Driving Your Dream: The Ultimate Guide on How to Buy a Used Car with a Loan

Driving Your Dream: The Ultimate Guide on How to Buy a Used Car with a Loan Carloan.Guidemechanic.com

Buying a used car can be an incredibly smart financial decision, offering significant savings compared to purchasing new. When you combine this with the flexibility of a loan, it opens up a world of possibilities for finding the perfect vehicle that fits your needs and budget. However, navigating the process of how to buy a used car with a loan can feel daunting, filled with financial jargon, endless choices, and potential pitfalls.

As an expert blogger and seasoned SEO content writer, I understand the complexities involved. My mission with this comprehensive guide is to demystify the entire journey for you. We’ll dive deep into every crucial step, from setting a realistic budget and securing the right financing to inspecting your potential purchase and negotiating like a pro. This article is designed to be your ultimate pillar content, providing actionable advice and invaluable insights to ensure you make an informed, confident, and successful used car purchase with a loan. Let’s get started on the road to your next pre-owned vehicle!

Driving Your Dream: The Ultimate Guide on How to Buy a Used Car with a Loan

Section 1: Laying the Financial Groundwork – Budgeting and Loan Preparation

Before you even begin to browse listings, the most critical first step is to get your financial house in order. Understanding your financial limits and preparing for a loan will save you time, stress, and potentially a lot of money in the long run.

Understanding Your Financial Landscape

Determining your true budget goes far beyond just the sticker price of the car. Many first-time buyers make the mistake of only considering the monthly loan payment. However, the total cost of ownership includes several other significant expenses that can quickly add up.

Based on my experience, it’s essential to factor in insurance, registration fees, taxes, potential maintenance costs, and even fuel. A good rule of thumb is to dedicate no more than 10-15% of your take-home pay to your total car expenses, including the loan payment. This holistic view prevents buyer’s remorse and ensures your new-to-you car remains a joy, not a burden.

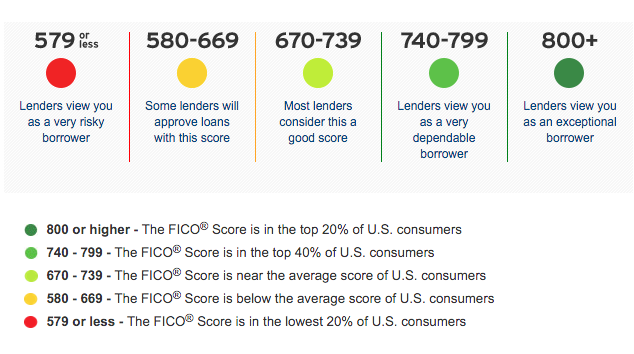

Assessing Your Credit Score

Your credit score is arguably the most influential factor when it comes to securing a car loan. Lenders use this three-digit number to gauge your financial reliability and determine the interest rate they’re willing to offer. A higher score typically translates to lower interest rates, saving you hundreds or even thousands of dollars over the life of the loan.

Pro tips from us: Obtain your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) well in advance. Review them carefully for any inaccuracies or errors that could be dragging your score down. Disputing these errors can often lead to a quick boost in your score, significantly improving your loan prospects.

Getting Pre-Approved for a Loan

One of the smartest moves you can make is to get pre-approved for a loan before you start serious car shopping. This step flips the script, putting you in a much stronger negotiating position. Instead of falling in love with a car and then scrambling for financing, you’ll know exactly how much you can afford.

The pre-approval process typically involves submitting a loan application to a bank, credit union, or online lender. They will review your credit history, income, and other financial details to determine the maximum loan amount you qualify for and an estimated interest rate. This crucial information empowers you to shop with confidence, knowing your financial boundaries.

Down Payment Strategies

A down payment is the initial sum of money you pay upfront towards the purchase of the car. While not always mandatory, making a substantial down payment offers several significant advantages. It reduces the total amount you need to borrow, which in turn lowers your monthly payments and the overall interest you’ll pay over time.

Common mistakes to avoid are underestimating the power of a down payment. Even a small down payment shows lenders your commitment and can sometimes help secure a better interest rate. Aim for at least 10-20% of the car’s value if possible, as this also provides you with immediate equity in the vehicle.

