Driving Your Dreams: Securing a New Car Loan with a 600 Credit Score

Driving Your Dreams: Securing a New Car Loan with a 600 Credit Score Carloan.Guidemechanic.com

For many, the dream of driving a brand-new car feels out of reach when their credit score hovers around the 600 mark. It’s a common misconception that a credit score in the "fair" or "subprime" range automatically slams the door shut on new car ownership. While it presents unique challenges, securing a new car loan with a 600 credit score is absolutely possible with the right approach and a clear understanding of the lending landscape.

As an expert blogger and SEO content writer, I’ve delved deep into the intricacies of auto financing, especially for those navigating the waters with less-than-perfect credit. This comprehensive guide is designed to empower you, offering a roadmap to understanding, preparing for, and ultimately securing the car loan you need. We’ll explore everything from lender expectations to practical strategies for improving your chances of approval, ensuring you get the best possible terms.

Driving Your Dreams: Securing a New Car Loan with a 600 Credit Score

Let’s buckle up and drive into the details, transforming that dream into a tangible reality.

Understanding Your 600 Credit Score in the Auto Loan World

A 600 credit score typically falls into the "fair" or "subprime" category. This means lenders perceive you as a higher risk compared to someone with excellent credit. However, it’s crucial to understand that "higher risk" doesn’t equate to "no chance." It simply means the terms of your loan might differ.

Lenders use credit scores to assess the likelihood of you repaying your debt. A 600 score suggests you may have had some past credit challenges, such as late payments or a high credit utilization ratio. This history makes lenders more cautious, but it doesn’t make them unwilling to lend.

The Realities of Interest Rates and Terms

One of the most significant differences you’ll encounter with a 600 credit score is the interest rate. Because you represent a higher risk, lenders will typically charge a higher interest rate to compensate for that risk. This means you’ll pay more over the life of the loan than someone with a prime credit score.

Based on my experience, many people with a 600 score are surprised by the initial interest rate offers. It’s important to manage these expectations and understand that a higher rate is a common reality in this credit tier. Your goal should be to secure an affordable loan, even if the rate isn’t ideal, with a plan to potentially refinance later.

Why Lenders Are Hesitant, But Not Entirely Closed Off

While lenders are cautious, they are also in the business of lending money. The auto loan market is vast, and there are many lenders who specialize in financing a car with low credit. They understand that life happens, and a 600 score isn’t necessarily a reflection of your current financial stability or your desire to repay a loan.

What they look for are mitigating factors. These can include a stable job history, a decent income, a low debt-to-income ratio (DTI), and the ability to make a substantial down payment. These elements can offset the perceived risk associated with your credit score, making you a more attractive borrower.

Preparing for Your Car Loan Application: Laying the Groundwork

Preparation is key when seeking a new car loan with a 600 credit score. By taking proactive steps, you can significantly improve your chances of approval and potentially secure more favorable terms. Don’t rush into the application process without doing your homework.

Checking Your Credit Report: The First Crucial Step

Before approaching any lender, pull your credit reports from all three major bureaus: Experian, Equifax, and TransUnion. You can do this for free annually at AnnualCreditReport.com. This step is non-negotiable.

Review each report meticulously for any errors or inaccuracies. Common mistakes include accounts that aren’t yours, incorrect payment statuses, or outdated information. Disputing and correcting these errors can potentially boost your credit score, even if by a few points, which can make a difference in lending decisions.

Budgeting Realistically: Knowing Your Limits

Pro tips from us: Don’t just look at the score; look at your overall financial picture. Before you even think about specific cars, create a realistic budget. This involves more than just the monthly loan payment. Consider the total cost of car ownership, including insurance, fuel, maintenance, and potential repair costs.

A common mistake to avoid is focusing solely on the monthly payment. A longer loan term might make payments seem more affordable, but it drastically increases the total interest paid over time. Aim for a payment that comfortably fits within your budget, leaving room for other expenses and savings.

Saving for a Down Payment: Your Secret Weapon

One of the most impactful things you can do to improve your chances of securing a new car loan with a 600 credit score is to make a significant down payment. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk.

Lenders view a substantial down payment as a sign of your commitment and financial responsibility. It shows you have skin in the game. Aim for at least 10-20% of the car’s purchase price, if possible. Even 5% can make a difference, but more is always better when dealing with subprime credit.

Gathering Essential Documentation

Lenders will want to verify your income, employment, and residency. Having all your documents ready before you apply will streamline the process and present you as an organized, serious borrower.

