Driving Your Dream Toyota: A Comprehensive Guide to Bad Credit Car Loans

Driving Your Dream Toyota: A Comprehensive Guide to Bad Credit Car Loans Carloan.Guidemechanic.com

The dream of owning a reliable car, especially a Toyota, often feels out of reach when your credit score isn’t where you want it to be. Many people believe that having bad credit automatically disqualifies them from securing a car loan. However, this simply isn’t true. While it presents unique challenges, getting a bad credit car loan for a Toyota is entirely possible with the right knowledge and approach.

As an expert blogger and professional SEO content writer, I understand the frustration and uncertainty that come with navigating the financial landscape with less-than-perfect credit. My mission with this in-depth guide is to provide you with a comprehensive roadmap, offering actionable strategies and expert insights to help you secure a Toyota car loan, even when facing credit hurdles. We’ll explore everything from understanding your credit to finding the right lender and managing your loan effectively.

Driving Your Dream Toyota: A Comprehensive Guide to Bad Credit Car Loans

Understanding Bad Credit and Its Impact on Car Loans

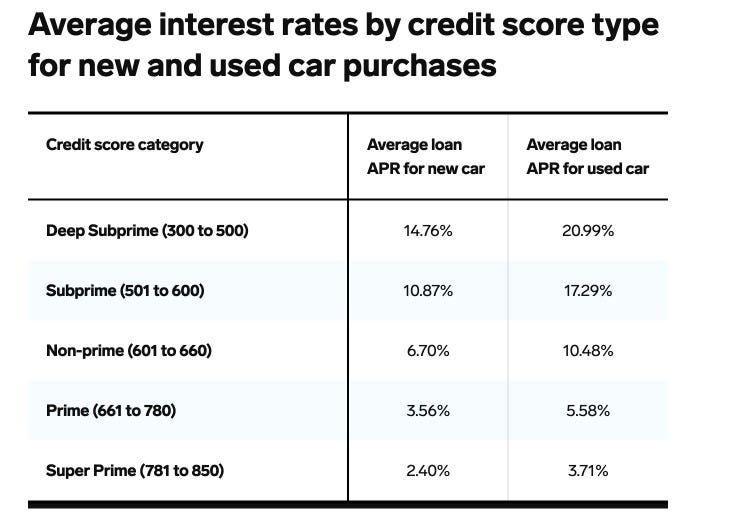

Before diving into the specifics of bad credit car loans Toyota, it’s crucial to understand what "bad credit" actually means and why it affects lending decisions. Your credit score is a three-digit number that lenders use to assess your creditworthiness – essentially, how likely you are to repay borrowed money. Scores range from 300 to 850, with different ranges categorized as excellent, good, fair, and poor.

Generally, a FICO score below 580 is considered "very poor" or "bad credit." Lenders view individuals with lower scores as higher risk. This doesn’t mean you’ll be denied outright, but it does mean you might face higher interest rates and potentially stricter loan terms to compensate for that increased risk. Understanding your current standing is the first critical step in this journey.

Why a Toyota is an Excellent Choice, Even with Bad Credit

When you’re working with a bad credit history, every financial decision matters, and choosing the right vehicle is paramount. This is where a Toyota truly shines. Based on my experience and extensive research, opting for a Toyota can be a particularly smart move for individuals securing a bad credit car loan. Their reputation for reliability and longevity isn’t just a marketing slogan; it’s a proven track record.

Toyota vehicles consistently rank high in consumer satisfaction and boast impressive resale values. This reliability translates directly into lower long-term ownership costs, which is a significant benefit for anyone on a tight budget. Fewer unexpected repairs mean you can better manage your finances and focus on making your loan payments on time. From the fuel-efficient Corolla to the versatile RAV4 or the robust Tacoma, Toyota offers a diverse range of models that cater to various needs and budgets, providing ample options for your specific situation.

Preparing for Your Bad Credit Toyota Car Loan

Preparation is the cornerstone of success when seeking a bad credit car loan. Walking into a dealership or approaching a lender without doing your homework is a common mistake that can lead to unfavorable terms or outright rejection. A proactive approach not only increases your chances of approval but can also help you secure a better deal.

1. Know Your Credit Score and Report:

The very first step is to obtain a copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion). You can do this for free annually through AnnualCreditReport.com. Scrutinize these reports for any errors or inaccuracies. Even a small mistake, like an incorrectly reported late payment, can significantly drag down your score. Disputing and correcting these errors can provide a quick, albeit sometimes modest, boost to your credit. Understanding your score gives you a realistic expectation of the loan terms you might be offered.

