Driving Your Dreams: The Ultimate Guide to Applying For a Car Loan with Bad Credit

Driving Your Dreams: The Ultimate Guide to Applying For a Car Loan with Bad Credit Carloan.Guidemechanic.com

Getting a car is often more than just a convenience; it’s a necessity for work, family, and daily life. But what happens when your credit score isn’t quite where you’d like it to be? The thought of applying for a car loan with bad credit can feel daunting, leading many to believe it’s an impossible feat. We’re here to tell you that it’s not only possible but, with the right strategy, entirely achievable.

Based on my extensive experience in the financial and automotive sectors, navigating the world of bad credit car loans requires a specific approach, a bit of preparation, and a lot of understanding. This comprehensive guide will walk you through every step, equipping you with the knowledge and confidence to secure the vehicle you need, even when your credit history has a few bumps in the road.

Driving Your Dreams: The Ultimate Guide to Applying For a Car Loan with Bad Credit

Understanding Bad Credit and Its Impact on Car Loans

Before we dive into solutions, let’s first clarify what "bad credit" truly means in the eyes of a lender and how it influences their decisions. Your credit score, primarily FICO and VantageScore, is a three-digit number that summarizes your financial reliability. It’s a snapshot of your past borrowing and repayment behavior.

Generally, a FICO score below 600-620 is considered "subprime" or "bad credit." This range signals to lenders that there might be a higher risk associated with lending you money. Common factors contributing to a low credit score include missed payments, high credit card utilization, bankruptcies, repossessions, and a short credit history.

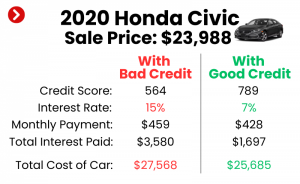

When you apply for a car loan with bad credit, lenders perceive a higher chance of default. To offset this increased risk, they typically offer less favorable terms. This usually translates into higher interest rates, which means you’ll pay significantly more over the life of the loan. You might also encounter stricter loan conditions, such as shorter repayment periods, requirements for a larger down payment, or the need for a co-signer.

It’s crucial to understand that while these terms might seem challenging, they are a lender’s way of managing risk. Your goal will be to mitigate that perceived risk as much as possible, making you a more attractive borrower despite your credit history.

Is a Car Loan with Bad Credit Even Possible? (The Good News)

Absolutely, getting a car loan with bad credit is not only possible but a common scenario for many individuals. The good news is that the lending landscape has evolved, and there are now numerous financial institutions and dealerships specializing in helping people with less-than-perfect credit. These are often referred to as "subprime lenders."

While the process might differ slightly from applying with excellent credit, the fundamental goal remains the same: to find a loan that fits your budget and helps you get on the road. The key is to approach this process with realistic expectations and a solid understanding of your financial situation. Don’t let past credit mistakes define your future mobility.

Many lenders recognize that life happens, and a low credit score doesn’t necessarily mean you’re irresponsible. It could be due to medical emergencies, job loss, or other unforeseen circumstances. Their focus is often on your current ability to repay the loan, not just your past performance.

Pre-Application Strategies: Laying the Groundwork for Success

Success in securing a car loan with bad credit hinges on thorough preparation. The more proactive steps you take before walking into a dealership or submitting an application, the stronger your position will be. This preparation demonstrates responsibility and minimizes the perceived risk to lenders.

1. Know Your Credit Score and Report Inside Out

This is your starting point. You can’t fix what you don’t understand. Begin by obtaining a copy of your credit report from all three major credit bureaus: Experian, Equifax, and TransUnion. You are legally entitled to a free report from each bureau once every 12 months via AnnualCreditReport.com.

Carefully review each report for any inaccuracies or errors. Mistakes on your credit report are surprisingly common and can negatively impact your score. If you find any discrepancies, dispute them immediately with the credit bureau. Correcting these errors can sometimes give your score a quick, much-needed boost.

Pro tip from us: Websites like Credit Karma or Credit Sesame offer free credit scores and monitoring, providing valuable insights into what’s affecting your score and how to improve it. While these aren’t always your official FICO scores, they offer a good general idea and help you track progress. Understanding your credit history is your most powerful tool.

2. Define Your Budget Realistically

Before you even think about car models, establish a firm budget. This isn’t just about the monthly car payment; it’s about the total cost of car ownership. Consider fuel costs, insurance premiums (which can be higher with bad credit and certain car types), maintenance, and potential repair expenses.

A common guideline is the 20/4/10 rule: a 20% down payment, a maximum 4-year loan term, and total car expenses (including insurance and fuel) not exceeding 10% of your gross monthly income. While the 20% down payment might be challenging with bad credit, aiming for a significant portion is wise. This comprehensive approach ensures you can comfortably afford the car without straining your finances, preventing future payment issues.

Overextending yourself on a car loan is a common mistake that can lead to further financial trouble. Be honest with yourself about what you can truly afford.

