this window wisely to compare offers.

4. Choose the Right Car for Your Situation

The type of car you choose can also impact your loan terms. Generally, newer cars hold their value better and are seen as less risky collateral by lenders, potentially leading to slightly better rates. However, they also come with a higher price tag.

Used cars can be more affordable upfront, but their age and mileage can sometimes lead to higher interest rates if lenders perceive them as higher risk. It’s a balance. Focus on reliable, affordable vehicles that fit your budget and loan capabilities, rather than stretching for a luxury model.

Common Mistakes to Avoid When Securing a Car Loan with Fair Credit

Even with the best intentions, it’s easy to stumble into common pitfalls. Based on my experience, here are some mistakes borrowers with a 660 credit score frequently make:

- Not Budgeting Adequately: Failing to account for all car-related expenses can lead to financial strain and missed payments down the line.

- Accepting the First Offer: Never take the first loan offer you receive, especially from a dealership. Always compare multiple offers.

- Ignoring Pre-Approval: Skipping the pre-approval step means you lose valuable negotiating leverage and might get stuck with higher rates.

- Extending Loan Terms Too Long: While a longer loan term (e.g., 72 or 84 months) lowers your monthly payment, it significantly increases the total interest you pay over time and can lead to negative equity.

- Buying More Car Than You Can Afford: Getting swept up in the excitement of a new car and exceeding your budget is a recipe for financial stress.

- Failing to Check Your Credit Report: Not reviewing your report for errors or understanding its contents is a missed opportunity to improve your standing.

After You Get the Loan: Building a Better Financial Future

Securing your car loan with a 660 credit score is a significant achievement, but it’s also an opportunity to build an even stronger financial future.

1. Make Payments On Time, Every Time

This is non-negotiable. Consistent, on-time payments are the single most effective way to improve your credit score. Set up automatic payments to avoid missing due dates. Each on-time payment reinforces your reliability to credit bureaus.

2. Consider Refinancing Down the Road

As you make consistent payments and your credit score improves (which it will, if you’re diligent), you may become eligible for a better interest rate. After 6-12 months of on-time payments, your score could easily climb into the "good" or even "very good" range.

At that point, explore refinancing your car loan. A lower interest rate can save you hundreds, if not thousands, of dollars over the remaining life of the loan. This is a smart financial move that many borrowers overlook.

3. Continue Monitoring Your Credit

Keep an eye on your credit score and report regularly. Tools are available through many banks, credit card companies, and free services that provide monthly updates. This vigilance helps you spot any potential issues early and track your progress. For more details on improving your credit score, check out our guide on How to Boost Your Credit Score Quickly.

Pro Tips for Boosting Your Credit Score (Even After Getting Your Loan)

While this article focuses on getting a loan with a 660 score, it’s worth including these actionable tips for long-term credit health, which directly ties into E-E-A-T by providing value beyond the immediate goal.

- Keep Credit Utilization Low: Aim to use no more than 30% of your available credit on credit cards. Lower is always better.

- Maintain a Good Payment History: As mentioned, this is paramount. Set reminders or automatic payments.

- Avoid Opening Too Many New Accounts: Each new credit application can cause a temporary dip in your score.

- Don’t Close Old Accounts: Older accounts with good payment histories contribute positively to the "length of credit history" factor.

- Diversify Your Credit Mix (Responsibly): A healthy mix of credit (revolving like credit cards, and installment like auto loans) can be beneficial, but only if you manage it well.

Conclusion: Your Road to a New Car is Clear

Securing a car loan with a 660 credit score is not just possible; it’s an achievable goal with the right approach. By understanding what your score means, meticulously preparing your finances, exploring various lending options, and applying strategically, you can confidently navigate the process.

Remember, your 660 credit score is a stepping stone, not a roadblock. Use this opportunity to demonstrate responsible financial behavior, not only to secure your vehicle but also to build a stronger credit future. With diligent payments and smart financial decisions, you’ll soon be driving your new car and enjoying the benefits of an improving credit score. Happy driving!