2. Create a Realistic Budget:

Before you even start looking at Toyota models, sit down and honestly assess your financial situation. Determine how much you can comfortably afford for a monthly car payment, taking into account all your other expenses. Don’t forget to factor in additional costs of car ownership, such as insurance, fuel, maintenance, and registration fees. Pro tips from us: use a spreadsheet or budgeting app to track your income and outgoings meticulously. A common mistake to avoid is focusing solely on the monthly payment without considering the total cost of ownership.

3. Save for a Down Payment:

A substantial down payment is one of your most powerful tools when seeking a bad credit car loan for a Toyota. Lenders see a significant down payment as a sign of your commitment and ability to manage finances. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. Aim for at least 10-20% of the car’s purchase price if possible. Even a small down payment is better than none.

4. Gather Necessary Documentation:

Lenders will require various documents to verify your identity, income, and residency. Having these prepared in advance demonstrates your seriousness and streamlines the application process. Typically, you’ll need:

- Proof of identity (driver’s license, passport)

- Proof of residency (utility bill, lease agreement)

- Proof of income (recent pay stubs, tax returns, bank statements)

- Proof of employment (employer contact information, recent W-2s)

- References (sometimes requested by subprime lenders)

Finding the Right Lender for Your Toyota Bad Credit Loan

Not all lenders are created equal, especially when it comes to bad credit car loans. It’s crucial to explore different avenues to find a lender who understands your situation and offers fair terms. Don’t just settle for the first offer you receive; comparison shopping is key.

1. Specialized Bad Credit Lenders (Subprime Lenders):

These lenders specialize in working with individuals who have lower credit scores. They are more willing to take on the increased risk associated with bad credit, though often at higher interest rates. Many online platforms connect you with a network of such lenders, allowing you to compare offers from the comfort of your home. It’s essential to research their reputation and read reviews before committing.

2. Toyota Dealership Financing:

Many Toyota dealerships have dedicated finance departments that work with a wide array of lenders, including those who specialize in bad credit car loans. They often have relationships with both traditional banks and subprime finance companies. Applying directly through a Toyota dealership can be convenient, as they can often match you with a suitable loan product while you’re shopping for your car. They are motivated to sell you a vehicle, so they will often go the extra mile to find a financing solution.

3. Credit Unions:

Credit unions are member-owned financial institutions known for their customer-centric approach. They may offer more flexible lending criteria and potentially lower interest rates compared to traditional banks, even for those with bad credit. If you’re already a member of a credit union, or if there’s one you can join, it’s definitely worth exploring their auto loan options. Their focus is often on helping their members rather than maximizing profits.

4. Online Lenders and Marketplaces:

The digital age has brought forth numerous online platforms that streamline the car loan application process. These sites often allow you to pre-qualify for a loan without a hard credit inquiry, which is excellent for comparing offers without impacting your credit score. They can connect you with multiple lenders, increasing your chances of finding a competitive rate for your Toyota bad credit loan. Always ensure these platforms are reputable and secure before sharing personal information.

The Application Process Demystified

Applying for a bad credit car loan might seem daunting, but understanding what lenders look for can significantly ease the process. Lenders assess your overall financial picture, not just your credit score. They want to ensure you have the capacity and willingness to repay the loan.

1. What Lenders Look For:

- Income Stability: A steady job with consistent income is paramount. Lenders want to see that you have a reliable source of funds to make your monthly payments.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income available for a car payment.

- Employment History: A stable employment history, ideally with the same employer for a year or more, reassures lenders about your financial reliability.

- Down Payment: As mentioned, a larger down payment reduces the lender’s risk.

- Credit History (Even if Bad): While your score might be low, lenders will review your report for any recent positive trends or explanations for past issues.

2. Common Mistakes to Avoid:

Based on my experience, one of the biggest mistakes people make is applying to too many lenders simultaneously, especially if each application results in a hard inquiry on their credit report. This can further lower your score. Another common error is not being fully transparent about your financial situation. Honesty builds trust. Finally, failing to negotiate terms, even with bad credit, can cost you money. Don’t be afraid to ask for a better rate or explore different loan structures.

3. The Importance of Honesty:

Always provide accurate and complete information on your application. Attempting to hide or falsify details will almost certainly lead to rejection and could have more severe consequences. Lenders have sophisticated verification processes. Being upfront about your credit history and financial situation can actually work in your favor, as it allows lenders to assess the real risk and potentially offer a tailored solution.

Navigating Loan Terms and Interest Rates for Your Toyota

Once you receive loan offers, it’s crucial to carefully review and understand all the terms and conditions. For individuals with bad credit, interest rates will undoubtedly be higher than for those with excellent credit. However, this doesn’t mean you should accept the first offer without scrutiny.