3. Save for a Substantial Down Payment

A down payment is one of the most effective ways to strengthen your application when you apply for a car loan with bad credit. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan term.

More importantly, a significant down payment signals to lenders that you are serious about the purchase and have some financial discipline. It demonstrates your commitment and reduces their risk. Even a 10-20% down payment can make a substantial difference in approval odds and interest rates.

If you don’t have a large sum saved, consider selling an existing, less reliable vehicle or waiting a few months to accumulate more funds. Every dollar you put down upfront works in your favor.

4. Consider a Co-signer

If your credit score is particularly low, or if you’re struggling to get approved, a co-signer can be a game-changer. A co-signer is someone with good credit who agrees to take on responsibility for the loan if you fail to make payments. This significantly reduces the lender’s risk, as they have a second, more creditworthy individual to pursue if you default.

Choosing a co-signer requires careful consideration. It should be someone you trust deeply and who understands the implications, such as a family member or close friend. Remember, if you miss payments, it will negatively impact their credit score as well, and they will be legally obligated to repay the debt.

While a co-signer can open doors, it’s a serious commitment for both parties. Ensure clear communication and a strong understanding of the responsibilities before proceeding.

5. Improve Your Credit Score (Even Slightly)

While you might need a car now, taking steps to improve your credit score, even incrementally, can yield better loan terms. Even a 20-30 point increase can sometimes shift you into a slightly better risk category.

Focus on these key actions:

- Pay all your bills on time: Payment history is the biggest factor in your credit score.

- Reduce existing debt: Lowering your credit utilization (the amount of credit you’re using versus your total available credit) can quickly boost your score.

- Avoid new credit applications: Each application can result in a hard inquiry, which temporarily dings your score. Limit these inquiries, especially in the months leading up to a car loan application.

Even small improvements can make a difference in the interest rate you’re offered. Every percentage point saved translates into hundreds, if not thousands, of dollars over the life of the loan.

Finding the Right Lender: Where to Apply For Car Loan Bad Credit

Not all lenders are created equal, especially when it comes to bad credit car loans. Knowing where to look can save you time, frustration, and money. It’s about finding lenders who specialize in your situation and are willing to work with you.

1. Subprime Lenders and Dealerships

Many dealerships have relationships with a network of subprime lenders who specialize in financing customers with bad credit. These "special finance" departments are designed precisely for this purpose. They understand the challenges and are often more flexible than traditional banks.

Be cautious with "Buy Here Pay Here" (BHPH) dealerships. While they often guarantee approval regardless of credit, their interest rates can be exceptionally high, and the vehicles might be older or less reliable. Payments are typically made directly to the dealership, not a bank. While they can be a last resort, explore other options first due to the potential for predatory terms.

Common mistakes to avoid are: Rushing into the first offer you receive from a dealership without comparing it to others. Always shop around.

2. Credit Unions

Credit unions are member-owned financial institutions that often have more flexible lending criteria than large banks. They prioritize their members’ financial well-being and might be more willing to work with individuals who have bad credit, especially if you have an existing relationship with them.

Their interest rates are often competitive, even for subprime loans, and they may offer personalized guidance. If you’re not already a member, consider joining one; membership requirements are often simple, such as living in a certain area or working for a specific employer.

3. Online Lenders and Lending Marketplaces

The digital age has brought forth numerous online lenders and lending marketplaces that specialize in bad credit car loans. These platforms allow you to pre-qualify with multiple lenders with a single application, often resulting in a "soft pull" on your credit that doesn’t impact your score.

This convenience allows you to compare offers from various lenders from the comfort of your home, giving you a clear picture of potential interest rates and terms. Some popular platforms include Capital One Auto Navigator, Carvana, and other specialized online auto lenders.

Pro tip from us: Pre-qualification is a great way to gauge your approval odds and potential rates without committing. It gives you negotiating power when you walk into a dealership.

The Application Process: What to Expect

Once you’ve done your homework and identified potential lenders, it’s time to formally apply. Being prepared for this step will make the process smoother and more efficient. Lenders want to verify your identity, your income, and your ability to repay the loan.

Required Documentation

Lenders will typically ask for a range of documents to verify your financial stability and identity. Having these ready will expedite the process:

- Proof of Income: Recent pay stubs (usually 2-3 months’ worth), bank statements showing direct deposits, tax returns if you’re self-employed.

- Proof of Residence: Utility bills (electricity, gas, water) with your current address, a lease agreement, or mortgage statements.

- Identification: A valid government-issued ID (driver’s license, state ID).

- References: Some lenders may request personal or professional references.

- Trade-in Information: If you’re trading in a vehicle, you’ll need its title or payoff information.

Be Honest and Transparent

When filling out the application, always be truthful and transparent about your financial situation. Attempting to hide information or misrepresent your income can lead to a denied application or even legal trouble down the line. Lenders have sophisticated systems to verify information, so honesty is always the best policy.

