Driving Your Dreams: Securing a Car Loan with a 690 Credit Score

Driving Your Dreams: Securing a Car Loan with a 690 Credit Score Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is exciting, and understanding your financial standing is the first crucial step. If you’re wondering about your prospects for a car loan with a 690 credit score, you’ve landed in the right place. This comprehensive guide will illuminate every facet of securing auto financing with this specific credit score, offering insights, strategies, and expert advice to ensure you drive away with the best possible deal.

A 690 credit score places you in an interesting position – it’s often considered "Good" or at the higher end of "Fair," depending on the credit scoring model. This means you’re generally seen as a responsible borrower, but there might still be room to optimize your loan terms. Our goal today is to equip you with the knowledge to confidently approach lenders, understand what to expect, and maximize your chances of approval for an attractive car loan.

Driving Your Dreams: Securing a Car Loan with a 690 Credit Score

Understanding Your 690 Credit Score: What It Means for Car Loans

Your credit score is a three-digit number that acts as a financial report card, indicating your creditworthiness to lenders. It’s derived from your credit history, including how consistently you pay bills, the amount of debt you carry, and the length of your credit history. For car loans, lenders use this score to gauge the risk associated with lending you money.

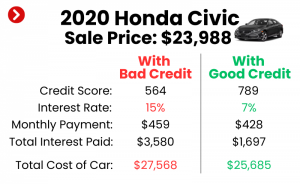

A 690 credit score typically falls within the "Good" range for many scoring models like FICO and VantageScore. This is a positive indicator. While it might not unlock the absolute lowest interest rates reserved for those with scores in the 780+ "Excellent" range, it certainly opens doors to competitive offers from a wide array of lenders. You’re generally past the stage where securing any loan is difficult, and now your focus shifts to securing a good loan.

This score suggests that you have a history of managing credit responsibly, making timely payments, and maintaining a reasonable debt load. Lenders view this favorably, often translating into more flexible terms and lower interest rates compared to individuals with lower scores. However, it’s essential to understand that your credit score is just one piece of the puzzle.

Beyond the Score: Other Factors Lenders Evaluate

While your 690 credit score is a strong foundation, lenders look at a holistic financial picture. Based on my experience in auto finance, focusing solely on your credit score can lead to missed opportunities. Here are other critical elements that influence a lender’s decision and the terms they offer:

Your Debt-to-Income (DTI) Ratio

Your DTI ratio is a crucial metric that compares your total monthly debt payments to your gross monthly income. Lenders want to see that you have enough disposable income to comfortably afford your new car payment in addition to your existing financial obligations. A lower DTI ratio indicates less financial strain and a greater ability to handle new debt.

For instance, if your total monthly debt (mortgage, student loans, credit card minimums) is $1,500 and your gross monthly income is $4,500, your DTI is 33%. Lenders generally prefer a DTI below 43%, though lower is always better. This ratio tells them whether adding a new car payment will stretch your finances too thin.

Employment History and Stability

Lenders seek stability. A consistent employment history, ideally with the same employer for several years, reassures them of a steady income stream. Frequent job changes or gaps in employment might raise questions about your ability to maintain consistent payments. They want to see that your income is reliable and likely to continue throughout the loan term.

The Down Payment Amount

Making a substantial down payment significantly reduces the risk for lenders. When you put more money down upfront, you finance less, which means lower monthly payments and less interest paid over the life of the loan. A larger down payment also shows your commitment and financial discipline, making you a more attractive borrower.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment. This not only improves your loan terms but also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early on.

The Vehicle Itself: Age and Type

The type and age of the car you wish to purchase also play a role. Lenders are more comfortable financing newer, more reliable vehicles because they hold their value better and are less likely to require expensive repairs that could impact your ability to pay. Older or high-mileage vehicles are considered higher risk due to potential mechanical issues and faster depreciation.

Considering a Co-signer

If you’re looking to secure even better terms or if there are any minor blemishes in your financial profile despite your 690 score, a co-signer with excellent credit can be a game-changer. A co-signer shares the responsibility for the loan, providing an additional layer of security for the lender. This can often lead to lower interest rates and more favorable terms.

Preparing for Your Car Loan Application: A Strategic Approach

Before you even step foot in a dealership or apply online, thorough preparation is key. This strategic approach will not only boost your approval chances but also empower you to negotiate for the best possible deal.

