Driving Your Dream: Unveiling the Great Car Loan Companies for a Smooth Ride

Driving Your Dream: Unveiling the Great Car Loan Companies for a Smooth Ride Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect. Whether it’s the sleek lines of a brand-new sedan or the reliable charm of a pre-owned SUV, securing the right financing is often the first crucial step. A car loan isn’t just about getting money; it’s about finding a financial partner that understands your needs, offers fair terms, and supports your long-term financial health. This is where the concept of "Great Car Loan Companies" truly comes into play.

Choosing the right lender can significantly impact your monthly budget, the total cost of your vehicle, and your overall car ownership experience. This comprehensive guide will delve deep into what distinguishes truly great car loan companies from the rest, helping you navigate the complexities of auto financing with confidence and clarity. Our goal is to empower you with the knowledge to make an informed decision, ensuring your car loan is a stepping stone, not a stumbling block, to driving your dream.

Driving Your Dream: Unveiling the Great Car Loan Companies for a Smooth Ride

What Makes a Car Loan Company "Great"? Beyond Just Low Rates

When evaluating potential lenders, it’s tempting to focus solely on the advertised interest rate. While a low Annual Percentage Rate (APR) is undeniably attractive, it’s just one piece of a much larger puzzle. A truly great car loan company offers a holistic package that prioritizes the borrower’s best interests.

Based on my experience, the finest lenders demonstrate a commitment to transparency, exceptional customer service, and flexibility, alongside competitive pricing. They understand that every borrower’s situation is unique and offer solutions that cater to a wide spectrum of financial profiles.

Transparency and Clarity in Terms

A hallmark of a great lender is crystal-clear communication about all aspects of the loan. This means no hidden fees, no confusing jargon, and a straightforward explanation of interest calculations, payment schedules, and any potential penalties. You should be able to understand exactly what you’re agreeing to before you sign on the dotted line.

Transparency builds trust, which is invaluable in a financial relationship. A company that is upfront about all costs, including origination fees, late payment charges, or prepayment penalties, ensures you won’t encounter unwelcome surprises down the road. This level of honesty is a strong indicator of a reputable and customer-centric operation.

Exceptional Customer Service and Support

The loan process can sometimes feel overwhelming, especially for first-time buyers. A great car loan company provides readily accessible and knowledgeable customer support. This includes helpful representatives who can answer your questions, guide you through the application, and assist with any issues that arise during the life of your loan.

Effective customer service goes beyond just problem-solving. It involves proactive communication, easy-to-use online portals, and a genuine willingness to help borrowers succeed. Proactive support, like payment reminders or clear instructions on how to manage your account, contributes significantly to a positive borrowing experience.

Flexibility in Loan Products and Terms

Life happens, and a great lender understands this. They offer a range of loan products tailored to different needs, whether you’re buying new or used, looking for a short or long-term loan, or even considering refinancing. Furthermore, they may offer flexible payment options or grace periods in certain circumstances, demonstrating a willingness to work with their customers.

This flexibility extends to accommodating various credit scores. While rates will naturally differ, a great company strives to provide viable options for individuals with excellent credit, fair credit, or even those rebuilding their credit history. Their goal is to find a solution that fits your budget and helps you achieve your car ownership goals.

Reputation and Trustworthiness

A company’s reputation precedes it. Great car loan companies consistently receive positive reviews and high ratings from their customers. They are often recognized for their ethical practices, reliable service, and commitment to consumer satisfaction. Checking independent review sites and consumer protection agencies can offer valuable insights.

Trustworthiness is built over time through consistent, fair dealings. A lender with a solid reputation demonstrates stability and reliability, assuring you that they will be a dependable partner throughout your loan term. Common mistakes to avoid are ignoring these reviews, as they often highlight critical aspects of a company’s performance.

Efficiency and Streamlined Processes

In today’s fast-paced world, efficiency is key. Great lenders offer streamlined application processes, often with online options for pre-approval and document submission. Quick decision-making and efficient disbursement of funds mean you can get into your new vehicle sooner without unnecessary delays or bureaucratic hurdles.

