Driving Your Dreams: A Comprehensive Guide to Car Loans with Good Credit and Low Income

Driving Your Dreams: A Comprehensive Guide to Car Loans with Good Credit and Low Income Carloan.Guidemechanic.com

For many, owning a reliable car is more than just a convenience; it’s a necessity, a gateway to better job opportunities, and a crucial link to daily life. However, the path to car ownership can seem daunting, especially if you have a lower income. The good news is that possessing a strong credit score can be your most powerful ally, even when your earnings are modest.

This comprehensive guide will demystify the process of securing a car loan when you have good credit but a lower income. We’ll explore how to leverage your excellent credit history, navigate the financial landscape, and secure an affordable loan that fits your budget. Our goal is to empower you with the knowledge and strategies to drive away in your dream car without financial strain.

Driving Your Dreams: A Comprehensive Guide to Car Loans with Good Credit and Low Income

The Unique Intersection: Good Credit, Low Income, and Car Loans

Before diving into the "how," let’s truly understand the dynamic at play. You have diligently built a robust credit history, demonstrating responsible financial behavior. This is a significant achievement and a valuable asset. However, your current income might not be as high as you’d like, which can sometimes raise concerns for lenders.

The key here is understanding how lenders assess risk. While income is a factor, your credit score speaks volumes about your reliability as a borrower. It tells them you’re likely to repay your debts, which can often mitigate concerns about a lower income, especially if the loan amount is sensible for your financial situation. This combination presents a unique opportunity, allowing you to access favorable terms that might be out of reach for someone with a low income and poor credit.

What "Good Credit" Really Means for Car Loans

When we talk about "good credit" in the context of car loans, we’re generally referring to a FICO score of 670 or higher, with "very good" starting around 740 and "excellent" at 800+. Lenders use these scores as a quick snapshot of your financial reliability. A higher score signals lower risk, which directly translates to better loan offers.

A strong credit score tells lenders that you have a history of making payments on time, managing various types of credit responsibly, and not overextending yourself. This track record of fiscal discipline is invaluable. It acts as a powerful counterbalance to a lower income, assuring lenders that you are a dependable borrower.

Understanding the "Low Income" Factor

"Low income" is a subjective term, but for car loans, it primarily relates to your ability to comfortably afford monthly payments and overall car ownership costs without jeopardizing other essential expenses. Lenders will look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income.

While your income might not be high, demonstrating stability and a reasonable DTI is crucial. This means having a steady job, even if the pay is modest, and ensuring your existing debts aren’t overwhelming. The challenge isn’t just about qualifying for a loan; it’s about securing one that doesn’t stretch your budget thin, allowing you to maintain financial health long-term.

Why Your Good Credit Is Your Superpower (Even with Low Income)

Your excellent credit score is not just a number; it’s a powerful negotiating tool. It opens doors that would otherwise remain closed, providing significant advantages when seeking a car loan. This is where your financial discipline truly pays off.

Access to Lower Interest Rates

The most direct benefit of good credit is access to lower interest rates. Lenders offer their best rates to borrowers they perceive as low-risk. With a high credit score, you fit this profile perfectly. Even a small difference in the interest rate can save you hundreds, if not thousands, of dollars over the life of the loan.

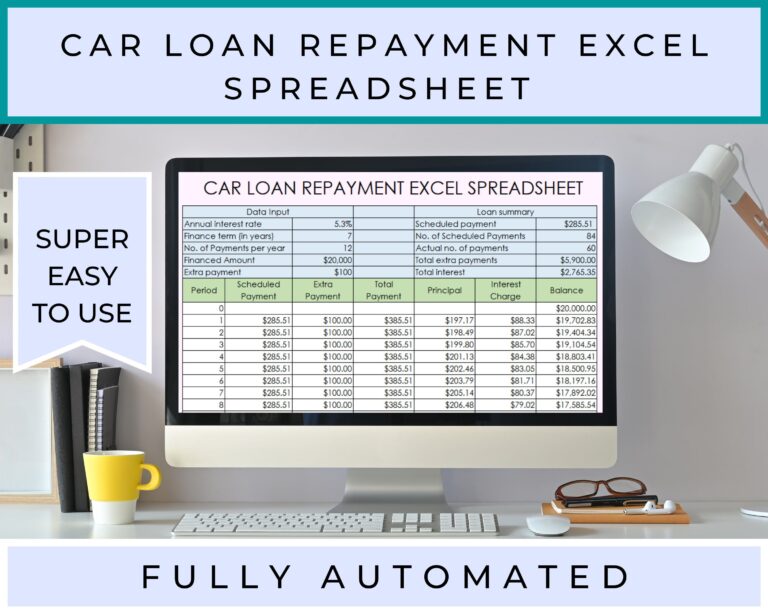

Consider this: on a $20,000 loan over five years, reducing your interest rate from 7% to 4% could save you over $1,900 in total interest paid. That’s a substantial sum, especially when you’re managing a lower income. These savings can then be allocated to other essential expenses or even towards a larger down payment on your next vehicle.