Loan Term Considerations

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). A longer loan term means lower monthly payments, which might seem appealing at first glance. However, it also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter loan term results in higher monthly payments but significantly less interest paid overall. Carefully consider your budget and financial goals when choosing a loan term. Pro tips from us: Try to strike a balance where the monthly payments are manageable, but the total interest paid isn’t exorbitant.

Section 2: Smart Car Shopping – Researching and Selecting the Right Vehicle

Once your finances are in order, the exciting part begins: finding the perfect used car. This phase requires diligent research and a clear understanding of your needs to avoid common pitfalls.

Defining Your Needs vs. Wants

Before you get swayed by flashy features, take a moment to honestly assess what you truly need in a vehicle versus what you merely want. Do you need seating for a large family, or is a compact sedan sufficient for your daily commute? Will you be hauling heavy loads, or is fuel efficiency your top priority?

Make a list of non-negotiable features and a separate list of desirable extras. This clarity will help narrow down your options and prevent you from overspending on features you wont actually use. Being realistic about your lifestyle will guide you toward a car that genuinely serves your purpose.

Researching Car Models

Not all car models are created equal, especially when it comes to pre-owned vehicles. Reliability, common mechanical issues, and the cost of parts can vary wildly between manufacturers and models. Thorough research is your best defense against buying a problematic car.

Based on my experience, reputable sources like Consumer Reports, J.D. Power, and Edmunds offer extensive reliability ratings and owner reviews. Look for models known for their longevity and relatively low maintenance costs. Pay attention to common complaints or recalls associated with specific years or trims you’re considering.

Where to Look for Used Cars

You have several avenues when searching for a used car, each with its own set of advantages and disadvantages. Dealerships, both new and used, offer convenience, financing options, and sometimes warranties. However, prices might be higher, and there could be additional dealer fees.

Private sellers often offer lower prices because they don’t have overhead costs, but the sale is typically "as-is," with less recourse if issues arise. Online marketplaces and auctions are other options, but they require extra caution and due diligence. Pro tips from us: Weigh the pros and cons of each source against your comfort level and mechanical expertise.

The Indispensable Vehicle History Report

A vehicle history report is a non-negotiable step when buying a used car. Services like CarFax and AutoCheck compile extensive data on a vehicle’s past, providing crucial insights that aren’t visible during a quick inspection. This report is your window into the car’s life story.

It typically includes information on previous accidents, flood damage, salvage titles, odometer discrepancies, service records, and the number of previous owners. Common mistakes to avoid are skipping this report to save a few dollars. It could reveal a catastrophic past that saves you from a very expensive mistake down the road. Always request and review this report before proceeding.

Section 3: The Critical Eye – Inspection and Verification

Once you’ve identified a potential vehicle, it’s time to put on your detective hat. A thorough inspection and verification process are paramount to ensure you’re not inheriting someone else’s problems.

Thorough Physical Inspection

Before you even start the engine, conduct a meticulous visual inspection of the car, both inside and out. Walk around the entire vehicle, looking for uneven paint, dents, rust, or mismatched panel gaps, which could indicate previous accident repairs. Check the tires for even wear and sufficient tread depth.

Inside, examine the upholstery for tears, stains, and excessive wear. Test all electronics: windows, locks, radio, air conditioning, and lights. Under the hood, look for any signs of fluid leaks, frayed belts, or suspicious wiring. Pro tips from us: Bring a checklist to ensure you don’t miss anything.

Test Driving the Car

A test drive is your opportunity to feel how the car performs on the road. Drive it in various conditions – city streets, highways, and even some bumpy roads if possible. Pay close attention to how it accelerates, brakes, and steers. Listen for any unusual noises: squeaks, rattles, grinding, or clunking.

Test the transmission by observing smooth gear changes, especially during acceleration and deceleration. Does the steering pull to one side? Does the brake pedal feel spongy or does the car vibrate when braking? Common mistakes to avoid are rushing the test drive; take your time and push the car a little to uncover any hidden issues.