A smooth, efficient process not only saves you time but also reduces stress. From the initial inquiry to the final loan signing, every step should be intuitive and well-supported. This attention to process optimization is a strong indicator of a modern and user-friendly financial institution.

Types of Great Car Loan Companies and Lenders

The landscape of auto financing is diverse, with several types of institutions offering car loans. Each has its unique strengths and may be a better fit depending on your financial situation and preferences. Understanding these categories is essential for finding the great car loan companies that align with your needs.

Traditional Banks: Established and Reliable

Major national and regional banks are often the first place people consider for car loans. They are well-established, widely recognized, and can offer competitive rates, especially for borrowers with excellent credit histories. Their extensive branch networks also provide a sense of familiarity and in-person support.

Banks typically have a wide range of financial products, allowing for potential bundling opportunities if you already bank with them. However, their application processes can sometimes be more stringent, and approval times might be longer compared to online-only lenders. It’s always wise to compare their offers, particularly if you have a strong credit profile.

Credit Unions: Member-Focused and Flexible

Credit unions are non-profit financial cooperatives owned by their members. This structure often translates into lower interest rates, fewer fees, and more personalized customer service compared to traditional banks. They are known for being more understanding and flexible, particularly for borrowers with less-than-perfect credit.

Pro tips from us: Don’t overlook local credit unions. While you typically need to be a member to secure a loan, membership requirements are often quite broad (e.g., living in a certain area, working for a specific employer, or joining a small association). Their focus on member well-being often leads to a more favorable borrowing experience.

Online Lenders: Speed, Convenience, and Variety

The digital age has brought forth a plethora of online lenders that specialize in auto financing. These companies often boast incredibly fast application and approval processes, sometimes within minutes. They are highly convenient, allowing you to compare offers from the comfort of your home, and many cater to a broader spectrum of credit scores, including those with fair or even bad credit.

Online lenders leverage technology to streamline operations, which can sometimes translate into lower overhead and potentially lower rates. However, it’s crucial to exercise due diligence. Ensure any online lender you consider is reputable, has strong customer reviews, and offers secure online transactions. Their digital nature means less personal interaction, which might not suit everyone.

Dealership Financing: One-Stop Shop Convenience

Many car dealerships offer financing options directly through their sales departments. This can be incredibly convenient, allowing you to handle the entire car buying and financing process in one location. Dealerships often work with a network of lenders, including captive finance companies (lenders owned by the car manufacturer, like Toyota Financial Services or Ford Credit) and third-party banks or credit unions.

While convenient, it’s a common mistake to solely rely on dealership financing without first exploring other options. Dealerships sometimes mark up interest rates to profit from the loan, so the rate you’re offered might not be the absolute best available to you. Always get pre-approved elsewhere before heading to the dealership to have a strong negotiating position.

Key Factors to Consider When Choosing a Car Loan Company

Selecting the right car loan is a complex decision that extends beyond simply picking a lender. You need to carefully evaluate the specific terms and conditions of each offer. Understanding these critical factors will empower you to identify the most advantageous loan for your situation.

Interest Rates (APR)

The Annual Percentage Rate (APR) is perhaps the most significant factor influencing the total cost of your loan. It represents the annual cost of borrowing, including the interest rate and certain fees. A lower APR means less money paid over the life of the loan. Your credit score, the loan term, and the current market conditions all play a role in determining the APR you’ll be offered.

It’s crucial to compare APRs from multiple lenders, not just the base interest rate. This comprehensive figure gives you a true apples-to-apples comparison of the actual cost of borrowing. Even a slight difference in APR can translate into hundreds or thousands of dollars saved over several years.

Loan Terms and Duration

The loan term refers to the length of time you have to repay the loan, typically ranging from 36 to 84 months. A shorter loan term usually means higher monthly payments but a lower total interest paid over the life of the loan. Conversely, a longer loan term results in lower monthly payments, making the car more "affordable" on a month-to-month basis, but you’ll pay significantly more in interest over time.

Carefully consider your budget and financial goals when choosing a loan term. While a lower monthly payment can be tempting, always calculate the total cost of the loan to understand the long-term financial commitment. Balancing affordability with total cost is key to smart borrowing.