1. Understanding APR vs. Interest Rate:

The Annual Percentage Rate (APR) is the most important number to focus on. It represents the total cost of borrowing money over a year, including the interest rate and any additional fees (like origination fees). While the interest rate is just the percentage charged on the principal, the APR gives you a more complete picture of the loan’s true cost. Always compare APRs when evaluating different loan offers for your Toyota bad credit loan.

2. Loan Term (Length):

The loan term refers to the duration over which you will repay the loan. Longer terms result in lower monthly payments but significantly increase the total amount of interest you’ll pay over time. Shorter terms mean higher monthly payments but save you money on interest in the long run. Based on my experience, for bad credit car loans, lenders might push for longer terms to make the monthly payment seem more affordable. However, if you can manage it, opting for the shortest term you can comfortably afford will save you thousands.

3. The Impact of a Down Payment Revisited:

A larger down payment not only reduces your principal loan amount but can also positively influence the interest rate you’re offered. Lenders see a higher down payment as a sign of lower risk, which might make them more inclined to offer a slightly more favorable APR. This also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth, a common issue with bad credit car loans.

4. Watch Out for Hidden Fees and Penalties:

Carefully read the fine print. Look for any prepayment penalties, which are fees charged if you pay off your loan early. Also, be aware of balloon payments, where a large lump sum is due at the end of the loan term. Pro tips from us: if anything in the loan agreement is unclear, don’t hesitate to ask for clarification. A reputable lender will be transparent about all terms.

Strategies for Success After Getting Your Toyota Loan

Securing a bad credit car loan for your Toyota is just the beginning. The period after approval is critical for rebuilding your credit and ensuring a positive financial future. This is your chance to demonstrate responsible financial behavior.

1. Making Payments On Time, Every Time:

This is, without a doubt, the most important strategy. Your payment history is the single largest factor in your credit score (accounting for 35%). Consistently making your Toyota car loan payments on or before the due date will steadily improve your credit score over time. Set up automatic payments from your bank account to avoid missed payments, which are common mistakes to avoid.

2. Explore Refinancing Opportunities:

Once you’ve made 6-12 months of on-time payments and your credit score shows improvement, you may be eligible to refinance your car loan. Refinancing allows you to get a new loan with a lower interest rate, which can significantly reduce your monthly payments and the total interest paid over the life of the loan. Keep an eye on your credit score and market rates; when the time is right, explore options with different lenders.

3. Budget for Car Ownership:

Beyond your monthly loan payment, remember to budget for other essential car ownership costs. This includes fuel, routine maintenance (oil changes, tire rotations), and comprehensive car insurance. Toyota’s reputation for reliability helps keep maintenance costs lower, but regular upkeep is still necessary to ensure your vehicle lasts and avoids unexpected, costly repairs. A well-maintained car is a safer and more economical car.

Common Myths About Bad Credit Car Loans

There are many misconceptions surrounding bad credit car loans that can deter individuals from even trying. Let’s debunk a few:

- Myth 1: "It’s impossible to get approved for a car loan with bad credit."

- Reality: While challenging, it’s far from impossible. Specialized lenders and dealership finance departments exist specifically to help individuals with less-than-perfect credit. It requires more effort and preparation, but approval is a real possibility.

- Myth 2: "You’ll always get ripped off with a bad credit car loan."

- Reality: While interest rates will be higher, not all bad credit loans are predatory. By doing your research, comparing offers, understanding terms, and being prepared, you can find a fair deal. The key is knowledge and vigilance.

- Myth 3: "A car loan won’t help improve my credit score."

- Reality: A bad credit car loan, when managed responsibly with on-time payments, is an excellent tool for rebuilding and improving your credit score. It demonstrates your ability to handle installment debt, which positively impacts your credit history.

Conclusion: Your Toyota Dream is Within Reach

Securing a bad credit car loan for a reliable Toyota might seem like an uphill battle, but as we’ve explored, it’s a journey you can successfully navigate. With careful preparation, a clear understanding of your financial situation, and the right approach to finding a lender, your dream of driving a dependable Toyota can become a reality. Remember, this isn’t just about getting a car; it’s also a significant opportunity to rebuild your credit and establish a stronger financial foundation for the future.

Don’t let past credit challenges define your present or future. Take the proactive steps outlined in this guide – know your credit, budget wisely, save for a down payment, and research your lending options thoroughly. Your journey to owning a Toyota, even with bad credit, begins today. For further reading on managing your finances, check out . You can also learn more about the importance of understanding your credit report by visiting .