The Pre-Purchase Inspection (PPI)

This is arguably the single most important step in buying a used car. Even if you’re mechanically inclined, nothing beats a professional, independent pre-purchase inspection by a certified mechanic you trust. This mechanic should have no affiliation with the seller.

Based on my experience, a PPI typically costs around $100-$200, but it can save you thousands in unexpected repairs. The mechanic will put the car on a lift, check for structural damage, assess the engine and transmission, inspect the suspension, brakes, and exhaust system, and look for any underlying issues that aren’t immediately apparent. If a seller resists a PPI, consider it a major red flag.

Understanding the Paperwork

Before finalizing any deal, carefully review all the documentation associated with the vehicle. This includes the car’s title, registration, and any available service records. Ensure the Vehicle Identification Number (VIN) on the title matches the VIN on the car itself (usually found on the dashboard or door jamb).

Verify that the seller is the legal owner of the vehicle. If it’s a private sale, make sure their name is on the title. If buying from a dealer, understand any warranties offered, whether they are factory, certified pre-owned, or third-party. Pro tips from us: Don’t be afraid to ask questions and take your time to read everything thoroughly.

Section 4: Navigating the Loan Approval Journey – Securing Your Financing

With your ideal car identified and thoroughly inspected, the next phase focuses on securing the best possible loan. This is where your earlier financial preparation pays off.

Comparing Loan Offers

If you followed our advice and got pre-approved, you likely have one or more loan offers in hand. Now is the time to compare them meticulously. Look beyond just the monthly payment. The Annual Percentage Rate (APR) is your most important metric, as it reflects the true cost of borrowing, including interest and any fees.

Compare the loan terms, any prepayment penalties, and late payment fees. Don’t be afraid to use the offers you have to leverage a better deal from another lender or even the dealership’s finance department. Pro tips from us: A difference of even one percentage point in APR can save you hundreds over the loan’s duration.

Understanding the Fine Print of Loan Agreements

Loan agreements can be filled with legal jargon, but it’s crucial that you understand every clause before signing. Pay close attention to the interest rate (fixed or variable), the total amount financed, the total interest paid over the life of the loan, and any associated fees like origination fees or documentation fees.

Common mistakes to avoid are rushing through this step. Ask the loan officer to explain anything you don’t understand in simple terms. Ensure that the terms you discussed and agreed upon are accurately reflected in the final document. You have the right to take the document home and review it before signing.

Options for Different Credit Scores

What if your credit score isn’t perfect? Don’t despair; there are still options for how to buy a used car with a loan. Lenders often have different tiers of loan products designed for various credit profiles. Subprime loans are available for those with lower credit scores, though they typically come with higher interest rates to offset the increased risk for the lender.

Another option is to consider a co-signer. A co-signer, usually a trusted family member or friend with excellent credit, agrees to be equally responsible for the loan if you default. This can significantly improve your chances of approval and help you secure a lower interest rate. Pro tips from us: While useful, a co-signer arrangement should be approached with extreme caution, as it impacts both parties’ credit.

Section 5: Mastering the Deal – Negotiation and Finalizing Your Purchase

You’re almost there! This stage involves skillful negotiation and careful review of the final paperwork to ensure you get the best deal possible.

Negotiation Strategies for Car Price

Negotiating the price of a used car can feel intimidating, but it’s a crucial part of the process. Remember, the listed price is rarely the final price. Start by researching the car’s market value using resources like Kelley Blue Book (KBB) or Edmunds to establish a fair baseline. This knowledge is your power.

When negotiating, always be polite but firm. Make a reasonable offer below the asking price, citing any imperfections or potential repair costs identified during your inspection. Be prepared to walk away if the deal isn’t right; there’s always another car. Pro tips from us: Focus on the out-the-door price, not just the monthly payment.

Negotiating Trade-Ins (If Applicable)

If you have a vehicle to trade in, it’s generally advisable to negotiate the price of the used car first, independent of your trade-in. Once you’ve agreed on a price for the car you’re buying, then introduce your trade-in. This prevents the dealer from muddying the waters and manipulating figures.

Research the trade-in value of your current vehicle beforehand using online tools. Be realistic about its condition. If you don’t like the trade-in offer, you always have the option to sell your old car privately, which often yields a higher return, albeit with more effort.