Fees and Penalties

Beyond the interest rate, be vigilant about any additional fees associated with the loan. These can include origination fees, application fees, documentation fees, or even prepayment penalties. Some lenders charge a fee if you pay off your loan early, which could negate some of the benefits of early repayment.

A great car loan company will be transparent about all fees upfront. Always read the fine print of the loan agreement to identify any hidden costs that could increase your total expenditure. Understanding these fees helps prevent unexpected charges and ensures you’re comparing offers accurately.

Eligibility Requirements

Each lender has specific criteria for loan approval, often centered around your credit score, income, and debt-to-income ratio. Some lenders specialize in prime borrowers with excellent credit, offering the lowest rates, while others cater to individuals with fair or even poor credit, albeit with higher interest rates.

Before applying, it’s beneficial to understand a lender’s typical eligibility requirements. This can help you target lenders where you have a higher chance of approval and avoid unnecessary credit inquiries. Being prepared means you can efficiently seek out the best options for your specific financial situation.

Customer Service and Online Tools

The quality of customer service and the availability of convenient online tools can greatly enhance your borrowing experience. Look for lenders with accessible support channels (phone, email, chat) and robust online platforms for managing your account, making payments, and accessing statements.

Efficient digital tools and responsive human support indicate a lender’s commitment to borrower satisfaction. Easy access to your loan information and the ability to resolve issues quickly contribute to a stress-free loan management process. This aspect is often overlooked but can make a significant difference in your long-term satisfaction.

Pre-approval Process

One of the most valuable steps in securing a car loan is getting pre-approved before you even set foot in a dealership. Pre-approval involves a lender reviewing your financial information and tentatively approving you for a specific loan amount at an estimated interest rate. This process typically involves a "soft" credit inquiry, which doesn’t harm your credit score.

The benefits of pre-approval are immense. It gives you a clear budget, transforms you into a cash buyer at the dealership, and empowers you to negotiate vehicle prices more effectively, rather than being focused on monthly payments. Having a pre-approval in hand also provides a benchmark against which to compare any financing offers from the dealership.

Navigating Different Credit Scenarios with Great Lenders

Your credit score is a major determinant of the interest rate and loan terms you’ll receive. However, having less-than-perfect credit doesn’t mean you can’t find a great car loan. It simply means you need to be more strategic in your search and understand which lenders are best suited for your credit profile.

