Driving Your Dream: The Ultimate Guide to PenFed New Car Loans

Driving Your Dream: The Ultimate Guide to PenFed New Car Loans Carloan.Guidemechanic.com

The exhilarating scent of a new car, the pristine interior, the promise of countless journeys – buying a new vehicle is an exciting milestone. Yet, for many, the path to ownership is often overshadowed by the complexities of financing. Securing the right loan can make all the difference, transforming a dream into an affordable reality.

This is where PenFed Credit Union steps in, offering a compelling solution for new car financing. With competitive rates, flexible terms, and a member-centric approach, a PenFed New Car Loan could be the smart choice you’ve been searching for. This comprehensive guide will illuminate every facet of securing a PenFed auto loan, ensuring you’re empowered with the knowledge to drive away with confidence.

Driving Your Dream: The Ultimate Guide to PenFed New Car Loans

Understanding PenFed Credit Union: A Partner in Your Car Buying Journey

Before diving into the specifics of new car loans, it’s essential to understand the institution behind them. PenFed (Pentagon Federal Credit Union) is one of the largest credit unions in the United States. Unlike traditional banks, credit unions are not-for-profit financial cooperatives owned by their members. This fundamental difference means their primary goal is to serve their members, often translating into better rates, lower fees, and more personalized service.

For decades, PenFed has built a strong reputation for offering competitive financial products, from mortgages to personal loans and, notably, auto loans. Their commitment to financial wellness and member satisfaction positions them as a trusted ally in your car buying process. When you choose a PenFed auto loan, you’re not just a customer; you’re a valued member of a financial community.

The PenFed Advantage: Why Choose Them for Your New Car Financing?

When exploring options for a new car loan, you’ll encounter numerous lenders. PenFed consistently stands out due to several key advantages that cater specifically to the new car buyer. Their unique structure and dedication to members create a financing experience that is both beneficial and straightforward.

Consistently Competitive Interest Rates (APR)

One of the most significant drawcards of a PenFed New Car Loan is their highly competitive Annual Percentage Rates (APR). Because PenFed operates as a credit union, their overheads are often lower, and their profits are reinvested into providing better services and rates for their members. This member-first philosophy directly translates into some of the best car loan rates available on the market.

A lower APR means less money spent on interest over the life of your loan, resulting in lower overall costs and more savings in your pocket. This factor alone can save you hundreds, if not thousands, of dollars compared to loans from traditional banks or dealership financing options.

Flexible Loan Terms Designed for Your Budget

PenFed understands that every borrower’s financial situation is unique. They offer a range of flexible loan terms, typically spanning from 36 months up to 84 months. This flexibility allows you to tailor your monthly payments to fit comfortably within your budget.

While longer terms can mean lower monthly payments, it’s crucial to understand that they also typically accrue more interest over time. Based on my experience, it’s always wise to choose the shortest term you can comfortably afford to minimize the total cost of your loan. PenFed provides the options, empowering you to make the decision that best suits your financial goals.

Streamlined and User-Friendly Application Process

Gone are the days of endless paperwork and arduous waiting periods. PenFed has embraced technology to offer a remarkably efficient and user-friendly online application process. You can apply for a PenFed New Car Loan from the comfort of your home, often receiving a decision within minutes.

This streamlined approach is particularly beneficial for those with busy schedules, allowing you to secure financing without disrupting your daily life. The clarity of their application portal further enhances the experience, guiding you through each step with ease.

The Power of Pre-Approval: Your Negotiation Superpower

One of the most valuable services PenFed offers is new car loan pre-approval. Getting pre-approved before you step foot on a dealership lot transforms your car buying experience. It shifts your position from a mere shopper to a cash buyer in the eyes of the dealer.

With a pre-approval letter in hand, you know exactly how much you can afford, and your interest rate is locked in. This eliminates the uncertainty of financing and allows you to focus solely on negotiating the vehicle price, often leading to a better deal. Pro tips from us: Never visit a dealership without first securing your pre-approval!

Transparent Terms with No Hidden Fees

Transparency is a hallmark of PenFed’s service. When you secure a PenFed auto loan, you can expect clear terms and conditions, free from unexpected charges or hidden fees. This commitment to honesty builds trust and ensures you fully understand your financial commitment from the outset.

Many traditional lenders or dealerships might sneak in processing fees or other charges, but PenFed’s model is designed to be straightforward. This peace of mind is invaluable when making a significant purchase like a new car.

