Driving Your Dream: Unlocking Luxury Car Loans Even with Bad Credit

Driving Your Dream: Unlocking Luxury Car Loans Even with Bad Credit Carloan.Guidemechanic.com

The allure of a luxury car is undeniable. The sleek lines, the powerful engine, the opulent interior – it’s more than just transportation; it’s a statement, an experience. However, for many, the dream often collides with the reality of a less-than-perfect credit score. The question "Can I really get a luxury car loan with bad credit?" echoes in the minds of aspiring high-end vehicle owners.

Based on my experience in the automotive financing world, the answer is a resounding "yes," but it comes with crucial caveats and requires a strategic, informed approach. This article isn’t about magic solutions; it’s a comprehensive guide to navigating the complexities of securing a luxury car with bad credit, empowering you with the knowledge to make that dream a tangible reality. We’ll dive deep into the challenges, unveil proven strategies, and provide the insider tips you need to confidently pursue your high-end automotive aspirations.

Driving Your Dream: Unlocking Luxury Car Loans Even with Bad Credit

The Dream vs. Reality: Understanding Bad Credit & Luxury Cars

Let’s first define what we’re talking about. "Bad credit" typically refers to a FICO score below 620-640, though some lenders consider anything under 660 as subprime. This score reflects your creditworthiness, or how likely you are to repay borrowed money. A lower score indicates a higher risk to lenders.

Now, let’s consider luxury cars. These aren’t just any vehicles; they often carry significantly higher price tags than their standard counterparts. This means larger loan amounts, which naturally increase the financial risk for any lender involved. Combining a high-value asset with a perceived high-risk borrower creates a challenging, but not impossible, scenario.

The good news is that the automotive financing landscape is vast and varied. While traditional banks might be hesitant, there are specialized lenders and unique strategies designed to help individuals in your position. It’s all about understanding the playing field and positioning yourself as the most attractive borrower possible, even with a credit history that tells a less-than-perfect story.

The Core Challenge: Why Lenders Are Wary of Bad Credit Luxury Car Loans

Before we explore solutions, it’s vital to understand the lender’s perspective. Why do they view bad credit luxury car loans as particularly risky? It boils down to several key factors that influence their decision-making process.

Firstly, higher loan amounts inherently mean higher risk. A luxury vehicle can easily cost $60,000, $80,000, or even well over $100,000. If a borrower defaults on such a substantial loan, the lender stands to lose a significant sum of money. This risk is amplified when the borrower’s credit history suggests a past struggle with debt repayment.

Secondly, lenders often perceive bad credit borrowers as having less financial stability. While this isn’t always true for everyone, the credit score acts as a quick indicator. They might worry about job security, emergency funds, or other financial obligations that could impact your ability to make consistent payments on a high-value loan. This perception directly influences their willingness to approve luxury car financing bad credit.

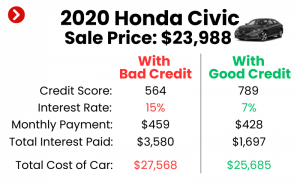

Interest rates also play a critical role. To offset the increased risk, lenders will typically offer higher interest rates for financing a luxury car with bad credit. While this allows them to make a profit even if a few borrowers default, it also means the total cost of the car will be significantly higher for you. Understanding this dynamic is crucial for setting realistic expectations.

Finally, luxury vehicles, like all cars, depreciate. Some luxury brands might hold their value better than others, but generally, the moment a new car leaves the lot, its value drops. If a bad credit borrower defaults early in the loan term, the lender might repossess a vehicle that is now worth less than the outstanding loan amount, resulting in a loss for them. This depreciation factor adds another layer of caution for lenders when considering high-end car loans bad credit.

Paving Your Path to Luxury: Strategies for Success with Bad Credit

Securing bad credit auto loans luxury requires a multi-faceted approach. You need to demonstrate reliability, reduce the lender’s risk, and present yourself as a committed borrower. Here are several proven strategies to help you achieve your goal.

Strategy 1: Know Your Credit Score and Report Inside Out

This is your starting point. You cannot fix what you don’t understand. Obtain your credit report from all three major bureaus (Experian, Equifax, TransUnion) and your FICO score. Many banks and credit card companies now offer free FICO scores to their customers.

