Driving Your Dream: The Ultimate Guide to Finding the Best Car Loans for Military Personnel and Veterans

Driving Your Dream: The Ultimate Guide to Finding the Best Car Loans for Military Personnel and Veterans Carloan.Guidemechanic.com

Serving our country comes with immense pride, unique challenges, and a distinct financial landscape. For active duty military personnel, reservists, veterans, and military families, purchasing a car is often a necessity, but navigating the loan process can feel like another deployment. You might face unique hurdles like frequent Permanent Change of Station (PCS) moves, deployments, or the complexities of building credit while often being away from home.

This comprehensive guide is designed to empower you with the knowledge and resources to secure the best car loans for military members and veterans. We’ll delve into specific lenders, crucial financial considerations, and pro tips to ensure you drive away with a great deal, not a financial burden. Our ultimate goal is to simplify this process, providing you with real value and actionable insights every step of the way.

Driving Your Dream: The Ultimate Guide to Finding the Best Car Loans for Military Personnel and Veterans

Understanding the Unique Financial Landscape for Military Members

Military life is dynamic, and your financial situation often mirrors that fluidity. Unlike civilians who might stay in one place for decades, service members frequently relocate, impacting everything from local banking relationships to credit history. These unique circumstances mean that standard car loan options might not always be the most advantageous fit for you.

Deployments can also affect income consistency and access to financial services, while the process of moving from base to base can make establishing a stable credit profile challenging. Lenders who understand these nuances are often better equipped to offer flexible and favorable terms specifically tailored to the military community. It’s not just about getting a loan; it’s about getting a loan that truly understands and accommodates your service.

Key Factors When Choosing a Military Car Loan

Selecting the right car loan involves more than just looking at the monthly payment. Based on my experience in financial advising for military families, several critical factors must be thoroughly evaluated to ensure you’re getting a truly beneficial deal. Overlooking any of these can lead to significant long-term costs.

Interest Rates (APR)

The Annual Percentage Rate (APR) is arguably the most crucial factor. It represents the total cost of borrowing money, including the interest rate and certain fees, expressed as a yearly percentage. A lower APR directly translates to less money paid over the life of the loan. Even a seemingly small difference of one or two percentage points can save you thousands of dollars, especially on larger loan amounts or longer terms. Always compare APRs, not just interest rates, as it gives you the full picture of the loan’s cost.

Loan Terms

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term generally means higher monthly payments but significantly less interest paid overall. Conversely, a longer term offers lower monthly payments, which might seem appealing, but it results in paying much more in interest over time. Common mistakes to avoid are automatically opting for the longest term for the lowest payment without considering the total cost.

Fees and Charges

Hidden fees can quickly add up, increasing the true cost of your car loan. Always ask about potential charges such as origination fees, application fees, or prepayment penalties. Some lenders might charge a fee if you pay off your loan early, which can negate the benefit of accelerated payments. Transparent lenders will clearly outline all associated fees upfront, allowing you to make a fully informed decision.

Down Payment

Making a substantial down payment can significantly reduce your monthly payments and the total interest paid over the life of the loan. It also demonstrates to lenders that you are a serious and responsible borrower, which can sometimes help secure a lower interest rate. Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment if your financial situation allows. This also reduces the risk of being "upside down" on your loan, where you owe more than the car is worth.

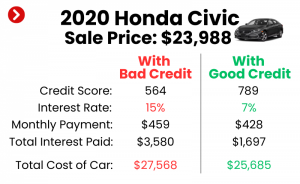

Credit Score Impact

Your credit score is a vital component in determining the interest rate you qualify for. Lenders use it as a primary indicator of your creditworthiness. A higher credit score signals lower risk, typically leading to more favorable interest rates and better loan terms. If your credit score isn’t where you want it to be, taking steps to improve it before applying for a car loan can save you a substantial amount of money. We’ll discuss credit building tips later in this guide.

Top Lenders for Military Car Loans

Fortunately, several financial institutions specialize in serving the military community, understanding their unique needs and often offering highly competitive rates and flexible terms. These are typically your first and best options when seeking car loans for military personnel.

Military-Specific Credit Unions

Credit unions are often heralded as the best choice for military auto financing due to their member-focused approach and not-for-profit structure. This often translates to lower interest rates and fewer fees compared to traditional banks.

- Navy Federal Credit Union (NFCU): Widely recognized as a top choice, Navy Federal offers competitive auto loan rates for new and used vehicles. They cater to all branches of the military, veterans, and their families. Their benefits often include pre-approval options, no down payment requirements for qualified members, and flexible repayment terms, making them an excellent resource for active duty car loans. Based on my experience, their customer service is also highly attuned to military life challenges.