Excellent/Good Credit: Access to Prime Rates

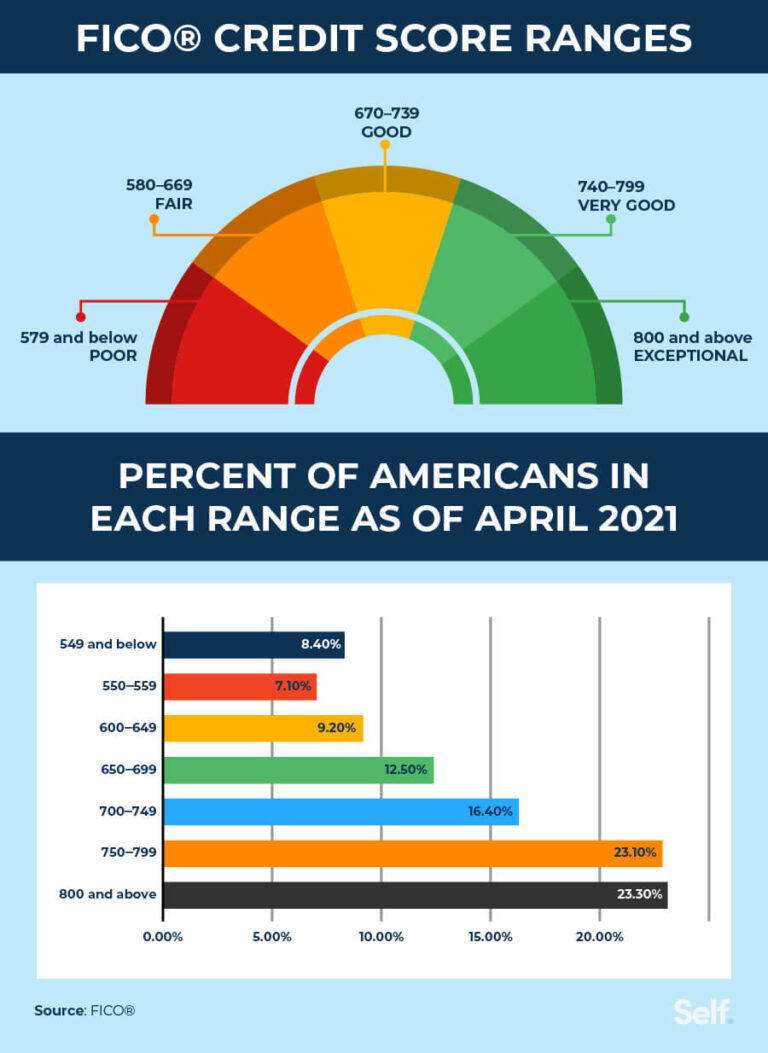

If you boast an excellent or good credit score (typically FICO scores above 670), you are in a prime position to secure the most competitive interest rates and favorable loan terms. Great car loan companies, including major banks, credit unions, and top online lenders, will actively compete for your business.

Pro Tip: Even with stellar credit, don’t settle for the first offer. Shop around and compare multiple pre-approvals to ensure you’re getting the absolute best deal available. Your strong credit is a powerful negotiating tool, so leverage it to your full advantage.

Average/Fair Credit: More Options Than You Think

Borrowers with average or fair credit (FICO scores generally between 580 and 669) will find more options than those with bad credit, though rates will be higher than for prime borrowers. Many online lenders and credit unions are particularly adept at working with this credit tier, often offering reasonable rates if other financial indicators (like income stability) are strong.

Focus on lenders that specialize in a broader range of credit profiles. While you might not qualify for the absolute lowest APRs, you can still find competitive offers. Consider ways to improve your credit score slightly before applying, as even a small bump can open up better rate possibilities.

Bad Credit/No Credit: Strategic Approaches for Approval

Securing a car loan with bad credit (FICO scores below 580) or no credit history can be challenging, but it is certainly not impossible. Several lenders specialize in subprime auto loans, and credit unions are often more willing to consider individual circumstances. You might encounter higher interest rates and potentially shorter loan terms to mitigate risk for the lender.

Common mistakes to avoid are jumping at the first offer without comparing, as predatory lenders sometimes target those with bad credit. Explore options like adding a co-signer with good credit, which can significantly improve your chances of approval and secure a better rate. For more on securing a car loan with less-than-perfect credit, check out our detailed guide on .

The Application Process: What to Expect

Understanding the typical car loan application process can demystify it and help you prepare effectively. Being organized and informed will streamline your experience and increase your chances of a smooth approval.

Gathering Your Documents

Before you even begin filling out applications, gather all necessary documentation. This typically includes a valid government-issued ID (driver’s license or state ID), proof of income (pay stubs, tax returns, bank statements), proof of residence (utility bill, lease agreement), and details about your current employment. You will also need information about the vehicle you intend to purchase, if you’ve already chosen one, and proof of car insurance once the loan is approved.

Having these documents readily available will significantly speed up the application process. It demonstrates your readiness and can prevent delays, allowing lenders to quickly verify your financial information.

Applying for Pre-approval

As discussed, applying for pre-approval is a highly recommended first step. You can do this with multiple lenders – banks, credit unions, and online providers – within a short timeframe (usually 14-45 days, depending on the credit scoring model) without significantly impacting your credit score. This is because multiple inquiries for the same type of loan are often grouped as a single inquiry.

The pre-approval process gives you a realistic understanding of what you can afford and the interest rate you qualify for. This knowledge is a powerful tool when you step onto the dealership lot, allowing you to focus on negotiating the vehicle price rather than getting caught up in financing discussions.

