Driving Your Dreams: The Ultimate Guide to Getting a Car Loan With Fair Credit

Driving Your Dreams: The Ultimate Guide to Getting a Car Loan With Fair Credit Carloan.Guidemechanic.com

Securing a car loan can feel like navigating a complex maze, especially when your credit score falls into the "fair" category. You’re not quite in the excellent tier, but you’re certainly not in the subprime zone either. This unique position often leaves many prospective buyers wondering: "Can I truly get a good car loan with fair credit?"

The answer, unequivocally, is yes! Based on my extensive experience in automotive finance and consumer lending, fair credit doesn’t close the door on car ownership; it simply means you need a more strategic approach. This comprehensive guide is designed to empower you with the knowledge, tips, and strategies needed to not only get approved for a car loan but to secure one with favorable terms, even with fair credit.

Driving Your Dreams: The Ultimate Guide to Getting a Car Loan With Fair Credit

We’ll dive deep into understanding your credit, preparing your finances, exploring your lending options, and common pitfalls to avoid. By the end of this article, you’ll be well-equipped to drive off the lot with confidence.

Understanding "Fair Credit" and Its Impact on Car Loans

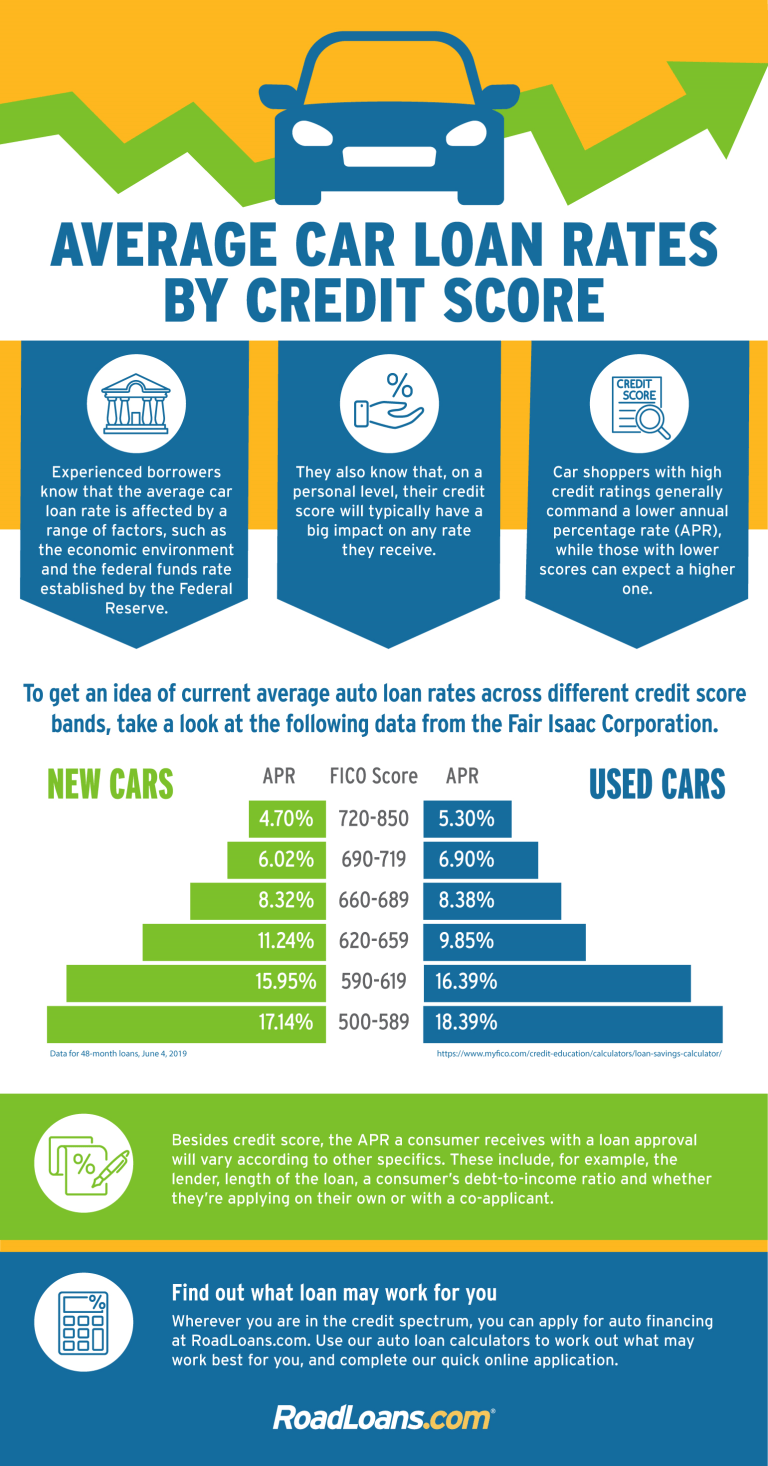

Before we delve into strategies, let’s clarify what "fair credit" actually means in the eyes of lenders. Credit scores, primarily FICO and VantageScore, typically range from 300 to 850. While the exact ranges can vary slightly by scoring model and lender, "fair credit" generally falls within the 580 to 669 range.

