Driving Your Dream: Uncovering the Best Loan To Buy A Car in 2024

Driving Your Dream: Uncovering the Best Loan To Buy A Car in 2024 Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, representing freedom, convenience, and a step towards personal independence. Yet, for all the excitement of choosing the perfect model, the financial aspect can often feel overwhelming. Navigating the world of auto loans can be complex, filled with jargon and countless options that leave many wondering: "What is the best loan to buy a car?"

As an expert blogger and professional SEO content writer, I understand this challenge deeply. My mission today is to demystify the car loan process, providing you with a super comprehensive, informative, and unique guide that not only explains your options but empowers you to make the smartest financial decision. This article aims to be your ultimate pillar content, ensuring you’re well-equipped to secure a loan that aligns with your financial health and driving aspirations. Let’s dive in and unlock the secrets to securing the ideal car loan.

Driving Your Dream: Uncovering the Best Loan To Buy A Car in 2024

Understanding Car Loans: More Than Just Monthly Payments

Before we explore the best options, it’s crucial to grasp the fundamental components of any car loan. A car loan isn’t just about the monthly payment you agree to; it’s a complex financial product with several key elements that collectively determine its true cost. Understanding these elements is your first step towards making an informed decision.

At its core, a car loan is an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a set period. This principal amount is the actual price of the car you’re financing, minus any down payment or trade-in value. The interest is the cost of borrowing that money, expressed as a percentage of the principal.

The loan term, often measured in months (e.g., 36, 48, 60, 72, or even 84 months), dictates how long you have to repay the loan. A longer term might mean lower monthly payments, but it almost always results in paying significantly more interest over the life of the loan. Conversely, a shorter term leads to higher monthly payments but a much lower total cost due to less interest accruing.

Based on my experience, many first-time buyers fall into the trap of focusing solely on the monthly payment. While it’s important for budgeting, ignoring the interest rate and loan term can lead to paying thousands more than necessary. A seemingly low monthly payment over an extended period can quickly inflate the total cost of your vehicle.

Types of Car Loans: Your Options Explored

When searching for the best loan to buy a car, you’ll encounter various types of auto loans, each suited to different situations. Knowing these distinctions can help you narrow down your search and find the most appropriate financing for your specific needs.

New Car Loans

Financing a brand-new vehicle typically comes with the most favorable terms. Lenders often view new cars as lower risk due to their predictable value and manufacturer warranties. This usually translates into lower interest rates and a wider range of loan terms.

New car loans are generally easier to qualify for if you have good credit. Manufacturers and dealerships frequently offer promotional interest rates, sometimes as low as 0% APR, to incentivize sales of new models. However, these special rates are usually reserved for borrowers with excellent credit scores.

Used Car Loans

Used car loans are a common choice for buyers looking for more affordable options. While they are still a great way to finance a vehicle, they generally come with slightly higher interest rates compared to new car loans. This is because used vehicles are seen as having a higher depreciation rate and potentially more maintenance issues.

The age and mileage of the used car can also influence the loan terms. Older vehicles or those with very high mileage might be harder to finance, or lenders might offer shorter loan terms to mitigate their risk. It’s crucial to balance the car’s price with the loan’s cost when buying used.

Refinance Car Loans

A refinance car loan isn’t for a new purchase, but it’s an excellent option if you already have a car loan and want to improve its terms. This involves taking out a new loan to pay off your existing one, ideally with a lower interest rate, a shorter term, or both. Refinancing can significantly reduce your monthly payments or the total interest you pay.

Pro tip: Consider refinancing if your credit score has improved since you first took out the loan, or if interest rates have dropped. It’s also a smart move if you want to change your loan term to better suit your current financial situation. Many lenders specialize in auto loan refinancing, making it a competitive market.

Private Party Car Loans

Buying a car from a private seller, rather than a dealership, can sometimes offer better prices. However, financing a private party purchase can be a bit trickier. Not all lenders offer loans for private sales, and those that do might have stricter requirements or slightly higher rates.

When seeking a private party car loan, expect lenders to scrutinize the vehicle’s condition more closely. They may require a professional inspection to ensure the car is worth the loan amount. Always make sure the title transfer and registration are handled correctly to avoid future headaches.