Eligibility for a PenFed New Car Loan: Are You Ready?

To qualify for a PenFed New Car Loan, there are a few key requirements you’ll need to meet. These criteria ensure that PenFed can responsibly lend to its members while maintaining its competitive rates. Understanding these points upfront will help you prepare your application.

The Essential Step: PenFed Membership

As a credit union, PenFed primarily serves its members. Therefore, the first and foremost requirement is to become a PenFed member. Don’t worry, it’s far simpler than you might think and doesn’t necessarily require military affiliation.

You can become a member by opening a savings account with as little as a $5 deposit and meeting one of their eligibility criteria. This includes being a member of certain associations (like the National Military Family Association) or by making a one-time donation of $17 to the Voices for America’s Troops or the National Military Family Association. It’s a small step that unlocks a world of financial benefits.

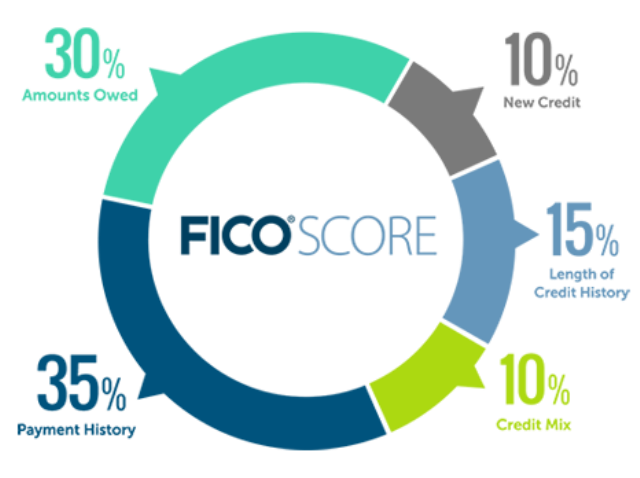

Your Credit Score: The Cornerstone of Your Application

Your credit score plays a pivotal role in determining both your eligibility and the interest rate you’ll receive for a PenFed New Car Loan. PenFed typically seeks borrowers with good to excellent credit scores, generally in the mid-600s and above, to qualify for their best rates.

A higher credit score demonstrates your reliability as a borrower and indicates a lower risk to the lender. Based on my experience, borrowers with scores in the 700s and 800s will unlock the most favorable terms. It’s crucial to check your credit score and report before applying to address any inaccuracies or areas for improvement.

Income and Debt-to-Income (DTI) Ratio

Lenders like PenFed assess your ability to repay the loan, and your income and debt-to-income (DTI) ratio are key indicators. They want to ensure your existing debt obligations, combined with the new car payment, don’t overextend your financial capacity.

While there isn’t a strict minimum income, your DTI ratio (your total monthly debt payments divided by your gross monthly income) is closely examined. A lower DTI ratio, ideally below 40%, signals a healthy financial position and increases your chances of approval.

Vehicle Requirements: What Qualifies as "New"?

For a PenFed New Car Loan, the vehicle typically needs to be a brand-new model, meaning it has not been previously titled. There might also be restrictions on the model year (e.g., current or previous year’s models) and mileage limits (e.g., under 7,500 miles). Always confirm the exact criteria with PenFed, as these can sometimes vary.

The Application Journey: Your Step-by-Step Guide to a PenFed Loan

Navigating the application process for a PenFed New Car Loan is straightforward when you know what to expect. Following these steps will help you move efficiently from initial inquiry to driving your new vehicle.

Step 1: Prepare Your Financial Foundation

Before you even start the application, take some time to get your finances in order. This includes checking your credit score and report from all three major bureaus (Equifax, Experian, TransUnion). Dispute any errors you find. Gather necessary documents such as proof of income (pay stubs, W-2s), proof of residence, and identification. Having these ready will expedite the application process.

Step 2: Become a PenFed Member

If you’re not already a member, this is your crucial second step. Visit the PenFed website and follow the easy instructions to open a savings account and fulfill the membership eligibility criteria. This typically takes only a few minutes and is a prerequisite for any PenFed loan product.

Step 3: Apply for Pre-Approval

This is where the magic happens. Head to PenFed’s auto loan section online and begin your pre-approval application. You’ll need to provide personal details, income information, and authorize a credit check. PenFed will typically perform a "soft inquiry" for pre-approval, which doesn’t impact your credit score.