Review every detail of your report for accuracy. Common mistakes to avoid are not checking for errors. Based on my experience, around 20-30% of credit reports contain some form of error, which could be negatively impacting your score. Disputing inaccuracies can quickly boost your score, making you a more attractive candidate for luxury vehicles bad credit financing. Understanding the factors that affect your score – payment history, amounts owed, length of credit history, new credit, and credit mix – will empower you to make targeted improvements. For a deeper dive, check out our guide on Understanding Your Credit Score: A Comprehensive Guide.

Strategy 2: Save a Significant Down Payment

This is perhaps the most impactful strategy for getting approved for luxury car loan bad credit. A substantial down payment directly addresses the lender’s primary concern: risk. When you put down a large sum of money, you reduce the total amount you need to borrow, thus decreasing the lender’s exposure.

Pro tips from us: Aim for at least 20% of the vehicle’s price, or even more if possible. A larger down payment shows the lender that you are financially committed to the purchase and have good saving habits. It also means you’ll have smaller monthly payments, making the loan more manageable for you and further reassuring the lender of your ability to repay. This financial commitment can often outweigh some of the negative aspects of a low credit score.

Strategy 3: Consider a Co-Signer with Excellent Credit

A co-signer with a strong credit history can be a game-changer. When someone with excellent credit co-signs your loan, they essentially promise to take over payments if you default. This significantly reduces the risk for the lender, as they now have two individuals legally responsible for the debt.

While this can open doors to better interest rates and approval, it’s crucial to understand the implications for your co-signer. Their credit will be affected if you miss payments, and it can impact their ability to secure other loans. Choose someone you trust deeply and ensure both of you are fully aware of the responsibilities involved. This isn’t a decision to take lightly.

Strategy 4: Explore Specific Lenders & Dealerships

Not all lenders are created equal, especially when it comes to bad credit luxury car loans. Traditional banks might have stricter criteria, but several types of institutions specialize in subprime lending.

- Subprime Lenders: These financial institutions specifically cater to borrowers with lower credit scores. They understand the challenges and are more willing to work with you, though often at higher interest rates.

- Captive Finance Companies: Many luxury car brands (e.g., Mercedes-Benz Financial Services, BMW Financial Services) have their own financing arms. While they often prefer strong credit, they might offer incentives or specialized programs to move inventory, sometimes being more flexible for certain models or promotions.

- Dealerships with Special Finance Departments: Many luxury dealerships have departments dedicated to helping customers with challenging credit. They work with a network of lenders, including subprime ones, to find suitable options. Common mistakes to avoid are not shopping around. Always compare offers from multiple sources.

Strategy 5: Choose the Right Luxury Vehicle (Smartly)

Your choice of vehicle can significantly impact your approval chances and loan terms. While the dream might be a brand-new, top-of-the-line model, a more pragmatic approach can yield better results.

- Used Luxury Vehicles: A pre-owned luxury car often comes at a much lower price point than a new one, reducing the overall loan amount needed. This immediately makes the loan less risky for lenders.

- Less Expensive Luxury Brands/Models: Consider entry-level luxury sedans or SUVs from reputable brands instead of their most expensive offerings. For example, a pre-owned Lexus ES or a lower-trim Audi A4 might be more attainable than a new Mercedes S-Class.

- Depreciation Considerations: Some luxury cars hold their value better than others. Researching depreciation rates can help you choose a vehicle that retains more equity, making it a safer bet for both you and the lender.

Strategy 6: Build Your Credit First (The Long Game)

This might not be the fastest path, but based on my experience, it is often the most reliable and financially sound strategy. Taking 6-12 months to actively improve your credit score can dramatically alter your financing options.

Practical steps include:

- Secured Credit Cards: These require a deposit, but they report to credit bureaus, helping you build a positive payment history.

- On-Time Payments: Consistently pay all your bills (credit cards, utilities, rent, existing loans) on time. Payment history is the biggest factor in your credit score.

- Reduce Debt: Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can significantly boost your score.

- Credit Builder Loans: Some credit unions offer small loans designed specifically to help you build credit.

Investing time in improving your credit will not only increase your chances of approval but also qualify you for much lower interest rates, saving you thousands over the life of the loan. This makes improving credit for luxury car a wise long-term goal.

Navigating the Application Process with Bad Credit

Once you’ve implemented these strategies, the application process for luxury car financing bad credit still requires careful attention. Being prepared and transparent is key.

Gathering Documentation: Lenders will want to see proof of your ability to repay. This typically includes:

- Proof of Income: Recent pay stubs, tax returns, or bank statements.