Typically, you’ll need:

- Proof of income (pay stubs, tax returns)

- Proof of residency (utility bills, lease agreement)

- Government-issued ID

- Social Security number

- Proof of insurance (you’ll need this before driving off the lot)

Having these readily available demonstrates your preparedness and can expedite the approval process.

Strategies for Securing a New Car Loan with a 600 Credit Score

Now that you’re prepared, it’s time to explore the specific strategies that will help you get approved for a new car loan with a 600 credit score. The key is to know where to look and how to present yourself as a reliable borrower.

Explore Different Lender Types

Don’t limit yourself to just one type of lender. Different institutions have varying risk appetites and lending criteria.

- Traditional Banks: While they often offer the best rates, they can be stricter with credit score requirements. It’s worth trying, especially if you have an existing relationship, but don’t be discouraged if denied.

- Credit Unions: Often more community-focused and flexible than traditional banks. They may be more willing to work with members who have a 600 credit score, especially if you have a history with them. Their rates can also be very competitive.

- Dealership Financing (Captive Lenders): Many dealerships work with a network of lenders, including those specializing in subprime auto loan financing. They can often get you approved on the spot, but be wary of higher interest rates.

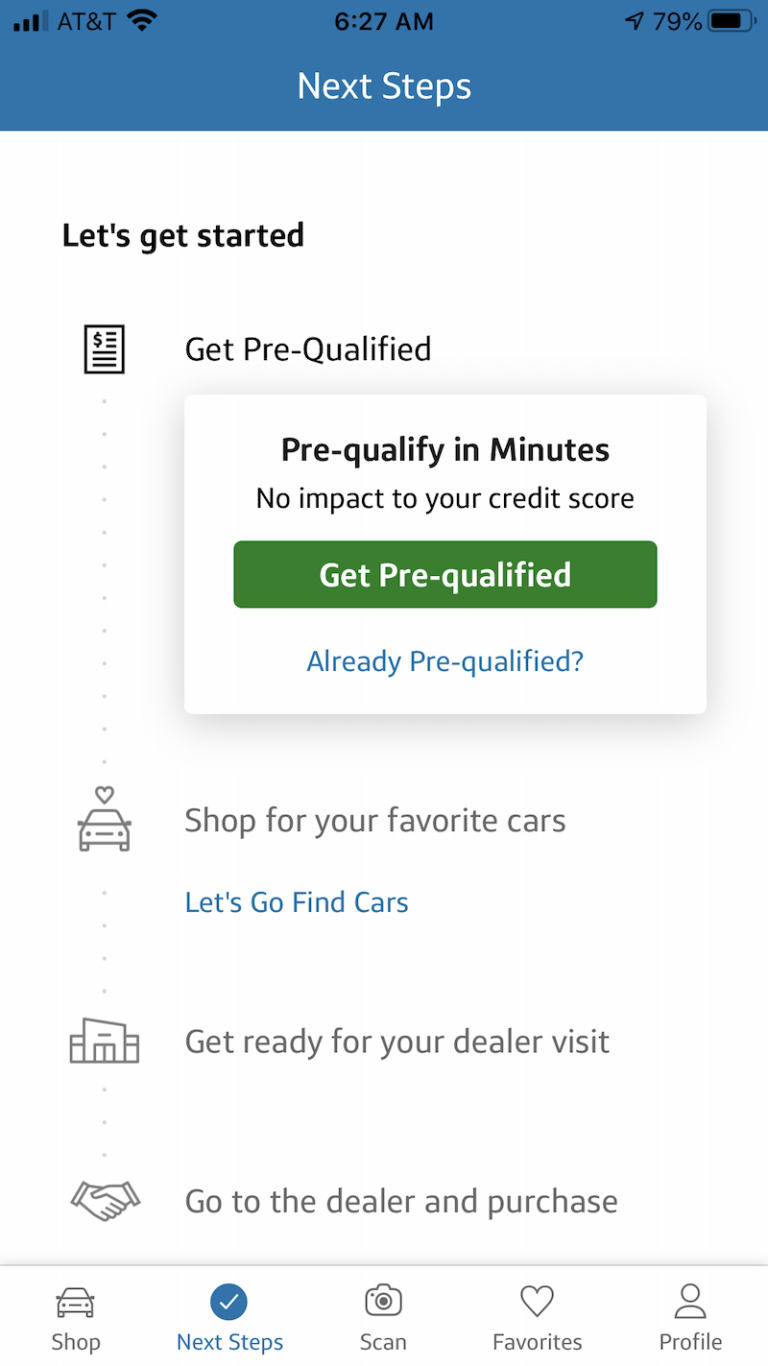

- Online Lenders Specializing in Bad Credit: Several online platforms specifically cater to individuals with lower credit scores. They can offer pre-qualification with a soft credit pull, allowing you to compare offers without impacting your score. Examples include Capital One Auto Finance, MyAutoLoan, and LightStream (though LightStream usually requires higher scores).