Reviewing Loan Offers

Once you receive pre-approval offers, take the time to carefully review and compare them. Look beyond just the monthly payment. Scrutinize the APR, the total loan amount, the loan term, and any associated fees. Understand the difference between a fixed-rate loan (where your interest rate remains constant) and a variable-rate loan (where it can fluctuate).

A great car loan company will present their offers clearly, allowing for easy comparison. Don’t hesitate to ask questions if anything is unclear. Your goal is to choose the offer that provides the best overall value and fits comfortably within your budget.

Finalizing the Loan

After selecting your preferred lender and finding your vehicle, the final step is to formalize the loan. This involves signing the loan agreement, which is a legally binding contract. Before signing, read every page meticulously. Ensure that all the terms and conditions discussed and agreed upon are accurately reflected in the document.

Pay close attention to the total loan amount, the repayment schedule, any late payment penalties, and the process for early repayment if you plan to do so. Once signed, the funds will be disbursed, and you’ll officially be the proud owner of your new car, with a clear path to repayment.

Refinancing Your Car Loan: Another Path to Greatness

Your financial situation isn’t static, and neither should your car loan be. Refinancing your existing auto loan is a smart strategy that can unlock better terms and significant savings, effectively turning your current loan into a "great" one.

When to Consider Refinancing

There are several compelling reasons to consider refinancing your car loan. Perhaps your credit score has significantly improved since you initially took out the loan, making you eligible for lower interest rates. Market interest rates might have dropped, or you might have found a better offer from another lender. You could also be looking to lower your monthly payments by extending the loan term, or conversely, shorten the term to pay off the car faster and reduce total interest.

Many borrowers also refinance to remove a co-signer, consolidate debt, or simply get a better deal than what was originally offered at the dealership. Evaluating your current loan against new offers is a financially savvy move.

Benefits of Refinancing

The primary benefit of refinancing is the potential to save money. A lower interest rate translates directly into less interest paid over the life of the loan. This can significantly reduce your total cost of ownership. Alternatively, lowering your monthly payment can free up cash flow in your budget, providing financial breathing room.

Refinancing also offers flexibility. You can adjust your loan term to better suit your current financial goals – whether that’s paying off the car faster or reducing your monthly expenses. It’s a proactive way to take control of your auto financing.

How Great Companies Handle Refinancing

Great car loan companies don’t just focus on new loans; they also offer competitive and straightforward refinancing options. They provide easy online applications, quick approvals, and transparent terms for refinancing. They understand that a satisfied customer, even one who wasn’t originally theirs, can become a loyal customer through a positive refinancing experience.

Look for lenders that specifically advertise competitive refinancing rates and have a clear, simple process. Learn more about refinancing strategies in our article, .

Pro Tips for Finding Your Great Car Loan Company

Navigating the car loan market can feel daunting, but with a strategic approach, you can significantly improve your chances of securing an excellent deal. These pro tips are designed to empower you in your search.

Shop Around and Compare Multiple Offers

This is arguably the most crucial piece of advice. Never settle for the first loan offer you receive, especially from a dealership. Apply for pre-approval with at least three to five different lenders, including banks, credit unions, and online lenders. Compare their APRs, loan terms, fees, and customer service reviews.

A competitive marketplace works in your favor. By having multiple offers in hand, you gain leverage and can confidently choose the option that truly serves your financial best interest. This comparison process ensures you’re getting the best possible terms.

Check Your Credit Score Beforehand

Knowing your credit score is like having a roadmap. Before applying for any loans, obtain a free copy of your credit report from each of the three major bureaus (Equifax, Experian, TransUnion) and check your credit score. This allows you to identify any errors that could be negatively impacting your score and gives you a realistic expectation of the rates you might qualify for.

Understanding your credit profile beforehand can save you time and frustration. If your score is lower than desired, you might consider taking steps to improve it before applying, such as paying down existing debts or correcting inaccuracies on your report.

Read Reviews and Testimonials

In today’s connected world, the experiences of other customers are invaluable. Before committing to a lender, thoroughly research their reputation online. Look for reviews on independent consumer sites, Better Business Bureau ratings, and social media. Pay attention to comments regarding transparency, customer service, and the efficiency of their process.