If you have a bankruptcy or repossession in your past, acknowledge it. Explain the circumstances if you can, focusing on how you’ve improved your financial habits since then.

Pre-qualification vs. Full Application

Many lenders offer a pre-qualification process. This is where you provide some basic information, and they give you an estimate of what you might be approved for, often with a soft credit inquiry. This is extremely valuable for understanding your options without affecting your credit score.

A full application, however, involves a "hard pull" on your credit, which will temporarily lower your score by a few points. Only proceed with a full application once you’re serious about a specific loan offer and vehicle. It’s wise to limit hard inquiries to a short window (typically 14-45 days) so they count as a single inquiry for scoring purposes if you’re rate shopping.

Negotiating Your Bad Credit Car Loan

Securing an approval is a significant step, but the work isn’t over. Negotiating the terms of your bad credit car loan is crucial to ensure you get the best possible deal and avoid overpaying. Remember, everything is negotiable.

Focus on the Total Cost, Not Just the Monthly Payment

Dealerships often try to focus buyers on the monthly payment, making a car seem more affordable. However, a lower monthly payment can sometimes be achieved by extending the loan term, meaning you pay more interest over time.

Always focus on the total cost of the loan, including the interest rate (APR) and the overall amount you’ll pay back. A slightly higher monthly payment over a shorter term can save you thousands in interest in the long run. Don’t be afraid to ask for a breakdown of all costs.

Beware of Add-ons

Dealerships often try to sell various add-ons, such as extended warranties, GAP insurance, paint protection, or VIN etching. While some of these might be valuable (like GAP insurance if you have a small down payment or a high loan-to-value ratio), many are unnecessary and simply inflate the total loan amount.

Scrutinize every add-on. Ask yourself if you truly need it and if the cost is justified. You can often purchase extended warranties or GAP insurance from third-party providers at a lower cost. If you don’t want an add-on, firmly say no.

Shop Around and Compare Offers

This is perhaps the most important negotiation tip, especially when you apply for a car loan with bad credit. Do not settle for the first offer you receive. Get pre-approvals from multiple lenders (credit unions, online lenders, and even different dealerships).

Having several offers in hand gives you leverage. You can use a better offer from one lender to negotiate a lower interest rate or better terms with another. Competition among lenders works in your favor.

Pro tips from us: Try to get pre-approved for financing before you even step foot on a dealership lot. This way, you know your financing options and can negotiate the car price separately, without the added pressure of simultaneously figuring out your loan. This approach splits the negotiation process into two distinct parts: the car price and the financing.

Post-Approval: Managing Your Loan and Rebuilding Credit

Congratulations, you’ve secured your bad credit car loan! This isn’t just about getting a car; it’s a golden opportunity to rebuild your credit and pave the way for a healthier financial future. Your actions now are more important than ever.

Make Payments On Time, Every Time

This cannot be stressed enough. Your car loan is a major credit account, and consistent, on-time payments are the single most effective way to improve your credit score. Each payment reported positively to the credit bureaus demonstrates your reliability and builds a strong payment history.

Set up automatic payments if possible, or mark your calendar with payment reminders. Missing even one payment can significantly set back your credit rebuilding efforts.

Common mistakes to avoid are: Assuming a few days late won’t matter. Late payments are typically reported to credit bureaus after 30 days and can have a severe negative impact.

Consider Refinancing When Your Credit Improves

As you consistently make on-time payments, your credit score will likely begin to improve. Once it reaches a healthier level (perhaps 6-12 months later), consider refinancing your car loan. Refinancing allows you to replace your current loan with a new one, ideally with a lower interest rate.

A lower interest rate means lower monthly payments and less money paid in interest over the life of the loan. This is a powerful strategy to save money and accelerate your credit rebuilding journey. Keep an eye on your credit score and explore refinancing options periodically.

Maintain Your Vehicle

While not directly related to your credit score, properly maintaining your vehicle is crucial for your financial stability. Unexpected breakdowns can lead to expensive repairs, which might strain your budget and potentially jeopardize your ability to make loan payments.

Regular oil changes, tire rotations, and addressing minor issues promptly can prevent major, costly problems down the road. A reliable car reduces stress and helps ensure you can get to work and maintain your income.

Conclusion: Driving Towards a Brighter Financial Future

Applying for a car loan with bad credit can feel like navigating a complex maze, but with the right guidance, it’s a journey you can successfully complete. Remember, having bad credit doesn’t define your future; it’s simply a reflection of your past. This process is not just about getting a car; it’s about taking proactive steps to improve your financial standing.

By understanding your credit, meticulously preparing your finances, strategically finding the right lenders, negotiating wisely, and diligently managing your loan, you’re not just buying a car – you’re building a foundation for a stronger financial future. Your new car loan can be a powerful tool for credit repair, opening doors to better financial opportunities down the road. Stay persistent, stay informed, and drive confidently towards your goals.