This score indicates that while you’ve likely made some payments on time, there might be a few late payments, higher credit utilization, or a shorter credit history that prevents you from reaching "good" or "excellent" status. Lenders view borrowers in this range as moderate risk. They’re not as risky as those with bad credit, but they’re not as low-risk as those with excellent credit.

Why Your Credit Score Matters for Auto Financing

Your credit score is a snapshot of your financial reliability. For car lenders, it’s a critical tool used to assess the likelihood of you repaying your loan. Here’s why it’s so important:

- Interest Rates: This is arguably the biggest impact. Borrowers with excellent credit scores typically qualify for the lowest interest rates, sometimes even 0% APR promotions. With fair credit, you’ll likely face higher interest rates. This is how lenders compensate for the perceived increased risk. A higher interest rate means you’ll pay more over the life of the loan.

- Loan Approval: While fair credit won’t automatically disqualify you, it can make approval more challenging than for someone with a higher score. Lenders might impose stricter conditions or require additional documentation.

- Loan Terms and Conditions: Beyond interest rates, your credit score can influence other loan terms. You might be offered a shorter loan term to reduce the lender’s risk, or you might be required to make a larger down payment.

It’s crucial to understand that even within the "fair" range, a score of 650 is generally viewed more favorably than a 590. Every point matters, so knowing your precise score is your first strategic step.

Preparing for Your Car Loan Journey: Laying the Groundwork

Success in securing a car loan with fair credit begins long before you step onto a dealership lot. Thorough preparation can significantly boost your chances of approval and help you land better terms.

1. Check Your Credit Report and Score

This is non-negotiable. Many people assume they know their credit standing, but details can be surprising.

- Access Your Reports: You are entitled to a free credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once a year. A trusted external source for this is AnnualCreditReport.com. This site allows you to access all three reports in one place.

- Review for Accuracy: Carefully examine each report for errors. Incorrect late payments, fraudulent accounts, or outdated information can unfairly drag down your score. Based on my experience, errors are more common than people think, and correcting them can quickly improve your score.

- Dispute Any Errors: If you find discrepancies, dispute them immediately with the relevant credit bureau. This process can take time, so start early. Removing inaccurate negative marks can significantly improve your credit standing.

- Know Your Score: Many credit card companies, banks, and online services now offer free access to your FICO or VantageScore. Knowing your exact score helps you understand where you stand and what rates you might expect.

2. Craft a Realistic Budget and Understand Your Debt-to-Income (DTI) Ratio

Lenders don’t just look at your credit score; they also want to ensure you can comfortably afford the monthly payments.

- Calculate Affordability: Before even looking at cars, determine how much you can truly afford each month without stretching your finances thin. Factor in not just the car payment, but also insurance, fuel, maintenance, and potential parking fees. Pro tip from us: Aim for your total car expenses (payment, insurance, gas) to be no more than 10-15% of your take-home pay.

- Understand DTI: Your debt-to-income ratio (DTI) is another critical metric. It’s the percentage of your gross monthly income that goes towards debt payments (rent/mortgage, credit cards, student loans, etc.). Lenders generally prefer a DTI below 36%, though some auto lenders may go higher. A lower DTI indicates you have more disposable income to manage new debt. If you’re looking to understand more about improving your credit score or managing debt, check out our comprehensive guide on How to Improve Your Credit Score Fast.

3. Save for a Significant Down Payment

This is one of the most powerful tools you have when seeking a car loan with fair credit.

- Reduce Lender Risk: A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. This can make them more willing to approve your loan and potentially offer a better interest rate.

- Lower Monthly Payments: A larger down payment also translates to lower monthly payments, making the loan more affordable for you.

- Avoid Being Upside Down: Putting down a substantial amount helps prevent you from owing more on the car than it’s worth (being "upside down" or having negative equity), especially in the early years of ownership when depreciation is highest. Based on my experience, aiming for at least 10-20% down on a used car and 20% or more on a new car is a strong strategy.