Where to Find the Best Loan To Buy A Car

The quest for the best loan to buy a car often begins with knowing where to look. The financial landscape offers several avenues for auto financing, each with its own advantages and disadvantages. Exploring all these options is key to securing the most favorable terms.

Common mistake to avoid: only checking one source. Relying solely on the dealership’s financing office can mean missing out on potentially better rates elsewhere. Smart borrowers always shop around.

Dealership Financing

Dealerships offer a one-stop shop for car buying and financing. They often work with multiple lenders, including their own "captive finance companies" (e.g., Ford Credit, Toyota Financial Services). This convenience can be appealing, as you can complete the entire purchase process in one place.

Dealerships can sometimes offer attractive promotional rates, especially on new vehicles, to move inventory. However, their primary goal is to sell cars, and the financing office might not always present you with the absolute lowest rate you qualify for. They may also try to push add-ons like extended warranties or GAP insurance, which can inflate your loan amount.

Banks

Traditional banks are a popular choice for auto loans. If you have an existing relationship with a bank, they might offer you competitive rates or special perks. Banks typically provide a range of loan products and terms, catering to various credit profiles.

Applying for a car loan at a bank often involves a straightforward process, whether online, over the phone, or in person. They are known for their stability and generally transparent terms. However, their rates might not always be the absolute lowest, especially when compared to credit unions or some online lenders.

Credit Unions

Credit unions are non-profit financial cooperatives owned by their members. This structure often allows them to offer highly competitive interest rates on auto loans, sometimes significantly lower than traditional banks. They are also known for their personalized service and willingness to work with members, even those with less-than-perfect credit.

To secure a loan from a credit union, you usually need to become a member, which often involves meeting certain eligibility criteria (e.g., living in a specific area, working for a particular employer, or being part of an association). Membership is typically easy to achieve, making credit unions an excellent option for many car buyers.

For more details on comparing lenders, check out our guide on .

Online Lenders

The rise of online lenders has revolutionized the car loan market, offering unparalleled speed and convenience. These platforms allow you to apply for and compare multiple loan offers from various lenders without leaving your home. Many online lenders specialize in auto loans and can offer highly competitive rates.

Online lenders are particularly beneficial for borrowers who want to shop around quickly and efficiently. They often cater to a wider range of credit scores, including those with fair or even bad credit, though rates will vary accordingly. The digital application process is typically streamlined, with quick approval times, sometimes within minutes.

Key Factors That Influence Your Car Loan

Securing the best loan to buy a car is heavily dependent on several critical factors. Understanding these elements will not only help you prepare but also give you leverage when negotiating. Lenders evaluate these aspects to assess your risk profile and determine the interest rate and terms they are willing to offer.

Credit Score: The Ultimate Game Changer

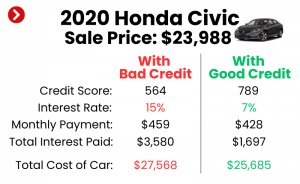

Your credit score is arguably the most significant factor influencing your car loan. It’s a three-digit number that represents your creditworthiness, essentially telling lenders how likely you are to repay your debts. A higher credit score signals lower risk, translating into lower interest rates and more favorable loan terms.

- Excellent Credit (780+): You’ll qualify for the absolute best rates, often promotional offers.

- Good Credit (670-779): Still very good rates, but might not hit the absolute lowest.

- Fair Credit (580-669): Expect higher interest rates, but financing is usually possible.

- Poor Credit (Below 580): You’ll face significantly higher interest rates and may need a larger down payment or a co-signer.

Based on years of helping people finance cars, I can tell you that even a small improvement in your credit score can save you hundreds, if not thousands, of dollars over the life of a loan. Regularly checking your credit report and disputing any errors is a crucial step before applying for a loan. For an official perspective on understanding credit reports, visit Consumer Financial Protection Bureau – Credit Reports and Scores.

Down Payment: Your Financial Foundation

A down payment is the initial amount of money you pay upfront towards the purchase of a car. It directly reduces the amount you need to borrow, which has several benefits. A larger down payment lowers your principal, resulting in smaller monthly payments and less interest paid over the life of the loan.