Within minutes, you’ll often receive an offer detailing the maximum loan amount, estimated interest rate, and terms you qualify for. This pre-approval gives you immense confidence and clarity.

Step 4: Shop for Your New Car with Confidence

With your PenFed pre-approval in hand, you’re now a powerful buyer. You know your budget and your financing terms. You can visit dealerships, test drive vehicles, and negotiate the purchase price with the assurance that your funding is already secured. This takes the pressure off discussing financing at the dealership, allowing you to focus on getting the best deal on the car itself.

Step 5: Finalize Your PenFed New Car Loan

Once you’ve chosen your new car and agreed on a price with the dealership, you’ll finalize your loan with PenFed. This usually involves providing the final vehicle details (VIN, exact purchase price) and any remaining documentation. PenFed will then send the funds directly to the dealership, or in some cases, provide you with a check to complete the purchase.

A "hard inquiry" on your credit report will be made at this stage, which is a normal part of finalizing any loan and will have a minor, temporary impact on your score.

Deciphering PenFed New Car Loan Rates and Terms

Understanding the nuances of interest rates and loan terms is vital for making an informed decision about your PenFed auto loan. These factors directly impact your monthly payment and the total cost of your vehicle.

Understanding APR: Beyond Just the Interest Rate

When PenFed quotes you a rate, it’s typically the Annual Percentage Rate (APR). The APR is more comprehensive than just the interest rate because it includes not only the interest charged on the loan but also any other fees associated with the loan, expressed as a yearly percentage. This provides a more accurate picture of the true cost of borrowing.

PenFed is known for its competitive APRs, which often means fewer hidden fees are rolled into that rate, unlike some other lenders. Always compare APRs when shopping for a loan, not just the advertised interest rate.

Factors Influencing Your PenFed Auto Loan Rate

Several elements come into play when PenFed determines your specific interest rate:

- Credit Score: As mentioned, a higher credit score (generally 700+) will secure you the lowest possible rates.

- Loan Term: Shorter loan terms typically come with lower interest rates because the lender takes on less risk over a shorter period.

- Loan Amount: The total amount you borrow can sometimes influence the rate, though credit score and term are usually more impactful.

- Down Payment: A larger down payment reduces the amount you need to borrow and can signal greater financial stability, potentially leading to a better rate.

Loan Terms Explained: Choosing the Right Duration

PenFed offers various loan terms, commonly ranging from 36, 48, 60, 72, and even 84 months. Each has its pros and cons:

- Shorter Terms (e.g., 36-48 months):

- Pros: Lower total interest paid, faster loan payoff, typically lower interest rates.

- Cons: Higher monthly payments.

- Medium Terms (e.g., 60 months):

- Pros: A good balance between affordable monthly payments and reasonable total interest.

- Cons: Slightly more interest than shorter terms.

- Longer Terms (e.g., 72-84 months):

- Pros: Significantly lower monthly payments, making expensive cars more "affordable" on a month-to-month basis.

- Cons: Substantially higher total interest paid, longer period of indebtedness, increased risk of being "upside down" on your loan (owing more than the car is worth).

Common mistakes to avoid are focusing solely on the monthly payment. While important, always consider the total cost of the loan over its lifetime. A slightly higher monthly payment for a shorter term can save you thousands in the long run.

The Strategic Role of Your Down Payment

Making a substantial down payment on your PenFed New Car Loan is a smart financial move. A larger down payment:

- Reduces Loan Amount: You borrow less, which means less interest accrues over the loan term.

- Lowers Monthly Payments: With a smaller principal, your payments will be more manageable.

- Improves Loan-to-Value (LTV): A lower LTV ratio (loan amount divided by car value) makes you a less risky borrower, potentially qualifying you for better rates.

- Protects Against Negative Equity: New cars depreciate rapidly. A good down payment helps you avoid owing more than your car is worth, especially in the early years of ownership.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment if your budget allows.

Comparing PenFed: New vs. Used Car Loans & Other Lenders

While this guide focuses on new car loans, it’s helpful to understand where PenFed stands in the broader auto loan landscape. They also offer competitive used car loans, though rates and terms may differ slightly due to the perceived higher risk of older vehicles. Generally, new car loans tend to have lower interest rates than used car loans.