1. Check Your Credit Report and Dispute Errors

Your credit score is derived from your credit report. It’s crucial to obtain a free copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) at AnnualCreditReport.com. Review them meticulously for any inaccuracies or outdated information. Errors, even small ones, can negatively impact your score.

If you find errors, dispute them immediately with the credit bureau and the creditor involved. Resolving these issues can potentially boost your score further, giving you an even stronger position for your car loan. This proactive step is often overlooked but can yield significant benefits.

2. Determine Your Budget and Affordability

Don’t just think about the monthly payment; consider the total cost of ownership. This includes insurance, fuel, maintenance, and potential repair costs, in addition to the loan payment. Use online calculators to estimate what you can truly afford without stretching your budget thin. A common mistake to avoid is focusing solely on the monthly payment without considering the overall impact on your financial health.

Based on my experience, many people get caught up in the excitement of a new car and forget to factor in these ancillary costs. Ensure your budget allows for comfortable payments and other car-related expenses.

3. Get Pre-Approved Before Shopping

One of the most powerful strategies is to get pre-approved for a car loan before you visit a dealership. Pre-approval involves a lender reviewing your credit and income information and offering you a loan amount and interest rate. This gives you a clear understanding of what you can afford and arms you with a strong negotiating tool.

With a pre-approval in hand, you walk into the dealership as a cash buyer, not just a loan applicant. This shifts the focus from your financing to the vehicle’s price, giving you significant leverage. You’ll know exactly what interest rate you qualify for, allowing you to compare it with any offers the dealership might present.

4. Gather Necessary Documents

Having your documents ready streamlines the application process. Typically, you’ll need:

- Proof of identity (driver’s license, passport)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of insurance (you’ll need to secure this before driving off the lot)

- Trade-in title, if applicable

Having these readily available makes the application process smoother and faster, projecting an image of preparedness and responsibility.

5. Understand Interest Rates and Loan Terms

Interest rates are the cost of borrowing money. With a 690 credit score, you should qualify for competitive rates, but they won’t be the absolute lowest. Loan terms refer to the length of the loan (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but more interest paid over time. Shorter terms mean higher monthly payments but less interest.

Pro tips from us: While a longer term might make a car more "affordable" on a monthly basis, always calculate the total interest paid. Often, a slightly higher monthly payment for a shorter term saves you hundreds or even thousands of dollars in interest over the life of the loan.

Navigating the Car Loan Process with a 690 Score

Now that you’re prepared, it’s time to engage with lenders and dealerships. Your 690 credit score puts you in a good position, but smart navigation is crucial.

Shop Around for Lenders

Do not settle for the first offer you receive. Different lenders have different criteria and offer varying rates. Explore options from:

- Banks: Your existing bank or credit union might offer preferential rates.

- Credit Unions: Often known for offering highly competitive rates to their members.

- Online Lenders: Many reputable online platforms specialize in auto loans and can provide quick quotes.

- Dealership Financing: While convenient, dealership financing sometimes marks up interest rates. Use your pre-approval to compare and negotiate.

Submitting multiple loan applications within a short window (typically 14-45 days, depending on the scoring model) will usually be counted as a single hard inquiry on your credit report, so don’t be afraid to rate shop. This allows you to compare offers without significantly impacting your score.

Negotiate the Best Terms

With your pre-approval in hand, you have the power to negotiate. If a dealership offers you financing, compare their APR (Annual Percentage Rate) to your pre-approved rate. If their offer is higher, you can use your pre-approval as leverage to ask them to beat or match it. Remember, everything is negotiable – the car price, the trade-in value, and the loan terms.

Based on my experience, many consumers leave money on the table because they don’t negotiate effectively. Be confident, informed, and ready to walk away if the terms aren’t favorable.

Read the Fine Print

Before signing any documents, read the entire contract thoroughly. Pay close attention to:

- The APR: This is the true cost of the loan, including interest and fees.

- The total loan amount.

- The monthly payment amount.

- The loan term.

- Any additional fees or charges.

- Prepayment penalties (though less common in auto loans, it’s good to check).

If anything is unclear, ask for clarification. Do not sign anything you don’t fully understand.

Maximizing Your Approval Chances and Getting Better Rates

Even with a 690 credit score, there are additional steps you can take to strengthen your application and potentially secure even better loan terms.

Increase Your Down Payment

We’ve mentioned this before, but it bears repeating. A larger down payment not only reduces your loan amount but also signals to lenders that you are less of a risk. It also lowers your monthly payments and the total interest you’ll pay over time. If you can save up an extra few hundred or thousand dollars, it’s often worth the wait.