- Proof of Residency: Utility bills or lease agreements.

- Proof of Employment: Contact information for your employer.

- Identification: Driver’s license.

- Trade-in Information (if applicable): Title, registration, loan payoff amount.

Having all this ready streamlines the process and shows your seriousness.

Be Transparent and Honest: Don’t try to hide your credit issues. Lenders will pull your credit report anyway. Instead, be upfront and, if possible, explain any extenuating circumstances that led to your bad credit (e.g., medical emergency, job loss). This transparency can build a level of trust.

Prepare for Higher Interest Rates: With bad credit, you should expect to pay a higher Annual Percentage Rate (APR). This is the cost of borrowing money. While we aim for the best possible rate, be realistic. Your focus should be on getting approved for a manageable payment, and then potentially refinancing later when your credit improves.

Understanding Loan Terms: Before signing anything, thoroughly understand all aspects of the loan:

- APR: The true annual cost of your loan.

- Loan Term: How many months you’ll be paying. Longer terms mean lower monthly payments but more interest paid overall.

- Prepayment Penalties: Check if there are any fees for paying off your loan early.

- Fees: Be aware of any origination fees or other charges. Pro tip: Don’t accept the first offer. Always compare and negotiate.

Beyond Approval: Managing Your Luxury Car Loan Responsibly

Getting approved for a bad credit luxury car loan is a significant step, but the journey doesn’t end there. Responsible management of your loan is crucial for both enjoying your new vehicle and improving your financial future.

Making Timely Payments: This cannot be stressed enough. Every on-time payment you make is reported to the credit bureaus and will positively impact your credit score. Set up automatic payments to avoid missing due dates. This consistent behavior is what transforms bad credit into good credit over time.

Refinancing Opportunities: As your credit score improves (thanks to those timely payments!), you may become eligible to refinance your loan. Refinancing allows you to secure a new loan with a lower interest rate, potentially saving you thousands of dollars over the remaining loan term. Keep an eye on your credit score and current interest rates; typically, after 12-18 months of perfect payments, you might be a good candidate.

Budgeting for Ownership Costs: A luxury car comes with luxury expenses beyond the monthly payment. Common mistakes to avoid are underestimating these costs.

- Insurance: High-end vehicles generally cost more to insure. Get quotes before you finalize your purchase.

- Maintenance: Luxury cars often require specialized parts and labor, which can be more expensive. Factor in routine maintenance and potential repairs.

- Fuel: Many luxury vehicles require premium fuel, which adds to the running costs.

Ensure your budget comfortably accommodates all these expenses, not just the loan payment.

Is a Luxury Car with Bad Credit Right for You? A Candid Assessment

The ultimate question isn’t just "Can I get a luxury car loan with bad credit?" but "Should I?" This requires a candid assessment of your financial situation and priorities.

Weighing the Pros and Cons:

- Pros: Fulfilling a dream, potential for credit improvement through responsible payments, enjoying a higher-quality vehicle.

- Cons: Higher interest rates, increased overall cost, significant financial commitment, potential for financial strain if not budgeted properly.

Financial Stability vs. Immediate Gratification: It’s important to differentiate between a want and a need. While a luxury car is a powerful want, ensure it doesn’t jeopardize your financial stability. If the payments (including insurance, maintenance, and fuel) will stretch your budget to its absolute limit, it might be wiser to wait and continue building your credit.

Long-Term Credit Health: Remember, your primary goal with any loan, especially one with bad credit, should be to use it as a tool to improve your financial standing. If the luxury car loan helps you achieve this by demonstrating responsible repayment, then it can be a positive step. However, if it leads to missed payments and further debt, it will only exacerbate your credit issues.

Conclusion: Your Luxury Dream is Within Reach, with Smart Planning

The journey to securing bad credit luxury car loans is challenging, but absolutely achievable with the right strategies and a disciplined approach. It’s about demonstrating your commitment, understanding the nuances of subprime lending, and being proactive in improving your financial profile.

By knowing your credit, making a substantial down payment, exploring specialized lenders, considering a co-signer, and choosing your vehicle wisely, you significantly increase your chances of driving away in the luxury car you’ve always envisioned. Remember, every on-time payment is a step towards not only owning your dream car but also building a stronger financial future. Start planning today, check your credit, and take the informed steps necessary to turn that aspiration into a luxurious reality.