While individual experiences can vary, consistent patterns in reviews can highlight a company’s strengths or weaknesses. A lender with overwhelmingly positive feedback is generally a safer and more reliable choice.

Don’t Be Afraid to Negotiate

Even with pre-approval, remember that loan terms can sometimes be negotiable. If a dealership offers you a financing package, compare it directly to your pre-approved offers. If their offer is higher, you can use your pre-approval as leverage to ask them to match or beat it.

Negotiation isn’t just for the car’s price; it extends to financing as well. A great car loan company or a competitive dealership will often be willing to work with you to secure your business, especially if you present a strong alternative offer.

Understand the Fine Print

This cannot be stressed enough: always, always read the entire loan agreement before signing. Don’t skim. Pay close attention to sections on interest calculation, payment schedules, late fees, prepayment penalties, and any clauses regarding repossession or default.

If you encounter any terms you don’t understand, ask for clarification. A reputable lender will patiently explain every detail. Signing a contract you don’t fully comprehend is a common mistake that can lead to costly surprises down the line.

Common Mistakes to Avoid

Even with the best intentions, borrowers can sometimes make missteps that lead to less-than-ideal car loan outcomes. Being aware of these common pitfalls can help you steer clear of them.

Not Getting Pre-Approved

One of the biggest mistakes is walking into a dealership without a pre-approval in hand. This leaves you vulnerable to the dealership’s financing offers, which may not be the most competitive. Without a benchmark, you lack the power to negotiate or even know if you’re getting a fair deal.

Always secure independent pre-approval first. It gives you a clear budget, puts you in a stronger negotiating position, and ensures you have a backup plan if dealership financing isn’t favorable.

Focusing Only on the Monthly Payment

While managing your monthly budget is important, fixating solely on the lowest possible monthly payment is a common trap. Lenders can easily lower monthly payments by simply extending the loan term, which drastically increases the total amount of interest you’ll pay over time.

Always consider the total cost of the loan, including all interest and fees, alongside the monthly payment. A slightly higher monthly payment for a shorter term can save you thousands in the long run.

Ignoring the Total Cost of the Loan

This mistake goes hand-in-hand with focusing only on monthly payments. Many borrowers fail to calculate the comprehensive cost of the loan over its entire term. A low monthly payment might seem attractive, but if it’s spread over 72 or 84 months, the accumulated interest can be substantial.

Always use a loan calculator to determine the total amount you will repay, including principal and interest. This holistic view helps you understand the true financial commitment and identify the most cost-effective loan.

Not Reading the Fine Print

As mentioned before, failing to thoroughly read and understand every clause of your loan agreement can lead to significant problems. Hidden fees, unexpected penalties, or unfavorable terms can be buried in the small print.

Take your time. Ask questions. Do not feel pressured to sign anything until you are 100% clear on all terms and conditions. Your signature is a legal agreement, and you must know what you are agreeing to.

Letting the Dealership Be Your Only Source of Financing

While convenient, relying solely on the dealership for financing limits your options and negotiating power. Dealerships often act as intermediaries, and they may mark up interest rates to earn a commission.

Always shop around for your own financing first. Having an outside offer provides you with a baseline for comparison and gives you the confidence to either accept a better offer from the dealership or walk away and use your independent financing. For unbiased consumer financial advice, we recommend visiting the Consumer Financial Protection Bureau (CFPB) website at .

Conclusion

Finding great car loan companies is not merely about securing funds; it’s about establishing a relationship with a financial partner that supports your journey to vehicle ownership responsibly and transparently. By understanding what constitutes a "great" lender, exploring the various types of financial institutions, and meticulously evaluating loan terms, you empower yourself to make the best decision for your financial future.

Remember, a low APR is just one component. Prioritize transparency, exceptional customer service, flexibility, and a solid reputation. Arm yourself with knowledge about your credit score, shop around for multiple pre-approvals, and always read the fine print. By avoiding common mistakes and leveraging these pro tips, you can navigate the car loan landscape with confidence. Your dream car awaits, and with the right financing, the ride will be even smoother. Start your informed search today and drive away with peace of mind!