Better Loan Terms and Flexibility

Beyond interest rates, good credit can also grant you more favorable loan terms. This might include a longer repayment period, which can lower your monthly payments, or more flexible conditions regarding down payments. Lenders are more willing to work with borrowers who have proven their reliability.

This flexibility can be incredibly beneficial when your income is limited. It allows you to tailor the loan to fit your budget more precisely, ensuring the monthly payment is manageable and doesn’t create financial stress. You might also find lenders more willing to offer grace periods or other support if unexpected financial challenges arise.

More Lender Options

A strong credit score significantly expands your choice of lenders. You won’t be limited to subprime lenders who cater to higher-risk borrowers with less favorable terms. Instead, you can approach traditional banks, credit unions, and reputable online lenders, all vying for your business.

Having more options means you can shop around and compare offers, ultimately selecting the best deal available. This competitive environment works in your favor, as lenders are motivated to provide attractive rates and terms to secure your business. Based on my experience, comparing at least three different loan offers is a non-negotiable step to ensure you’re getting the most competitive rate.

Reduced Overall Cost of Ownership

Ultimately, lower interest rates and better terms translate into a reduced overall cost for your car. This isn’t just about the purchase price; it’s about the total amount you pay over the life of the loan. When every dollar counts, minimizing these costs is paramount.

A lower overall cost frees up more of your income for other needs, contributing to your overall financial stability. It makes car ownership more sustainable and less of a burden, allowing you to enjoy the benefits of having a vehicle without constant worry about payments.

Navigating the "Low Income" Aspect – Strategies for Success

While your good credit is a huge asset, addressing the "low income" component requires strategic planning. It’s about demonstrating financial prudence and choosing a loan and a vehicle that truly align with your budget.

Budgeting Like a Pro: Beyond the Monthly Payment

One of the common mistakes to avoid is focusing solely on the monthly car payment. Car ownership involves many other expenses that can quickly add up, especially on a lower income. A truly successful car loan strategy requires a comprehensive budget that accounts for every potential cost.

- Insurance: This can be a significant expense, varying widely based on your age, driving record, location, and the vehicle type. Get quotes before you buy.

- Fuel: Estimate your weekly or monthly fuel costs based on your commute and driving habits.

- Maintenance & Repairs: Even reliable cars need oil changes, tire rotations, and occasional repairs. Factor in an emergency fund for unexpected issues.

- Registration & Taxes: Annual fees and potential sales tax on the purchase are part of the deal.

- Parking Fees/Tolls: If applicable, these can add up.

Pro tips from us: Create a detailed spreadsheet or use a budgeting app to track all these potential expenses. Be realistic about what you can truly afford. It’s always better to underestimate your income and overestimate your expenses to build a buffer.

The Debt-to-Income (DTI) Ratio Explained: Why It Matters

Lenders pay close attention to your Debt-to-Income (DTI) ratio. This percentage indicates how much of your gross monthly income goes towards paying debts. A lower DTI ratio suggests you have more disposable income to handle new debt, making you a less risky borrower. Most lenders prefer a DTI of 36% or lower, though some might go up to 43% for car loans.

To calculate your DTI, add up all your monthly debt payments (credit cards, student loans, mortgage/rent, etc.) and divide that sum by your gross monthly income (before taxes). For example, if your total monthly debt payments are $1,000 and your gross monthly income is $3,000, your DTI is 33.3%. Keeping this number low is critical.

If your DTI is on the higher side, consider paying down existing debts before applying for a car loan. Even reducing a small credit card balance can make a difference. This proactive step demonstrates financial responsibility and improves your chances of approval and better rates.

The Power of a Down Payment

Even with good credit, a substantial down payment can significantly strengthen your loan application, especially with a lower income. A larger down payment reduces the amount you need to borrow, which directly lowers your monthly payments and the total interest paid over the life of the loan.

Furthermore, a down payment shows the lender you have "skin in the game" and are committed to the purchase. It also provides a buffer against immediate depreciation, preventing you from being "upside down" on your loan (owing more than the car is worth) early on. Aim for at least 10-20% of the vehicle’s purchase price if possible.