When comparing PenFed to other lenders, here’s what often sets them apart:

- Traditional Banks: While banks offer auto loans, their rates might not always be as aggressive as credit unions due to their for-profit structure. The application process can also sometimes be more rigid.

- Dealership Financing: Dealerships often present attractive "special" rates, but these are typically reserved for borrowers with impeccable credit. Furthermore, the focus on financing at the dealership can distract from negotiating the car’s price. PenFed pre-approval empowers you to separate the two.

For a deeper dive into choosing between new and used car financing, check out our article on . This resource can help you weigh the financial implications of both options.

Maximizing Your Chances of Approval & Getting the Best Rate

Even if you meet the basic eligibility criteria, there are proactive steps you can take to strengthen your application and secure the most favorable terms on your PenFed New Car Loan.

- Boost Your Credit Score: Prioritize paying all your bills on time, reduce outstanding credit card balances, and avoid opening new lines of credit just before applying. Even a few points increase can impact your rate tier.

- Reduce Your Debt: Lowering your overall debt, especially revolving debt like credit cards, will improve your debt-to-income ratio, making you a more attractive borrower.

- Increase Your Down Payment: As discussed, a larger down payment signals financial responsibility and reduces the lender’s risk, often resulting in a better rate.

- Consider a Co-signer: If your credit score is borderline or you have a limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower rate. Ensure both parties understand the responsibilities involved.

- Negotiate Wisely: Even with pre-approval, don’t forget to negotiate the final price of the car itself. The less you pay for the car, the less you need to borrow, which is always a win.

Post-Approval: What to Expect and Smart Strategies

Congratulations, your PenFed New Car Loan is approved! But the journey doesn’t end there. Managing your loan effectively is crucial for maintaining financial health.

- Online Account Management: PenFed provides robust online portals and mobile apps for easy loan management. You can view your balance, make payments, and access statements conveniently.

- Payment Options: Set up automatic payments to avoid missing due dates and potentially incurring late fees or damaging your credit score. PenFed usually offers various payment methods, including direct debit from your bank account.

- No Prepayment Penalties: A significant advantage of PenFed loans is the absence of prepayment penalties. This means you can make extra payments or pay off your loan early without incurring additional fees. This flexibility allows you to save on interest if your financial situation improves.

- Refinancing Possibilities: While less common for a brand-new car loan initially, if interest rates drop significantly in the future, or your credit score improves dramatically, you might consider refinancing your PenFed auto loan for an even better rate. This is usually more relevant for older loans. For current PenFed auto loan details and to explore options, visit the official PenFed Auto Loans page.

Common Mistakes to Avoid When Applying for a New Car Loan

Based on my experience helping countless buyers navigate the car financing landscape, several common pitfalls can derail your plans or cost you money. Being aware of these can save you a lot of headaches.

- Not Getting Pre-Approved: This is perhaps the biggest mistake. Without pre-approval, you lose your negotiating power and risk being upsold on dealership financing that may not be in your best interest.

- Focusing Only on Monthly Payments: As discussed, a low monthly payment over an extended term often means paying significantly more in total interest. Always look at the total cost of the loan.

- Ignoring Your Credit Report: Errors on your credit report can negatively impact your score and lead to higher interest rates or even denial. Always review it thoroughly before applying.

- Extending the Loan Term Too Much: While a longer term offers lower monthly payments, it prolongs your indebtedness and increases the total interest paid. It also increases the risk of negative equity.

- Forgetting About Other Costs: Remember that a car loan is just one part of car ownership. Factor in insurance, maintenance, fuel, and registration costs into your budget.

- Settling for the First Offer: Always compare offers. Even with PenFed’s competitive rates, it’s wise to understand the market. However, with pre-approval, you already have a strong benchmark.

Conclusion: Your Smart Path to a New Car with PenFed

Securing a PenFed New Car Loan offers a compelling combination of competitive rates, flexible terms, and a member-focused approach that sets it apart from many other financing options. By understanding the eligibility requirements, preparing your finances, and leveraging the power of pre-approval, you can navigate the new car buying process with confidence and ease.

This comprehensive guide has equipped you with the knowledge to make an informed decision, ensuring your journey to owning a new car is as smooth and financially sound as possible. PenFed empowers you to take control of your financing, allowing you to focus on the joy of driving your dream vehicle. Embrace the PenFed advantage and drive smarter, not harder.