Common mistakes to avoid are applying to too many lenders at once, which can result in multiple hard inquiries and further depress your score. Use pre-qualification services where available.

Consider a Co-signer: A Powerful Ally

If you’re struggling to get approved or offered extremely high interest rates, a co-signer can be a game-changer. A co-signer is someone with good credit who agrees to take on the responsibility of the loan if you default.

Having a co-signer significantly reduces the lender’s risk, as they have a second, more creditworthy individual to pursue if payments are missed. This can lead to approval and potentially a much lower interest rate. However, understand the implications: the co-signer is equally responsible for the debt, and their credit will be affected if you miss payments. Choose someone you trust implicitly, and ensure they understand the commitment.

Focus on Affordability, Not Just Approval

While getting approved is the immediate goal, the long-term goal is to afford the loan comfortably. Don’t let the excitement of approval lead you into an unsustainable financial commitment. It’s better to walk away from a deal that stretches your budget too thin.

Pro tips from us: Look beyond the monthly payment. Calculate the total cost of the loan, including interest, over its entire term. A shorter loan term, even with slightly higher monthly payments, can save you thousands in interest.

Negotiating Terms: Don’t Be Afraid to Ask

Even with a 600 credit score, there’s often room for negotiation, especially on the interest rate. Once you have an approval, or even a pre-approval, don’t be afraid to compare offers and ask lenders if they can beat a competitor’s rate.

Remember, the dealership wants to sell you a car, and lenders want to lend money. If you present yourself as a prepared and informed buyer, you have more leverage than you might think. Focus on getting a fair interest rate, a manageable loan term, and avoiding unnecessary add-ons that inflate the total price.

The Application Process: What to Expect When Seeking a New Car Loan with a 600 Credit Score

Navigating the application process for a new car loan with a 600 credit score requires patience and a clear understanding of what lenders are looking for. It’s a bit different than applying with an excellent score, but it’s not insurmountable.

Pre-qualification vs. Full Application

Many lenders offer pre-qualification, which is a soft credit pull that doesn’t affect your score. This is an excellent way to gauge your eligibility and get an idea of potential interest rates without committing.

A full application, however, involves a hard credit inquiry, which can temporarily ding your score by a few points. It’s wise to use pre-qualification to narrow down your options before proceeding with full applications to a select few lenders. This minimizes the impact on your credit score while still allowing you to compare concrete offers.

Impact of Multiple Inquiries

While multiple hard inquiries can lower your score, credit scoring models typically group auto loan inquiries made within a short period (usually 14-45 days) as a single inquiry. This is because they understand you’re shopping for the best rate.

So, if you apply to a few different auto lenders within a two-week window, it will likely count as one inquiry for scoring purposes. This gives you the flexibility to compare offers without undue penalty. Just don’t drag out the shopping process over several months.

What Lenders Look for Beyond the Score

While your 600 credit score is a major factor, it’s not the only one. Lenders specializing in bad credit car loan scenarios look at a holistic picture:

- Debt-to-Income (DTI) Ratio: This measures how much of your gross monthly income goes towards debt payments. A lower DTI indicates you have more disposable income to cover new loan payments.

- Employment History: A stable job history (e.g., two years or more with the same employer) signals reliability and a consistent income stream.

- Income Stability: Lenders want to see that you have a reliable source of income that can comfortably cover the monthly car payments, even if unexpected expenses arise.

- Current Savings/Assets: Demonstrating financial responsibility through savings or other assets can reassure lenders.

Be prepared to provide documentation for all these factors, as they are crucial in helping lenders make an informed decision beyond just your credit score.

Be Prepared for Higher Interest Rates

As reiterated earlier, a new car loan with a 600 credit score almost universally comes with a higher interest rate than loans for prime borrowers. Don’t be surprised if you’re offered rates in the double digits.