Consider a Co-signer (If Applicable)

If you have a trusted family member or friend with an excellent credit score, asking them to co-sign could significantly lower your interest rate. Remember, a co-signer is equally responsible for the loan, so both parties must understand the implications. This is a big commitment for them, so approach this option with careful consideration.

Improve Your Debt-to-Income Ratio

Before applying, look for ways to reduce your existing monthly debt payments. Paying off a small credit card balance or a personal loan can positively impact your DTI ratio, making you look more financially sound to lenders. Even a slight reduction can make a difference.

Focus on Debt Reduction

While a 690 score is good, reducing your overall debt before applying can free up more of your income. This improves your DTI and potentially your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit. A lower utilization ratio (ideally below 30%) is always favorable.

Common Mistakes to Avoid When Getting a Car Loan

Even with a good credit score, missteps during the car loan process can cost you time and money. Here are common mistakes we frequently see applicants make:

- Applying Everywhere: While rate shopping is good, applying for multiple loans indiscriminately can lead to numerous hard inquiries, which can temporarily ding your credit score. Be strategic in your applications.

- Ignoring the APR: Focusing solely on the monthly payment can be misleading. Always look at the Annual Percentage Rate (APR), which includes all interest and fees, to understand the true cost of borrowing. A lower monthly payment over a longer term often means a higher total cost due to more interest paid.

- Not Reading the Contract Thoroughly: As mentioned, rushing through the paperwork is a recipe for regret. Ensure you understand every clause and condition before signing.

- Buying More Car Than You Can Afford: It’s easy to get swept away by the allure of a luxury vehicle. Stick to your budget and prioritize affordability over aspiration to avoid financial strain down the road.

- Not Factoring in Additional Costs: Remember insurance, maintenance, fuel, and registration. These can significantly add to your monthly vehicle expenses.

- Accepting Dealership Add-ons Without Question: Dealerships often offer extended warranties, GAP insurance, and other add-ons. While some can be beneficial, always research their value and negotiate their price. You’re not obligated to accept them.

690 Credit Score Car Loan: What to Expect for Interest Rates

With a 690 credit score, you are likely to receive interest rates that are quite competitive, typically falling into the "good" to "average" tier. While the absolute best rates (often below 3-4% for new cars) are reserved for those with scores above 740-760, you can still expect rates that are significantly better than what someone with a fair or poor score would receive.

- For New Cars: You might see rates in the range of 5% to 8%, depending on the current market, the lender, the loan term, and your other financial factors.

- For Used Cars: Rates for used cars are generally slightly higher than new cars due to the perceived higher risk. You might expect rates from 6% to 10% with a 690 score.

These figures are estimates and can fluctuate based on economic conditions and individual lender policies. The key is to shop around and compare offers to ensure you’re getting the best possible rate available to you. Don’t forget that a larger down payment and a shorter loan term can also help reduce the overall interest you pay.

Improving Your Credit Score For Future Loans (or Even Better Rates Now)

Even with a 690 score, continuous credit improvement is a smart financial habit. A higher score means access to even better rates on future loans and credit products.

- Pay Your Bills On Time, Every Time: Payment history is the most significant factor in your credit score. Set up automatic payments to avoid missing due dates.

- Keep Your Credit Utilization Low: Aim to use no more than 30% of your available credit on credit cards. Lower is always better.

- Don’t Close Old Accounts: The length of your credit history positively impacts your score. Keep older accounts open, even if you don’t use them frequently.

- Limit New Credit Applications: Each new application results in a hard inquiry, which can temporarily lower your score. Only apply for credit when genuinely needed.

- Monitor Your Credit Regularly: Keep an eye on your credit report for any unauthorized activity or errors.

Conclusion: Driving Forward with Confidence

A 690 credit score is a solid foundation for securing a car loan. It positions you as a responsible borrower and opens the door to competitive interest rates and favorable terms. By understanding the factors lenders consider, preparing diligently, shopping wisely, and negotiating effectively, you can confidently navigate the auto financing landscape.

Remember, the goal isn’t just to get approved, but to secure a loan that genuinely aligns with your financial goals and capabilities. With the insights provided in this comprehensive guide, you are well-equipped to drive away in your desired vehicle, knowing you’ve made a smart financial decision. Happy driving!

Internal Link Suggestion:

- Link to an article about "Understanding Your Debt-to-Income Ratio"

- Link to an article about "Tips for Improving Your Credit Score Quickly"

External Link Suggestion: