Driving Your Dreams: The Ultimate Expert Guide to Navigating Car Loans with Confidence

Driving Your Dreams: The Ultimate Expert Guide to Navigating Car Loans with Confidence Carloan.Guidemechanic.com

The exhilarating feeling of getting behind the wheel of a new car is a universal dream for many. Whether it’s a sleek sedan, a rugged SUV, or a practical family vehicle, the prospect of owning your ideal ride is incredibly exciting. However, for most of us, this dream often involves securing a car loan.

Navigating the world of vehicle financing can seem daunting, filled with jargon and complex terms. But it doesn’t have to be. Understanding the intricacies of car loans is not just about getting approval; it’s about securing the right loan that aligns with your financial health and future goals.

Driving Your Dreams: The Ultimate Expert Guide to Navigating Car Loans with Confidence

This comprehensive guide, crafted by an expert in auto financing, will demystify the entire car loan process. We’ll equip you with the knowledge and confidence to make informed decisions, avoid common pitfalls, and ultimately drive away with a deal that makes financial sense. Prepare to become an expert yourself!

1. Understanding the Foundation: What Exactly is a Car Loan?

At its core, a car loan is a secured loan specifically designed to finance the purchase of a vehicle. When you take out an auto loan, a lender (such as a bank, credit union, or dealership finance company) provides you with the funds to buy the car. In return, you agree to repay this amount, known as the principal, plus an additional cost called interest, over a predetermined period, or term.

The vehicle itself acts as collateral for the loan. This means that if you fail to make your payments as agreed, the lender has the legal right to repossess the car to recover their losses. This collateralized nature is what makes car loans a common and accessible form of credit for vehicle purchases.

Understanding these fundamental components – principal, interest, and term – is crucial. They are the building blocks of every car loan agreement and directly impact your monthly payments and the total cost of ownership. Without a clear grasp of these basics, it’s easy to get lost in the details of loan offers.

2. The Different Paths: Types of Car Loans

Not all car loans are created equal. Depending on the type of vehicle you’re buying, your financial situation, and where you source your financing, different options will be available. Knowing these distinctions is the first step toward finding the perfect fit.

New Car Loans

These loans are for brand-new vehicles straight from the dealership. Typically, new car loans come with lower interest rates and longer repayment terms compared to used car loans. This is because new cars tend to hold their value better initially and are considered less risky by lenders.

Used Car Loans

When you opt for a pre-owned vehicle, you’ll be looking at a used car loan. These often have slightly higher interest rates and shorter terms than new car loans. Lenders perceive used cars as having a higher risk due to potential mechanical issues and faster depreciation, especially for older models.

Refinancing Car Loans

Refinancing involves taking out a new loan to pay off your existing car loan. People often do this to secure a lower interest rate, reduce their monthly payments, or change their loan term. It’s a strategic move that can save you a significant amount over the life of your loan.

- Pro tip from us: Refinancing is a smart move if interest rates have dropped since you took out your original loan, your credit score has significantly improved, or you need to lower your monthly payments due to a change in your financial situation. Always compare your current loan with potential refinancing offers.

Private Party Car Loans

Buying a car from a private seller, rather than a dealership, requires a specific type of financing. Some lenders offer private party auto loans, which can sometimes have stricter requirements or slightly different terms than loans for dealership purchases. This is because the lender cannot easily verify the vehicle’s condition or history from a private seller.

Bad Credit Car Loans

For individuals with a low credit score, securing a traditional car loan can be challenging. Bad credit car loans are designed for these situations, though they typically come with much higher interest rates and less favorable terms. While they offer a path to vehicle ownership, they should be approached with caution and a clear plan for improving credit.

Leasing vs. Buying (Brief Overview)

While not a loan in the traditional sense, leasing is a common alternative to buying a car with a loan. When you lease, you essentially rent the car for a set period, making monthly payments without owning the vehicle. At the end of the lease, you can return the car, buy it, or lease a new one. This option suits those who prefer lower monthly payments and enjoy driving new cars frequently.

3. The Crucial Pre-Application Steps: Paving Your Way to Approval

Securing the best possible car loan doesn’t start at the dealership; it begins with thorough preparation. These pre-application steps are vital for empowering you as a buyer and ensuring you get a fair deal.

Check Your Credit Score & Report

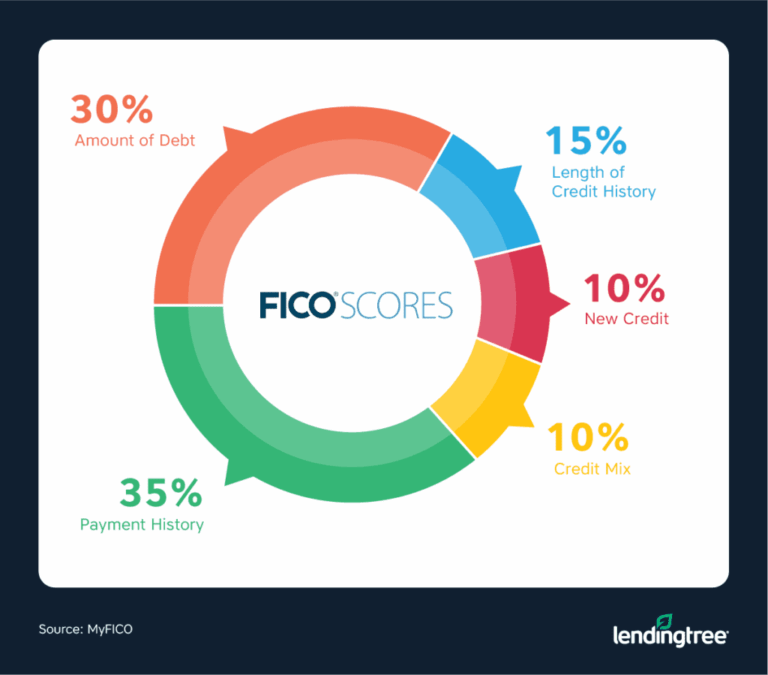

Your credit score is arguably the most influential factor in your car loan journey. It’s a three-digit number that lenders use to assess your creditworthiness and determine your interest rate. A higher score generally translates to lower interest rates, saving you thousands over the loan term.

It’s crucial to obtain your credit report from all three major bureaus (Equifax, Experian, TransUnion) and review them carefully. You can get free annual reports through AnnualCreditReport.com. Look for any errors or discrepancies that could be negatively impacting your score. Correcting these can significantly boost your standing.

- Based on my experience: Many people skip this step, only to be surprised by a high interest rate. Even small improvements to your credit score before applying can translate into substantial savings on interest payments over the life of the loan. Don’t underestimate its power.

Determine Your Budget

Before you even start looking at cars, establish a clear budget. This goes beyond just the monthly loan payment. Remember to factor in:

- Insurance costs: Premiums can vary significantly based on the car model, your driving history, and location.

- Fuel expenses: Consider the car’s fuel efficiency and your typical driving habits.

- Maintenance and repairs: All cars require upkeep; newer cars might have warranty coverage, but older ones can incur higher costs.

- Registration and taxes: These upfront costs are often overlooked.

A larger down payment can significantly reduce the amount you need to borrow, thus lowering your monthly payments and the total interest paid. Aim for at least 10-20% of the car’s purchase price if possible. This also shows lenders you’re a serious and responsible borrower, potentially leading to better terms.

Get Pre-Approved

One of the most powerful tools in your car-buying arsenal is a pre-approval letter. This means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate. Pre-approval offers several key benefits:

- Shopping power: You know exactly how much you can afford, preventing you from falling in love with a car outside your budget.

- Negotiating leverage: You walk into the dealership with your own financing in hand, putting you in a stronger position to negotiate the car’s price.

- Comparison shopping: It allows you to compare the pre-approved offer with any financing options the dealership might present.

When you seek pre-approval, lenders typically perform a "soft inquiry" on your credit, which doesn’t harm your score. Once you formally apply for a loan, a "hard inquiry" occurs. It’s wise to get all your loan applications submitted within a short window (e.g., 14-45 days) so they count as a single inquiry for scoring purposes.

Research Vehicle Value

Knowledge is power, especially when it comes to car prices. Before you step onto a lot, research the fair market value of the specific make and model you’re interested in. Resources like Kelley Blue Book (KBB.com), Edmunds, and NADAguides provide excellent valuation tools for both new and used vehicles.

Knowing the vehicle’s true worth prevents you from overpaying and gives you a strong basis for price negotiation. This research should be done independently of your loan application process.

4. Navigating the Application Process: Step-by-Step

Once your groundwork is laid, the actual application process for a car loan becomes much smoother. Being organized and informed will make all the difference.

Gather Necessary Documents

Before applying, ensure you have all the required paperwork ready. Lenders will typically ask for:

-

Proof of identity: Driver’s license or state ID.

-

Proof of income: Recent pay stubs, W-2 forms, or tax returns if self-employed.

-

Proof of residence: Utility bill or lease agreement.

-

Social Security number.

-

Vehicle information: If you’ve already chosen a specific car.

-

Common mistakes to avoid are: Showing up to apply without all your documents. This can delay the process and create frustration. Double-check the lender’s requirements beforehand.

Choose Your Lender Wisely

You have several avenues for securing a car loan:

-

Banks and Credit Unions: Often offer competitive rates and personalized service. Credit unions, in particular, are known for their favorable terms to members.

-

Online Lenders: Provide convenience and quick approvals, often with competitive rates.

-

Dealership Financing: Dealers work with multiple lenders and can offer convenience, but their initial offers might not always be the best.

-

Pro tips from us: Don’t settle for the first offer you receive. Apply with at least 2-3 different lenders (including your bank/credit union) to compare rates and terms. This competitive shopping can yield significant savings.

Complete the Application

Once you’ve chosen your preferred lender(s), fill out the application accurately and honestly. Provide all requested information, ensuring there are no discrepancies. Any misrepresentations can lead to delays or even loan denial.

Understand the Loan Offer

When you receive a loan offer, it’s critical to review every detail before signing. Pay close attention to:

-

Annual Percentage Rate (APR): This is the true cost of borrowing, encompassing the interest rate and any fees. It’s the most important number to compare between offers.

-

Loan Term: The length of the repayment period (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but more interest paid overall.

-

Total Loan Cost: Calculate the total amount you’ll pay back (principal + interest).

-

Any Fees: Look for origination fees, prepayment penalties, or other hidden charges.

-

Based on my experience: Many buyers get fixated on the monthly payment alone. While important for budgeting, always prioritize the APR and the total cost of the loan. A slightly higher monthly payment over a shorter term can save you thousands in interest.

5. Factors That Drive Your Car Loan Approval & Interest Rates

Several key elements come into play when lenders assess your loan application. Understanding these factors will help you improve your chances of approval and secure the most favorable interest rate.

Credit Score

As discussed, your credit score is paramount. Lenders use it as a primary indicator of your ability and willingness to repay debt. Generally, scores above 700 are considered excellent and qualify for the best rates, while scores below 600 will likely face higher rates or require a specialized bad credit car loan.

Debt-to-Income Ratio (DTI)

Your DTI ratio compares your total monthly debt payments (including your prospective car loan payment) to your gross monthly income. Lenders prefer a lower DTI, typically below 40%, as it indicates you have enough disposable income to comfortably manage new debt. A high DTI signals that you might be overextended financially.

Loan-to-Value Ratio (LTV)

The LTV ratio compares the amount you’re borrowing to the car’s actual value. For example, if a car is worth $20,000 and you borrow $18,000, your LTV is 90%. A lower LTV (meaning you’re borrowing less relative to the car’s value, often due to a larger down payment) reduces the lender’s risk.

Down Payment

A substantial down payment reduces the principal amount you need to borrow, which directly lowers your monthly payments and total interest paid. It also decreases the lender’s risk, making you a more attractive borrower. Lenders view a significant down payment as a sign of financial commitment and stability.

Loan Term

The length of your loan term directly impacts your monthly payments and the total interest you’ll pay. Shorter terms (e.g., 36 or 48 months) usually come with lower interest rates but higher monthly payments. Longer terms (e.g., 72 or 84 months) offer lower monthly payments but accrue more interest over time, making the car more expensive overall.

Vehicle Age & Mileage

For used car loans, the age and mileage of the vehicle are significant factors. Lenders often have stricter requirements for older, higher-mileage vehicles due to their perceived higher risk of mechanical failure and faster depreciation. This can result in higher interest rates or shorter available loan terms.

Current Interest Rate Environment

Beyond your personal financial situation, broader economic conditions play a role. When the Federal Reserve raises or lowers interest rates, it can influence the rates offered on car loans. Staying aware of the general economic climate can help you anticipate rate trends.

6. Common Pitfalls and How to Avoid Them

Even with the best intentions, car buyers can fall into traps that cost them money or lead to regret. Being aware of these common mistakes is your best defense.

Focusing Only on Monthly Payments

This is perhaps the most prevalent pitfall. While a low monthly payment might seem appealing, it often comes at the cost of a longer loan term and significantly more interest paid over time. Always consider the total cost of the loan, not just the monthly figure.

Not Shopping Around for Rates

Accepting the first financing offer, especially from a dealership, can be an expensive mistake. As highlighted earlier, getting pre-approved and comparing offers from multiple lenders is crucial. This competitive bidding ensures you’re getting the best possible rate available to you.

Adding Unnecessary Extras

Dealerships often push add-ons like extended warranties, paint protection, and GAP insurance (Guaranteed Asset Protection). While some of these can be valuable, others might be overpriced or unnecessary for your situation. Evaluate each add-on carefully and negotiate their prices separately, or consider purchasing them from third parties for less.

Lying on Your Application

Providing false information on your loan application is a serious offense. It can lead to immediate loan denial, and if discovered later, could result in your loan being revoked or even legal consequences. Always be truthful and accurate in your financial disclosures.

Ignoring the Fine Print

Loan agreements are legal documents. It’s imperative to read and understand every clause, even the small print. Look for details about:

-

Prepayment penalties: Fees charged if you pay off your loan early.

-

Late payment fees: What happens if you miss a payment.

-

Acceleration clauses: Conditions under which the lender can demand full payment immediately.

-

Common mistakes to avoid are: Signing any document you haven’t fully read and understood. Don’t let pressure from a salesperson rush you. Take your time.

7. Strategies for Securing the Best Car Loan Deal

Now that you’re armed with knowledge about the process and potential pitfalls, let’s refine your strategy for landing the most advantageous car loan.

Boost Your Credit Score

Prioritize improving your credit score months before you plan to buy a car. Pay all bills on time, reduce existing debt, and avoid opening new credit accounts. Even a 20-point increase can lead to a better interest rate.

Save for a Larger Down Payment

The more you put down upfront, the less you borrow, and the lower your interest payments will be. A substantial down payment also gives you equity in the car from day one, reducing the risk of being "upside down" (owing more than the car is worth).

Negotiate the Car Price Separately

Always negotiate the purchase price of the car before you discuss financing. If you combine these negotiations, it’s easier for dealerships to shuffle numbers around and confuse you about where you’re getting a "deal." Get the best car price first, then focus on the best loan.

Consider a Shorter Loan Term

If your budget allows for higher monthly payments, opt for a shorter loan term. You’ll pay significantly less interest over the life of the loan and own your car outright much faster. This also reduces your exposure to depreciation.

Shop Rates Aggressively

As emphasized, compare offers from banks, credit unions, and online lenders before considering dealership financing. Use your pre-approved offer as leverage to ensure the dealer matches or beats it. This is your most powerful negotiating tool.

Know Your Value

If you have a trade-in vehicle, research its fair market value using online tools. Don’t let the dealership lowball your trade-in. Similarly, know the true market value of the car you intend to buy to avoid overpaying.

- – A great resource for consumer protection information.

Conclusion

The journey to financing your next vehicle can feel complex, but with the right knowledge, it transforms into an empowering experience. By understanding the types of loans available, diligently preparing your finances, meticulously navigating the application process, and sidestepping common mistakes, you’re no longer a passive applicant but an informed negotiator.

You are now equipped with the expert insights needed to secure a car loan that not only gets you into your dream car but also aligns perfectly with your financial well-being. Drive smart, finance smart, and enjoy the open road ahead with the confidence that comes from making a truly informed decision.

Start your journey today by checking your credit, setting your budget, and securing that pre-approval. Your ideal car and the perfect loan are waiting!