The most important thing is to ensure the monthly payment is affordable and sustainable for your budget. If the initial rates seem too high, consider a slightly used car, which will have a lower overall price, thus reducing the loan amount and potentially the total interest paid. Focus on getting a reliable vehicle that serves your needs, rather than chasing the lowest possible rate at the expense of financial stability.

Improving Your Financial Position for Better Loan Terms (Even After Approval)

Getting approved for a new car loan with a 600 credit score is a significant achievement, but the journey doesn’t end there. This loan can serve as a powerful tool to rebuild your credit and unlock better financial opportunities in the future.

Making Timely Payments: The Cornerstone of Credit Repair

The absolute best thing you can do for your credit score is to make every single car loan payment on time, every time. Payment history is the most heavily weighted factor in credit scoring models (accounting for 35% of your FICO score).

Consistent, on-time payments will gradually demonstrate your reliability to credit bureaus and lenders. This positive payment history will slowly but surely start to nudge your 600 credit score upwards. Set up auto-pay or calendar reminders to ensure you never miss a due date.

Reducing Other Debt: Lowering Your DTI

Beyond your car loan, actively work to reduce other outstanding debts, especially high-interest credit card balances. This not only frees up more of your income but also improves your debt-to-income (DTI) ratio and credit utilization ratio.

A lower DTI makes you a more attractive borrower for future credit opportunities. As you pay down other debts, your credit score will likely see further improvement, paving the way for better terms on other loans or credit cards down the line.

Refinancing Options: When and Why

Once you’ve made 6-12 months of consistent, on-time payments on your new car loan, and if your credit score has shown improvement, you might be a candidate for refinancing. Refinancing involves taking out a new loan to pay off your current car loan, ideally at a lower interest rate.

This can significantly reduce your monthly payments or the total interest paid over the life of the loan. Many lenders specialize in refinancing bad credit car loans once a borrower has established a track record of responsible payments. It’s a smart strategy to save money and continue building your credit. For more details on this, you might find our article on "How to Improve Your Credit Score Quickly" insightful.

Making the Right Car Choice: A Strategic Decision

When your goal is a new car loan with a 600 credit score, your choice of vehicle plays a critical role. It’s not just about what you like, but what makes financial sense and increases your chances of approval.

New vs. Used: The Financial Implications

While the article focuses on new car loans, it’s worth considering the new vs. used debate. Sometimes, securing a new car loan can be easier than a used one for subprime borrowers. New cars often have manufacturer incentives and can be easier for lenders to value.

However, a new car depreciates rapidly, and the total cost will be higher. A reliable, slightly used car often offers better value. If a new car is your definite preference, opt for a more affordable model that doesn’t push the boundaries of your budget.

Consider a Reliable, Affordable Model

Avoid going for luxury vehicles or models with excessive features when you have a 600 credit score. Lenders prefer to finance reliable, moderately priced vehicles. These cars hold their value better and are generally less risky from a lender’s perspective.

Focus on cars known for their longevity, fuel efficiency, and lower insurance costs. This prudent choice not only aids in loan approval but also contributes to your long-term financial health. For tips on smart car buying, check out our guide on "Choosing the Right First Car Loan".

Avoiding Unnecessary Add-ons

Dealerships often push extended warranties, paint protection, and other add-ons. While some might offer value, many are overpriced and simply inflate the total loan amount. When you have a 600 credit score, every dollar added to the loan means more interest paid.

Be firm in declining anything you don’t genuinely need or that isn’t included in the manufacturer’s warranty. Your priority should be securing the vehicle itself at the most favorable terms, not loading up on extras.

Conclusion: Your Path to a New Car Loan with a 600 Credit Score

Securing a new car loan with a 600 credit score is a journey that requires careful planning, smart strategies, and a good understanding of the lending process. It’s a testament to your determination and a significant step towards both new car ownership and improving your financial standing. While the path might have its challenges, it is undoubtedly achievable.

Remember, your 600 credit score is not a life sentence. It’s a starting point. By thoroughly checking your credit report, budgeting realistically, saving for a down payment, and exploring various lending options, you significantly enhance your prospects. Don’t shy away from considering a co-signer or exploring reputable online lenders who specialize in financing a car with low credit.

Once approved, commit to making every payment on time. This single action is your most powerful tool for rebuilding your credit, opening doors to better financial opportunities, including the possibility of refinancing at a lower rate down the line. The dream of a new car is within reach, and with the right approach, you can drive off the lot with confidence, knowing you’ve made a smart financial decision.