Understanding Additional Fees

When buying from a dealership, be prepared for various additional fees beyond the car’s price and sales tax. These can include documentation fees, registration fees, title transfer fees, and sometimes even arbitrary "prep" or "dealer services" fees. Always ask for a detailed breakdown of all charges.

Common mistakes to avoid are accepting these fees without question. While some, like registration and title fees, are unavoidable, others may be negotiable or even questionable. Challenge any fee that seems excessive or unclear. Ensure that you are only paying for legitimate services.

Finalizing the Paperwork

Once you’ve agreed on all terms – car price, trade-in value, loan terms, and fees – it’s time to sign the final purchase agreement and loan documents. This is your last chance to review everything for accuracy. Double-check all numbers, including the car’s price, down payment, loan amount, interest rate, and total amount due.

Ensure that no last-minute changes have been made without your knowledge. Take your time, read every page, and don’t hesitate to ask for clarification on anything you don’t understand. Once you sign, the deal is legally binding.

Section 6: Beyond the Sale – Protecting Your Used Car Investment

Congratulations, you’ve successfully purchased a used car with a loan! But the journey doesn’t end there. Protecting your investment ensures peace of mind and long-term satisfaction.

Car Insurance Requirements

Before you can legally drive your new-to-you car off the lot, you’ll need to secure proper car insurance. Since you’ve financed the vehicle, your lender will almost certainly require you to carry full coverage insurance, including collision and comprehensive coverage. This protects their investment in case of an accident or theft.

Shop around for insurance quotes from multiple providers to find the best rates. Based on my experience, getting quotes before you finalize the car purchase can help you budget accurately, as insurance costs can vary significantly depending on the vehicle’s make, model, year, and your driving history.

Extended Warranties (Pros and Cons)

Dealerships or third-party providers may offer extended warranties for used cars. These plans cover specific mechanical failures beyond the manufacturer’s original warranty or the limited warranty offered by the dealer. While they can provide peace of mind, they also come with a cost.

Carefully weigh the pros and cons. Consider the car’s reliability ratings, your financial comfort with unexpected repairs, and the cost of the warranty itself. Pro tips from us: Read the fine print of any extended warranty very carefully, understanding what is and isn’t covered, deductibles, and the claims process. Often, a dedicated emergency fund for repairs is a more cost-effective solution.

Maintenance Schedule

One of the best ways to protect your used car and ensure its longevity is to adhere strictly to a regular maintenance schedule. Consult the owner’s manual for recommended service intervals, or find an online version if a physical copy isn’t available. This includes routine oil changes, tire rotations, fluid checks, and filter replacements.

Staying on top of maintenance not only prevents major breakdowns but also helps maintain the car’s value. A well-maintained vehicle will perform better, be safer, and ultimately cost you less in the long run.

Registration and Titling

The final administrative steps involve properly registering and titling your vehicle with your state’s Department of Motor Vehicles (DMV) or equivalent agency. If you purchased from a dealership, they typically handle this process for you, adding the fees to your purchase price. However, if you bought from a private seller, you’ll be responsible for completing these steps yourself.

Ensure all paperwork is correctly filled out and submitted within your state’s specified timeframe to avoid penalties. You’ll receive your new license plates, registration, and eventually the title (which the lender will hold until the loan is paid off).

Conclusion: Driving Away with Confidence

Buying a used car with a loan is a significant financial decision, but by following these detailed steps, you can approach the process with confidence and clarity. From meticulously preparing your finances and thoroughly researching vehicles to performing critical inspections and skillfully negotiating, every stage plays a vital role in securing a successful outcome.

Remember, patience and due diligence are your greatest allies. Don’t rush into a purchase, and always prioritize transparency and understanding throughout the entire transaction. By empowering yourself with knowledge, you’re not just buying a car; you’re making a smart investment in your future mobility.

We hope this guide has provided you with invaluable insights into how to buy a used car with a loan. For more expert advice on managing your automotive finances, check out our article on or . And for a deeper dive into vehicle history reports, visit a trusted external source like CarFax: https://www.carfax.com/.

Happy driving, and may your new-to-you car bring you many miles of reliable and enjoyable journeys!