- USAA: Another cornerstone of military financial services, USAA provides auto loans with competitive rates for both new and used vehicles. They are known for their comprehensive services that extend beyond banking to insurance, offering a seamless experience for military members. USAA’s understanding of PCS moves and deployments can be invaluable, often making the financing process smoother for those in active service.

- PenFed Credit Union (Pentagon Federal Credit Union): PenFed offers strong auto loan programs with attractive rates, often extending special offers for military members. They provide financing for new, used, and even refinance loans, catering to a broad spectrum of needs. Like other credit unions, their focus is on member benefits, which can include discounts and personalized service.

Traditional Banks (with Military Programs)

While credit unions often lead the pack, some traditional banks also offer specific programs or advantages for military personnel. It’s always worth checking with your existing bank, especially if you have a long-standing relationship.

- Chase Bank: Chase offers a "Military Banking" program which includes benefits like no monthly service fees on checking accounts. While they don’t always have explicit "military car loans," their preferred customer status or special promotions might provide competitive rates for service members. It’s essential to inquire directly about any specific auto loan benefits for military personnel.

- Bank of America: Similar to Chase, Bank of America provides banking solutions for military members and veterans. They offer competitive auto loan rates and it’s prudent to discuss any potential discounts or specialized loan products they might have for service members. Leveraging an existing banking relationship can sometimes simplify the application process.

Online Lenders

The digital age has brought a plethora of online lenders, some of whom specialize in niche markets or offer streamlined application processes. While not all are military-focused, some provide competitive rates and convenience.

- LightStream: A division of Truist Bank, LightStream is known for its low-interest, unsecured personal loans that can be used for various purposes, including car purchases. While not exclusively military, their strong credit requirements can lead to excellent rates for service members with good credit. The application is entirely online, offering speed and convenience.

- Carvana/Vroom (Online Car Retailers with Financing): These platforms allow you to buy a car entirely online, including financing. While they don’t specifically target military members, their convenience can be a huge advantage for service members who are deployed or frequently moving. Always compare their financing offers with pre-approvals from credit unions to ensure you get the best deal.

Special Considerations for Military Car Buyers

The unique aspects of military life demand special attention when it comes to car financing. Being prepared for these situations can save you stress and money.

Bad Credit Military Car Loans

Building credit can be challenging when you’re frequently moving or deployed. If you have a low or no credit score, securing a car loan might seem daunting. However, options exist:

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and help secure a better interest rate. Ensure both parties understand the full implications and responsibilities.

- Secured Loans: These loans use an asset, often the car itself, as collateral. While they can be easier to obtain with bad credit, they typically come with higher interest rates.

- Smaller, Less Expensive Car: Opting for a more affordable vehicle reduces the loan amount, making it easier to get approved and manage payments. This is a practical step towards rebuilding credit.

- Common mistakes to avoid: Falling prey to predatory lenders who offer "guaranteed approval" but charge exorbitant interest rates and hidden fees. Always research a lender thoroughly and compare multiple offers.

No Credit/Thin Credit

Many young service members enter the military without an established credit history. This "thin file" can be a hurdle for lenders.

- Secured Credit Cards: Start building credit with a secured credit card, making small purchases and paying them off in full each month.

- Credit Builder Loans: Some credit unions offer specific "credit builder" loans designed to help you establish a positive credit history.

- Authorized User: Becoming an authorized user on a family member’s established credit card account can help, provided they have a good payment history.

PCS and Deployments

Frequent moves and deployments are inherent to military service and can complicate car ownership and financing.

- Vehicle Registration and Insurance: Be aware that state vehicle registration and insurance requirements change with each PCS. Ensure your loan provider is flexible and understands these movements.

- Power of Attorney: If you’re deploying, establish a Power of Attorney (POA) for someone you trust to handle vehicle-related matters, including payments or registration renewals, in your absence.

- Loan Deferment Options: Some military-friendly lenders offer loan deferment options during deployments. Always inquire about these possibilities before you deploy.

SCRA (Servicemembers Civil Relief Act)

The Servicemembers Civil Relief Act (SCRA) is a federal law designed to protect service members from certain financial burdens while on active duty. This is a critical piece of legislation that every service member should understand.

- Interest Rate Cap: For loans taken out before active duty service, SCRA caps interest rates at 6% per year during your period of service. This can significantly reduce your monthly payments and total interest paid on existing loans, including car loans.

- Foreclosure and Repossession Protection: SCRA also provides protections against foreclosure, repossession, and eviction under certain circumstances. It’s a powerful tool designed to ease the financial strain of active duty. For more detailed information on your rights under SCRA, you can visit a trusted external source like the Consumer Financial Protection Bureau (CFPB) website.

VA Car Loans (Clarification)

It’s a common misconception that the Department of Veterans Affairs (VA) directly offers car loans. The VA does not provide auto loans. However, VA benefits, such as disability compensation, can free up personal funds that can then be used for a larger down payment on a car or to make monthly payments more manageable. Some states also offer specific grants for veterans with service-connected disabilities to assist with vehicle modifications.

The Car Buying Process: A Military Member’s Checklist

Navigating the car buying process can be overwhelming. Follow these steps for a smooth and informed experience. Pro tips from us: preparation is key to saving money and avoiding stress.

- Budgeting and Affordability: Before anything else, determine how much car you can truly afford. Consider not just the monthly loan payment, but also insurance, fuel, maintenance, and potential registration costs. Create a realistic budget to avoid financial strain.

- Check Your Credit Score and Report: Obtain a free copy of your credit report from AnnualCreditReport.com. Review it for any errors and understand your current credit score. This knowledge empowers you during the loan application process.

- Get Pre-Approval: This is a non-negotiable step. Seek pre-approval from at least 2-3 military-friendly credit unions or banks before you even step foot on a dealership lot. Pre-approval gives you a firm offer, sets a maximum loan amount, and allows you to negotiate as a cash buyer, focusing solely on the car’s price.

- Research Vehicles: Decide whether a new or used car best fits your needs and budget. Research reliability ratings, safety features, and resale values. Consider vehicles that are practical for military life, such as those with good fuel economy or ample storage for gear.

- Dealership Negotiation: With your pre-approval in hand, you have leverage. Negotiate the car’s purchase price separately from financing. Don’t be afraid to walk away if the deal isn’t right. Be wary of extended warranties or add-ons pushed by the dealership; evaluate their necessity carefully.

- Read the Fine Print: Before signing any document, meticulously read the entire loan agreement and purchase contract. Ensure all figures match what you agreed upon and understand every clause. If anything is unclear, ask for clarification.

- Secure Auto Insurance: You’ll need proof of insurance before you can drive off the lot. Get quotes from multiple providers, including USAA if you’re eligible, to find the best rates for your new vehicle.

Common Mistakes Military Members Make When Getting a Car Loan

Having advised numerous service members on financial matters, I’ve observed several recurring pitfalls. Avoiding these common mistakes can save you significant money and stress.

- Not Getting Pre-Approved: This is perhaps the biggest mistake. Without pre-approval, you’re negotiating blind at the dealership, potentially accepting whatever financing they offer, which is often at a higher interest rate than you could secure independently.

- Focusing Only on Monthly Payments: While monthly payments are important, fixating solely on them can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan.

- Ignoring the Total Cost of the Loan: This includes the purchase price, interest, fees, and the cost of insurance and maintenance over the loan term. A "good deal" on monthly payments might hide a very expensive overall cost.

- Buying More Car Than You Can Afford: It’s easy to get excited and overspend. Stick to your budget, even if a shiny, more expensive vehicle catches your eye. Remember that vehicle depreciation is a real factor.

- Not Understanding SCRA or Other Benefits: Many service members are unaware of their rights and benefits under SCRA, missing out on potential interest rate reductions on existing loans. Similarly, not exploring military-specific discounts can cost you savings.

- Skipping a Thorough Vehicle Inspection: Especially for used cars, a pre-purchase inspection by an independent mechanic is crucial. It can uncover hidden issues that save you from costly repairs down the line.

Building and Maintaining Good Credit While Serving

A strong credit score is your ally in securing the best possible car loans and other financial products. It’s crucial for future financial stability, particularly with the unique challenges of military life. For more tips on managing your finances while in the service, check out our guide on .

- Pay Your Bills On Time, Every Time: Payment history is the most significant factor in your credit score. Set up automatic payments to avoid missed deadlines.

- Keep Credit Utilization Low: Aim to use no more than 30% of your available credit on credit cards. High utilization can negatively impact your score.

- Maintain a Diverse Credit Mix: Having a mix of credit types (e.g., credit card, installment loan) can be beneficial, but only if managed responsibly.

- Regularly Monitor Your Credit Report: Check your credit report annually for errors and signs of identity theft. You can get free copies from AnnualCreditReport.com.

- Be Patient: Building good credit takes time and consistent effort. There are no quick fixes.

Conclusion

Securing the best car loans for military personnel and veterans requires a proactive, informed approach. By understanding the unique financial landscape of military life, leveraging military-specific lenders, and meticulously preparing for the car buying process, you can navigate the journey with confidence. Remember to prioritize low APRs, reasonable loan terms, and transparency from lenders.

Your service to our nation is invaluable, and you deserve financial solutions that respect and accommodate your unique circumstances. Don’t settle for less than the best. Take these insights, apply them diligently, and drive forward towards your next adventure with peace of mind. Start your research and pre-approval process today – your ideal car, and an excellent loan, await! For further assistance in understanding loan terms and making informed decisions, you might also find our article on helpful.