4. Consider a Co-signer

If you have a trusted friend or family member with excellent credit, asking them to co-sign your loan can be a game-changer.

- Leverage Stronger Credit: A co-signer’s strong credit profile essentially acts as a guarantee for the lender. If you default, they are legally responsible for the payments. This significantly reduces the lender’s risk.

- Better Terms: With a co-signer, you’re much more likely to qualify for better interest rates and more favorable loan terms than you would on your own.

- Important Note: This is a serious commitment for the co-signer. Ensure both parties understand the full implications and have a clear agreement in place. It can impact their credit if you miss payments.

Strategies to Improve Your Chances of Approval (Even with Fair Credit)

Beyond preparing your finances, there are specific strategies you can employ during the loan application process itself to increase your likelihood of approval and secure better terms.

1. Shop Around for Pre-Approval from Multiple Lenders

This is a critical step that many car buyers overlook, often going straight to dealership financing.

- Empower Yourself: Getting pre-approved from banks, credit unions, and online lenders before visiting a dealership puts you in a much stronger negotiating position. You’ll know exactly what interest rate and terms you qualify for.

- "Shopping" for Rates: Unlike applying for multiple credit cards, applying for multiple car loans within a short window (typically 14-45 days, depending on the scoring model) will usually only count as a single hard inquiry on your credit report. This allows you to compare offers without negatively impacting your score multiple times.

- Different Lender Types:

- Banks: Offer competitive rates, especially if you’re an existing customer.

- Credit Unions: Often have more flexible lending criteria and can offer lower rates to members, especially for those with fair credit. They are member-focused, not profit-focused.

- Online Lenders: Many specialize in borrowers across the credit spectrum, including fair credit. They often have quick application processes.

- Dealership Financing: While convenient, dealers often act as intermediaries, marking up interest rates offered by their partner lenders. However, they can also sometimes find specific programs for various credit tiers.

Pro tips from us: Always get at least three pre-approvals from different types of lenders. This gives you a baseline to compare against any offers from the dealership.

2. Focus on a More Affordable and Reliable Vehicle

While it’s tempting to aim for your dream car, being realistic is key when you have fair credit.

- Reduce Loan Amount: Opting for a more affordable car means you need to borrow less. This reduces the lender’s risk and increases your chances of approval.

- New vs. Used: New cars depreciate rapidly, and often come with higher price tags. A reliable used car can be a smart choice, requiring a smaller loan and potentially lower insurance costs.

- Reliability Matters: Lenders might look more favorably on loans for reliable, well-maintained vehicles. They want to ensure the collateral (the car) holds its value.

Common mistakes to avoid are falling in love with a car outside your budget. Stick to what you’ve budgeted for and remember that this car can be a stepping stone to better credit and, eventually, that dream car. For a deeper dive into budgeting for a major purchase like a car, read our article on Mastering Your Personal Budget.

3. Consider a Shorter Loan Term

While longer loan terms mean lower monthly payments, they also mean more interest paid over time and higher overall cost.

- Less Interest Paid: A shorter term (e.g., 36 or 48 months instead of 60 or 72) means you pay off the loan faster and accrue less interest.

- Reduced Risk for Lender: From the lender’s perspective, a shorter term means their money is tied up for less time, reducing their risk. This can make them more willing to approve your loan.

- Higher Monthly Payment: Be aware that shorter terms come with higher monthly payments. Ensure your budget can comfortably handle this. If it’s a stretch, it might be better to opt for a slightly longer term that you can reliably pay.

4. Leverage Your Trade-in Value

If you have an existing vehicle, using its trade-in value is similar to making a down payment.

- Boost Equity: The value of your trade-in directly reduces the amount you need to borrow, improving your loan-to-value (LTV) ratio. A lower LTV is attractive to lenders.

- Research Value: Before heading to the dealership, research your car’s trade-in value using resources like Kelley Blue Book (KBB) or Edmunds. This will help you negotiate fairly.

The Application Process: Navigating the Final Steps

Once you’ve done your homework and are ready to apply, understanding the process and what to expect can ease anxieties and prevent missteps.

1. Gather All Necessary Documents

Being prepared with all required paperwork will streamline the application process.

- Personal Identification: Driver’s license, passport, or state ID.

- Proof of Income: Recent pay stubs (1-2 months), W-2 forms, or tax returns if self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Insurance: You’ll need valid car insurance before driving off the lot.

- Trade-in Information (if applicable): Title, registration, and loan payoff amount.

Having these documents ready demonstrates your seriousness and ability to follow through.