Furthermore, a substantial down payment can make you a more attractive borrower to lenders. It demonstrates your financial commitment and reduces their risk, potentially leading to better interest rates, especially if your credit isn’t stellar. Aim for at least 10-20% of the car’s purchase price if possible.

Loan Term: The Time-Cost Trade-Off

The loan term refers to the length of time you have to repay the loan, typically ranging from 36 to 84 months. While a longer loan term means lower monthly payments, it significantly increases the total interest you’ll pay over time. This is because the interest accrues for a longer duration.

A shorter loan term, conversely, means higher monthly payments but a much lower total cost of the loan. It allows you to pay off your car faster, building equity sooner. It’s a common mistake to extend the loan term purely to reduce monthly payments without considering the total financial impact.

Interest Rate (APR): The True Cost of Borrowing

The Annual Percentage Rate (APR) is the most critical number to focus on. It represents the total cost of borrowing money over a year, expressed as a percentage. The APR includes not only the interest rate but also any additional fees charged by the lender, giving you a comprehensive view of the loan’s cost.

A lower APR directly translates to less money spent on interest over the life of the loan. Factors like your credit score, the loan term, the down payment, and even the type of vehicle all influence the APR you’re offered. Always compare APRs, not just interest rates, when evaluating different loan offers.

Debt-to-Income Ratio: Lender’s Financial Lens

Your debt-to-income (DTI) ratio is another crucial metric lenders examine. It compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to manage your new car payment, making you a less risky borrower.

Lenders typically prefer a DTI ratio below 36%, with some allowing up to 43%. A high DTI might lead to higher interest rates or even loan denial, as it suggests you might be overextended financially. Managing your existing debts and improving your DTI before applying can significantly improve your chances of getting a favorable loan.

Vehicle Age and Type: Asset Depreciation

The age and type of the vehicle you’re buying also play a role. New cars generally secure lower interest rates because they hold their value better initially and pose less risk to the lender. Used cars, particularly older models, depreciate faster and carry more potential for mechanical issues, which can translate to higher interest rates or shorter loan terms.

Luxury vehicles or specialty cars might also have different financing considerations. Lenders assess the resale value and overall risk associated with the specific car you intend to purchase. This is why a vehicle’s value is often a key part of the loan approval process.

The Pre-Approval Process: Your Secret Weapon

When embarking on your car buying journey, getting pre-approved for a loan is arguably the most powerful step you can take. It’s your secret weapon, transforming you from a hopeful buyer into a confident negotiator. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate, pending a final vehicle choice.

What is pre-approval? It’s a conditional offer of credit from a lender before you even step foot on a dealership lot. They will conduct a ‘hard inquiry’ on your credit report, which will temporarily ding your score by a few points, but the benefits far outweigh this minor drawback. Importantly, multiple auto loan inquiries within a short period (typically 14-45 days) are often grouped together as a single inquiry by credit bureaus, recognizing you’re rate shopping.

The benefits of pre-approval are immense. First, it gives you a clear budget. You know exactly how much car you can afford, preventing you from falling in love with a vehicle outside your financial reach. This clarity helps you focus your search and avoid wasting time.

Second, pre-approval provides immense negotiating power. When you walk into a dealership with a pre-approved loan in hand, you’re essentially a cash buyer. You’ve already secured your financing, so the dealership knows they can’t inflate the interest rate on you. This allows you to focus purely on negotiating the car’s price, rather than getting caught up in a complex discussion about monthly payments that bundle the car price and interest.

Pro tip: Never step onto a dealership lot without pre-approval. It allows you to compare the dealer’s financing offer against your pre-approved rate. If the dealer can beat your pre-approval, great! If not, you already have a solid fallback. This strategy ensures you always get the most competitive financing available.

Navigating the Application & Closing

Once you’ve identified the best loan to buy a car and chosen your vehicle, the final stages involve the application and closing process. While much of the heavy lifting is done with pre-approval, these steps require careful attention to detail to ensure a smooth transaction.

When you’re ready to finalize your loan, the lender will require several documents. These typically include proof of identity (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and potentially proof of insurance. Having these documents readily available will significantly speed up the process.