Choosing the Right Vehicle: Realistic Expectations

This might be the most crucial step when managing a lower income. Your good credit allows you to qualify for certain loans, but your income dictates what you can afford. Resist the temptation to overextend yourself for a brand-new, luxury vehicle.

- New vs. Used: Used cars typically come with a lower purchase price, lower insurance costs, and less rapid depreciation. Based on my experience, a reliable used car often offers the best value for someone managing a lower income, allowing you to get a quality vehicle without the hefty price tag of a new model.

- Reliability: Research vehicle reliability ratings. A car that constantly breaks down will quickly negate any savings from a lower purchase price due to repair costs. Look for models known for their longevity and low maintenance.

- Fuel Efficiency: Prioritize fuel-efficient models. High gas prices can quickly erode a modest budget.

- Insurance Costs: Get insurance quotes for specific models you’re considering. Some cars are significantly more expensive to insure than others.

Finding the Right Lender – Where to Look

Your good credit gives you the luxury of choice. Don’t settle for the first offer you receive. Explore various lending institutions to find the best terms tailored to your situation.

Credit Unions: Often Your Best Bet

Credit unions are non-profit organizations that are member-owned. They often offer more competitive interest rates and flexible terms than traditional banks, especially for members. They tend to be more community-focused and might be more willing to work with individuals who have unique financial situations, like good credit with a lower income.

If you’re not already a member, consider joining one. Membership requirements are usually straightforward, often just requiring a small deposit. Many credit unions also offer personalized service and financial counseling, which can be invaluable.

Online Lenders: Speed and Convenience

The digital age has brought a plethora of online lenders that specialize in car loans. These platforms offer the convenience of applying from home, often with quick approval processes. They also make it easy to compare multiple offers from different lenders through a single application.

Reputable online lenders like Capital One Auto Finance, LightStream, and others can be excellent options. Just ensure you’re dealing with a legitimate and well-reviewed institution. Read reviews and compare their offerings carefully.

Traditional Banks: Leverage Existing Relationships

If you have a long-standing banking relationship, your current bank or a large national bank could be a good option. They might offer preferential rates to existing customers, especially if you have other accounts or investments with them.

While they might not always have the absolute lowest rates, the convenience and trust of working with an established institution can be appealing. It’s always worth checking what your bank can offer before looking elsewhere.

Dealership Financing: Convenience vs. Cost

Dealerships often offer financing options directly through their partnerships with various lenders. This can be convenient, as you can handle the car purchase and financing in one place. However, it’s crucial to approach dealership financing with caution.

While they might advertise attractive rates, their primary goal is to sell cars. Always get pre-approved for a loan before visiting the dealership. This way, you have a benchmark to compare against their offers and can negotiate from a position of strength. Never let them rush you into signing anything without thoroughly reviewing the terms. For more insights on choosing the right loan, you might find this article on understanding loan terms helpful: .

External Link Pro Tip: To better understand your rights and the various types of consumer loans available, the Consumer Financial Protection Bureau (CFPB) offers excellent resources. Visit their website at https://www.consumerfinance.gov/ for unbiased information.

The Application Process – Your Step-by-Step Guide

Approaching the loan application process strategically can make a significant difference in your outcome. Preparation is key to securing the best terms.

Pre-Approval is Your Best Friend

Never walk into a dealership without a pre-approval in hand. Pre-approval means a lender has conditionally agreed to lend you a specific amount at a particular interest rate, based on your creditworthiness and financial information. It’s a powerful tool because:

- It sets a budget: You know exactly how much you can afford before you start shopping.

- It gives you leverage: You can negotiate the car price more effectively, as you’re not reliant on the dealership’s financing.

- It saves time: The financing aspect is largely handled, speeding up the purchase process.

Most pre-approvals involve a soft credit pull, which doesn’t impact your credit score. Once you proceed with a full application, a hard inquiry will occur.

Gather Your Documents

Lenders will require various documents to verify your identity, income, and residency. Having these ready will streamline the application process:

- Proof of Identity: Driver’s license, state ID.

- Proof of Income: Pay stubs (from the last 1-3 months), W-2 forms, tax returns (if self-employed), bank statements.

- Proof of Residency: Utility bills, lease agreement.

- Social Security Number.

- References: Sometimes requested, but less common for car loans.

Organizing these documents beforehand shows professionalism and readiness, making the process smoother for both you and the lender.

Review Your Credit Report: Spotting Errors

Before applying for any loan, obtain a free copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Scrutinize it for any errors or inaccuracies. Even a small mistake could negatively impact your score and affect your loan terms.