2. Understand the Loan Offer

Don’t just look at the monthly payment. Dive deep into all aspects of the loan offer.

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and any fees. Compare APRs from different lenders, not just interest rates.

- Loan Term: How many months will you be paying? As discussed, shorter terms generally mean less interest.

- Total Loan Cost: Calculate the total amount you will pay over the life of the loan (principal + interest).

- Fees: Look out for any origination fees, documentation fees, or prepayment penalties.

- Read the Fine Print: Never sign anything you don’t fully understand. Ask questions until you’re completely clear on all terms and conditions.

3. Negotiate (If Possible)

With pre-approvals in hand, you have leverage.

- Use Your Best Offer: Present your best pre-approval offer to the dealership and see if they can beat it. Dealerships often have access to various lenders and might be able to find a more competitive rate, especially if they want to make the sale.

- Negotiate Price Separately: Try to negotiate the car’s purchase price before discussing financing. This prevents the dealer from shifting numbers around between the car price and loan terms.

Common Mistakes to Avoid When Getting a Car Loan with Fair Credit

Even with the best intentions, certain pitfalls can derail your efforts. Being aware of these common mistakes can save you time, money, and frustration.

1. Applying to Too Many Lenders Indiscriminately

While shopping for rates is good, applying everywhere can hurt your credit.

- Multiple Hard Inquiries: Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your score. While multiple auto loan inquiries within a short period (rate shopping window) are typically grouped as one, spreading them out over weeks or months will result in multiple hits.

- Targeted Applications: Focus on lenders known to work with fair credit, and use your pre-approvals wisely.

2. Ignoring Your Credit Report and Score

As mentioned earlier, not knowing your credit situation is a major disadvantage.

- Surprises at the Dealership: Walking into a dealership without knowing your credit score leaves you vulnerable to whatever terms they present.

- Missed Opportunities: You might miss opportunities to correct errors or improve your score before applying.

3. Not Budgeting Realistically

Overestimating what you can afford is a recipe for financial stress.

- Payment Shock: Focusing solely on a low monthly payment without considering the total cost, insurance, and maintenance can lead to payment shock.

- Risk of Default: If the payments are too high, you risk missing them, which severely damages your credit and could lead to repossession.

4. Focusing Only on the Monthly Payment

While important, the monthly payment is just one piece of the puzzle.

- Extended Terms, More Interest: Lenders might offer very low monthly payments by stretching the loan term to 72 or even 84 months. This significantly increases the total interest you pay over time.

- Negative Equity: Longer terms also mean it takes longer to build equity in the car, increasing the chances of being upside down on your loan.

5. Buying More Car Than You Can Afford

The temptation for a fancier, more expensive car is strong, but resist it.

- Higher Payments, Higher Insurance: An expensive car comes with higher payments, higher insurance premiums, and often higher maintenance costs.

- Financial Strain: Don’t let a car purchase put undue strain on your overall financial health. This purchase should enhance, not hinder, your financial stability.

Post-Approval: Driving Off and Building Better Credit

Congratulations! You’ve secured your car loan. But the journey doesn’t end there. This is a prime opportunity to use your new loan to improve your credit standing for future financial endeavors.

1. Make All Payments On Time, Every Time

This is the single most important action you can take.

- Payment History is Key: Your payment history accounts for 35% of your FICO score. Consistent on-time payments will gradually and significantly boost your credit score.

- Set Reminders: Use automatic payments, calendar reminders, or payment alerts to ensure you never miss a due date.

2. Consider Refinancing Down the Road

As your credit score improves, you might qualify for better terms.

- Lower Interest Rates: After 6-12 months of on-time payments, your credit score could rise. At that point, explore refinancing your car loan for a lower interest rate, which will reduce your monthly payment or the total interest paid over the remaining term.

- Shop Around Again: Just like with your initial loan, shop around with multiple lenders for the best refinancing offers.

By responsibly managing your car loan, you’re not just paying for a vehicle; you’re actively building a stronger financial future.

Conclusion: Your Road to Car Ownership with Fair Credit

Securing a car loan with fair credit is not just possible; it’s an achievable goal with the right approach. It demands diligence, strategic planning, and a deep understanding of your financial landscape. By checking your credit, budgeting wisely, saving for a down payment, and proactively shopping for the best loan terms, you can transform a challenging situation into a successful outcome.

Remember, this car loan is more than just transportation; it’s an opportunity to demonstrate your financial responsibility and improve your credit score. Embrace the journey, make informed decisions, and soon you’ll be driving towards a brighter financial future, one on-time payment at a time. Your dream car might be closer than you think, even with fair credit.