A critical step is to thoroughly read the loan agreement before signing. Don’t rush through it. Pay close attention to the interest rate (APR), the total loan amount, the loan term, and any fees involved. Ensure there are no hidden charges or clauses you don’t understand. If anything is unclear, ask for clarification.

Common mistakes often occur around add-ons. Dealerships may try to include extras like GAP insurance, extended warranties, paint protection, or VIN etching into your loan. While some of these might offer value, many are overpriced or unnecessary. Carefully evaluate each add-on. GAP insurance, for instance, can be worthwhile if you put down a small down payment, but you can often find it cheaper through your car insurance provider or a separate lender.

Considering GAP insurance? Read our in-depth analysis here: .

Remember, you are in control. You have the right to decline any add-ons you don’t want or need. Only sign the paperwork once you are completely comfortable with all the terms and conditions. Finalizing the deal involves signing the loan documents, transferring the vehicle title, and arranging for vehicle registration. Congratulations, you’re now a car owner!

Common Mistakes to Avoid When Getting a Car Loan

Even with the best intentions, borrowers often make common missteps that can lead to paying more than necessary or getting stuck with an unfavorable loan. As an expert, I’ve seen these errors repeatedly. Avoiding them is crucial to securing the best loan to buy a car for your circumstances.

- Not Shopping Around for Rates: This is perhaps the biggest mistake. Relying on the first offer you receive, especially from a dealership, almost guarantees you’re not getting the most competitive rate. Always get quotes from multiple sources – banks, credit unions, and online lenders – and use pre-approval to leverage your position.

- Focusing Only on Monthly Payment: While an affordable monthly payment is important, it shouldn’t be your sole focus. Dealers often try to "sell the payment" by extending the loan term, which drastically increases the total interest paid over time. Always ask for the total cost of the loan and the APR.

- Ignoring the Total Cost of the Loan: The sum of all your monthly payments plus your down payment is the true cost of your car. A low monthly payment on an 84-month loan might seem appealing, but you could end up paying significantly more in interest than if you chose a 60-month term with slightly higher payments.

- Extending the Loan Term Too Much: While longer terms reduce monthly payments, they also mean you’re "upside down" (owe more than the car is worth) for a longer period. This can be problematic if you need to sell or trade in the car prematurely. Furthermore, you’ll pay substantially more in interest.

- Not Getting Pre-Approved: As discussed, pre-approval is your most powerful tool. Without it, you lack negotiating leverage and might be pressured into less favorable dealership financing. It also helps you set a realistic budget.

- Ignoring Your Credit Score: Your credit score is paramount. Not checking it beforehand, or not taking steps to improve it, means you’re going into the loan process blind. A higher score translates directly into lower interest rates and better terms.

- Adding Unnecessary Add-ons: Dealerships are masters at bundling extra products like extended warranties, paint protection, or GAP insurance into your loan. While some might be useful, many are overpriced and inflate your loan amount, costing you more in interest. Carefully scrutinize and decline anything you don’t genuinely need or can find cheaper elsewhere.

From my vantage point, these are the most frequent missteps that prevent individuals from securing the best car loan. By being aware of these pitfalls, you can navigate the financing process with confidence and clarity.

Conclusion: Driving Away with Confidence

Finding the best loan to buy a car is a journey that demands research, patience, and an informed approach. It’s not merely about securing funds for a vehicle; it’s about making a sound financial decision that supports your long-term economic health. By understanding the different types of loans, knowing where to seek financing, and recognizing the factors that influence your terms, you empower yourself to make the smartest choice.

Remember, your credit score is your most valuable asset, a substantial down payment is your financial bedrock, and pre-approval is your ultimate negotiating tool. Avoid the common pitfalls of focusing solely on monthly payments or neglecting to shop around for the most competitive rates.

Armed with the insights from this comprehensive guide, you are now well-prepared to navigate the complexities of auto financing. Take your time, compare offers, read the fine print, and negotiate with confidence. Your dream car awaits, and with the right loan, you can drive it home knowing you’ve made a decision that is both exciting and financially savvy. Start your research today, get pre-approved, and embark on your car-buying adventure with peace of mind.