If you find errors, dispute them immediately with the credit bureau. This process can take time, so start well in advance of your loan application. Understanding your credit report also helps you identify areas for improvement and ensures lenders are working with accurate information.

Negotiating Like a Pro: Not Just the Car Price

Many people focus solely on negotiating the car’s price, but with a pre-approved loan, you also have room to negotiate the loan terms. While your interest rate might be fixed by your pre-approval, you can discuss other aspects.

- Loan Term: A shorter term means higher monthly payments but less interest paid overall. A longer term means lower monthly payments but more interest. Choose what fits your budget best.

- Fees: Be aware of any origination fees or other charges associated with the loan. Some lenders may waive certain fees for highly qualified borrowers.

- Add-ons: Dealerships often try to sell extended warranties, GAP insurance, or other add-ons. While some might be useful, evaluate them carefully and consider purchasing them separately if the dealership’s price is inflated.

Common Mistakes to Avoid When Getting a Car Loan

Even with good credit, certain pitfalls can derail your efforts or lead to a less favorable outcome. Awareness is your first line of defense.

- Not Budgeting for Total Ownership Costs: As mentioned earlier, ignoring insurance, maintenance, and fuel can lead to financial strain down the road. This is the most common mistake people make.

- Skipping Pre-Approval: Going to the dealership without pre-approval puts you at a disadvantage. You lose negotiating power and might feel pressured into unfavorable financing.

- Focusing Only on the Monthly Payment: A low monthly payment might seem attractive, but it often comes with a longer loan term and significantly more interest paid over time. Always consider the total cost of the loan.

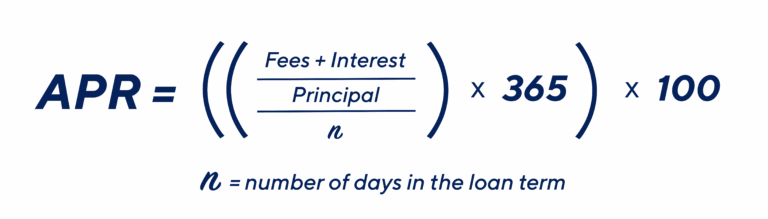

- Ignoring the Fine Print: Read every clause of your loan agreement carefully. Understand the interest rate, APR, fees, prepayment penalties, and late payment clauses. Don’t be afraid to ask questions.

- Applying to Too Many Lenders at Once: While it’s good to shop around, multiple hard credit inquiries within a short period can temporarily lower your credit score. Most credit scoring models will count multiple car loan inquiries within a 14-45 day window as a single inquiry, so do your rate shopping within that timeframe.

Post-Loan Approval – Maintaining Financial Health

Securing your car loan is a significant achievement, but the journey doesn’t end there. Maintaining good financial habits ensures you continue to build your credit and enjoy your vehicle without stress.

Making Timely Payments

This might seem obvious, but consistently making your car loan payments on time is paramount. Payment history is the most significant factor in your credit score. Missing even one payment can severely damage your credit and incur late fees.

Set up automatic payments if possible, or create reminders to ensure you never miss a due date. This diligent approach will further strengthen your credit profile, paving the way for even better financial opportunities in the future.

Considering Refinancing in the Future

Life circumstances change. Your income might increase, or interest rates might drop. If either of these happens, consider refinancing your car loan. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

This can significantly reduce your monthly payments or the total interest you pay over the loan’s life. Keep an eye on market rates and your financial situation; refinancing can be a smart move to save money.

Building Your Credit Further

Your car loan can be a powerful tool for continuing to build an excellent credit history. By consistently making on-time payments, you’re demonstrating responsible financial behavior. This positive activity will be reflected in your credit report and score.

Look for other ways to build your credit, such as keeping credit card balances low, paying off other debts, and diversifying your credit mix responsibly. The stronger your credit, the more financial doors will open for you in the future. For more practical advice on managing your finances, check out our guide on .

Conclusion: Drive Forward with Confidence

Securing a car loan with good credit and a lower income is not just possible; it’s an opportunity to demonstrate your financial savvy and discipline. By understanding how lenders assess risk, strategically budgeting, choosing the right vehicle, and diligently managing the application process, you can unlock favorable loan terms that make car ownership affordable and sustainable.

Your good credit score is a testament to your financial responsibility. Leverage it wisely, combine it with meticulous planning, and you’ll not only drive away in a reliable vehicle but also reinforce your foundation for a secure financial future. Drive forward with confidence, knowing you’ve made a smart, informed decision.